|

시장보고서

상품코드

2063778

말레이시아의 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Malaysia Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

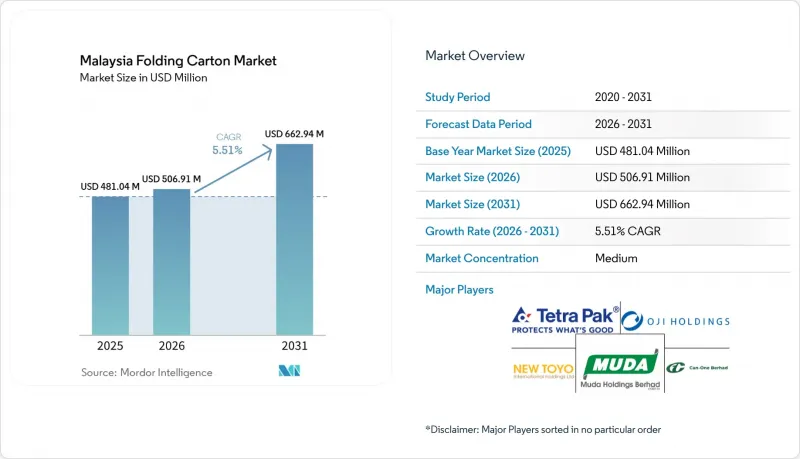

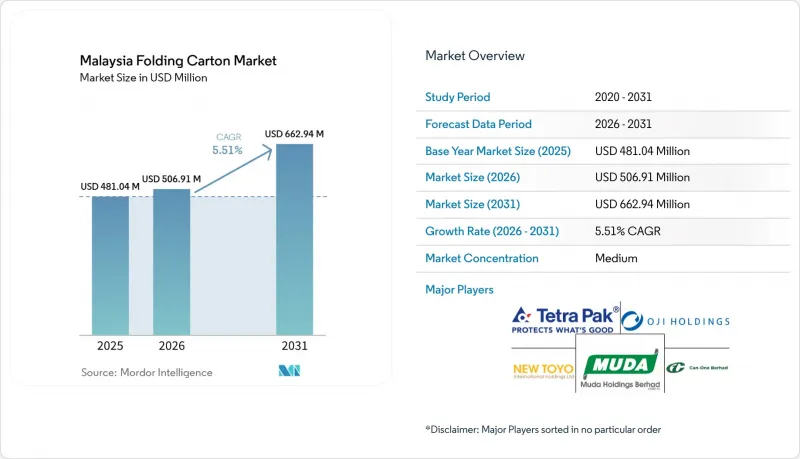

Mordor Intelligence에 의하면, 말레이시아의 접이식 카톤 시장 규모는 2025년 4억 8,104만 달러로 평가되었습니다. 2026년 5억 691만 달러에서 2031년까지 6억 6,294만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 5.51%를 나타낼 것으로 예측됩니다.

본 보고서는 원료 유형(고형 표백 황산 펄프, 접이식 카톤, 코팅 미표백 크라프트지 등), 인쇄 기술(오프셋 인쇄, 플렉소 인쇄, 디지털 인쇄, 그라비아 인쇄 등), 최종 사용자 산업(식품 및 음료, 헬스케어 및 의약품, 퍼스널케어 및 화장품, 전기 및 전자기기 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

말레이시아의 접이식 카톤 시장 동향 및 인사이트

고급 포장 상품의 보급 확대

프리미엄 화장품, 과자, 헬스케어 제품 수요가 확대됨에 따라, 브랜드 소유주들이 엠보싱 가공, 메탈릭 잉크, 촉감 바니시를 적용할 수 있는 골판지를 요구하게 되면서, 기판의 사양이 재정의되고 있습니다. 네슬레 말레이시아의 ‘킷캣 레디 투 드링크’ 음료와 휴대용 ‘매기 보울’은 고속 충전 라인에서도 브랜드 이미지를 유지할 수 있는 내유성 코팅으로 전환한 대표적인 사례입니다. 설문 응답자의 60-70%를 차지하는 도시 지역 소비자들은 가격에 대한 민감도가 여전히 높은 상황에서도 재활용 가능성에 관한 정보를 공개하는 브랜드를 선호하는 경향을 보이고 있습니다. 따라서 접이식 판지보다 15-20% 비싼 SBS(고형 표백 황산 펄프 판지)는 비용 측면에서의 역풍에도 불구하고 고급 제품 시장에서 점유율을 유지하고 있습니다. 국내무역부의 2026년 광고 규정은 재활용 가능 여부를 명확히 표시하도록 의무화하고 있으며, 이로 인해 인증을 받지 못한 가공업체들 시장 철수가 가속화되고 있습니다. 고급 지향적인 포지셔닝과 규제에 따른 지원이 맞물리면서, 인증된 원자재에 고해상도 그래픽을 인쇄할 수 있는 가공업체들이 활용할 수 있는 가치의 범위가 확대되고 있으며, 이는 말레이시아의 접이식 카톤 시장의 상승 추세를 뒷받침하고 있습니다.

지속 가능한 포장 기준을 위한 정부의 추진

말레이시아의 ‘순환형 경제 청사진 2025-2035’에 따르면, 2030년까지 확대 생산자 책임(EPR) 제도가 자발적 참여에서 의무화로 전환되며, 컨버터는 조달, 에너지 소비량, 재활용 실적을 추적해야 합니다. 위반 시 건당 5만 링깃(1만 2,337달러)의 벌금이 부과됩니다. Lazada와 Shopee는 2026년 7월부터 기준을 충족하지 않는 포장에 대해 3%의 추가 요금을 부과함으로써 이러한 압박을 더욱 강화했고, 인증을 받지 않은 공급업체에 대한 진입 장벽을 즉시 높였습니다. Box-Pak Malaysia는 3개국에 걸친 CoC(생산 및 유통 과정 관리) 시스템 인증을 획득함으로써 이러한 규제 변경에 선제적으로 대응하여, 다국적 FMCG(일용소비재) 기업의 입찰에서 그룹에 유리한 입지를 확보했습니다. 2025년 지정폐기물 규정에 따른 잉크 슬러지의 재분류는 폐쇄형 수처리 시스템에 대한 투자를 더욱 촉진하고 있습니다. 이러한 조치들이 맞물리면서 거래량은 자본력이 있는 대기업으로 집중되고 있으며, 말레이시아의 접이식 카톤 시장에서 지속가능성은 더 이상 양보할 수 없는 필수 요건으로 자리 잡고 있습니다.

변동이 심한 폐지 수입 가격

2025년, 혼합지 등급의 거래 가격은 톤당 180-260달러 사이에서 등락했으며, 이 44%의 가격 차이로 인해 분기별 계약을 체결한 가공업체의 이익률은 3-5퍼센트포인트 감소했습니다. 국내 제지 회사들이 섬유를 대량으로 사들인 탓에, 미국에서 동남아시아로 수출되는 물량은 2023년 180만 톤에서 2025년에는 120만 톤으로 감소했습니다. 2025년 1분기, OCC 현물 가격이 28% 급등한 후 하락세로 돌아서면서, 60일 결제 조건으로 거래하는 가공업체들의 재고 평가를 복잡하게 만들었습니다. 징싱(Jingxing)의 새로운 공장이 버진 펄프 부족 현상을 완화하고는 있지만, 화이트 라이닝 칩보드의 대부분은 여전히 수입 폐지에 의존하고 있습니다. 국내 원자재 공급이 더욱 확대될 때까지, 가격의 급등락은 말레이시아의 접이식 카톤 시장의 가격 상승을 계속 억제할 것입니다.

부문별 분석

접이식 카톤은 그 강성과 브랜드 식품, 의약품, 화장품 라인에서의 높은 인쇄 재현성을 바탕으로, 2025년 말레이시아의 접이식 상자 시장에서 41.71%의 점유율을 유지했습니다. 한편, 100% 재생 섬유로 제조되는 화이트 라이닝 칩보드는 비용 효율성을 중시하는 가정용품 브랜드와 전자상거래 사업자들이 20-25%에 달하는 단가 경쟁력을 높이 평가하고 있어, 연평균 성장률(CAGR) 6.41%로 성장할 전망입니다. 말레이시아의 화이탈리아너 골판지 시장은 Nextgreen IOI사의 야자 섬유 펄프가 ISO 22002-4 : 2025 이행 기준을 준수하는 등급으로 배합되는 대로 급속히 확대될 전망입니다. 고급 화장품용으로는 여전히 고형 표백 황산 펄프가 원료로 선택되고 있으며, 스칸디나비아와 북미에 대한 수입 의존으로 인해 입고 비용이 상승하고 있음에도 불구하고 프리미엄 위치를 유지하고 있습니다. 한편, 코팅되지 않은 미표백 크라프트지는 자연스러운 갈색 색상이 지속가능성 메시지와 잘 어울릴 뿐만 아니라 운송 중량을 최대 10%까지 줄일 수 있어, 상온 보관 식품 분야에서 시장 점유율을 확대되고 있습니다. 하이브리드 마이크로 플루트 라미네이트는 틈새 시장이긴 하지만, 내낙하성이 가격보다 더 중요하게 여겨지는 전자기기 분야에서 점유율을 점차 확대되고 있습니다.

가공업체는 비용 균형을 맞추면서 브랜드가 요구하는 냄새, 이물질, 광도에 관한 기준을 충족하기 위해 버진 펄프와 재생 펄프를 혼합하고 있습니다. Lazada의 2026년 FSC 인증 규정은 재생 원자재에 대한 수요를 확고히 하는 한편, CoC(생산 및 유통 과정 관리) 감사를 받지 않은 제지 공장을 도태시키고, ISO 14001 인증을 취득한 기업에 수요를 집중시키는 결과를 가져올 것입니다. 예측 기간 동안, 국내 펄프 공급 증가로 인해 접이식 판지와 화이트 라이닝 칩보드의 비용 격차는 줄어들고, 후자의 가격 경쟁력은 약화되겠지만, 재생 소재 기반 원료는 말레이시아의 접이식 카톤 시장의 구조적 성장 동력으로서의 입지를 공고히할 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the malaysia folding carton market size is projected to expand from USD 481.04 million in 2025 and USD 506.91 million in 2026 to USD 662.94 million by 2031, registering a CAGR of 5.51% between 2026 to 2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Malaysia Folding Carton Market Trends and Insights

Growing Adoption of Premium Packaged Goods

Demand for premium cosmetics, confectionery, and healthcare SKUs is reshaping substrate specifications as brand owners insist on cartons that accept embossing, metallic inks, and tactile varnishes. Nestle Malaysia's ready-to-drink KitKat beverages and portable Maggi bowls exemplify the shift toward grease-resistant coatings that preserve brand imagery under high-speed filling lines. Urban consumers, 60-70% of survey respondents, now favor brands that publish recyclability information, even when price sensitivity remains high. Solid bleached sulfate board, priced at a 15-20% premium to folding boxboard, is therefore holding share in luxury goods despite cost headwinds. The Ministry of Domestic Trade's 2026 advertising code compels clear labeling of recyclability, accelerating the exit of non-certified converters. Collectively, prestige positioning and regulatory nudges are expanding the value pool available to converters capable of delivering high-definition graphics on certified substrates, reinforcing upward momentum in the Malaysian folding carton market.

Government Push for Sustainable Packaging Standards

Malaysia's Circular Economy Blueprint 2025-2035 transitions from voluntary to mandatory extended producer responsibility by 2030, requiring converters to track sourcing, energy intensity, and recycling outcomes, or face MYR 50,000 (USD 12,337) in fines per violation. Lazada and Shopee magnified the pressure by levying a 3% surcharge on non-compliant packaging starting July 2026, instantly raising the entry bar for uncertified suppliers. Box-Pak Malaysia pre-empted the rule change by certifying chain-of-custody systems across three countries, giving the group pole position for multinational FMCG tenders. Ink sludge re-classification under the 2025 scheduled-waste rules is further motivating investments in closed-loop water treatment. In combination, these measures channel volume toward large, well-capitalized firms and cement sustainability as a non-negotiable qualifier within the Malaysian folding carton market.

Volatile Recovered Paper Import Prices

Mixed-paper grades traded between USD 180 and USD 260 per tonne in 2025, a 44% spread that erased 3-5 percentage-point margins for converters locked into quarterly contracts. U.S. shipments to Southeast Asia fell from 1.8 million tonnes in 2023 to 1.2 million tonnes in 2025 as domestic mills hoarded fiber. Spot OCC prices spiked 28% in Q1 2025 before retreating, complicating inventory valuation for converters on 60-day terms. While Jingxing's new mill eases virgin-fiber tightness, most white-lined chipboard still relies on imported recovered paper. Until additional domestic furnish arrives, price turbulence will continue to cap upside in the Malaysia folding carton market.

Other drivers and restraints analyzed in the detailed report include:

- Surge in Quick-Commerce Grocery Delivery

- Capacity Expansion by Domestic Paper Mills

- Shortage of Skilled Press Operators

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard retained 41.71% of Malaysia's folding carton market share in 2025 on the back of its stiffness and print fidelity for branded food, pharma, and cosmetic lines. Yet white-lined chipboard, built from 100% recycled fiber, is on track for a 6.41% CAGR as cost-conscious household-goods brands and e-commerce shippers embrace its 20-25% unit-price advantage. The Malaysian folding carton market for white-lined chipboard is poised to expand sharply once Nextgreen IOI's palm-fiber pulp is blended into grades that comply with ISO 22002-4:2025 migration norms. Solid bleached sulfate remains the substrate of choice for prestige cosmetics, sustaining premium positioning even though import dependency from Scandinavia and North America inflates landed cost. Coated unbleached kraft is capturing ambient grocery items where its natural brown look aligns with sustainability messaging and trims freight weight by up to 10%. Hybrid micro-flute laminates, although niche, are carving a share in electronics where drop resistance trumps price.

Converters are mixing virgin and recycled furnish to hit brand-mandated barriers on odor, migration, and brightness while juggling cost. Lazada's 2026 FSC-certification rule cements recycled-content demand but simultaneously weeds out mills lacking chain-of-custody audits, concentrating volume with ISO 14001 holders. Over the forecast window, domestic pulp additions should narrow the cost gap between folding boxboard and white-lined chipboard, softening the latter's price edge yet cementing recycled substrates as the structural growth engine of the Malaysian folding carton market.

List of Companies Covered in this Report:

- Muda Holdings Berhad

- Oji Holdings Corporation

- Can-One Berhad

- Tetra Pak Malaysia Sdn Bhd

- New Toyo International Holdings Ltd

- Orient Press Sdn Bhd

- KYM Holdings Berhad

- Ornapaper Industry (M) Sdn Bhd

- Rengo Co., Ltd.

- Tat Seng Packaging Group Ltd

- Kian Joo Can Factory Berhad

- Box-Pak (Malaysia) Bhd

- Lamipak (Malaysia) Sdn Bhd

- Paper-Based Packaging Sdn Bhd

- Mondi plc

- SCG Packaging Public Company Limited

- Hexachase Packaging Sdn Bhd

- Printpack Asia Sdn Bhd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Premium Packaged Goods

- 4.2.2 Government Push for Sustainable Packaging Standards

- 4.2.3 Surge in Quick-Commerce Grocery Delivery

- 4.2.4 Capacity Expansion by Domestic Paper Mills

- 4.2.5 AI-Enabled Quality Inspection Systems

- 4.2.6 Near-Shoring of Regional Consumer-Goods Production

- 4.3 Market Restraints

- 4.3.1 Volatile Recovered Paper Import Prices

- 4.3.2 Shortage of Skilled Press Operators

- 4.3.3 Rising Popularity of Flexible Pouches for Beverage

- 4.3.4 Logistic Bottlenecks at Port Klang

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-Commerce and Retail-Ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Muda Holdings Berhad

- 6.4.2 Oji Holdings Corporation

- 6.4.3 Can-One Berhad

- 6.4.4 Tetra Pak Malaysia Sdn Bhd

- 6.4.5 New Toyo International Holdings Ltd

- 6.4.6 Orient Press Sdn Bhd

- 6.4.7 KYM Holdings Berhad

- 6.4.8 Ornapaper Industry (M) Sdn Bhd

- 6.4.9 Rengo Co., Ltd.

- 6.4.10 Tat Seng Packaging Group Ltd

- 6.4.11 Kian Joo Can Factory Berhad

- 6.4.12 Box-Pak (Malaysia) Bhd

- 6.4.13 Lamipak (Malaysia) Sdn Bhd

- 6.4.14 Paper-Based Packaging Sdn Bhd

- 6.4.15 Mondi plc

- 6.4.16 SCG Packaging Public Company Limited

- 6.4.17 Hexachase Packaging Sdn Bhd

- 6.4.18 Printpack Asia Sdn Bhd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment