|

시장보고서

상품코드

2063764

미국의 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)United States Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

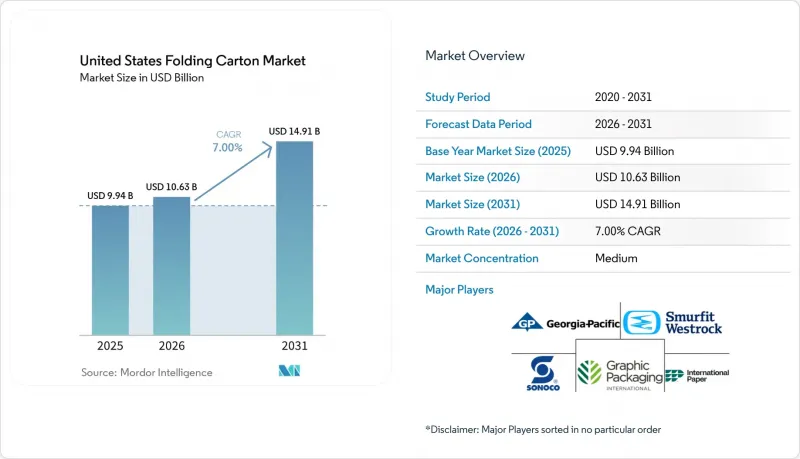

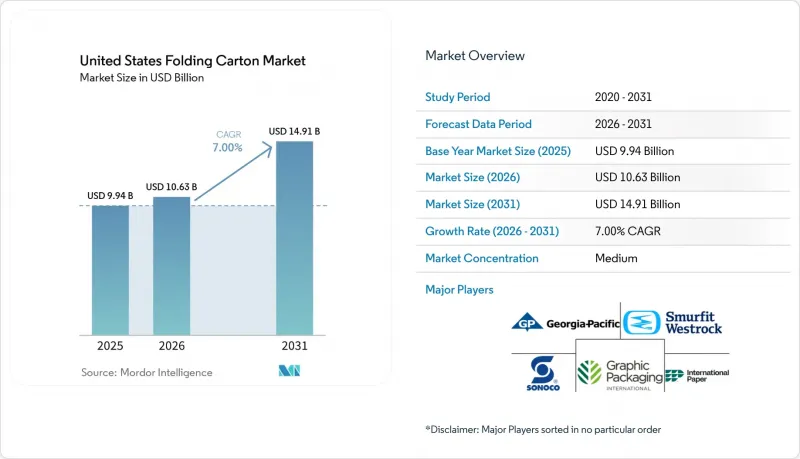

Mordor Intelligence에 의하면, 미국의 접이식 카톤 시장 규모는 2025년에 99억 4,000만 달러로 평가되었습니다. 2026년 106억 3,000만 달러에서 2031년까지 149억 1,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 7%를 나타낼 전망입니다.

본 보고서는 원료 유형(고형 표백 황산 펄프, 접이식 카톤, 코팅 미표백 크라프트지 등), 인쇄 기술(오프셋 인쇄, 플렉소 인쇄, 디지털 인쇄, 그라비아 인쇄 등), 최종 사용자 산업(식품 및 음료, 헬스케어 및 의약품, 퍼스널케어 및 화장품, 전기 및 전자기기 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국의 접이식 카톤 시장 동향 및 분석

전자상거래의 급속한 성장이 경량 보호 포장 수요를 견인하고 있습니다.

상자와 골판지 상자는 모든 전자상거래 포장 형태의 40%를 차지하고 있으며, 각 골판지 가공업체들은 매장 진열과 배송 네트워크 모두에 견딜 수 있는 적절한 크기의 구조를 설계해야 합니다. 여분의 공간을 줄여주는 자동화 시스템 덕분에 북미에서는 평균 포장 중량이 43% 감소했고, 배송 중 파손도 24% 줄었습니다. 이에 따라 ISTA 인증을 받은 가장자리와 보강된 모서리 홈이 적용된 접이식 상자에 대한 수요가 증가하고 있습니다. 현재 디지털 인쇄기를 통해 로열티 사이트로 연결되는 가변 QR 코드를 인쇄할 수 있게 되어, 코드를 스캔하는 소비자의 50%와 2027년까지 2차원 바코드를 전면적으로 도입할 계획인 소매업체의 요구를 충족시키고 있습니다. 이러한 자동화, 추적성, 옴니채널 대응이라는 장점이 결합됨에 따라, 미국의 접이식 카톤 시장은 범용 등급에서 설계된 형식으로 전환되고 있습니다.

지속 가능하고 재활용 가능한 포장 솔루션에 대한 수요 증가

7개 주가 생산자에게 회수 및 재활용 비용을 부담하도록 의무화하는 EPR(확대 생산자 책임)법을 제정했습니다. 미네소타주는 2032년까지 모든 포장재를 재활용 가능, 재사용 가능, 리필 가능 또는 퇴비화 가능하도록 의무화하고, 2031년까지 시스템 비용의 최소 90%를 조달하도록 규정하고 있습니다. 워싱턴주의 프로그램에 따르면, 2032년까지 90%의 상환을 단계적으로 도입하고, 2029년부터 재사용 인프라에 500만 달러를 배정할 예정입니다. 이러한 법률은 검증 가능한 회수율을 갖춘 재생 섬유 골판지에 대해 우대 조치를 제공하는 환경 조정 요금을 부과하고 있으며, 브랜드 소유자들은 버진 표백 판지 대신 사용된 소비자 섬유가 더 많이 포함된 접이식 판지로 전환해야 하는 상황에 처해 있습니다. 오리건주에서는 2026년, 요금 투명성과 관련된 헌법적 쟁점이 제기되면서 생산자들의 비용 전가 전략에 대한 심사가 강화되었습니다. 그러나 장기적인 추세로 볼 때 여전히 재활용이 가능한 코팅지나 얇은 두께의 판지가 유리합니다. 그 결과, 지속 가능한 원자재 선정은 현재 재무 및 규정 준수 문제와 밀접하게 연관되어 있으며, 미국의 접이식 카톤 시장에서 재생지 골판지에 대한 지속적인 호재가 이어지고 있습니다.

폐지 및 원지 가격의 변동

사용된 골판지(OCC) 가격은 2025년 11월 톤당 평균 44달러로 전년 대비 41% 하락했으나, 제지 업체들이 봄철 가동 중단을 대비해 물량을 비축함에 따라 2026년 1월에는 톤당 1달러로 반등했습니다. 고품질 재활용 펄프의 생산자물가지수는 2025년 11월 77.411에서 2025년 10월 87.545로 급등했다가, 2026년 2월까지 82.723으로 되돌아갔습니다. 이는 계약 예산을 왜곡하는 월별 비용 변동을 여실히 드러내고 있습니다. 중국에서 습식 및 건식 재생 펄프 수입량 공개를 의무화하는 정책 전환으로 인해 수출에 미치는 파급 효과가 줄어들고, 국내 가격의 불확실성이 커지고 있습니다. 접이식 카톤 제조업체들은 일반적으로 고객에 대한 가격 조정을 3-6개월의 시차를 두고 실시하기 때문에 생산 주기의 중간에 폐지(OCC)나 원지 펄프 가격이 급등할 때마다 이익률이 압박을 받게 됩니다. 이러한 지속적인 가격 변동은 미국의 접이식 카톤 업계의 전략적 조달을 복잡하게 만들고, 장기적인 가격 약정을 저해하고 있습니다.

부문별 분석

2025년, 미국의 접이식 카톤 시장에서 고체 표백 황산 펄프(SBS)는 38.21%의 시장 점유율을 차지했습니다. 이는 완벽한 잉크 고정력과 식품 접촉용 표면 인증이 필요한 식품, 음료, 의약품 SKU에 힘입은 결과입니다. 접이식 박스 보드는 재활용 소재 사용을 장려하는 EPR(확대 생산자 책임) 요금 체계와 톤당 44달러라는 가격의 풍부한 폐지(OCC)에 힘입어, 연평균 성장률(CAGR) 8.19%로 시장 전체를 상회하는 성장이 예상됩니다. 표백하지 않은 크라프트지는 내유성이 뛰어나고 자연스러운 질감이 요구되는 틈새 시장에 적합하며, 한편 화이트 라인 칩보드는 비식품 분야의 2차 포장 분야에서 비용 경쟁력을 발휘하고 있습니다. 2025년에는 그래픽 패키징(Graphic Packaging)사의 웨코 공장 생산 확대가 미네소타주와 텍사스주에서의 폐쇄분을 상쇄함에 따라, 재생 보드의 순생산 능력은 소폭 증가했습니다. 무게 감소를 권장하는 미네소타주의 EPR 에코모듈레이션 규정에 따라, 각 브랜드는 더 얇은 접이식 상자용 보드로 전환하고 있으며, 버진 표백 원료에서 벗어나려는 추세가 더욱 강해지고 있습니다.

고품질 재생 원료를 확보하고 있는 컨버터들은 가격을 견조하게 유지하고 있습니다. 이는 재생 원료 함유량에 연동되는 EPR(확대 생산자 책임) 수수료로 인해 버진 등급과의 비용 차이가 줄어들고 있기 때문입니다. Packaging Corporation of America가 Greif의 재활용 공장을 인수함에 따라, 해당 기업의 재활용 소재 비율은 20%에서 30%로 상승했으며, 비용 대비 효율이 높은 원자재로의 전략적 전환이 부각되었습니다. 이러한 섬유 배합 조정은 특히 비용 구조가 총 납품 비용에 직접적인 영향을 미치는 규제가 엄격한 연안 주에서 미국의 접이식 카톤 시장이 앞으로도 계속해서 재생 섬유 쪽으로 기울어질 것임을 시사합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.26According to Mordor Intelligence, the united states folding carton market size was valued at USD 9.94 billion in 2025 and is estimated to grow from USD 10.63 billion in 2026 to reach USD 14.91 billion by 2031, at a CAGR of 7% during the forecast period (2026-2031).

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, and More), Printing Technology (Lithographic, Flexographic, Digital, Gravure, and More), End-User Industry (Food and Beverage, Healthcare/Pharmaceuticals, Personal Care and Cosmetics, Electrical and Electronics, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Folding Carton Market Trends and Insights

E-Commerce Boom Driving Demand for Lightweight Protective Packaging

Boxes and cartons account for 40% of all e-commerce packaging formats, compelling converters to engineer right-sized structures that survive both shelf display and parcel networks. Automated systems that trim void space have cut average package weight by 43% in North America and lowered shipping damage by 24%, pushing demand toward folding cartons with ISTA-validated edges and reinforced corner scores. Digital presses now add variable QR codes that link to loyalty sites, meeting the 50% of consumers who scan codes and the retailers who plan universal 2D barcode acceptance by 2027. This convergence of automation, traceability, and omnichannel aesthetics is steering the United States folding cartons market away from commodity grades toward engineered formats.

Increasing Demand for Sustainable and Recyclable Packaging Solutions

Seven states enacted EPR statutes requiring producers to finance collection and recycling, with Minnesota mandating that all packaging be recyclable, reusable, refillable, or compostable by 2032 and to fund at least 90% of system costs by 2031. Washington's program phases in 90% reimbursement by 2032 and earmarks USD 5 million for reuse infrastructure starting in 2029. These laws impose eco-modulated fees that privilege recycled-fiber cartons with verifiable recovery rates, driving brand owners to swap virgin bleached board for folding boxboard containing higher post-consumer fiber. Oregon's 2026 constitutional challenge over fee transparency has heightened producer scrutiny of cost pass-through strategies, yet the long-term trajectory still favors recyclable-coated barriers and lightweight calipers. As a result, sustainable substrate selection is now intertwined with finance and compliance, giving recycled paperboard a lasting tailwind in the United States folding cartons market.

Volatility in Recovered Paper and Virgin Pulp Prices

Old corrugated containers (OCC) averaged USD 44 per ton in November 2025, sinking 41% from the prior year before rebounding USD 1 per ton in January 2026 as mills pre-bought for spring downtime. The Producer Price Index for high-grade recyclable pulp whipsawed from 77.411 in November 2025 to 87.545 in October 2025 and back to 82.723 by February 2026, underscoring monthly cost swings that distort contract budgeting. Chinese policy shifts requiring disclosure of wet versus dry recycled pulp imports cut export pull-through, intensifying domestic price uncertainty. Because folding carton converters typically adjust customer pricing with a 3- to 6-month lag, margin compression surfaces whenever OCC or virgin pulp spikes mid-cycle. Persistent volatility complicates strategic sourcing and discourages long-term price commitments in the United States folding carton industry.

Other drivers and restraints analyzed in the detailed report include:

- Premiumization in Food and Beverage Boosting High-Quality Printing

- State-Level Extended Producer Responsibility Legislation Accelerating Carton Adoption

- Capacity Expansion of Flexible Packaging Displacing Folding Cartons

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The United States folding carton market size for solid bleached sulfate captured 38.21% market share in 2025, underpinned by food, beverage, and pharmaceutical SKUs that require flawless ink laydown and certified food-contact surfaces. Folding boxboard is projected to outpace the overall market at an 8.19% CAGR, buoyed by EPR fee schedules that reward recycled content and by plentiful OCC priced at USD 44 per ton. Coated unbleached kraft serves grease-resistant, natural-aesthetic niches, while white line chipboard competes on cost for non-food secondary packs. Net recycled board capacity rose modestly in 2025 as Graphic Packaging's Waco mill ramp offset closures in Minnesota and Texas. Minnesota's EPR eco-modulation rules that favor weight reduction are pushing brands toward lighter caliper folding boxboard, reinforcing momentum away from virgin bleached substrates.

Converters that secure high-quality recycled furnish enjoy price resilience, because EPR fees linked to recycled content narrow the cost gap versus virgin grades. Packaging Corporation of America's acquisition of Greif's recycled mills raised its recycled mix from 20% to 30%, highlighting a strategic pivot toward fee-friendly substrates. These fiber-mix adjustments suggest that the United States folding cartons market will continue tilting toward recycled fiber, especially in regulated coastal states where fee structures directly impact total delivered cost.

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Graphic Packaging Holding Company

- International Paper Company

- Sonoco Products Company

- Georgia-Pacific LLC

- Pratt Industries Inc.

- Atlantic Packaging Corp.

- Mayr-Melnhof Karton AG

- AR Packaging Group AB

- Clearwater Paper Corporation

- Hood Container Corporation

- PaperWorks Industries Inc.

- Bell Incorporated

- L Industrial Packaging

- JohnsByrne Company

- Curtis Packaging Corporation

- All Packaging Company

- American Carton Company

- Diamond Packaging

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Threat of New Entrants

- 4.6.2 Bargaining Power of Suppliers

- 4.6.3 Bargaining Power of Buyers

- 4.6.4 Threat of Substitute Products

- 4.6.5 Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 E-commerce Boom Driving Demand for Lightweight Protective Packaging

- 4.7.2 Increasing Demand for Sustainable and Recyclable Packaging Solutions

- 4.7.3 Premiumization in Food and Beverage Boosting High-Quality Printing

- 4.7.4 Rapid Growth of Meal Kit and Ready-to-Eat Delivery Services

- 4.7.5 State-Level Extended Producer Responsibility Legislation Accelerating Carton Adoption

- 4.7.6 Rise of Pharmaceutical Cold-Chain Shipments Requiring Specialized Folding Cartons

- 4.8 Market Restraints

- 4.8.1 Volatility in Recovered Paper and Virgin Pulp Prices

- 4.8.2 Capacity Expansion of Flexible Packaging Displacing Folding Cartons

- 4.8.3 Supply Chain Disruptions from Trucker Shortages Increasing Lead Times

- 4.8.4 Labor Shortage in Skilled Press Operators Restricting Output Growth

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging Holding Company

- 6.4.3 International Paper Company

- 6.4.4 Sonoco Products Company

- 6.4.5 Georgia-Pacific LLC

- 6.4.6 Pratt Industries Inc.

- 6.4.7 Atlantic Packaging Corp.

- 6.4.8 Mayr-Melnhof Karton AG

- 6.4.9 AR Packaging Group AB

- 6.4.10 Clearwater Paper Corporation

- 6.4.11 Hood Container Corporation

- 6.4.12 PaperWorks Industries Inc.

- 6.4.13 Bell Incorporated

- 6.4.14 L Industrial Packaging

- 6.4.15 JohnsByrne Company

- 6.4.16 Curtis Packaging Corporation

- 6.4.17 All Packaging Company

- 6.4.18 American Carton Company

- 6.4.19 Diamond Packaging

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment