|

시장보고서

상품코드

2044056

GaN-on-Silicon(GaN-on-Si) LED 에피텍셜 웨이퍼 시장 : 점유율 분석, 산업 동향 및 통계, 성장 예측(2026-2031년)GaN-on-Silicon (GaN-on-Si) LED Epitaxial Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

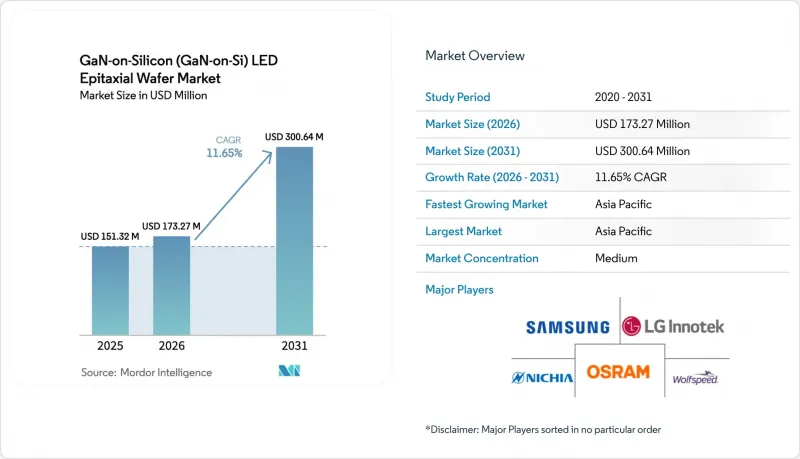

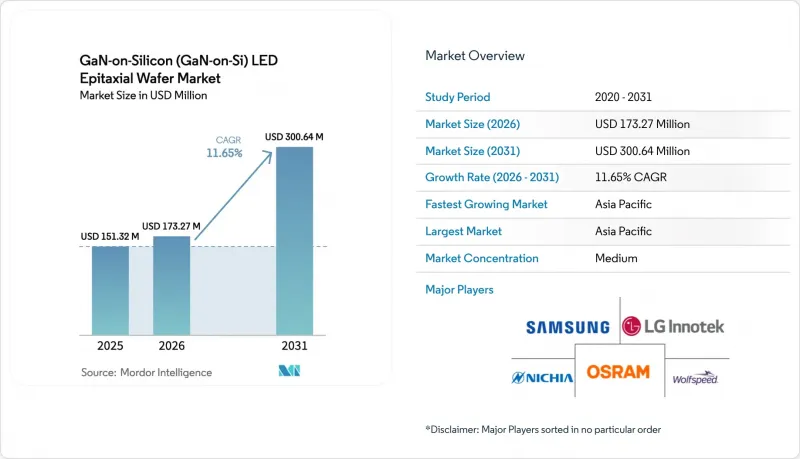

GaN-on-Silicon(GaN-on-Si) LED 에피텍셜 웨이퍼 시장 규모는 2025년 1억 5,100만 달러에서 2026년에는 1억 7,300만 달러로 확대되어 2031년까지 3억 100만 달러에 이를 것으로 예상되고 있으며 2026년부터 2031년까지 CAGR 11.65%로 성장할 전망입니다.

램프의 광속 효율에 대한 지속적인 규제 압력, 200mm 공정으로의 전환, 증강현실(AR) 장치에서 마이크로 LED의 채택이 결합되어 GaN-on-Si 에피택시의 상업적 매력이 증가하고 있습니다. 조명 분야 전체에서 LED의 보급으로 백열등과 할로겐 램프는 이미 경제적으로 구식이 되었지만, 미국, 유럽연합(EU), 중국, 인도 등에서의 기준 강화로 인해 고효율 다이아키텍처의 잠재 시장이 확대되고 있습니다. 파운드리 업체들은 실리콘 기판이 기존 CMOS 라인과 호환되는 것을 자본 비용 절감의 수단으로 인식하고 있으며, 이에 따라 업체들은 100mm 사파이어 생산 라인의 9배에 달하는 다이 생산 능력을 구현할 수 있는 300mm MOCVD 장비의 시험 도입에 박차를 가하고 있습니다. 이 기세는 10µm 미만의 픽셀을 목표로 하는 수직 통합형 디스플레이 프로그램을 통해 더욱 강화되고 있습니다. 이 분야에서는 GaN-on-Si 기술을 통해 사파이어에서 필요한 웨이퍼와 드라이버의 본딩 공정을 생략할 수 있습니다. 약 15개 업체가 리액터 생산 능력을 장악하고 있고, 결함 밀도를 허용 범위 내로 유지하는 데 필요한 공정 노하우를 보유하고 있기 때문에 경쟁의 격렬함은 여전히 완만한 수준에 머물러 있습니다.

세계 GaN-on-Silicon(GaN-on-Si) LED 에피택셜 웨이퍼 시장 동향 및 인사이트

고효율 고체 조명에 대한 수요 증가

2025년 설치 조명기구의 65%를 고체 조명이 차지했지만, 국제에너지기구(IEA)는 2026년 추정치에서 기술적으로 30%의 추가 효율 향상이 가능하다고 예측하고 있으며, GaN-on-Si LED 에피택셜 웨이퍼 시장에는 충분한 성장 여력이 남아있습니다. 2028년 7월부터 시행되는 미국 에너지부 규정은 백열등이나 할로겐 기술로는 달성할 수 없는 램프 효율을 의무화하고 있으며, 실리콘을 포함한 대체 기판 옵션을 실행 가능한 설계 방법으로 명시적으로 언급하고 있습니다. 주거 및 상업용 리노베이션을 위한 조명기구 제조업체들은 현재 부품 비용 절감과 130lm/W의 효율 기준치 달성이라는 이중의 압박에 직면해 있으며, 대구경 실리콘 웨이퍼를 사용하면 100mm 사파이어에 비해 루멘당 비용을 최대 25%까지 절감할 수 있습니다. 절감할 수 있습니다. 북미 전력회사들의 리베이트 프로그램은 고효율 제품에 대한 인센티브와 리스팅을 연계하여 수요를 촉진하고 있습니다. 이러한 요인들이 복합적으로 작용하여 대량 생산되는 조명 제품 전반에서 GaN-on-Si 에피택시에 대한 수요는 향후 몇 년 동안 지속될 것으로 보입니다.

GaN-on-Si 기판과 사파이어 기판의 비용 절감 가능성

실리콘 웨이퍼는 200mm 웨이퍼당 50-70달러에 판매되고 있으며, 이는 동급 사파이어의 약 8분의 1 가격입니다. 이는 구조적 우위를 가져오고, 웨이퍼 직경이 커질수록 그 차이는 더욱 커집니다. 2025년 실증 실험에서 5.25×108cm-2의 전위밀도가 현재 표준이 되었으며, 사파이어와의 효율 차이를 좁히면서도 기판 비용의 70% 차이를 유지하고 있습니다. 상하이 소재 공급업체에 따르면, 200mm GaN-on-Si 공정 1회로 100mm 사파이어 기판 1장의 4배에 달하는 다이 면적을 생산할 수 있으며, 1대의 장비로 연간 50만 개의 차량용 충전기용 LED를 공급할 수 있다고 합니다. 그러나 이러한 규모의 수익성은 수율을 85% 이상으로 유지할 수 있는지에 달려 있으며, 이는 실시간 휨 제어와 최적화된 버퍼 스택을 통해서만 달성할 수 있는 목표입니다. 이러한 공정 개선이 확산됨에 따라 비용에 민감한 최종 시장에서는 실리콘의 가격 우위가 남은 효율성 저하를 상쇄할 것으로 예측됩니다.

GaN-on-Si 에피택시의 높은 전위 밀도 및 수율에 대한 과제

실리콘과 질화갈륨 사이의 17% 격자 불일치로 인해 스레딩 전위 밀도는 1×109cm-2에 가깝습니다. 이는 사파이어계 재료보다 약 두 배 정도 높은 수치로, 외부 양자 효율이 10-15% 정도 떨어지는 주요 원인입니다. 60쌍의 AlN/GaN 다층막과 같은 완충 기술을 통해 응력을 억제할 수 있지만, 웨이퍼 한 장당 최대 12달러의 추가 리액터 시간이 발생합니다. 200mm 기판에서 100µm 이상의 휨이 발생하면 리소그래피와 다이싱이 복잡해지고, 일부 팹에서는 엣지 다이를 폐기해야 하기 때문에 대형 웨이퍼의 비용 이점이 손상됩니다. 진행상황은 제각각입니다. 현재 몇몇 공급업체는 30µm 미만의 휨 측정값을 보고하고 있지만, 표준화된 공정이 확립되지 않아 평균 수율이 사파이어 경쟁사 제품의 벤치마크인 90%를 밑돌고 있습니다.

부문 분석

기존 150mm와 신흥 300mm 생산의 가교 역할을 하는 200mm 부문은 전체 GaN-on-Silicon(GaN-on-Si) LED 에피택셜 웨이퍼 시장보다 더 빠르게 성장하고 있습니다. 2025년에도 중출력 조명 및 백라이트 분야의 확고한 입지로 인해 150mm 포맷이 출하량의 48.19%를 차지하며 여전히 주류를 이루고 있지만, 장비 로드맵은 현재 압도적으로 대구경화를 우선시하고 있습니다. 2026년 300mm 리액터 생산량 예측은 100mm 사파이어 로트 대비 9배의 다이를 생산할 수 있는 12인치 장비로의 전략적 전환을 강조하고 있으며, 이 계산은 디스플레이 패널 제조업체에 큰 반향을 불러일으키고 있습니다. GaN-on-Si(GaN-on-Si) LED 에피택셜 웨이퍼 시장 규모에서의 우위는 웨이퍼 면적의 확대와 함께 증가하지만, 이는 에지 제거 및 크랙과 관련된 스크랩을 최소화할 수 있는 경우에만 가능합니다. 8인치 웨이퍼에서 30µm 미만의 휨을 달성했다고 주장하는 공급업체는 90% 이상의 수율을 보고하고 있으며, 이는 경제성을 좌우하는 것은 단순한 직경이 아닌 공정 제어라는 것을 보여줍니다.

설비투자의 배분도 비슷한 논리에 따라 이루어집니다. 200mm CMOS 라인의 감가상각이 완료된 파운드리는 신규 사파이어 공장 건설 비용의 약 60%의 비용으로 GaN-on-Si용 챔버를 개조할 수 있습니다. 이 수치는 LED 수익률의 주기성을 우려하는 투자자들에게 매력적인 수치입니다. 100mm 및 150mm 웨이퍼는 UV 및 시제품 제작에 계속 사용되겠지만, 2027년 이후 신규 생산능력 증설은 200mm 이상으로 크게 편중될 것으로 애널리스트들은 예상하고 있습니다. 300mm로의 전환에는 여전히 가스 흐름의 균일성 및 온도 구배와 같은 기술적 과제가 남아 있지만, 특히 고화소 디스플레이에서 그 이점은 매우 매력적이며, 여러 최고 수준의 장비 제조업체가 2027년까지 대량 생산 시스템을 출하할 것을 약속하고 있습니다.

지역별 분석

아시아태평양은 GaN-on-Si(GaN-on-Si) LED 에피택셜 웨이퍼 시장의 제조 및 혁신의 원동력이 되고 있습니다. 이 지역은 2025년 매출의 66.93%를 차지해, 중국, 대만, 한국의 국가 프로그램이 2031년까지 연평균 복합 성장률(CAGR) 12.64%를 견인할 것으로 예측됩니다. 중국만 해도 마이크로 LED 인프라에 800억 위안(112억 달러)을 할당했으며, 그 중 대부분은 200mm 및 300mm GaN-on-Si 팹에 할당되어 대구경 기판의 현지 조달을 보장하고 있습니다. 대만과 일본 업체들은 재료 과학 전문성과 장비의 혁신성으로 이 규모를 보완하고 있습니다. Nichia Chemical Industry의 무수은 UV 이니셔티브와 ROHM의 GaN 공정 내재화 결정은 자체 공급망으로의 전환 추세를 잘 보여주고 있습니다.

북미는 고부가가치 용도와 정책 주도의 도입에 초점을 맞추었습니다. 2028년 7월부터 시행되는 에너지부의 결정으로 기존 백열전구 재고의 대체가 사실상 확실시되는 가운데, 온세미컨덕터와 세계 파운드리와 같은 제휴는 기존 CMOS 라인에 GaN 에피택시를 도입하려는 의지를 보여주고 있습니다. 유럽 진출은 독일 인피니언(Infineon)이 주도하고 있으며, 2025년 4분기에 300mm 웨이퍼를 출하하면서 유럽은 자동차 및 산업용 파워 디바이스의 거점 지역으로 자리매김하고 있습니다. 한편, 남미, 중동 및 아프리카는 현재 전 세계 출하량의 한 자릿수에 불과하지만, Off-grid 태양광 조명과 산업 현대화 노력으로 2020년대 말까지 저비용 GaN-on-Si LED에 대한 수요가 더욱 확대될 것으로 예측됩니다.

아시아태평양의 우위는 수직적 통합을 통해 더욱 강화되고 있습니다. 중국 및 대만 기업들은 GaN의 원료 성장부터 완성된 LED 모듈에 이르기까지 모든 공정을 자체적으로 진행하는 사례가 늘고 있으며, 이를 통해 공급망을 단축하고 시장 출시 기간을 단축하고 있습니다. 정부 보조금을 통해 파일럿 라인의 위험을 줄이고, 유럽과 미국의 경쟁사들이 자본 집약적이라고 여기는 300mm 포맷을 실험할 수 있게 되었습니다. 그럼에도 불구하고, 지적재산권 집행과 수출 관리의 불확실성이 이 지역의 장기적인 전망을 둔화시키고 있으며, 다국적 OEM 업체들은 북미와 유럽의 에피택셜 생산 능력을 도입하는 이중 소싱 전략을 채택하도록 촉구하고 있습니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.02The GaN-on-Silicon LED epitaxial wafer market size is expected to increase from USD 0.151 billion in 2025 to USD 0.173 billion in 2026 and reach USD 0.301 billion by 2031, growing at a CAGR of 11.65% over 2026-2031.

Persistent regulatory pressure on lamp efficacy, the migration to 200 mm processing, and micro-LED adoption in augmented-reality (AR) devices are converging to widen the commercial appeal of GaN-on-Si epitaxy. Across lighting classes, LED penetration has already made incandescent and halogen formats economically obsolete, yet tightening standards in the United States, the European Union, China, and India are expanding the addressable market for more efficient die architectures. Foundries view the compatibility of silicon substrates with existing CMOS lines as a capital-saving lever, spurring vendors to pilot 300 mm MOCVD tools that can deliver nine times the die output of 100 mm sapphire runs. Momentum is reinforced by vertically integrated display programs targeting sub-10 µm pixels, where GaN-on-Si eliminates the wafer-to-driver bonding step that sapphire requires. Competitive dynamics remain moderate because roughly fifteen players control reactor capacity and hold the process know-how needed to keep defect densities within acceptable limits.

Global GaN-on-Silicon (GaN-on-Si) LED Epitaxial Wafer Market Trends and Insights

Increasing Demand for Energy-Efficient Solid-State Lighting

Solid-state lighting accounted for 65% of installed luminaires in 2025, yet the International Energy Agency calculated in 2026 that another 30% efficiency gain remains technically achievable, leaving ample headroom for the GaN-on-Silicon LED epitaxial wafer market to grow. The U.S. Department of Energy rule, effective July 2028, mandates lamp efficacies that cannot be met by incandescent or halogen technology, explicitly citing alternative substrate options, including silicon, as viable design pathways. Fixture makers addressing residential and commercial retrofits now face dual pressures to lower bill-of-materials cost and exceed 130 lm/W efficacy thresholds, and larger-diameter silicon wafers reduce per-lumen cost by up to 25% compared with 100 mm sapphire. Utility rebate programs in North America reinforce demand by linking incentives to high-efficacy product listings. Collectively, these forces sustain a multiyear pull for GaN-on-Si epitaxy across high-volume lighting classes.

Cost Reduction Potential of GaN-on-Si Substrates Versus Sapphire

Silicon substrates sell for USD 50-70 per 200 mm wafer, roughly one-eighth the price of comparable sapphire, creating a structural advantage that expands as diameters scale upward. Demonstrations in 2025 showed that 5.25 X 108 cm-2 dislocation densities are now routine, cutting the efficiency gap with sapphire while still preserving a 70% substrate-cost delta. In reactor economics, a 200 mm GaN-on-Si run produces four times the die area of a 100 mm sapphire load, enabling a single tool to support 500,000 onboard-charger LEDs yearly, according to a Shanghai materials supplier. Such scale profitability, however, hinges on maintaining yields above 85%, a target achievable only with real-time warp control and optimized buffer stacks. As these process refinements diffuse, silicon's price advantage is expected to offset residual efficiency penalties in cost-sensitive end markets.

High Dislocation Density and Yield Challenges in GaN-on-Si Epitaxy

The 17% lattice mismatch between silicon and gallium nitride drives threading dislocation densities near 1 X 109 cm-2, roughly two orders of magnitude higher than sapphire-based material and a primary cause of 10-15% lower external quantum efficiency. Buffer techniques such as 60-pair AlN/GaN multilayers can suppress stress but add up to USD 12 per wafer in extra reactor time. Warp above 100 µm on 200 mm substrates complicates lithography and dicing, forcing some fabs to scrap edge die, which undermines the cost benefits of larger wafers. Progress is uneven: while a handful of suppliers now report sub-30 µm bow metrics, the lack of standardized processes keeps average yields below the 90% benchmark enjoyed by sapphire competitors.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of 200 mm and 300 mm CMOS Fabs for GaN-on-Si Epi

- Growth of Automotive LED Adoption for Headlamps and ADAS Sensors

- Competition from Sapphire-Based LED Wafers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The 200 mm tier, representing the bridge between legacy 150 mm and emerging 300 mm production, is expanding faster than the overall GaN-on-Silicon LED epitaxial wafer market. In 2025 the 150 mm format still dominated shipments at 48.19%, thanks to its entrenched position in mid-power illumination and backlighting, yet equipment roadmaps now overwhelmingly favor larger diameters. Volume evaluations of 300 mm reactors in 2026 underscore a strategic pivot to 12-inch tools that yield ninefold more die than 100 mm sapphire lots, an arithmetic that resonates strongly with display panel makers. The GaN-on-Silicon LED epitaxial wafer market size advantage grows as wafer area increases, but only if edge exclusion and crack-related scrap remain minimal. Suppliers claiming sub-30 µm bow on 8-inch substrates report yields north of 90%, demonstrating that process control rather than raw diameter dictates economic viability.

Capital allocation is following the same logic. Foundries with depreciated 200 mm CMOS lines can retrofit chambers for GaN-on-Si at roughly 60% of the cost of new sapphire fabs, a figure that appeals to investors wary of cyclical LED margins. Although 100 mm and 150 mm wafers will persist in UV and prototyping roles, analysts expect new capacity additions after 2027 to skew heavily toward 200 mm and above. The inflection to 300 mm still confronts technical hurdles, most notably uniform gas flow and temperature gradients, but the payback, especially for high-pixel-count displays, is compelling enough that several tier-one equipment makers have committed to shipping production systems by 2027.

The GaN-On-Silicon (GaN-On-Si) LED Epitaxial Wafer Market Report is Segmented by Wafer Diameter (Up To 100 Mm, 150 Mm, 200 Mm, and 300 Mm and Above), Application (General Lighting, Automotive Lighting, Display and Backlighting, and Specialty and Industrial Lighting), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Geography Analysis

Asia-Pacific is both the manufacturing and innovation engine of the GaN-on-Silicon LED epitaxial wafer market. The region accounted for 66.93% of 2025 revenue, and national programs in China, Taiwan, and South Korea are forecast to drive a 12.64% CAGR through 2031. China alone has earmarked RMB 80 billion (USD 11.2 billion) for micro-LED infrastructure, much of which is dedicated to 200 mm and 300 mm GaN-on-Si fabs, ensuring local availability of large-diameter substrates. Taiwanese and Japanese vendors complement this scale with materials science expertise and equipment innovation. Nichia's mercury-free UV initiative and ROHM's decision to internalize GaN processes underscore a trend toward captive supply chains.

North America concentrates on high-value applications and policy-led adoption. The Department of Energy ruling that becomes enforceable in July 2028 virtually guarantees replacement of legacy incandescent stock, whereas partnerships such as onsemi-GlobalFoundries signal a willingness to incorporate GaN epitaxy into brownfield CMOS lines. European participation is anchored by Germany's Infineon, whose 300 mm wafer deliveries in Q4 2025 position the region as a node for automotive and industrial power devices. While South America, the Middle East, and Africa currently absorb only single-digit percentages of global shipments, off-grid solar lighting initiatives and industrial modernization efforts are likely to generate incremental demand for low-cost GaN-on-Si LEDs by the end of the decade.

Asia-Pacific's dominance is enhanced by vertical integration: Chinese and Taiwanese firms increasingly handle everything from raw GaN growth to finished LED modules, compressing the supply chain and accelerating time-to-market. Government subsidies lower risk for pilot lines, allowing experimentation with 300 mm formats that Western competitors regard as capital intensive. Nonetheless, intellectual-property enforcement challenges and export-control uncertainties temper the region's longer-term outlook, encouraging multinational OEMs to adopt dual-sourcing strategies that include North American or European epitaxial capacity.

- Nichia Corporation

- Wolfspeed Inc.

- Epistar Corporation

- OSRAM GmbH

- LG Innotek Co. Ltd.

- Samsung Electronics Co. Ltd.

- Plessey Semiconductors Ltd.

- Qorvo Inc.

- Infineon Technologies AG

- NXP Semiconductors N.V.

- Power Integrations Inc.

- Efficient Power Conversion Corporation

- Exagan SA

- STMicroelectronics N.V.

- Panasonic Corporation

- Toshiba Corporation

- ROHM Co. Ltd.

- Sumitomo Electric Industries Ltd.

- Sanan Optoelectronics Co. Ltd.

- Aixtron SE

- IQE plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Demand For Energy-Efficient Solid-State Lighting

- 4.2.2 Cost Reduction Potential Of GaN-on-Si Substrates Versus Sapphire

- 4.2.3 Government Regulations Phasing-Out Incandescent And Halogen Bulbs

- 4.2.4 Growth Of Automotive LED Adoption For Headlamps And ADAS Sensors

- 4.2.5 Integration Of GaN-Based Micro-LED Arrays For AR Displays

- 4.2.6 Expansion Of 200 mm And 300 mm CMOS Fabs For GaN-on-Si Epi

- 4.3 Market Restraints

- 4.3.1 High Dislocation Density And Yield Challenges In GaN-on-Si Epitaxy

- 4.3.2 Competition From Sapphire-Based LED Wafers

- 4.3.3 Limited Availability Of Patterned Si Substrates With Stress Control

- 4.3.4 Risk Of IP Litigation In GaN Epitaxy Processes

- 4.4 Industry Analysis

- 4.5 Impact Of Macroeconomic Factors On The Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power Of Suppliers

- 4.6.2 Bargaining Power Of Buyers

- 4.6.3 Threat Of New Entrants

- 4.6.4 Threat Of Substitutes

- 4.6.5 Intensity Of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Wafer Diameter

- 5.1.1 Upto 100 mm

- 5.1.2 150 mm

- 5.1.3 200 mm

- 5.1.4 300 mm and Above

- 5.2 By Application

- 5.2.1 General Lighting

- 5.2.2 Automotive Lighting

- 5.2.3 Display and Backlighting

- 5.2.4 Specialty and Industrial Lighting

- 5.3 By Geography

- 5.3.1 North America

- 5.3.2 Europe

- 5.3.3 Asia-Pacific

- 5.3.4 Rest of the World

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Wolfspeed Inc.

- 6.4.3 Epistar Corporation

- 6.4.4 OSRAM GmbH

- 6.4.5 LG Innotek Co. Ltd.

- 6.4.6 Samsung Electronics Co. Ltd.

- 6.4.7 Plessey Semiconductors Ltd.

- 6.4.8 Qorvo Inc.

- 6.4.9 Infineon Technologies AG

- 6.4.10 NXP Semiconductors N.V.

- 6.4.11 Power Integrations Inc.

- 6.4.12 Efficient Power Conversion Corporation

- 6.4.13 Exagan SA

- 6.4.14 STMicroelectronics N.V.

- 6.4.15 Panasonic Corporation

- 6.4.16 Toshiba Corporation

- 6.4.17 ROHM Co. Ltd.

- 6.4.18 Sumitomo Electric Industries Ltd.

- 6.4.19 Sanan Optoelectronics Co. Ltd.

- 6.4.20 Aixtron SE

- 6.4.21 IQE plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment