|

시장보고서

상품코드

2063709

스페인의 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Spain Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

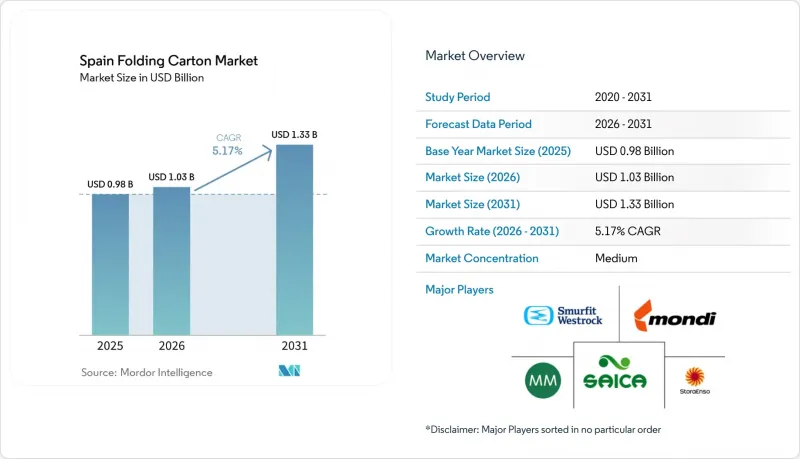

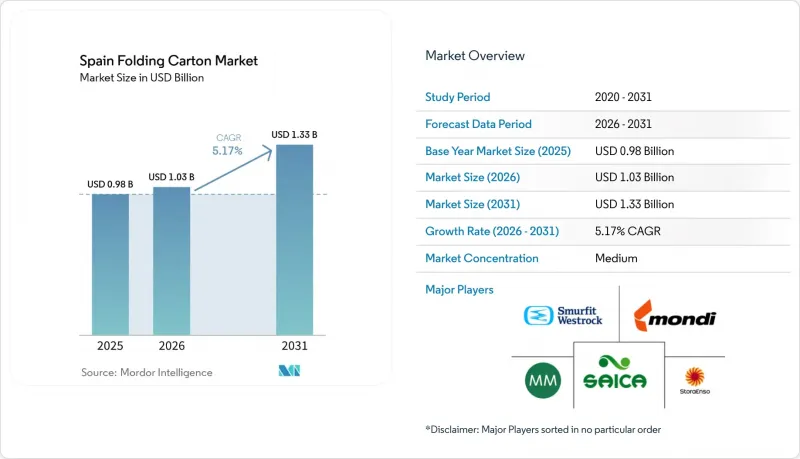

Mordor Intelligence에 의하면, 스페인의 접이식 카톤 시장 규모는 2026년 10억 3,000만 달러에서 2031년까지 13억 3,000만 달러로 확대되어 2026-2031년 CAGR은 5.17%를 나타낼 것으로 예측됩니다.

본 보고서는 원료 유형(무표백 황산 펄프, 접이식 골판지, 코팅 무표백 크라프트지, 화이트라인 칩보드 등), 인쇄 기술(오프셋 인쇄, 플렉소 인쇄, 디지털 인쇄 등), 최종 사용자 산업(식품 및 음료, 헬스케어 및 의약품, 퍼스널케어 및 화장품 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

스페인의 접이식 카톤 시장 동향 및 인사이트

지속 가능한 포장에 대한 수요 증가

재활용 가능한 소재에 대한 소비자의 선호도와 소매업체의 규제로 인해, 스페인에서는 섬유 기반 1차 및 2차 포장재로의 전환이 가속화되고 있습니다. EU의 포장 및 포장 폐기물 규정에 따르면, 2030년까지 사용된 재활용 소재를 35% 함유해야 할 의무가 부과되어 있으며, 이에 따라 브랜드 소유자들은 적절한 크기의 배송에 대응할 수 있도록 접이식 상자를 재설계하거나, 혼합 소재로 인한 장벽을 해소해야 하는 상황에 직면해 있습니다. ALASKA SMART 및 ALASKA KRAFT와 같은 고품질 버진 펄프 등급은 가벼운 무게에도 불구하고 점자 인쇄가 가능하며, 식품 접촉 적합성을 유지할 수 있는 대안으로 판매되고 있습니다. 업스트림 공정에서는 Papkot과 같은 코팅 스타트업 기업들이 플라스틱이 없는 배리어 소재를 상품화하기 위한 자금 조달을 추진하고 있으며, 이는 스페인의 접이식 카톤 시장에서 지속가능성 노력을 강화하는 더 심층적인 혁신 주기의 조짐으로 보입니다.

2차 포장이 필요한 전자상거래 출하량 증가

2025년에는 조리 식품의 출하량이 7.6% 증가하여 소매용 골판지 상자 수요를 끌어올렸습니다. 특히 메르카도나(Mercadona)에서는 즉석 식품의 품목 구색이 24% 확대되어, 현재 구매자의 40%에게 도달하고 있습니다. EU 규제로 인해 공극률이 50%로 제한됨에 따라, 온라인 판매업체들은 골판지 운송 상자를 콤팩트한 접이식 상자로 대체해야 할 필요에 직면해 있으며, 일체형 완충재 디자인에 대한 관심이 높아지고 있습니다. 디지털 플랫폼을 통해 신속한 디자인 변경에 대응할 수 있는 컨버터는 다품종 소량 생산 계약을 수주하고 있으며, 2025년 9월에 출시된 사이카 프레시(Saica Fresh)의 MAP 대응 카톤 솔루션이 그 대표적인 사례입니다.

변동이 심한 재생 판지 가격

2025년 4월 폐지(OCC) 가격이 톤당 20-30유로(톤당 22-33달러)로 급등함에 따라, 가공업체의 EBITDA가 압박을 받게 되었고, 스페인의 접이식 카톤 시장은 업스트림 시장의 가격 변동에 더 취약해졌습니다. 사무용지 회수량 감소와 지정학적 요인으로 인한 운송 차질로 인해 SOP(단섬유 펄프) 공급이 부족해지면서, 제지 업체들은 높은 운임 프리미엄을 지불하고 스칸디나비아산 버진 펄프를 수입함으로써 위험을 회피할 수밖에 없는 상황에 처해 있습니다. 이러한 상황은 시장 내에서 비용 효율성을 유지하는 데 따르는 어려움이 커지고 있음을 여실히 보여주고 있습니다.

부문별 분석

2025년, 스페인의 접이식 카톤 시장에서 고형 표백 황산 펄프(SOP)는 34.78%의 점유율을 차지했습니다. 이는 그 백색도, 무취성, 그리고 의약품 규정을 준수함으로써 확보된 지위입니다. 이 부문은 화장품, 과자, 블리스터 포장용 접이식 카톤 시장에서 프리미엄 가격대를 확보하고 있어, OCC 가격 변동으로부터 가공업체를 보호하고 있습니다. 코팅되지 않은 미표백 크라프트지는 유기농 식품 및 수제 빵 브랜드들이 그 자연스러운 갈색의 미관과 내유성을 높이 평가함에 따라, 2031년까지 연평균 성장률(CAGR) 7.34%로 가장 빠르게 성장하고 있습니다. 접이식 박스용 보드와 화이트라인 칩보드는 규제에 따른 재생재 함유율 기준 상향으로 인해 탈색 공정에 대한 투자가 증가하고 있음에도 불구하고, 비용 효율성이 중시되는 대량 생산 냉동식품 및 시리얼 분야 수요를 충족시키고 있습니다.

스트라 엔소(Stora Enso)사의 75만 톤 규모 PM6 재건과 같은 대규모 업스트림 프로젝트를 통해, 스페인 제지업체에 대한 코팅지의 안정적인 공급이 확보되고 있습니다. 특수 코팅지, 마이크로플루트 골판지, 메탈라이즈 보드는 고급 증류주나 와인 용도로 사용되고 있지만, 비금속화 요건이 강화됨에 따라 그 성장세는 둔화되고 있습니다. 스페인의 접이식 카톤 시장에서 틈새 원자재 시장 규모는 여전히 작지만, 위조 개봉 방지 캡 및 스마트 라벨 통합에 대한 수요가 증가함에 따라, 특히 고성장 분야인 GLP-1 요법 포장 분야에서 고품질 버진 펄프가 확고한 우위를 유지하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the spain folding carton market size is projected to expand from USD 1.03 billion in 2026 to USD 1.33 billion by 2031, registering a 5.17% CAGR over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Flexographic Printing, Digital Printing, and More), and End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Spain Folding Carton Market Trends and Insights

Growing Demand for Sustainable Packaging

Consumer preference for recyclable materials and retailer mandates are accelerating Spain's shift toward fiber-based primary and secondary packs. The EU Packaging and Packaging Waste Regulation requires 35% post-consumer recycled content by 2030, pushing brand owners to redesign folding cartons for right-sized deliveries and to eliminate mixed-material barriers. Premium virgin-fiber grades such as ALASKA SMART and ALASKA KRAFT are marketed as lighter yet Braille-ready options that keep food-contact approvals intact. Upstream, coating start-ups like Papkot are securing capital to commercialize plastic-free barriers, signaling a deeper innovation cycle that reinforces the Spanish folding carton market's sustainability narrative.

Rising E-commerce Shipments Requiring Secondary Packaging

Prepared-food volumes grew 7.6% in 2025, driving up retail-ready carton demand, particularly from Mercadona, whose ready-to-eat range expanded 24% and now reaches 40% shopper penetration. The EU regulation capping void space at 50% forces online merchants to replace corrugated shippers with compact folding cartons, spurring interest in integrated cushioning designs. Converters that can deliver rapid artwork changes through digital platforms are winning high-mix, low-volume contracts, as exemplified by Saica Fresh's MAP-compatible carton solution launched in September 2025.

Volatile Recycled Paperboard Prices

April 2025 OCC spikes of EUR 20-30 per metric ton (USD 22-33 per metric ton) squeezed converter EBITDA, exposing the Spain folding carton market to upstream volatility. Declining office paper collection and geopolitical freight disruptions have tightened SOP supply, compelling mills to hedge by importing Scandinavian virgin fiber at higher freight premiums. This situation underscores the growing challenges in maintaining cost efficiency within the market.

Other drivers and restraints analyzed in the detailed report include:

- Stringent EU and Spanish Regulations on Single-Use Plastics

- Cost Advantages of Lightweight Board for Logistics

- Competition from Flexible Packaging in Snack Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Solid Bleached Sulfate held 34.78% of the Spain folding carton market share in 2025, a position secured by its white optics, odor neutrality, and pharmaceutical compliance credentials. The segment captures premium price points in cosmetics, confectionery, and blister folding cartons, cushioning converters against OCC price swings. Coated Unbleached Kraft is scaling fastest at a 7.34% CAGR through 2031, as organic food and artisan bakery brands adopt its natural-brown aesthetics and grease resistance. Folding Boxboard and White Line Chipboard satisfy high-volume frozen-food and cereal categories where cost efficiency prevails, even as regulatory recycled-content thresholds raise de-inking investments.

Large upstream projects, such as Stora Enso's 750,000-metric ton PM6 rebuild, ensure a stable supply of coated grade for Spanish converters. Coated specialty grades, micro-flute corrugated, and metalized boards serve luxury spirits and wine but face stricter demetallization requirements, slowing their momentum. The Spain folding carton market size for niche substrates remains modest, yet heightened demand for tamper-evident closures and smart-label integration is giving premium virgin fibers a defensible edge, particularly in high-growth GLP-1 therapy packaging.

List of Companies Covered in this Report:

- Smurfit WestRock plc

- Mayr-Melnhof Karton AG

- Graphic Packaging International LLC

- International Paper Company

- Saica Pack SL

- Edelmann Group

- Mayr-Melnhof Karton AG

- Stora Enso Oyj

- Autajon Group

- Fedrigoni Group

- Hinojosa Packaging Group

- Cartonajes VIR

- Mondi plc

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Sustainable Packaging

- 4.2.2 Rising E-commerce Shipments Requiring Secondary Packaging

- 4.2.3 Stringent EU and Spanish Regulations on Single-Use Plastics

- 4.2.4 Cost Advantages of Lightweight Board for Logistics

- 4.2.5 Rapid Expansion of Spain's Chilled Ready-Meals Segment

- 4.2.6 Digitization of Supply Chains Enabling Short Print Runs

- 4.3 Market Restraints

- 4.3.1 Volatile Recycled Paperboard Prices

- 4.3.2 Competition from Flexible Packaging in Snack Formats

- 4.3.3 Limited Domestic Hardwood Pulp Availability

- 4.3.4 Brand Owner Reluctance Toward High-CapEx Digital Presses

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Smurfit WestRock plc

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Graphic Packaging International LLC

- 6.4.4 International Paper Company

- 6.4.5 Saica Pack SL

- 6.4.6 Edelmann Group

- 6.4.7 Mayr-Melnhof Karton AG

- 6.4.8 Stora Enso Oyj

- 6.4.9 Autajon Group

- 6.4.10 Fedrigoni Group

- 6.4.11 Hinojosa Packaging Group

- 6.4.12 Cartonajes VIR

- 6.4.13 Mondi plc

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment