|

시장보고서

상품코드

2061698

의료용 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Folding Carton In Healthcare - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

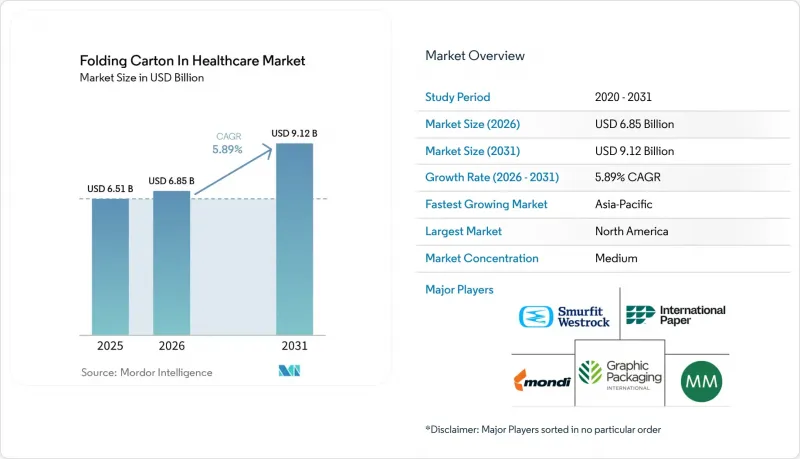

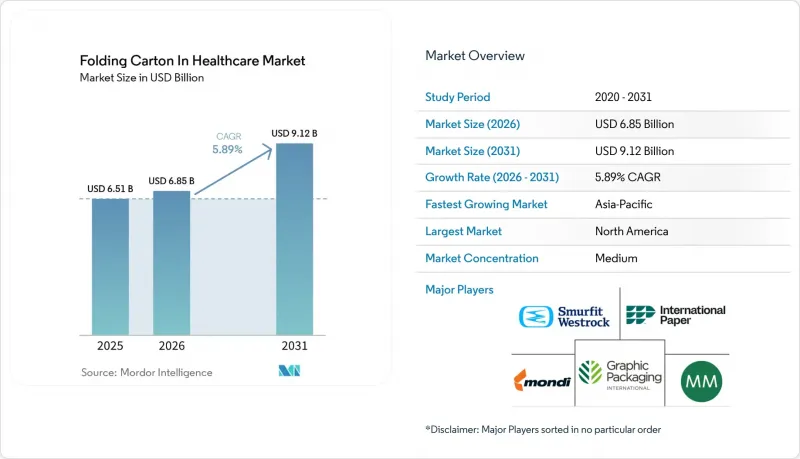

Mordor Intelligence에 의하면, 의료용 접이식 카톤 시장 규모는 2025년 65억 1,000만 달러로 평가되었습니다. 2026년 68억 5,000만 달러로 확대되어 2031년까지 91억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR은 5.89%를 나타낼 전망입니다.

본 보고서는 원료 유형(고형 표백 황산 펄프, 접이식 카톤용 판지, 코팅 미표백 크라프트지 등), 인쇄 기술(오프셋 인쇄, 플렉소 인쇄 등), 용도(제약 제조업체, 의료기기 제조업체, 영양 보조 식품·건강기능식품 기업 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

의료용 접이식 카톤 시장 동향 및 인사이트

단회 투여 치료가 필요한 만성 질환 증가

의료용 접이식 카톤 시장은 반복 투여와 더욱 엄격한 복약 순응도 관리가 필요한 만성 질환 증가로 인해 꾸준한 수요를 유지하고 있습니다. 1회 투여용 블리스터 팩이나 캘린더형 약상자는 투여 일정을 준수하기 쉽고 조제 현장에서 확인하기도 용이하기 때문에 당뇨병, 순환기 질환 및 종양학 치료 분야에서 점점 더 많이 사용되고 있습니다. 따라서 각 제약사는 반복적으로 열고 닫아도 접힘 강도가 저하되지 않으며, 28일분 및 90일분의 블리스터 포장을 수납할 수 있는 카톤 구조를 지정하고 있습니다. 론자(Lonza)는 인도의 레와리 공장과 중국의 쑤저우 공장에서 캡슐 생산 능력을 확대했습니다. 두 공장은 2024년 말에 가동을 시작하며, 2025년 3분기에는 추가 생산 라인이 가동될 예정으로, 아시아태평양 내 일회 투여 제형으로의 광범위한 전환을 뒷받침하고 있습니다. 인도의 의약품 시장은 2024년 613억 6,000만 달러에서 2033년까지 1,300억 달러로, 중국 시장은 2024년 804억 달러에서 2030년까지 1,266억 달러로 확대될 것으로 예측되어, 의료용 접이식 카톤에 대한 장기적인 수요를 뒷받침하고 있습니다. 이러한 수요로 인해 의료용 접이식 카톤 시장의 수량 성장은 가격 주기에 대한 의존도가 낮아지고, 치료 패턴 및 복약 순응도를 중시하는 패키지 디자인과의 연관성이 더욱 강화되고 있습니다.

시리얼화 규제가 카톤의 표시 면적 확대를 촉진

의료용 접이식 카톤 시장은 더 많은 상자 공간과 높은 인쇄 정밀도를 요구하는 일련번호 부여 규제로 인해 성장세를 보이고 있습니다. 유럽연합(EU)의 위조 의약품 지침에 따르면, 2019년부터 처방약 포장에 고유한 2차원 데이터 매트릭스 코드를 기재하는 것이 의무화되어 있는 반면, 미국의 의약품 공급망 보안법에서는 제품 식별자, 일련번호, 로트 번호, 유효 기간을 기계 판독 가능한 형식으로 기재해야 합니다. 유럽연합 집행위원회 위임규정 2016/161에서는 데이터 매트릭스 영역의 최소 크기를 8mm×8mm로 하고, 사방에 1mm의 퀄트 존을 설정하도록 규정하고 있습니다. 이로 인해, 1회 투여용 바이알이나 프리필드 주사기의 소형 포장지의 경우, 상자의 유효 표면적 중 12%에서 15%가 차지될 가능성이 있습니다. 그 결과, 의료용 접이식 카톤 시장의 각 변환 업체들 사이에서는 선명한 코드 표시를 견디고, 잉크 번짐을 방지하며, 검사나 스캔 시 평평한 상태를 유지할 수 있는 고품질 판지에 대한 수요가 증가하고 있습니다. 암콜사는 2026년 3월, 이탈리아 공장에서 재활용이 가능한 필름을 출시했습니다. 이 필름에는 시리얼화 대응 코팅이 적용되어 있어, 고속 검증 시 발생하는 잉크 번짐과 관련된 문제를 줄여줍니다. 유럽 의약품 검증 시스템(EMVS)에서는 현재 하루 4,000만 건 이상의 검증 처리가 이루어지고 있으며, 이로 인해 의료용 접이식 카톤에 대해 더욱 엄격한 인쇄 공차 유지와 더 높은 신뢰성을 갖춘 원자재 성능이 요구되는 압박이 계속되고 있습니다.

판지 가격 변동

의료용 접이식 카톤 시장은 불안정한 펄프 및 판지 원가 상승으로 인한 명백한 제약에 직면해 있습니다. 2024년부터 2025년에 걸쳐 북미산 표백 침엽수 크라프트 펄프 가격은 톤당 1,050-1,350달러 범위에서 등락을 보였으나, 스칸디나비아 제지 공장의 에너지 가격 변동으로 인해 생산 비용은 계속해서 압박을 받았습니다. 고형 표백 판지 및 접이식 카톤용 판지의 가격은 보통 60일에서 90일 정도 뒤처져 변동하기 때문에 제약 회사 고객과 고정 가격 공급 계약을 체결한 가공업체는 위험에 노출될 수밖에 없습니다. 의료용 접이식 카톤 시장에서 이러한 가격 변동의 시차로 인해, 규정 준수 비용, 인쇄 품질, 인증 비용이 이미 급등하고 있는 바로 그 시점에 이익률이 압박받을 가능성이 있습니다. 지역 내 중소규모 제지업체들은 펄프 부문으로의 역통합이 부족하기 때문에 더 큰 위험에 노출되어 있습니다. 또한, 펄프 가격이 톤당 1,300달러를 넘어섬에 따라 유럽의 여러 전문 제조업체들은 2025년 하반기 가동률을 70%-75%로 낮췄습니다. 이에 대해 제약사의 구매 담당자들은 듀얼 소싱이나 펄프 가격 연동 조항을 도입하는 방식으로 대응하고 있으며, 이로 인해 공급 안정성은 향상되고 있지만, 의료용 접이식 카톤의 가격 경쟁이 격화되면서 중소규모의 독립 공급업체들에게는 불리한 상황이 되고 있습니다.

부문별 분석

2025년 기준으로, 의료용 접이식 카톤 시장 규모의 43.28%를 고형 표백 황산 펄프가 차지했으며, 이는 이 펄프의 높은 불투명도, 높은 백색도, 그리고 고속 오프셋 인쇄기에서 보여주는 신뢰할 수 있는 인쇄 성능을 반영한 것입니다. 접이식 박스 보드는 2031년까지 연평균 성장률(CAGR) 7.06%를 기록하며 성장할 것으로 예상되며, 의료용 접이식 카톤 시장에서 가장 빠르게 성장하는 소재 부문이 될 전망입니다. 메츠아 보드(Metsa Board)의 생애주기 평가(LCA) 결과에 따르면, 신선한 섬유를 사용한 등급은 코팅되지 않은 미표백 크라프트 보드에 비해 이산화탄소 배출량이 50%에서 60% 낮은 것으로 나타나, 해당 제품의 채택이 확대되고 있습니다. 또한, 섬유가 길기 때문에 내천자성을 저해하지 않으면서도 평량(g/m²)을 15%에서 20%까지 줄일 수 있게 되었습니다. 표백하지 않은 코팅 크라프트 보드는 우수한 인쇄 적합성보다는 구조적 강도가 중시되는 외장재나 2차 포장 용도로 계속해서 사용되고 있습니다. 화이트 라이닝 칩보드는 재활용 소재가 지속가능성 메시지를 뒷받침하며, 인쇄 요건이 그리 까다롭지 않은 비용 효율을 중시하는 뉴트라슈티컬(기능성 식품) 용도로만 한정되어 있습니다.

헬스케어 업계에서는 접이식 카톤를 구매하는 고객들이 규제 준수 인쇄 요건과 재활용 가능성이라는 두 가지 기대를 모두 충족하는 골판지를 점점 더 선호하는 추세입니다. 2025년 2분기에 출하된 스트라 엔소의 오울 생산 라인은 공급업체들이 이러한 수요에 부응하기 위해 의약품 등급의 소비자용 판지 생산 능력을 어떻게 확대하고 있는지를 보여주었습니다. 또한, 유럽연합(EU)의 ‘포장 및 포장 폐기물에 관한 규정’에 따라, 변환업체들은 재활용성을 저하시키는 폴리에틸렌이나 폴리프로필렌 층을 사용한 라미네이트 판지 구조에서 점차 벗어나고 있습니다. 수성 배리어 소재의 중요성이 커지고 있지만, 습기에 민감한 바이오의약품의 경우 여전히 성능상의 격차가 존재하기 때문에 일부 콜드체인 용도에서는 기존의 왁스 코팅이나 기타 보호 성능이 뛰어난 등급이 계속해서 사용되고 있습니다. 이러한 균형 덕분에, 의료용 접이식 카톤는 의약품의 안정성과 유통 안전성을 해치지 않으면서도 더욱 청결하고 가벼운 소재로 전환되고 있습니다.

지역별 분석

2025년 기준으로 북미는 의료용 접이식 카톤 시장의 34.63%를 차지했으나, 아시아태평양은 2031년까지 지역별 가장 높은 연평균 성장률(CAGR)인 6.57%를 나타낼 것으로 전망됩니다. 북미의 위상은 미국의 의약품 포장 수요 규모와 경구용 고형 제제 부문 전반에서 병 및 카톤 시스템이 지속적으로 사용되고 있는 점을 반영하고 있습니다. 또한, 이 지역은 주류 의약품 유통 분야에서 어린이 안전 기준, 일련번호 관리 규정 준수 및 고품질 인쇄 요건이 엄격하게 시행되고 있기 때문에 의료용 접이식 카톤 시장에서 계속해서 핵심적인 위치를 차지하고 있습니다. 아시아태평양이 더 빠르게 성장하고 있는 이유는 의약품 생산이 확대되고 현지 생산 능력이 증가함에 따라, 인구 밀집 지역에서는 1회 투여형 제제가 점점 더 보편화되고 있기 때문입니다. 인도의 의약품 시장은 2024년 613억 6,000만 달러에서 2033년까지 1,300억 달러로, 중국 시장은 2024년 804억 달러에서 2030년까지 1,266억 달러로 확대될 것으로 전망됩니다.

론자(Lonza)가 인도 레와리와 중국 쑤저우에서 진행 중인 생산 능력 확충은 다국적 공급업체들이 1회 투여용 포장 및 복약 순응도 향상을 위한 제형으로의 지역적 전환에 발맞추어 생산 체계를 정비하고 있음을 보여줍니다. 이는 의료용 접이식 카톤에 있어 중요한 의미를 지닙니다. 왜냐하면 2차 포장 수요는 일반적으로 제형의 생산량이나 의약품 제조의 현지화 추세를 따르기 때문입니다. 유럽은 매출 점유율 면에서 1위는 아니지만, 여전히 중요한 지역입니다. 왜냐하면 엄격한 순차화 요건과 더불어, 재활용이 가능한 판지 구조와 환경 부하가 낮은 포장 시스템에 대한 강력한 수요가 공존하고 있기 때문입니다. ‘위조 의약품 지침’ 및 ‘포장 및 포장 폐기물 규정’에 따라, 유럽의 제약 구매 담당자들은 판지 선정, 인쇄 레이아웃, 차단 설계 등을 동시에 재검토해야 하는 상황에 놓여 있습니다. 이러한 조합으로 인해 유럽은 의료용 접이식 카톤 분야에서 규제의 영향을 가장 크게 받는 지역 중 하나가 되었으며, 특히 프리미엄급의 지속 가능한 원자재를 판매하고자 하는 공급업체들에게 중요한 시장이 되고 있습니다.

남미, 중동 및 아프리카에서는 현지 접이식 카톤의 생산 능력이 제한적이고, 헬스케어 관련 규제도 국가마다 차이가 있어 시장 확대 속도가 완만합니다. 이 지역에서는 유럽이나 북미에서 수입함에 따라 착륙 비용이 15%에서 25%까지 추가될 가능성이 있으며, 이로 인해 현지에서 조달된 골판지 상자가 다른 포장 옵션에 비해 경쟁력을 잃고 있습니다. 2024년에 135억 달러 규모에 달했으며, 2017년 이후 연평균 성장률(CAGR) 7%로 성장하고 있는 인도의 의약품 원료(API) 부문은 중국산 수입에 대한 의존도를 낮추고 있어, 국내 골판지 공급업체들이 의약품 생산 거점에 더 가까이 진출할 수 있는 여지를 마련하고 있습니다. 투자 규모가 약 2,700억 달러에 달할 것으로 예상되는 미국의 리쇼어링 추진 움직임 속에서 인도가 그중 25%에서 30%를 차지할 것으로 전망되며, 이는 아시아태평양의 포장 현지화를 뒷받침하고 있습니다. 이러한 변화가 지속되는 가운데, 의료용 접이식 카톤의 생산은 수요가 북미, 유럽 및 가장 빠르게 성장하고 있는 아시아의 제약 거점에 여전히 집중되어 있더라도, 지역적으로 보다 균형 잡힌 양상을 보일 가능성이 높습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the folding carton in healthcare market size is expected to increase from USD 6.51 billion in 2025 to USD 6.85 billion in 2026 and reach USD 9.12 billion by 2031, growing at a CAGR of 5.89% over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic Printing, Flexographic Printing, and More), Application (Pharmaceutical Manufacturers, Medical Device Companies, Nutraceutical and Dietary Supplement Firms, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Folding Carton In Healthcare Market Trends and Insights

Growth of Chronic Diseases Requiring Unit-Dose Treatments

The folding carton in healthcare market is seeing steady support from the rise in chronic diseases that require repeat dosing and tighter adherence controls. Unit-dose blister packs and calendar cartons are increasingly used for therapies in diabetes, cardiovascular care, and oncology because these formats make dosing schedules easier to follow and verify at dispensing points. Drug makers are therefore specifying carton structures that can hold 28-day and 90-day blister formats without losing crease strength after repeated opening and closing cycles. Lonza expanded capsule manufacturing capacity at its Rewari facility in India and its Suzhou facility in China, with both sites active in late 2024 and additional lines commissioned in Q3 2025, supporting the wider move toward unit-dose formats in Asia-Pacific. India's pharmaceutical market was projected to rise from USD 61.36 billion in 2024 to USD 130 billion by 2033, while China's market was projected to increase from USD 80.4 billion in 2024 to USD 126.6 billion by 2030, reinforcing long-term demand for folding cartons in the healthcare market. This demand is making volume growth in the folding carton market in healthcare less dependent on pricing cycles and more tied to treatment patterns and adherence-focused packaging design.

Serialization Mandates Driving Larger Carton Real Estate

The folding carton in healthcare market is also being pushed by serialization rules that require more carton space and better print accuracy. The European Union Falsified Medicines Directive has required a unique 2D DataMatrix code on prescription drug packs since 2019, while the U.S. Drug Supply Chain Security Act requires product identifiers, serial numbers, lot numbers, and expiration dates in machine-readable form. Commission Delegated Regulation 2016/161 specified a minimum 8-millimeter-by-8-millimeter DataMatrix area with a 1-millimeter quiet zone on all sides, which can consume 12% to 15% of usable carton surface on compact packs for single-dose vials and pre-filled syringes. As a result, converters in the folding carton market for healthcare are seeing increased demand for premium boards that can withstand sharp codes, prevent ink bleed, and remain flat during inspection and scanning. Amcor launched recycle-ready films at its Italian facility in March 2026 with serialization-compatible coatings that reduced a failure point linked to ink smudging during high-speed verification. The European Medicines Verification System now processes more than 40 million verification events each day, which keeps pressure on the folding carton in healthcare market to maintain tighter print tolerances and more reliable substrate performance.

Volatility in Paperboard Prices

The folding carton in healthcare market faces a clear restraint from unstable pulp and paperboard costs. Northern bleached softwood kraft pulp prices ranged from USD 1,050 to USD 1,350 per metric ton during 2024 and 2025, while energy swings in Scandinavian mills kept production costs under pressure. Solid bleached board and folding boxboard prices usually lag by 60 to 90 days, leaving converters exposed when they have fixed-price supply contracts with pharmaceutical customers. In the folding carton market for healthcare, that lag can compress margins at exactly the point when compliance, print quality, and certification costs are already high. Smaller regional converters are more exposed because they lack backward integration into pulp, and several European specialists lowered utilization to 70%-75% in H2 2025 as pulp prices rose above USD 1,300 per metric ton. Pharmaceutical buyers are responding by adopting dual sourcing and pulp-linked price clauses, which improve supply security but make folding cartons in the healthcare market more price-competitive and less favorable to smaller independent suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Rising Demand for Child-Resistant Pharmaceutical Packaging

- Shift Toward Sustainable and Recyclable Paperboard

- Competition from Flexible Packaging Alternatives

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid bleached sulfate accounted for 43.28% share of the folding carton in healthcare market size in 2025, reflecting its strong opacity, high brightness, and reliable print performance on high-speed offset presses. Folding boxboard is projected to grow at a 7.06% CAGR through 2031, making it the fastest-growing material segment in the folding carton market for healthcare. Fresh-fiber grades are gaining ground because life-cycle assessments from Metsa Board showed carbon emissions 50% to 60% lower than those of coated unbleached kraftboard, while longer fibers also supported 15% to 20% basis-weight reductions without sacrificing puncture resistance. Coated unbleached kraftboard continues to serve outer shipping and secondary pack formats where structural strength matters more than premium printability. White-lined chipboard remains limited to more cost-sensitive nutraceutical applications where recycled content supports sustainability messaging and print requirements are less demanding.

In the healthcare industry, folding carton buyers are increasingly favoring boards that meet both compliance printing requirements and recyclability expectations. Stora Enso's Oulu line, with first deliveries in Q2 2025, shows how suppliers are expanding pharmaceutical-grade consumer board capacity to meet this demand. The European Union's Packaging and Packaging Waste Regulation is also pushing converters away from laminated paperboard structures that use polyethylene or polypropylene layers that reduce recyclability. Water-based barriers are becoming more relevant, but moisture-sensitive biologics still create a performance gap that supports continued use of traditional wax-coated or otherwise more protective grades in some cold-chain uses. That balance means the folding carton in healthcare market is moving toward cleaner and lighter substrates, but not at the expense of drug stability or distribution safety.

Geography Analysis

North America held 34.63% of the folding carton in healthcare market share in 2025, while Asia-Pacific is projected to record the fastest regional CAGR at 6.57% through 2031. North America's position reflects the scale of U.S. pharmaceutical packaging demand and the continued use of bottle-and-carton systems across oral solid dosage categories. The region also remains central to the folding carton in healthcare market because child-resistant standards, serialization compliance, and premium print requirements are tightly enforced in mainstream drug distribution. Asia-Pacific is growing faster because pharmaceutical manufacturing is expanding, local capacity is increasing, and unit-dose formats are becoming more common in large population centers. India's pharmaceutical market was projected to rise from USD 61.36 billion in 2024 to USD 130 billion by 2033, while China's market was projected to increase from USD 80.4 billion in 2024 to USD 126.6 billion by 2030.

Lonza's capacity additions at Rewari, India, and Suzhou, China, show how multinational suppliers are aligning production with the regional shift toward unit-dose packaging and better adherence formats. That matters for the folding carton in healthcare market because secondary packaging demand usually follows dosage-form output and localization of drug manufacturing. Europe remains a critical region even without the top revenue share because it combines strict serialization requirements with strong pressure for recyclable board structures and lower-impact packaging systems. The Falsified Medicines Directive and the Packaging and Packaging Waste Regulation are forcing pharmaceutical buyers in Europe to rethink board selection, print layout, and barrier design at the same time. This combination makes Europe one of the most regulation-shaped parts of the folding carton in healthcare market, especially for suppliers that want to sell premium sustainable substrates.

South America and the Middle East and Africa are expanding more slowly because local folding-carton capacity is limited and healthcare regulations remain more fragmented across countries. Imports from Europe and North America can add 15% to 25% to landed costs in these regions, which affects the competitiveness of locally supplied cartons versus other packaging options. India's active pharmaceutical ingredient sector, valued at USD 13.5 billion in 2024 and growing at 7% CAGR since 2017, is reducing dependence on Chinese imports and opening room for domestic carton suppliers to move closer to pharmaceutical production hubs. The United States' reshoring push, with an estimated USD 270 billion investment pool and India expected to capture 25% to 30% of that allocation, also supports packaging localization in Asia-Pacific. As those shifts continue, the folding carton in healthcare market is likely to become more regionally balanced in production, even if demand remains concentrated in North America, Europe, and the fastest-growing Asian pharmaceutical centers.

- Smurfit WestRock plc

- Graphic Packaging International LLC

- Mayr-Melnhof Karton AG

- International Paper Company

- Stora Enso Oyj

- Georgia-Pacific LLC

- Mondi plc

- Huhtamaki Oyj

- Seaboard Folding Box Co. Inc.

- American Carton Company

- Packaging Corporation of America

- Edelmann GmbH

- CCL Industries Inc.

- Rengo Co., Ltd.

- Sonoco Products Company

- Autajon Group

- Southern Champion Tray, L.P.

- Klabin S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expansion of Food and Beverage Processing Sector

- 4.2.2 Growth of E-commerce Packaging Demand

- 4.2.3 Rising Demand for Sustainable Packaging Solutions

- 4.2.4 Increased Adoption of Digital Printing for Short-Run Cartons

- 4.2.5 Government Excise Tax on Plastic Packaging Spurring Shift Toward Paperboard

- 4.2.6 Rapid Growth of Cloud Kitchen and Meal-Kit Start-ups Requiring Small-Batch Cartons

- 4.3 Market Restraints

- 4.3.1 Volatility in Paperboard Prices

- 4.3.2 Competition From Flexible Packaging Alternatives

- 4.3.3 Limited Domestic Pulp Production Increasing Import Dependence

- 4.3.4 Power Supply Interruptions Elevating Production Costs for Converters

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By Application

- 5.3.1 Pharmaceutical Manufacturers

- 5.3.2 Medical Device Companies

- 5.3.3 Nutraceutical and Dietary Supplement Firms

- 5.3.4 Veterinary Healthcare Providers

- 5.3.5 Other Applications

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 Germany

- 5.4.3.2 United Kingdom

- 5.4.3.3 France

- 5.4.3.4 Italy

- 5.4.3.5 Spain

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 Japan

- 5.4.4.3 South Korea

- 5.4.4.4 India

- 5.4.4.5 Australia and New Zealand

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Nigeria

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Graphic Packaging International LLC

- 6.4.3 Mayr-Melnhof Karton AG

- 6.4.4 International Paper Company

- 6.4.5 Stora Enso Oyj

- 6.4.6 Georgia-Pacific LLC

- 6.4.7 Mondi plc

- 6.4.8 Huhtamaki Oyj

- 6.4.9 Seaboard Folding Box Co. Inc.

- 6.4.10 American Carton Company

- 6.4.11 Packaging Corporation of America

- 6.4.12 Edelmann GmbH

- 6.4.13 CCL Industries Inc.

- 6.4.14 Rengo Co., Ltd.

- 6.4.15 Sonoco Products Company

- 6.4.16 Autajon Group

- 6.4.17 Southern Champion Tray, L.P.

- 6.4.18 Klabin S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment