|

시장보고서

상품코드

2063932

중국의 LED 에피텍셜 웨이퍼 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China LED Epitaxial Wafer - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

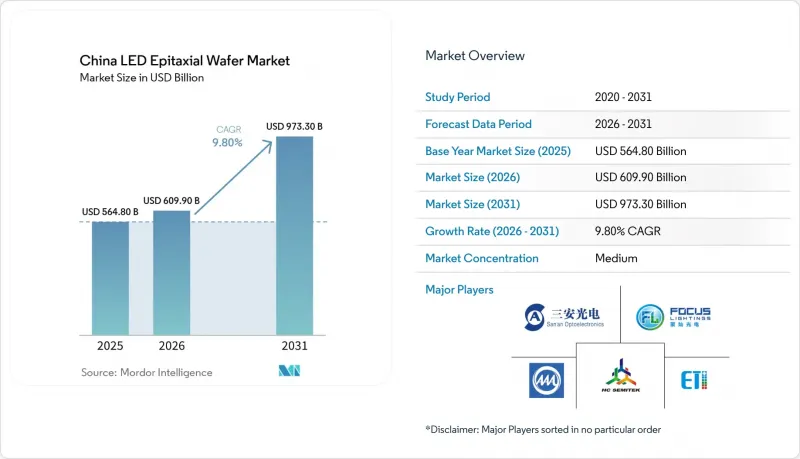

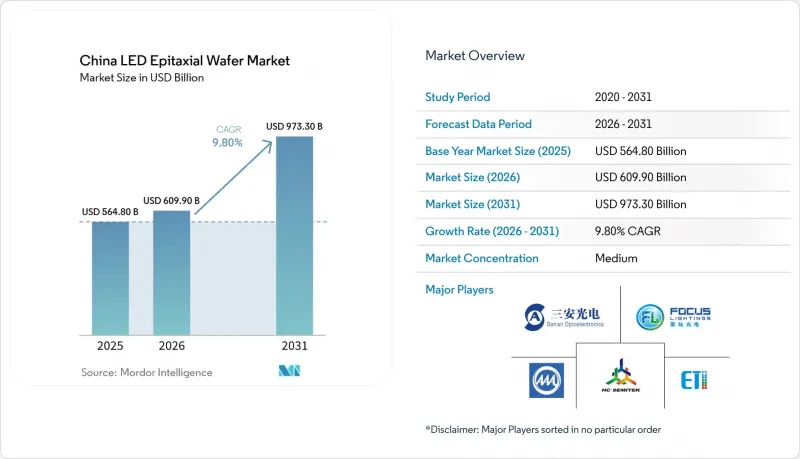

Mordor Intelligence에 의하면, 중국 LED 에피텍셜 웨이퍼 시장 규모는 2025년에 5억 6,480만 달러, 2026년에 6억 990만 달러, 2031년까지 9억 7,330만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 9.8%로 성장할 것으로 전망됩니다.

본 보고서는 재료 시스템(GaN 기반 에피택셜 웨이퍼, AlInGaP 에피택셜 웨이퍼 등), 기판 유형(사파이어, 실리콘, 실리콘 카바이드(SiC), 갈륨 비소(GaAs)), 웨이퍼 직경(100mm 이하, 150mm, 200mm 이상) 및 용도(일반 조명, 자동차용 조명, 디스플레이 및 백라이트 등)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

중국 LED 에피택셜 웨이퍼 시장 동향 및 분석

국내 LED 공급망에 대한 정부의 보조금 및 세제 혜택

제14차 5개년 계획에서는 단순한 생산량뿐만 아니라 첨단 노드에 대한 보조금을 중점적으로 배분함으로써, 200mm GaN-on-Si 및 AlGaN 리액터의 실질 자본 비용을 최대 30% 절감하고 있습니다. 샤먼과 우한에서 시행되고 있는 성 차원의 프로그램에서는 토지 무상 제공과 공공요금 할인을 결합하여 운영비를 10-15% 절감함으로써, 신규 팹의 손익분기점을 앞당기고 있습니다. 현재 2027년까지 국산 장비의 채택률을 70%로 하라는 요건이 마련되어 있으며, 이에 따라 AMEC 등 현지 MOCVD 공급업체에 수주가 집중되면서 전략적 노하우가 보호되고 있습니다. 이러한 정책들의 조합을 통해 투자 회수 기간이 단축되었고, 칩의 이익률이 하락하고 있음에도 불구하고 연구개발비가 유지되어, 2031년까지 프리미엄 등급 웨이퍼 생산 확대를 위한 기반이 강화되고 있습니다.

일반 조명에 LED 도입을 촉진하는 에너지 효율 규제

중국의 탄소중립 공약에 따라, 건물 개보수가 수요를 구조적으로 뒷받침하고 있습니다. GB 50034-2024 규격에 따르면, 최소 광속 효율 기준이 110-130 lm/W로 상향 조정됨에 따라 기존 형광등 기구는 이 기준을 충족하지 못하게 되어, 정부 시설에서의 개조가 의무화되었습니다. 지자체 보조금 제도에 따라 개보수 비용의 최대 40%가 환급되므로, 교체 주기가 앞당겨져 상품화가 진행되는 상황에서도 웨이퍼의 기준 출하량은 유지될 것입니다. 주거용 스마트 전구는 조광이 가능한 백색 조명 솔루션에 듀얼 칩 또는 RGB 웨이퍼가 필요하기 때문에 수요를 더욱 끌어올리고 있습니다. 이러한 요인으로 인해, 중국의 LED 에피택셜 웨이퍼 시장은 설비 투자가 디스플레이 및 자동차 분야로 전환되는 상황에서도 조명 분야의 안정적인 수요를 지속적으로 누릴 수 있을 것으로 전망됩니다.

미니 및 마이크로 LED 디스플레이 생산 라인의 급속한 확대

주요 디스플레이 기업들은 웨이퍼 공급을 패널 로드맵과 직접 연계하고, 장기 공급 계약을 체결함으로써 6인치 및 200mm 생산 능력을 RGB 및 고균일성 블루 제품으로 전환하고 있습니다. TCL CSOT의 Prima 인수는 백엔드 통합을 확보하는 동시에, 3nm 미만의 파장 목표를 충족하는 웨이퍼에 대한 안정적인 수요를 창출하고 있습니다. Sanan은 2024년부터 2025년까지 월간 마이크로 LED 웨이퍼 생산량을 5배 이상 늘려 삼성의 플래그십 TV에 공급할 자격을 획득하는 한편, 중국 업체도 프리미엄 수준의 균일성 기준을 달성할 수 있음을 입증했습니다. HC 세미텍의 주하이 공장은 BOE의 30억 달러 규모 8.6세대 백라이트 투자와 연계하여,월3,000장의 6인치 웨이퍼 증산을 실현했습니다. 이러한 움직임들이 맞물려 중기적인 성장의 기반이 될 것이며, 주요 팹의 가동률을 높이는 동시에 일반 조명용 생산 라인공급 과잉을 해소하게 될 것입니다.

부문별 분석

GaN 기반 웨이퍼는 형광체 변환형 백색 램프, RGB 백라이트, 자동차용 헤드램프용 청색 발광에 힘입어 2025년 시장 가치의 65%를 차지했습니다. 조명 및 디스플레이 분야의 안정적인 공급량 덕분에, 이 부문은 계속해서 현금 흐름의 기반이 되어 연구 개발(R&D) 비용을 충당하고 있습니다. AlGaN은 현재 생산량의 극히 일부에 불과하지만, 의료 분야에서 수은 램프 사용이 금지되는 규제와 사용 현장에서의 멸균에 대한 수요가 증가함에 따라 연평균 성장률(CAGR) 12.34%를 달성하며, 중국의 전체 LED 에피택셜 웨이퍼 시장을 크게 웃도는 성장이 예상됩니다. Sanan이 추진하는 9억 5,000만 달러 규모의 다년간 설비 확장 계획에 더해, 후베이 DUVTek의 시범 라인 가동은 중국이 수입품을 대체하고 심자외선(DUV) 밸류체인을 장악하고자 한다는 점을 시사합니다. 부수적인 AlInGaP 제품군은 자동차 브레이크 램프 및 원예 분야에 공급되고 있으며, 이는 팹(fab)에게 우량 기업의 경기 변동에 대한 헤지 수단이 되고 있습니다.

웨이퍼 스케일 AlGaN 시장 수용은 외부 양자 효율을 10% 가까이 끌어올린 최근의 기술적 돌파구에 힘입어, 동남아시아의 수도 유틸리티자들에 대한 수출 전망이 밝아지고 있습니다. 국내 지자체 입찰에서는 고체 UVC의 채택이 점점 더 의무화되고 있어, 지속적인 수요 기반이 확보되고 있습니다. 이러한 요소들을 종합해 보면, GaN의 우위와 AlGaN 성장에 따른 포트폴리오 효과가 수익을 안정화시켜, 중국의 LED 에피택셜 웨이퍼 시장이 단기적인 수익에 차질을 빚지 않으면서도 공정 혁신에 자금을 투입할 수 있도록 보장하고 있습니다.

사파이어는 격자 정합성, 확립된 8인치 공급 체계, 그리고 자동차 OEM 업체들의 선호도 덕분에 2025년에는 55.63%의 시장 점유율을 차지했습니다. 이러한 입증된 신뢰성 덕분에, 조명 분야의 가격 압박이 심화되는 상황에서도 헤드램프나 실외 조명 기구에 대한 채택은 계속되고 있습니다. 실리콘 기반 GaN은 직경 200mm라는 큰 크기, 낮은 웨이퍼 비용, 기존 CMOS 팹과의 호환성을 제공하며, 사파이어의 성장률을 능가하는 연평균 성장률(CAGR) 13.3%를 뒷받침하는 유력한 경쟁자입니다. 패널 제조업체들이 부품 원가 절감을 추구하는 분야, 특히 미니 LED 백라이트 분야에서 실리콘의 중국 LED 에피택셜 웨이퍼 시장 점유율이 가장 빠르게 증가하고 있습니다.

프로세스의 성숙도가 여전히 걸림돌로 작용하고 있습니다. 200mm GaN-on-Si에서 발생하는 에지 관련 순방향 전압 드리프트는 여전히 사용 가능한 다이 면적을 감소시키고 있지만, ALLOS와 Ennostar간의 제휴를 통해 파장 균일도 3% 미만을 달성할 수 있을 것으로 전망됩니다. 이는 병에 나누어 담을 필요 없이 대량으로 재사용할 수 있게 해주는 기준치입니다. 실리콘 카바이드는 틈새 시장인 고출력 및 고온 용도에 활용되며, 전기차(EV) 구동계용 인버터와 중복되는 부분이 있어 결정 성장 노하우를 상호 활용할 수 있는 장점이 있습니다. 따라서 기판의 구성은 듀얼 트랙 구조로 진화하고 있으며, 사파이어는 엄격한 신뢰성이 요구되는 시장을 지키고, 실리콘은 대량 생산되는 소비자용 디스플레이 수요를 흡수하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the china lED epitaxial wafer market size is projected to be USD 564.8 million in 2025, USD 609.9 million in 2026, and reach USD 973.3 million by 2031, growing at a CAGR of 9.8% from 2026 to 2031.

This report is Segmented by Material System (GaN-Based Epitaxial Wafers, Alingap Epitaxial Wafers, and More), Substrate Type (Sapphire, Silicon, Silicon Carbide (SiC), Gallium Arsenide (GaAs)), Wafer Diameter (Up To 100 Mm, 150 Mm, 200 Mm and Above), and Application (General Lighting, Automotive Lighting, Displays and Backlighting and More). The Market Forecasts are Provided in Terms of Value (USD).

China LED Epitaxial Wafer Market Trends and Insights

Government Subsidies And Tax Incentives For Domestic LED Supply Chain

The 14th Five-Year Plan tilts subsidies toward advanced nodes rather than sheer volume, cutting effective capital costs for 200 mm GaN-on-Si and AlGaN reactors by up to 30%. Provincial programs in Xiamen and Wuhan layer land concessions and utility discounts that shave operating expenses by 10-15%, accelerating breakeven for new fabs. Conditions now require 70% domestic equipment content by 2027, funneling orders to local MOCVD vendors such as AMEC and protecting strategic know-how. The policy mix reduces payback periods, sustains R&D outlays despite thinning chip margins, and lengthens the runway for premium-grade wafer expansion through 2031.

Energy Efficiency Mandates Driving LED Adoption In General Lighting

China's carbon-neutral pledge turns building retrofits into a structural floor of demand. Standard GB 50034-2024 lifts minimum efficacy thresholds to 110-130 lm/W, rendering legacy fluorescent fixtures non-compliant and triggering mandated upgrades in government facilities.Municipal rebates reimburse up to 40% of retrofit costs, bringing forward replacement cycles and sustaining baseline wafer shipments even amid commoditization. Residential smart bulbs add incremental pull by requiring dual-chip or RGB wafers for tunable white solutions. This driver ensures the China LED epitaxial wafer market continues to harvest steady lighting demand while shifting capex toward display and vehicle segments.

Rapid Expansion Of Mini And Micro LED Display Manufacturing Lines

Display giants are tying wafer supply directly to panel roadmaps, locking in long-term offtake agreements that pull 6-inch and 200 mm capacity toward RGB and high-uniformity blue products. TCL CSOT's acquisition of Prima secures back-end integration and creates stable demand for wafers that meet sub-3 nm wavelength targets.Sanan more than quintupled monthly microLED wafer output across 2024-2025, qualifying for Samsung's flagship televisions and proving Chinese vendors can hit premium uniformity benchmarks. HC Semitek's Zhuhai fab adds 3,000 six-inch wafers a month of incremental volume, synchronized with BOE's USD 3 billion Gen 8.6 backlight investments. Together, these moves anchor medium-term growth, lifting utilization at leading fabs and absorbing oversupply from general-lighting lines.

Other drivers and restraints analyzed in the detailed report include:

- Accelerated Automotive LED Penetration In New Energy Vehicles

- Price Erosion Due To Overcapacity In Conventional LED Chips

- High Capital Intensity And Depreciation Of MOCVD Equipment

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

GaN-based wafers captured 65% of the 2025 value, underpinned by blue emission for phosphor-converted white lamps, RGB backlights, and automotive headlamps. Stable volumes from lighting and displays mean this segment continues to anchor cash flow and subsidize R&D. AlGaN supplies only a fraction of present output, yet health-sector regulations banning mercury lamps and rising demand for point-of-use sterilization enable a 12.34% CAGR that materially outpaces the China LED epitaxial wafer market size as a whole. Sanan's USD 950 million multiyear build-out, plus pilot lines at Hubei DUVTek, signal that China aims to displace imports and own the deep-UV value chain. Secondary AlInGaP lines serve automotive brake lights and horticulture, giving fabs a hedge against blue-chip cyclicality.

Commercial acceptance of wafer-scale AlGaN rides on recent breakthroughs pushing external quantum efficiency near 10%, opening export prospects to Southeast Asian water utilities. Domestic municipal tenders increasingly stipulate solid-state UVC, locking in a durable demand baseline. Taken together, the portfolio effect of GaN dominance and AlGaN growth stabilizes revenue, ensuring the China LED epitaxial wafer market can bankroll process innovations without jeopardizing near-term earnings.

Sapphire commanded a 55.63% share in 2025 thanks to lattice compatibility, an established 8-inch supply, and familiarity among automotive OEMs. Its proven reliability preserves design-in status for headlamps and outdoor fixtures even as price pressure mounts in lighting. Silicon-based GaN is the natural challenger, offering a larger 200 mm diameter, lower raw-wafer cost, and compatibility with existing CMOS fabs, underpinning a 13.3% CAGR that overtakes sapphire growth. The China LED epitaxial wafer market share for silicon rises fastest where panel makers chase bill-of-materials savings, particularly in mini-LED backlighting.

Process maturity remains the gating factor. Edge-related forward-voltage drift on 200 mm GaN-on-Si still reduces usable die area, but partnerships such as ALLOS-Ennostar promise sub-3% wavelength uniformity, a threshold that unlocks bin-free mass transfer. Silicon carbide fills niche power and high-temperature roles, overlapping with EV drive-train inverters and offering cross-utilization of crystal growth know-how. The substrate mix therefore evolves toward a dual-track structure, with sapphire safeguarding stringent reliability markets and silicon harvesting high-volume consumer displays.

List of Companies Covered in this Report:

- Sanan Optoelectronics Co., Ltd.

- HC Semitek Corporation

- Focus Lightings Tech Co., Ltd.

- Elec-Tech International Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Epistar Corporation

- Osram Opto Semiconductors GmbH

- Cree LED (Smart Global Holdings, Inc.)

- Seoul Semiconductor Co., Ltd.

- Genesis Photonics Inc.

- Changelight Co., Ltd.

- Epileds Technologies Inc.

- Opto Tech Corporation

- Aucksun Crystal

- EpiWorld International Co., Ltd.

- SinoNitride Semiconductor Co., Ltd.

- Advanced Epitaxy Technology Inc.

- Lextar Electronics Corp.

- Nichia Corporation

- Hangzhou Silan Microelectronics Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Expansion of Mini and Micro LED Display Manufacturing Lines

- 4.2.2 Government Subsidies and Tax Incentives for Domestic LED Supply Chain

- 4.2.3 Energy Efficiency Mandates Driving LED Adoption in General Lighting

- 4.2.4 Accelerated Automotive LED Penetration in New Energy Vehicles

- 4.2.5 Rising Demand for UVC LED Epitaxial Wafers for Water Purification

- 4.2.6 Localization Push for Silicon Carbide Substrate Supply Security

- 4.3 Market Restraints

- 4.3.1 High Capital Intensity and Depreciation of MOCVD Equipment

- 4.3.2 Price Erosion Due to Overcapacity in Conventional LED Chips

- 4.3.3 Technical Yield Challenges in 200 mm GaN-on-Si Platforms

- 4.3.4 Environmental Regulations on Ammonia and Arsine Emissions Limiting Expansion

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material System

- 5.1.1 GaN-based Epitaxial Wafers

- 5.1.2 AlInGaP Epitaxial Wafers

- 5.1.3 AlGaN Epitaxial Wafers

- 5.2 By Substrate Type

- 5.2.1 Sapphire

- 5.2.2 Silicon

- 5.2.3 Silicon Carbide (SiC)

- 5.2.4 Gallium Arsenide (GaAs)

- 5.3 By Wafer Diameter

- 5.3.1 Up to 100 mm

- 5.3.2 150 mm

- 5.3.3 200 mm and Above

- 5.4 By Application

- 5.4.1 General Lighting

- 5.4.2 Automotive Lighting

- 5.4.3 Displays and Backlighting

- 5.4.4 UV Sterilization

- 5.4.5 Industrial and Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Market Positioning

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sanan Optoelectronics Co., Ltd.

- 6.4.2 HC Semitek Corporation

- 6.4.3 Focus Lightings Tech Co., Ltd.

- 6.4.4 Elec-Tech International Co., Ltd.

- 6.4.5 NationStar Optoelectronics Co., Ltd.

- 6.4.6 Epistar Corporation

- 6.4.7 Osram Opto Semiconductors GmbH

- 6.4.8 Cree LED (Smart Global Holdings, Inc.)

- 6.4.9 Seoul Semiconductor Co., Ltd.

- 6.4.10 Genesis Photonics Inc.

- 6.4.11 Changelight Co., Ltd.

- 6.4.12 Epileds Technologies Inc.

- 6.4.13 Opto Tech Corporation

- 6.4.14 Aucksun Crystal

- 6.4.15 EpiWorld International Co., Ltd.

- 6.4.16 SinoNitride Semiconductor Co., Ltd.

- 6.4.17 Advanced Epitaxy Technology Inc.

- 6.4.18 Lextar Electronics Corp.

- 6.4.19 Nichia Corporation

- 6.4.20 Hangzhou Silan Microelectronics Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment