|

시장보고서

상품코드

1906978

시설 관리 시장 : 시장 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)Facility Management - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

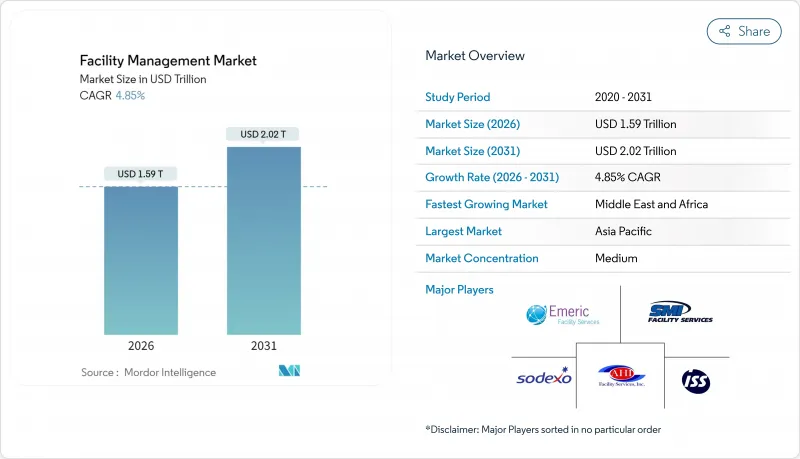

시설 관리 시장 규모는 2026년 1조 5,900억 달러로 추정되고, 2025년 1조 5,170억 달러부터 성장을 계속하고 있습니다. 2031년까지 2조 200억 달러에 이를 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR) 4.85%로 확대될 것으로 전망됩니다.

이러한 성장세는 시설 관리가 단순한 지원 비용에서 비즈니스 회복력, 디지털 통합, 직원 생산성 향상을 위한 전략적 수단으로 자리매김이 변화하고 있음을 반영합니다. 아웃소싱 수요 증가, 사이버 보안 사고에도 불구하고 진행되는 클라우드 마이그레이션 가속화, ESG 요구사항의 꾸준한 보급이 결합되어 대응 가능한 수요를 확대하고 있습니다. 신흥 시장, 특히 아시아태평양의 인프라 투자 증가는 시설 관리 시장의 여러 지역에 걸친 확대주기를 강화하고 있습니다. 기술 플랫폼과 성과 기반 모델을 융합하는 공급자는 투명한 비용 관리와 측정 가능한 효율성을 요구하는 고객으로부터 높은 부가가치 계약을 획득했습니다.

세계의 시설 관리 시장 동향 및 인사이트

비중핵 업무의 아웃소싱에 대한 관심 증가

기업은 시설 관리 업무를 전문 파트너로 이관함으로써 핵심적 혁신에 자본을 집중시키고 있습니다. 2024년에는 35%의 기업이 운영 복잡성을 억제하기 위해 FM 예산을 증가시키고 있습니다. 시설 관리 시장은 공급망의 혼란을 흡수하고 다양한 노동력을 제공할 수 있는 규모의 경제 효과의 혜택을 받고 있습니다. 수요는 기술 및 헬스케어 분야에서 두드러지며 CBRE의 2025년 1분기 시설 계약에서 순수익 16% 증가를 지원했습니다. 이 기법은 공급업체 위험을 줄이는 데에도 기여하며(29%의 기업이 혼란 우려를 표명), 강화된 물류체제를 가진 FM 파트너에 대한 선호를 촉진하고 있습니다. 아웃소싱량이 증가하는 동안 공급자는 이익률 향상을 자동화, 예측 분석, 직원 기술 향상에 재투자하고 있으며, 시설 관리 시장 전반에 걸쳐 순환적인 성장주기를 강화하고 있습니다.

IoT를 활용한 예지보전에 의한 시설의 디지털화

예측보전 플랫폼은 2025년 55억 달러 규모에 이르렀으며, 연간 17%의 성장률로 사후 대응형 수리에서 상태 모니터링형 관리로의 구조적 전환을 지원합니다. 의료 분야의 도입 사례에서는 자동화된 작업 지시서 생성에 의해 시설 비용을 10-15% 삭감한 것으로 보고되었습니다. 소프트웨어 계층(지출의 44%를 차지함)은 사전 학습된 알고리즘을 패키징하고 시설 관리 시장 내 중간 규모 시설에 대한 액세스를 민주화합니다. 산업 플랜트에 있어서의 초기 파일럿에서는 폐열 회수 속도가 25% 향상되어, 구체적인 ESG 효과를 실증했습니다. 이상 감지 모델의 성숙에 따라 데이터 요건이 축소되어 풍부한 이력 로그가 없어도 소규모 자산이 참가 가능하게 됩니다. 이에 따라 지역을 넘은 시장 침투가 확대되고 있습니다.

시설 관리 업무에서의 임금 상승

시설 관리 업무의 평균 시급은 2024년에 4.1% 상승했으며, 중앙값은 21.74달러에 달했습니다. 이에 따라 노동집약형 계약의 이익률이 압박되고 있습니다. 특히 공조설비(HVAC)와 전기공사 등의 기술직 부족이 입찰 경쟁을 격화시키고 있으며, 코넬대학의 시설 관리 노동자 파업과 같은 사례는 노동 조합 활동의 활성화를 돋보이게 하고 있습니다. 숨겨진 계약 수수료와 백엔드 추가 요금이 예산을 더욱 압박하고, 구매 담당자는 아웃소싱의 경제성을 재검토할 수밖에 없습니다. 이에 반해 프로바이더는 로봇 기술 및 자율 청소 시스템의 도입을 가속화하고 있지만 초기 투자 및 재훈련의 필요성이 시설 관리 시장 전체에 있어서 단기적인 도입을 방해하고 있습니다.

부문 분석

하드 서비스는 자산 보전을 목적으로 하는 기계, 전기 및 배관(MEP) 설비의 의무적 보수에 힘입어 2025년 시설 관리 시장 규모의 58.65%를 차지했습니다. 규제 기준 및 자산의 복잡화가 진행되고 있는 가운데, 인증 기술자 수요가 안정적으로 증가하고 있습니다. 예측 기간 동안 고객이 통합된 체험 관리를 요구하는 경향이 강해져 소프트 서비스와의 융합이 진전될 전망입니다. 이것은 통합 벤더에게 크로스셀링 기회를 창출합니다.

소프트 서비스는 규모가 작은 반면, 위생, 보안 및 거주자 복지에 대한 관심의 고조를 반영해, 6.05%의 연평균 복합 성장률(CAGR)로 성장을 가속하고 있습니다. 청소 계약에는 항균 프로토콜과 로봇 청소기가 포함되어 보안 분야에서는 AI 영상 분석으로의 이행이 진행됩니다. ESG 평가 기준이 실내 공기 품질과 케이터링의 지속가능성까지 확대되는 가운데, 소프트 서비스는 경영진 수준의 인지도를 높이고 있습니다. 하드 데이터와 소프트 데이터를 융합하는 공급자는 예방 보전 일정을 적극적으로 조정할 수 있어 구체적인 운영상의 이익을 창출하는 동시에 시설 관리 시장에서 월렛 점유율을 확대합니다.

2025년 시점에서 책임의 위치를 명확히 하는 통합형 FM(IFM) 계약을 기반으로 사내 관리 모델이 시설 관리 시장 점유율의 53.20%를 차지했습니다. 여러 거점 기업은 단일 송장의 투명성을 평가하고 도입을 추진하고 있습니다. 동시에 사이버 보안에 민감한 업계가 중요 관리 기능을 유지하는 중 아웃소싱 FM은 CAGR 5.71%로 확대됩니다. 하이브리드 구조가 보급되고 전략적 계획은 사내에 남아있는 동안 현장 실행을 파트너에게 이전함으로써 유연성과 위험의 균형을 맞추고 있습니다.

IFM의 범위가 확대되는 가운데 벤더는 위치별 서비스 제공 비용을 가시화하는 분석 포털을 통합하여 데이터 중심의 계약 갱신을 가능하게 하고 있습니다. 단일 서비스 옵션은 고객이 종합적인 가치 제안을 요구함에 따라 쇠퇴하고 중소 계약자는 합병 및 전문 분야에 대한 전문화를 강요합니다. CBRE에 의한 16억 달러 규모의 인더스트리우스 인수는 시설 관리, 접객, 공간 분석을 통합한 체험형 구독 서비스에 대한 전략적 재편을 강조하고 시설 관리 시장의 경쟁 구도를 재정의합니다.

지역별 분석

아시아태평양은 2025년에 시설 관리 시장의 41.10%를 차지하였고, 정부의 경기 자극책 및 도시로의 인구 이동에 지지되어, 6.05%의 연평균 복합 성장률(CAGR)로 확대가 전망됩니다. 중국의 51조 4,000억 달러 규모의 고정 자산 투자(인프라 투자 5.9% 증가 포함)가 장기적인 서비스 수요를 지원합니다. 인도의 상업용 부동산 급증은 원격 감시 수요를 불러일으키며, 아세안의 스마트 시티 계획에서는 FM 계약이 마스터 플랜 단계에서 통합되었습니다. 지역 특화형 공급망과 다국어 플랫폼을 구축하는 사업자는 선행자 우위를 획득할 것입니다.

북미는 성숙하면서도 혁신적인 시장 환경을 유지하고 있으며, 클라우드 보급과 ESG 컴플라이언스가 프리미엄 요금을 견인하고 있습니다. 이 지역의 시설 관리 시장은 노동력 부족에 직면하여 자동화 도입을 촉진하고 있습니다. 에너지 최적화의 의무화 및 인플레이션 억제법에 의한 인센티브로 FM 전문가의 개수가 촉진되고 있습니다. 유럽도 마찬가지로 디지털화가 진행되고 있습니다만, EPBD 등의 엄격한 탄소 규제가 특징이며, 계약은 실적 연동형 보상으로 이행하고 있습니다. 범유럽 벤더는 국경을 넘은 거버넌스의 틀을 활용하여 서비스 품질의 표준화를 도모하고 있습니다.

중동 및 아프리카에서는 교통, 의료, 교육 인프라에서 관민 협력을 통해 도입이 가속화되고 있습니다. 걸프 협력 회의(GCC)의 메가 프로젝트에서는 설계 단계부터 시설 관리(FM) 규정이 통합되어 라이프사이클의 가치가 정착되어 있습니다. 남미에서는 물류 및 제조업이 확대됨에 따라 안정적인 수요를 볼 수 있지만 통화 변동으로 인해 유연한 가격 설정이 필요합니다. 모든 신흥지역에서 공급업체의 분산화가 진행됨에 따라 통합의 움직임이 촉진되고 합병 통합에 뛰어난 세계의 대기업에 있어서 시설 관리 시장이 확대되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 서포트

자주 묻는 질문

목차

제1장 서론

- 조사의 전제조건 및 시장 정의

- 조사 범위

제2장 조사 방법

제3장 주요 요약

제4장 시장 상황

- 시장 개요

- 시장 성장 촉진요인

- 비중핵 업무의 아웃소싱에 대한 중시 고조

- IoT를 활용한 예지보전에 의한 시설 디지털화

- 지속가능성 및 ESG 연동형 FM 계약

- 팬데믹 후의 하이브리드형 직장 재설계의 필요성

- 신흥 시장에서의 관민 제휴 인프라 계획

- AI 주도의 에너지 최적화 요건

- 시장 성장 억제요인

- 관리 업무에서의 임금 상승

- 신흥 시장에서의 벤더 기반 분산화

- 클라우드 기반 FM 플랫폼의 사이버 보안 위험

- 중소기업에서 IFM 플랫폼의 자본 고정화

- 밸류체인 분석

- 규제 상황

- 기술 전망

- Porter's Five Forces 분석

- 공급기업의 협상력

- 구매자의 협상력

- 신규 참가업체의 위협

- 대체품의 위협

- 경쟁 기업 간 경쟁 관계

- 가격 분석

- 시장의 거시 경제 동향 평가

제5장 시장 규모 및 성장 예측

- 서비스 유형별

- 하드 서비스

- 자산 운용

- MEP 및 HVAC

- 방화 및 안전 대책

- 기타 하드 서비스

- 소프트 서비스

- 청소

- 보안 및 사무실 지원

- 케이터링

- 기타 소프트 서비스

- 하드 서비스

- 제공 형태별

- 사내

- 외부 위탁

- 단일 서비스 FM

- 번들 FM

- 통합 시설 관리(IFM)

- 전개 모드별

- 온프레미스

- 클라우드 기반

- 기업 규모별

- 대기업

- 중소기업(SME)

- 최종 사용자 업계별

- 상업시설(IT 및 통신, 소매, 창고)

- 접객(호텔, 레스토랑)

- 공공기관 및 공공 인프라

- 헬스케어

- 산업 및 프로세스

- 주택 및 레저

- 지역별

- 북미

- 미국

- 캐나다

- 멕시코

- 유럽

- 영국

- 독일

- 프랑스

- 이탈리아

- 스페인

- 베네룩스(벨기에, 네덜란드, 룩셈부르크)

- 북유럽 국가(스웨덴, 노르웨이, 덴마크, 핀란드)

- 폴란드

- 러시아

- 기타 유럽

- 아시아태평양

- 중국

- 인도

- 일본

- 한국

- 호주 및 뉴질랜드

- 기타 아시아태평양

- 남미

- 브라질

- 아르헨티나

- 콜롬비아

- 칠레

- 기타 남미

- 중동 및 아프리카

- 중동

- GCC(사우디아라비아, 아랍에미리트(UAE), 카타르, 오만, 쿠웨이트, 바레인)

- 튀르키예

- 기타 중동

- 아프리카

- 남아프리카

- 나이지리아

- 이집트

- 케냐

- 기타 아프리카

- 중동

- 북미

제6장 경쟁 구도

- 시장 집중도

- 전략적 동향

- 시장 점유율 분석

- 기업 프로파일

- CBRE Group Inc.

- Cushman and Wakefield plc

- JLL(Jones Lang LaSalle Inc.)

- ISS A/S

- Sodexo SA

- Compass Group plc

- Emeric Facility Services

- SMI Facility Services

- AHI Facility Services Inc.

- Aramark Corporation

- ABM Industries Inc.

- G4S Limited

- Atalian Global Services

- Vinci Facilities(VINCI SA)

- EMCOR Group Inc.

- Comfort Systems USA

- Balfour Beatty-Workplace

- Serco Group plc

- Reliance Facilities(India)

- Sinopec Engineering FM(China)

- Unispace Global

제7장 시장 기회 및 장래 전망

AJY 26.01.26facility management market size in 2026 is estimated at USD 1.59 trillion, growing from 2025 value of USD 1.517 trillion with 2031 projections showing USD 2.02 trillion, growing at 4.85% CAGR over 2026-2031.

Growth momentum reflects the repositioning of facility management from a support cost to a strategic lever for operational resilience, digital integration, and employee productivity. Heightened outsourcing appetite, rapid cloud migration despite cybersecurity incidents, and the steady pull of ESG mandates are collectively widening addressable demand. Rising infrastructure spending in emerging markets, particularly Asia-Pacific, is reinforcing a multi-regional expansion cycle for the facility management market. Providers that blend technology platforms with outcome-based models are capturing premium contracts as clients seek transparent cost control and measurable efficiency.

Global Facility Management Market Trends and Insights

Growing emphasis on outsourcing non-core operations

Corporations are channeling capital toward core innovation by transferring facilities responsibilities to specialist partners, with 35% of enterprises boosting FM budgets in 2024 to curb operational complexity. The facility management market is benefiting from scale effects that let providers absorb supply-chain shocks and provide diversified labor pools. Demand is pronounced in technology and healthcare, supporting CBRE's 16% net revenue rise from facilities contracts during Q1 2025. The practice also mitigates supplier-risk exposure-29% of firms flagged disruption fears-fueling preference for FM partners with fortified logistics. As outsourcing volume mounts, providers are reinvesting margin gains into automation, predictive analytics, and workforce upskilling, reinforcing a virtuous growth cycle across the facility management market.

Facility digitisation via IoT-enabled predictive maintenance

Predictive maintenance platforms worth USD 5.5 billion in 2025 and expanding 17% annually underpin a structural shift from reactive repairs to condition-based care. Healthcare adopters report 10-15% facility cost savings through automated work-order generation. The software layer-44% of spend-packages pre-trained algorithms that democratize access for midsize sites inside the facility management market. Early pilots in industrial plants reveal 25% faster waste-heat recovery, highlighting tangible ESG payoffs. As anomaly-detection models mature, data prerequisites shrink, enabling smaller assets to participate without dense historical logs, thereby broadening market penetration across geographies.

High wage inflation in custodial labour

Average hourly earnings in facilities support soared 4.1% in 2024, lifting median pay to USD 21.74 and compressing margins for labour-intensive contracts. Skilled-trade shortages, especially HVAC and electrical, intensify bidding wars, while events such as Cornell University's facilities-worker strike underscore rising union activism. Hidden contract fees and backend surcharges further strain budgets, pushing buyers to reconsider outsourcing economics. Providers respond by accelerating robotics and autonomous-cleaning pilots, but up-front capital and retraining requirements weigh on near-term adoption across the facility management market.

Other drivers and restraints analyzed in the detailed report include:

- Sustainability and ESG-linked FM contracting

- Post-pandemic hybrid workplace re-design needs

- Fragmented vendor base in emerging markets

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hard Services generated 58.65% of the facility management market size in 2025, buoyed by mandatory mechanical, electrical, and plumbing (MEP) maintenance that safeguards asset integrity. Regulatory codes and rising asset complexity necessitate certified technicians, reinforcing demand stability. Over the forecast horizon, convergence with Soft Services will intensify as clients seek unified experience management, creating cross-selling avenues for integrated vendors.

Soft Services, though smaller, accelerate at a 6.05% CAGR, reflecting heightened focus on hygiene, security, and occupant well-being. Cleaning contracts embed anti-microbial protocols and robotic vacuums, while security shifts toward AI video analytics. As ESG scorecards widen to include indoor air and catering sustainability, Soft Services gain board-level visibility. Providers that fuse Hard and Soft data streams can proactively adjust preventive schedules, creating tangible operational gains and broadening wallet share within the facility management market.

In-house models held 53.20% of the facility management market share in 2025, underpinned by integrated FM (IFM) contracts that streamline accountability. Multisite firms appreciate single-invoice transparency, propelling uptake. Simultaneously, Outsourcing FM expands 5.71% CAGR as cyber-sensitive industries retain critical controls. Hybrid structures are proliferating: strategic planning stays internal, while field execution shifts to partners, balancing flexibility and risk.

As IFM scope widens, vendors embed analytics portals that surface cost-to-serve by location, enabling data-driven renewals. Single-service options erode as clients insist on total-value propositions, nudging smaller contractors toward mergers or specialisation niches. CBRE's USD 1.6 billion Industrious acquisition underscores strategic re-positioning toward experiential subscriptions that bundle facilities, hospitality, and space analytics, thereby redefining competitive contours of the facility management market.

The Facility Management Market Report is Segmented by Service Type (Hard Services, and Soft Services), Offering Type (In-House, and Outsourced), Deployment Model (On-Premise, and Cloud-Based), Organisation Size (Large Enterprises, and Small and Medium Enterprises), End-User Industry (Commercial, Hospitality, Institutional, Healthcare, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific accounted for 41.10% of the facility management market in 2025 and is set to expand at a 6.05% CAGR, sustained by government stimulus and urban migration. China's USD 51.4 trillion fixed-asset push, including 5.9% growth in infrastructure placements, underpins long-run service pipelines. India's commercial real estate surge adds demand for remote monitoring, while ASEAN smart-city programs embed FM contracts into master planning stages. Providers scaling localized supply chains and multilingual platforms will gain early-mover advantage.

North America maintains a mature yet innovative landscape where cloud penetration and ESG compliance drive premium fees. The facility management market in the region contends with tight labor pools, spurring automation adoption. Energy-optimisation mandates and the Inflation Reduction Act's incentives incentivize retrofits managed by FM specialists. Europe exhibits similar digital sophistication but is distinguished by stringent carbon regulations such as EPBD, steering contracts toward performance-linked remuneration. Pan-European vendors leverage cross-border governance frameworks to standardise service quality.

The Middle East and Africa witness accelerating adoption through public-private partnerships in transport, healthcare, and education infrastructure. Gulf Cooperation Council megaprojects integrate FM provisions from the design stage, anchoring lifecycle value. South America experiences steady demand tied to logistics and manufacturing expansion, though currency volatility necessitates flexible pricing. Across all emerging regions, fragmented supplier landscapes encourage consolidation plays, broadening the facility management market for global majors adept at merger integration.

- CBRE Group Inc.

- Cushman and Wakefield plc

- JLL (Jones Lang LaSalle Inc.)

- ISS A/S

- Sodexo SA

- Compass Group plc

- Emeric Facility Services

- SMI Facility Services

- AHI Facility Services Inc.

- Aramark Corporation

- ABM Industries Inc.

- G4S Limited

- Atalian Global Services

- Vinci Facilities (VINCI SA)

- EMCOR Group Inc.

- Comfort Systems USA

- Balfour Beatty - Workplace

- Serco Group plc

- Reliance Facilities (India)

- Sinopec Engineering FM (China)

- Unispace Global

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing emphasis on outsourcing non-core operations

- 4.2.2 Facility digitisation via IoT-enabled predictive maintenance

- 4.2.3 Sustainability and ESG-linked FM contracting

- 4.2.4 Post-pandemic hybrid workplace re-design needs

- 4.2.5 Public-private infrastructure pipelines in EMs

- 4.2.6 AI-led energy optimisation mandates

- 4.3 Market Restraints

- 4.3.1 High wage inflation in custodial labour

- 4.3.2 Fragmented vendor base in emerging markets

- 4.3.3 Cyber-security risk in cloud-based FM platforms

- 4.3.4 Capital lock-in for IFM platforms among SMEs

- 4.4 Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Assessment of Macro Economic Trends on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUES)

- 5.1 By Service Type

- 5.1.1 Hard Services

- 5.1.1.1 Asset Management

- 5.1.1.2 MEP and HVAC

- 5.1.1.3 Fire and Safety

- 5.1.1.4 Other Hard Services

- 5.1.2 Soft Services

- 5.1.2.1 Cleaning

- 5.1.2.2 Security and Office Support

- 5.1.2.3 Catering

- 5.1.2.4 Other Soft Services

- 5.1.1 Hard Services

- 5.2 By Offering Type

- 5.2.1 In-house

- 5.2.2 Outsourced

- 5.2.2.1 Single-service FM

- 5.2.2.2 Bundled FM

- 5.2.2.3 Integrated FM (IFM)

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud-Based

- 5.4 By Organisation Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises (SMEs)

- 5.5 By End-User Industry

- 5.5.1 Commercial (IT/Telecom, Retail, Warehouses)

- 5.5.2 Hospitality (Hotels, Restaurants)

- 5.5.3 Institutional and Public Infrastructure

- 5.5.4 Healthcare

- 5.5.5 Industrial and Process

- 5.5.6 Residential and Leisure

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 Europe

- 5.6.2.1 United Kingdom

- 5.6.2.2 Germany

- 5.6.2.3 France

- 5.6.2.4 Italy

- 5.6.2.5 Spain

- 5.6.2.6 Benelux (Belgium, Netherlands, Luxembourg)

- 5.6.2.7 Nordics (Sweden, Norway, Denmark, Finland)

- 5.6.2.8 Poland

- 5.6.2.9 Russia

- 5.6.2.10 Rest of Europe

- 5.6.3 Asia-Pacific

- 5.6.3.1 China

- 5.6.3.2 India

- 5.6.3.3 Japan

- 5.6.3.4 South Korea

- 5.6.3.5 Australia and New Zealand

- 5.6.3.6 Rest of Asia-Pacific

- 5.6.4 South America

- 5.6.4.1 Brazil

- 5.6.4.2 Argentina

- 5.6.4.3 Colombia

- 5.6.4.4 Chile

- 5.6.4.5 Rest of South America

- 5.6.5 Middle East and Africa

- 5.6.5.1 Middle East

- 5.6.5.1.1 GCC (Saudi Arabia, UAE, Qatar, Oman, Kuwait, Bahrain)

- 5.6.5.1.2 Turkey

- 5.6.5.1.3 Rest of Middle East

- 5.6.5.2 Africa

- 5.6.5.2.1 South Africa

- 5.6.5.2.2 Nigeria

- 5.6.5.2.3 Egypt

- 5.6.5.2.4 Kenya

- 5.6.5.2.5 Rest of Africa

- 5.6.5.1 Middle East

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 CBRE Group Inc.

- 6.4.2 Cushman and Wakefield plc

- 6.4.3 JLL (Jones Lang LaSalle Inc.)

- 6.4.4 ISS A/S

- 6.4.5 Sodexo SA

- 6.4.6 Compass Group plc

- 6.4.7 Emeric Facility Services

- 6.4.8 SMI Facility Services

- 6.4.9 AHI Facility Services Inc.

- 6.4.10 Aramark Corporation

- 6.4.11 ABM Industries Inc.

- 6.4.12 G4S Limited

- 6.4.13 Atalian Global Services

- 6.4.14 Vinci Facilities (VINCI SA)

- 6.4.15 EMCOR Group Inc.

- 6.4.16 Comfort Systems USA

- 6.4.17 Balfour Beatty - Workplace

- 6.4.18 Serco Group plc

- 6.4.19 Reliance Facilities (India)

- 6.4.20 Sinopec Engineering FM (China)

- 6.4.21 Unispace Global

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-need Assessment