|

시장보고서

상품코드

2061732

아시아태평양의 접이식 카톤 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia-Pacific Folding Carton - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

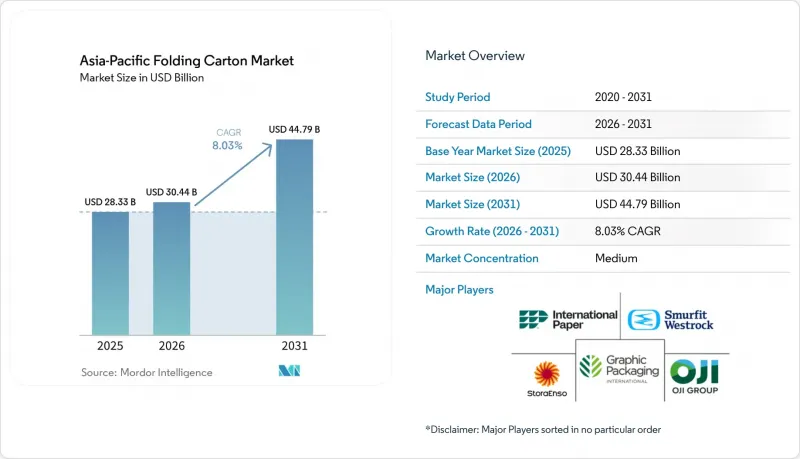

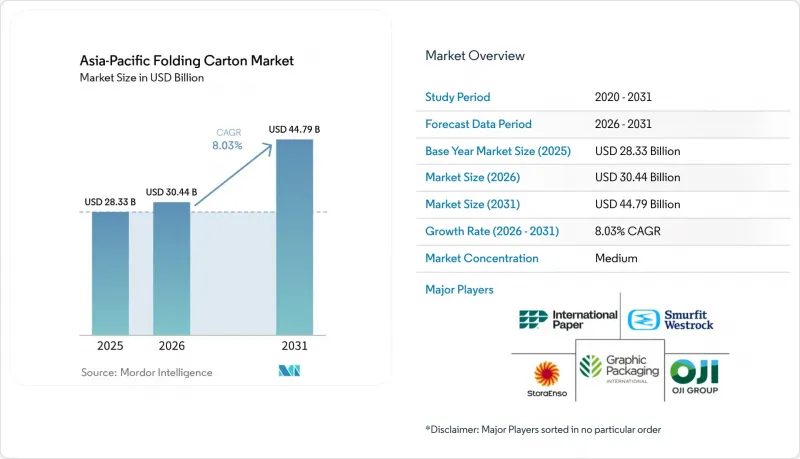

Mordor Intelligence에 의하면, 아시아태평양의 접이식 카톤 시장 규모는 2025년 283억 4,000만 달러로 평가되었습니다. 2026년 304억 3,000만 달러로 확대되고 2026년부터 2031년에 걸쳐 CAGR은 8.03%를 나타내, 2031년에는 447억 9,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 원료 유형(고형 표백 황산 펄프, 접이식 상자용 판지, 코팅 미표백 크라프트지, 화이트라인 칩보드 등), 인쇄 기술(평판 인쇄, 그라비아 인쇄, 디지털 인쇄 등), 최종 사용자 산업(퍼스널케어 및 화장품, 전기 및 전자 기기 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 접이식 카톤 시장 동향 및 분석

아시아 신흥국에서의 식품 및 음료 소비 확대

식품 및 음료 수요는 아시아태평양의 접이식 카톤 시장에서 여전히 가장 확실한 수요 기반을 형성하고 있습니다. 이는 현대의 소매, 수출 유통 채널, 편의점 형태에서 유제품, 냉장 식품, 스낵, 음료, 즉석식사에 대한 2차 포장이 필요하기 때문입니다. 가장 큰 변화는 소비량 증가뿐만 아니라, 국내 및 수출 판매 모두에서 더 높은 인쇄 품질, 더 강력한 진열 효과, 그리고 식품 접촉 적합성을 요구하는 포장 제품으로의 꾸준한 전환에 있습니다. 베트남과 인도네시아가 두드러지는 이유는 컨버터가 국내 수요와 수출용 생산 모두와 관련된 가공식품의 유통을 점점 더 잘 처리하고 있기 때문입니다. 이에 따라, 더 고성능의 판지 등급과 더 신뢰할 수 있는 가공 능력에 대한 수요가 높아지고 있습니다. 또한, 단품용, 냉장 제품 및 편의성을 중시한 형태도 용도가 확대되고 있으며, 특히 도시 지역의 구매 패턴에서 대용량 가정용 제품 구매보다 소용량 패키지와 빈번한 재구매를 선호하는 지역에서 이러한 경향이 두드러집니다.

지속 가능하고 재활용 가능한 포장재로 전환

브랜드 소유주들이 재활용 가능성, 섬유 함량, 그리고 제시한 환경 목표와의 부합 여부에 대해 포장재 선택지를 더욱 엄격하게 심사하게 됨에 따라, 지속가능성은 조달 결정을 통해 아시아태평양의 접이식 카톤 시장에 영향을 미치고 있습니다. 이러한 변화가 중요한 이유는 재활용이 어렵거나 브랜드의 지속가능성 관련 주장과 일관성이 떨어지는 플라스틱을 많이 사용한 형태에 비해, 접이식 카톤는 그러한 요건을 더 쉽게 충족시키는 경우가 많기 때문입니다. 그 결과, 특히 고급 식품, 개인 위생 용품, 수출 지향 소비재 분야에서 컨버터와 브랜드 소유자 간의 대화가 더욱 활발해지고 있습니다. 이러한 분야에서는 패키징 선정에 규정 준수 및 평판과 같은 측면이 더욱 크게 반영되고 있습니다. 그래픽 패키징사는 ‘비전 2030’ 프로그램을 통해 이러한 방향성을 강화하고 있습니다. 이 프로그램은 재생 가능 연료 사용률 90% 및 지속 가능한 방식으로 관리된 산림 제품의 구매율 100%를 목표로 하고 있으며, 이는 지속가능성 성과가 포장 관련 논의에서 공급업체의 입지를 결정하는 요소 중 하나로 자리 잡고 있음을 보여줍니다. 이러한 조달 기준이 지역 공급망 전반으로 확산됨에 따라, 아시아태평양의 접이식 카톤 시장은 재활용이 가능하고 인쇄성이 뛰어나며, 점점 더 프리미엄화되는 섬유 기반 포장 솔루션과의 밀접한 연관성 덕분에 혜택을 보고 있습니다.

판지 원료 가격의 변동

원자재 가격 변동은 아시아태평양의 접이식 카톤 시장에 있어 여전히 가장 뚜렷한 단기적 제약 요인으로 작용하고 있습니다. 왜냐하면 독립 계열 가공업체는 판지나 펄프의 원가가 대형 소비재 제조업체와의 계약 가격보다 급격하게 변동할 때마다 그 영향을 받기 때문입니다. 이 압력은 지역 전체에 고르게 분포되어 있는 것은 아닙니다. 수입에 의존하는 시장이나 후방 통합을 실시하지 않는 컨버터는 자사의 판지 공급 대부분을 관리하고 있는 제지 공장에 비해 비용 변동을 관리할 여지가 적기 때문입니다. 이는 투자 행위에 있어 중요한 의미를 지닙니다. 왜냐하면, 최종 수요가 견조한 시장이라 하더라도 이익률 전망이 어두워지면 생산 능력 확충이 지연될 가능성이 있기 때문입니다. 스마핏 웨스트록의 2026년 1분기 실적은 에너지 비용 상승과 수요 회복으로 인해 2026년 3월과 4월에 해당 지역에서 컨테이너보드 가격이 상승했음을 보여주고 있으며, 이는 가격 환경이 여전히 변동성을 보이고 있고, 포장 업계가 여전히 비용 변동에 민감한 환경에서 사업을 영위하고 있음을 뒷받침합니다. 그 결과, 경기 사이클 전반에 걸쳐 이익률을 유지할 수 있는 통합형 공급업체와, 표준 등급이나 계약에 따른 물량을 놓고 치열한 경쟁을 벌이는 중소규모의 가공업체 간의 격차가 더욱 확대될 가능성이 있습니다.

부문별 분석

2025년, 아시아태평양의 접이식 카톤 시장에서 접이식 보드는 53.78%의 점유율을 차지했습니다. 이는 강성, 표면 품질, 그리고 대량 생산 시 효율적인 가공이 요구되는 대중 소비재에 이 소재가 매우 적합하다는 점을 반영하고 있습니다. 해당 지역의 대규모 포장 프로그램에서 외관, 구조적 성능, 비용 간의 균형이 실용적이기 때문에 식품, 음료, 가정용품 및 일반 소비재의 다양한 용도에서 여전히 주요 기판으로 선택되고 있습니다. 그 밖의 등급들도 여전히 중요하며, 인열 강도가 중시되는 분야에서는 ‘코팅되지 않은 미표백 크라프트보드’가 그 역할을 수행하고, 진화하는 지속가능성 요건에 부합하는 재생 소재 비율이 높은 용도에서는 ‘화이트 라이닝 칩보드’가 여전히 중요한 위치를 차지하고 있습니다. 전반적으로, 특히 규모, 인쇄 품질, 그리고 확립된 가공 기술에 대한 숙련도에 좌우되는 아시아태평양의 접이식 골판지 시장에서 접이식 골판지가 계속해서 주류 수요를 지탱하는 소재 구성으로 자리 잡고 있습니다.

솔리드 블리치드 보드는 2026년부터 2031년까지 연평균 성장률(CAGR) 10.23%를 나타낼 것으로 예측되며, 이러한 성장세는 대량 생산형 식품 분야와 같은 주류 시장이 아닌 의약품, 고급 퍼스널케어, 뉴트라슈티컬, 영유아용 영양식품과 같은 용도에서 수요 증가를 반영하고 있습니다. 이 등급의 매력은 그 백색도나 인쇄 시의 외관뿐만 아니라, 더욱 균일한 질감, 더욱 깔끔한 섬유 구조, 그리고 안전성, 제품 이미지, 세세한 부분까지 신경 쓴 인쇄 성능 등 모든 요소가 중요한 섬세한 용도에 대한 높은 적합성에도 있습니다. 따라서 솔리드 블리치드 보드는 아시아태평양의 접이식 카톤 업계에서 특히 고부가가치 부문에서 중요한 역할을 하고 있습니다. 이 분야에서는 구매자들이 신뢰할 수 있는 골판지의 성능과 더욱 엄격한 규정 준수 여부에 대해 더 높은 대가를 지불할 의향이 있기 때문입니다. 따라서 이러한 성장 가속화는 광범위한 상품화의 확대라기보다는 규제와 브랜드 가치가 모두 높아지고 있는 용도 분야에서 시장이 프리미엄 원자재로 꾸준히 전환되고 있음을 보여줍니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the asia-Pacific folding carton market size is expected to grow from USD 28.34 billion in 2025 to USD 30.43 billion in 2026 and is forecast to reach USD 44.79 billion by 2031 at 8.03% CAGR over 2026-2031.

This report is Segmented by Material Type (Solid Bleached Sulfate, Folding Boxboard, Coated Unbleached Kraft, White Line Chipboard, and More), Printing Technology (Lithographic Printing, Gravure Printing, Digital Printing, and More), End-User Industry (Personal Care and Cosmetics, Electrical and Electronics, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Folding Carton Market Trends and Insights

Growing Food and Beverage Consumption in Emerging Asian Economies

Food and beverage demand remains the clearest volume base for the Asia-Pacific folding carton market because secondary packs for dairy, chilled foods, snacks, beverages, and ready meals are needed across modern retail, export channels, and convenience formats. The greatest change is not only higher consumption, but also a steady shift toward packaged products that require better print quality, stronger shelf impact, and food-contact suitability in both domestic and export sales. Vietnam and Indonesia stand out because converters are increasingly serving packaged food flows linked to both local demand and export manufacturing, which lifts the need for more capable board grades and more reliable finishing capacity. Single-serve, chilled, and convenience-oriented formats are also expanding the application base, especially where urban shopping patterns favor smaller packs and more frequent replenishment rather than larger household purchases.

Shift Toward Sustainable and Recyclable Packaging Materials

Sustainability is influencing the Asia-Pacific folding carton market through procurement decisions, because brand owners now screen packaging options more closely for recyclability, fiber content, and alignment with stated environmental targets. This shift matters because folding cartons often fit those requirements more easily than plastic-heavy formats that carry a more difficult recycling profile or a weaker fit with brand sustainability claims. The result is a broader conversation between converters and brand owners, especially in premium food, personal care, and export-oriented consumer goods, where packaging selection now carries a stronger compliance and reputation dimension. Graphic Packaging has reinforced this direction through its Vision 2030 program, which targets 90% renewable fuel use and 100% sustainably managed purchased forest products, showing how sustainability performance is becoming part of supplier positioning in packaging discussions. As these procurement filters spread across regional supply chains, the Asia-Pacific folding carton market benefits from its close association with recyclable, high-print, and increasingly premium fiber-based packaging solutions.

Volatility In Paperboard Raw Material Prices

Raw material volatility remains the clearest near-term constraint on the Asia-Pacific folding carton market because independent converters are exposed whenever paperboard and pulp costs move faster than contract pricing with large consumer goods customers. The pressure is not evenly distributed across the region, since import-dependent markets and converters without backward integration have less room to manage cost swings than mills that control a greater share of their own board supply. This matters for investment behavior because capacity upgrades can be delayed when margin visibility weakens, even in markets where end demand remains healthy. Smurfit WestRock's first-quarter 2026 results pointed to higher containerboard prices in the region during March and April 2026 due to energy costs and improving demand, confirming that pricing conditions are still moving and that packaging players are operating in a cost environment that remains sensitive. The likely consequence is more differentiation between integrated suppliers that can hold margins through the cycle and smaller converters that compete heavily on standard grades and contract-driven volumes.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of E-Commerce and Omni-Channel Retail

- Increasing Pharmaceutical Production and Healthcare Spending

- Competition from Flexible Packaging Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held a 53.78% share of the Asia-Pacific folding carton market in 2025, reflecting the material's strong fit with mass-market consumer goods that need stiffness, surface quality, and efficient conversion across large production runs. It remains the preferred volume substrate in many food, beverage, household, and general consumer applications because it offers a practical balance between appearance, structural performance, and cost across the region's largest packaging programs. Other grades still matter, with Coated Unbleached Kraftboard retaining a role where tear strength is important and White-lined Chipboard staying relevant in more recycled-content-oriented applications that align with evolving sustainability requirements. The broad result is a material mix in which Folding Boxboard continues to anchor mainstream demand, especially in the parts of the Asia-Pacific folding carton market that depend on scale, print quality, and established converting familiarity.

Solid Bleached Board is forecast to grow at a 10.23% CAGR from 2026 to 2031, and that pace reflects rising demand in pharmaceutical, premium personal care, nutraceutical, and infant nutrition applications rather than in the high-volume food mainstream. The appeal of this grade is not only its brightness or print appearance, but also its tighter consistency, cleaner fiber profile, and stronger fit for sensitive end uses where safety, product image, and detailed print performance all matter. This makes Solid Bleached Board especially important in the higher-value layers of the Asia-Pacific folding carton industry, where buyers are willing to pay more for dependable carton performance and stronger compliance alignment. Its faster growth therefore says less about broad commoditized expansion and more about the market's steady movement toward premium substrates in applications where regulation and brand value are both rising.

List of Companies Covered in this Report:

- Graphic Packaging International, LLC

- International Paper Company

- Smurfit WestRock plc

- Stora Enso Oyj

- Oji Holdings Corporation

- Rengo Co., Ltd.

- Nippon Paper Industries Co., Ltd.

- Toppan Holdings Inc.

- Amcor plc

- Huhtamaki Oyj

- Cheng Loong Corporation

- Jiangsu Zhongnan Packaging Co., Ltd.

- Greatview Aseptic Packaging Co., Ltd.

- TCPL Packaging Limited

- Lee and Man Paper Manufacturing Limited

- Siegwerk Druckfarben AG & Co. KGaA

- Parksons Packaging Limited

- SIG Group AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising E-commerce Demand for Sustainable Secondary Packaging

- 4.2.2 Growing Preference for Recyclable Substitutes to Rigid Plastics

- 4.2.3 Expansion of Quick-Service Restaurants Requiring Custom Printed Cartons

- 4.2.4 Government Bans on Single-Use Plastics Accelerating Carton Adoption

- 4.2.5 Advancements in Water-Based Barrier Coatings Enhancing Food Safety

- 4.2.6 Converting Plant Automation Driving High-Volume, Cost-Effective Output

- 4.3 Market Restraints

- 4.3.1 Volatility in Wood Pulp Prices Compressing Converters' Margins

- 4.3.2 Stringent VOC Regulations Raising Printing Technology Costs

- 4.3.3 Competition From Flexible Packaging in Ready-Meal Formats

- 4.3.4 Limited Recycling Infrastructure in Emerging ASEAN Nations

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Material Type

- 5.1.1 Solid Bleached Sulfate

- 5.1.2 Folding Boxboard

- 5.1.3 Coated Unbleached Kraft

- 5.1.4 White Line Chipboard

- 5.1.5 Other Material Types

- 5.2 By Printing Technology

- 5.2.1 Lithographic Printing

- 5.2.2 Flexographic Printing

- 5.2.3 Digital Printing

- 5.2.4 Gravure Printing

- 5.2.5 Other Printing Technologies

- 5.3 By End-User Industry

- 5.3.1 Food and Beverage

- 5.3.2 Healthcare/Pharmaceuticals

- 5.3.3 Personal Care and Cosmetics

- 5.3.4 Electrical and Electronics

- 5.3.5 Household and Industrial Goods

- 5.3.6 Tobacco

- 5.3.7 E-commerce and Retail-ready Packaging

- 5.3.8 Other End-User Industries

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 India

- 5.4.3 Japan

- 5.4.4 South Korea

- 5.4.5 Australia and New Zealand

- 5.4.6 Rest of Asia-Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Graphic Packaging International, LLC

- 6.4.2 International Paper Company

- 6.4.3 Smurfit WestRock plc

- 6.4.4 Stora Enso Oyj

- 6.4.5 Oji Holdings Corporation

- 6.4.6 Rengo Co., Ltd.

- 6.4.7 Nippon Paper Industries Co., Ltd.

- 6.4.8 Toppan Holdings Inc.

- 6.4.9 Amcor plc

- 6.4.10 Huhtamaki Oyj

- 6.4.11 Cheng Loong Corporation

- 6.4.12 Jiangsu Zhongnan Packaging Co., Ltd.

- 6.4.13 Greatview Aseptic Packaging Co., Ltd.

- 6.4.14 TCPL Packaging Limited

- 6.4.15 Lee and Man Paper Manufacturing Limited

- 6.4.16 Siegwerk Druckfarben AG & Co. KGaA

- 6.4.17 Parksons Packaging Limited

- 6.4.18 SIG Group AG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment