|

시장보고서

상품코드

2062065

머시닝 센터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Machining Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

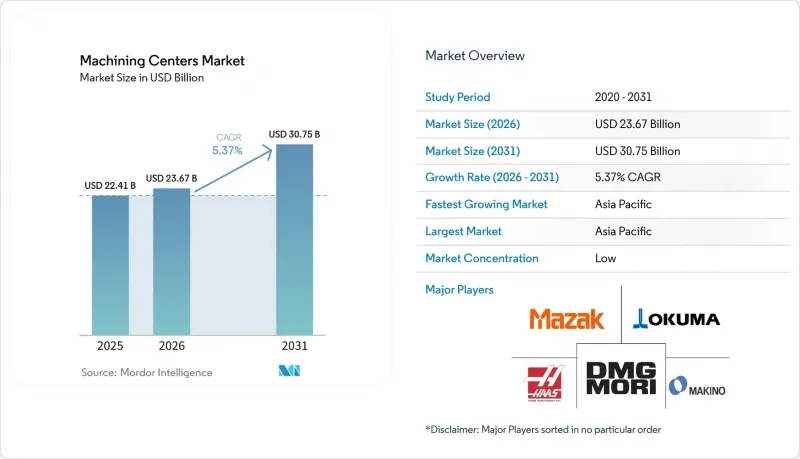

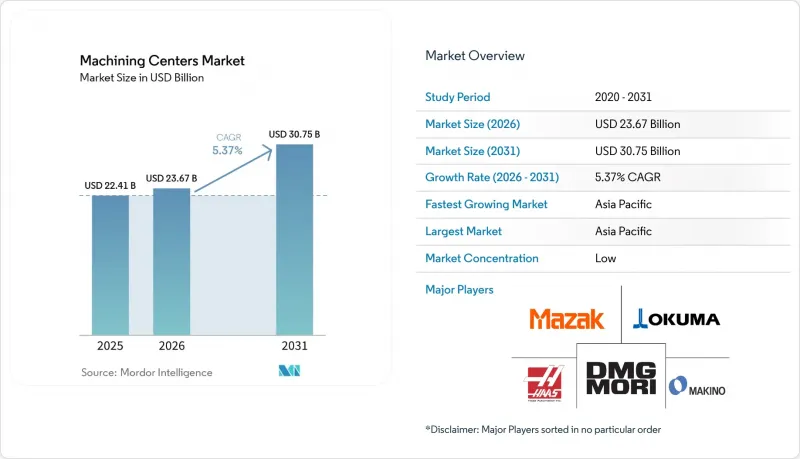

Mordor Intelligence에 의하면, 머시닝 센터 시장 규모는 2025년 224억 1,000만 달러, 2026년 236억 7,000만 달러에서 2031년까지 307억 5,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 5.37%를 나타낼 것으로 예측됩니다.

본 보고서는 기계 유형별(수평형 머시닝 센터 등), 축 구성별(3축 등), 스핀들 방향별(수평, 수직 등), 구조 유형별(컬럼형, 갠트리형 등), 최종 사용자 산업별(자동차, 에너지 등), 지역별(북미, 유럽 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 머시닝 센터 시장 동향과 인사이트

항공우주 부품 제조 능력 확대

항공우주 프로그램에서는 수평형 및 5축 가공 플랫폼에 대한 수요를 촉진하기 위해 수년까지 생산 능력 확충 투자가 진행되고 있습니다. 프랫 앤드 휘트니는 2028년까지 압축기 및 터빈 디스크 생산량을 30% 늘리기 위해 조지아주 콜럼버스에 위치한 사업장에 2억 달러를 투자했습니다. 이는 기어드 터보팬(GTF) 및 F135 엔진의 생산 속도와 직결되어, 티타늄 및 니켈 가공이 가능한 5축 및 대형 수평 가공 라인 수요를 촉진하고 있습니다. 카만 스페이스 앤 디펜스(Kaman Space and Defense)는 2026년 4분기 가동을 목표로 솔트레이크시티에 신설하는 자동 가공 허브를 통해 발사 시스템 생산량을 4배로, 고체 로켓 모터 노즐 생산량을 2배로 확대할 예정입니다. 이를 위해서는 자동 검사와 통합된 고처리량 금속 가공이 필요합니다. 하네웰사의 캔자스주 올레이사 지역 확장 사업은 항공 전자 장비 및 인쇄 회로 기판 조립용 국내 전자기기 제조거점을 강화하고, 비행 시스템 밸류체인 전반에 걸친 현지 정밀 제조를 뒷받침할 것입니다. 이러한 생산 능력 확대를 위해서는 다축 가공 셀, 팔레트 자동화, 그리고 높은 이송 속도와 회전 속도에서도 공차를 안정적으로 유지하기 위한 일관된 열 관리가 필요하며, 이는 북미 및 유럽의 항공우주 클러스터 전반에 걸친 최우선 과제입니다. 이러한 투자는 시운전, 공정 검증 및 양산 체제 구축과 연계된 2-4년의 영향 기간을 설정하고 있으며, 이는 머시닝 센터 시장의 단기적인 수요를 뒷받침하게 될 것입니다.

의료기기 제조의 정밀도 요건

2026년 품질 관리 시스템 규정은 의료기기 제조업체에 대한 추적성 및 공정 관리 기준을 강화함으로써, 서브미크론 가공 및 공정 내 측정의 필요성을 높이고 있습니다. 이 규정은 ISO 원칙에 부합하며, 21 CFR의 다수 조항을 개정함으로써 안정적인 가공 공정에 기반을 둔 품질 시스템과 문서화를 강화합니다. 생산 능력 확충이 이러한 추세를 뒷받침하고 있으며, 의료용 정밀 부품 및 조립품 생산에 대응하기 위해 새로운 클린룸과 규제 기준을 충족하는 생산 환경이 도입되고 있습니다. 스크랩을 줄이고, 일관성 있으며 검증 가능한 가공 결과를 통해 감사 통과를 실현하기 위해, 온도 보정, 프로빙 사이클, 디지털 트윈을 활용한 검증에 대한 투자가 확대되고 있습니다. 이러한 요인은 FDA의 관할 하에 있는 미국에서 가장 두드러지게 나타나며, CE 마킹이 적용되는 유럽에도 영향을 미치고 있어, 다국적 OEM 기업에 서비스를 제공하는 인도 및 아세안(ASEAN)의 위탁 생산 거점에서도 그 영향이 확대되고 있습니다. 2-4년까지 영향의 시간적 흐름은 인증 주기와 설비 리드타임과 일치하며, 이로 인해 의료 분야의 파이프라인이 머시닝 센터 시장을 지속적으로 뒷받침하게 될 것입니다.

숙련된 CNC 조작자 및 프로그래머의 부족

기계 기술자 및 CNC 프로그래머에 대한 구인 수요가 계속 증가하고 있어 생산량에 큰 부담이 되고 있으며, 이로 인해 공장에서 복잡한 작업을 얼마나 빨리 가동할 수 있는지가 제한받고 있습니다. 업계 관계자들의 추산에 따르면, 미국에서는 2030년까지 은퇴 인구가 수요를 따라잡을 것으로 예상되는 반면, 단기 교육 과정만으로는 다축 프로그래밍, 세팅, 검사에 필요한 기술을 충분히 습득할 수 없어 심각한 인력 부족이 발생할 것으로 전망됩니다. 고도의 CAM 업무에서 숙련된 수준에 도달하기까지 걸리는 기간은 수년 단위로 측정되지만, 이는 분기별 납기 주기와 맞지 않아 무인화 프로그램에서 반복적으로 병목 현상을 일으키고 있습니다. 대기업들은 대개 대학과 제휴를 맺고 더 높은 임금을 제시하고 있습니다. 이로 인해 소규모 위탁 가공 업체에서 인력이 유출되면서 채용 경쟁이 치열해지고 있습니다. 그 결과, 고가의 다축 장비 가동률이 떨어지고, 팀이 교대 근무를 넘나들며 프로그래밍이나 설정을 처리할 수 없는 경우, 공정 통합 도입이 지연될 수 있습니다. 이러한 제약은 북미와 유럽에서 가장 심각하며, 자동화 프로젝트로 인해 기초 기술 요건이 높아짐에 따라 아시아태평양으로까지 확산되고 있어, 이는 머시닝 센터 시장에 당분간 걸림돌이 되고 있습니다.

부문별 분석

2025년 기준으로 수직형 머시닝 센터는 머시닝 센터 시장 점유율의 47.68%를 차지했으나, 범용형 및 5축 가공기는 2031년까지 연평균 성장률(CAGR) 6.12%로 성장할 것으로 전망됩니다. 수직형 구조는 공구 접근성, 칩 배출 및 인체공학적 설계 덕분에 신속한 설비 전환이 가능하기 때문에 자동차 업계나 소규모 가공 공장의 대량 생산 업무에서 주류를 이루고 있습니다. 또한, 최근 도입된 수직형 5축 가공기는 더 높은 주축 회전수, 뛰어난 강성, 그리고 더욱 종합적인 기술 사이클을 구현하여, 단일 플랫폼에서 가공 가능한 부품의 범위를 넓히고 있습니다. 수평형 머시닝 센터는 여전히 2위 카테고리를 차지하고 있으며, 팔레트 방식의 자동화 및 중절삭에 적합하기 때문에 파워트레인, 항공우주용 구조 부품 및 대형 직육면체 부품 가공에 주로 사용됩니다. 선삭과 밀링 가공을 통합한 멀티태스크 가공기는 세팅 횟수를 줄이고 기하학적 정밀도를 향상시키며, 공정 경로를 단일 기계 워크플로로 통합함으로써 공장이 인력 부족 문제를 해결하는 데 도움을 줍니다.

다품종 소량 생산 프로그램에서는 프로브 기능과 공구 모니터링 기능을 갖춘 5축 수직 머시닝 센터가 부품 계열의 신속한 전환과 오염 관리를 가능하게 하는 반면, 유연한 생산 시스템과 연동된 수평 머시닝 센터는 예측 가능한 처리량을 확보합니다. 윤곽의 복잡화, 벽 두께의 얇아짐, 일체 성형 부품 증가와 같은 OEM의 설계 변경은 머시닝 센터 시장에서 범용 및 5축 머신의 대형화를 촉진하는 요인이 되고 있습니다. 디지털 트윈을 통한 검증과 기내 측정이 초기 제품 승인 주기를 단축하고, 새로운 절삭유 관리 시스템이 공구 수명과 표면 마감을 개선함에 따라 추가적인 이익이 기대됩니다. 이러한 상황은 더욱 충실한 자동화 포트폴리오, 다양한 소재에 맞춘 스핀들 옵션, 그리고 머시닝 센터 시장의 모든 장비에 적용 가능한 소프트웨어 제품군을 갖춘 공급업체에게 유리하게 작용합니다.

지역별 분석

아시아태평양은 2025년에 전 세계 소비량의 54.69%를 차지해, 강력한 산업 확장과 제조업 고도화에 힘입어 2031년까지 연평균 성장률(CAGR) 7.12%로 성장할 것으로 전망됩니다. 중국은 수입과 수출을 모두 지속적으로 확대해 왔으며, 2025년 상반기에는 세계 공작기계 수출 점유율의 19%를 차지하며 독일을 제쳤습니다. 이는 고정밀 시스템에 대한 수요 증가와 더불어 국내 생산 능력이 향상되고 있음을 반영한 것입니다. 수입은 여전히 일본, 독일, 대만이 주도하고 있으며, 첨단 수평형 공작기계와 5축 가공기에 대한 의존도가 계속되고 있음이 드러나고 있습니다. 동시에, 중국에서는 신규 공장이 중·고급 제품의 생산 능력을 확대하며 해당 지역의 제조거점을 강화하고 있습니다.

인도는 생산 연계형 인센티브(PLI) 제도나 자본재 프로그램과 같은 정책 지원을 통해 입지를 강화하고 있으며, 이러한 조치들은 정밀 제조 분야의 잠재 시장을 확대되고 있습니다. ‘PLI Auto’ 제도와 승인된 자본재 프로젝트는 역량 강화, 우수 센터, 시험 인프라를 지원하고 있습니다. 이러한 정책적 지원과 기술 개발에 대한 집중이 맞물려, 인도는 고부가가치 부품 및 조립품 시장으로의 진출을 가능하게 하고 있습니다. 중국과 더불어 이러한 동향으로 인해 아시아태평양은 머시닝 센터 시장의 주요 성장 동력으로서의 입지를 확고히 하고 있습니다.

북미는 2025년에 항공우주, 방위, 자동차 산업의 국내 복귀에 힘입어 강력한 성장세를 보였습니다. 미국의 제조 기술 수주가 사상 최고치를 기록한 것은 생산 능력의 한계에 부딪혔음을 나타내며, 단기적인 수요 증가를 시사합니다. 독일과 이탈리아가 주도하는 유럽은 첨단 산업 기반과 지속가능성을 중심으로 한 설비 투자 사이클의 혜택을 지속적으로 누리고 있으며, 업계 재편을 통해 OEM의 역량도 강화되고 있습니다. 중동 및 아프리카는 다각화와 에너지 투자를 통해 점차 성장하고 있지만, 공작기계 수입에 대한 의존도는 여전히 높은 상태입니다. 전반적으로 아시아태평양이 성장의 기반이 되고 있으며, 북미와 유럽은 고부가가치 분야 및 규제 산업에서 안정적인 수요를 제공합니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the machining centers market size is projected to expand from USD 22.41 billion in 2025 and USD 23.67 billion in 2026 to USD 30.75 billion by 2031, registering a CAGR of 5.37% between 2026 to 2031.

This report is Segmented by Machine Type (Horizontal Machining Centers, and More), by Axis Configuration (3-Axis, and More), by Spindle Orientation (Horizontal, Vertical, and More), by Structure Type (Column-Type, Gantry-Type, and More), by End-User Industry (Automotive, Energy, and More), and by Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Machining Centers Market Trends and Insights

Aerospace Component Manufacturing Capacity Expansion

Aerospace programs are moving ahead with multi-year capacity investments that lift demand for horizontal and 5-axis machining platforms. Pratt & Whitney committed USD 200 million to its Columbus, Georgia operations to increase compressor and turbine disk output by 30% by 2028, which ties directly to Geared Turbofan and F135 engine build rates and favors 5-axis and heavy-duty horizontal lines with titanium and nickel capability. Karman Space & Defense is quadrupling launch system production and doubling solid rocket motor nozzle output through a new automated machining hub in Salt Lake City that targets Q4 2026 readiness, which will require high-throughput metallic machining integrated with automated inspection. Honeywell's expansion in Olathe, Kansas, is building domestic electronics manufacturing depth for avionics and printed circuit board assemblies, reinforcing localized precision manufacturing across the flight systems value chain. Ramping such capacity requires multi-axis cells, pallet automation, and consistent thermal management to stabilize tolerance at higher feeds and speeds, which is a priority across North American and European aerospace clusters. These investments set up a 2 to 4 year impact window that aligns with commissioning, process validation, and rate readiness, which in turn underpins near term demand in the machining centers market.

Medical Device Manufacturing Precision Requirements

The 2026 Quality Management System Regulation raises the bar on traceability and process control for medical device manufacturers, which elevates the need for sub-micron machining and in-process gauging. The regulation aligns with ISO principles and updates scores of sections across 21 CFR, which solidifies quality systems and documentation that depend on stable machining processes. Capacity additions support the trend, with new cleanrooms and compliant production environments being installed to serve precision parts and assemblies for medical use cases. Investments in thermal compensation, probing cycles, and digital twin validation are spreading to reduce scrap and to pass audits with consistent, verifiable machining outcomes. This driver is strongest in the United States under FDA jurisdiction and extends to Europe under CE marking, with a growing effect in India and ASEAN contract manufacturing hubs that serve multinational OEMs. The 2 4-year impact timeline matches certification cycles and equipment lead times, which keeps the medical pipeline supportive for the machining centers market.

Skilled CNC Operator and Programmer Shortage

Open positions for machinists and CNC programmers continue to weigh on throughput, which limits how fast plants can ramp complex work. Industry sources estimate a significant gap through 2030 in the United States as retirements keep pace with demand, while short training cycles cannot fully cover the skills needed for multi-axis programming, setup, and inspection. Time to proficiency is measured in years for advanced CAM roles, which does not align with quarterly delivery cycles and creates recurring bottlenecks in light-out programs. Larger manufacturers often partner with technical colleges and offer higher wages, which can draw talent away from small job shops and intensify hiring friction. The net effect is idle time on expensive multi-axis assets and slower adoption of process consolidation when teams cannot support programming and setup across shifts. This restraint is most acute in North America and Europe and is spreading in APAC as automation projects raise the baseline skill requirements, which keeps this a near-term drag for the machining centers market.

Other drivers and restraints analyzed in the detailed report include:

- Electric Vehicle Powertrain Component Production

- Mold and Die Industry Growth in Emerging Markets

- Economic Uncertainty Delaying Capital Equipment Purchases

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vertical machining centers held 47.68% of the machining centers market share in 2025, while universal and 5-axis machines are projected to expand at a 6.12% CAGR through 2031. Vertical configurations dominate high-volume work for automotive and job shop environments because tooling access, chip evacuation, and ergonomics support fast changeovers. Recent vertical 5-axis introductions also push higher spindle speeds, better rigidity, and more comprehensive technology cycles, which widens the set of parts that can be consolidated on a single platform. Horizontal machining centers remain the second largest category and are preferred for palletized automation and heavy cutting, which favors their use in powertrain, aerospace structural parts, and larger prismatic components. Multi-tasking centers that integrate turning and milling reduce setups, improve geometric integrity, and help plants cope with labor constraints by compressing process routes into single machine workflows.

In higher mix and lower volume programs, 5-axis verticals with probing and tool monitoring enable quick part family changeovers and contamination control, while horizontals tied to flexible manufacturing systems secure predictable throughput. OEM design changes that increase contour complexity, thin walls, and integrated features are a catalyst for universal and 5-axis upsizing within the machining centers market. Further gains are likely as digital twin validation and on-machine measurement accelerate first article approval cycles, and as new coolant management systems enhance tool life and surface finish. This mix favors suppliers with deeper automation portfolios, spindle options matched to material families, and software suites that can be deployed across fleets in the machining centers market.

Geography Analysis

Asia Pacific accounted for 54.69% of global consumption in 2025 and is projected to grow at a 7.12% CAGR through 2031, driven by strong industrial expansion and manufacturing depth. China continues to scale both imports and exports, surpassing Germany with a 19% share of global machine tool exports in H1 2025, reflecting rising domestic capabilities alongside demand for high-precision systems. Imports remain led by Japan, Germany, and Taiwan, highlighting continued reliance on advanced horizontals and 5-axis machines. At the same time, new plants in China are expanding mid- to high-end production capacity, reinforcing the region's manufacturing base.

India is strengthening its position through policy support such as Production Linked Incentive schemes and capital goods programs, which are expanding the addressable market for precision manufacturing. The PLI Auto scheme and sanctioned capital goods projects are supporting capability building, centers of excellence, and testing infrastructure. This policy push, combined with a focus on skill development, is enabling India to move into higher-value components and assemblies. Together with China, these trends position Asia Pacific as the primary growth engine for the machining centers market.

North America gained strong momentum in 2025, supported by aerospace, defense, and automotive reshoring, with record U.S. manufacturing technology orders signaling tight capacity and near-term demand. Europe, led by Germany and Italy, continues to benefit from a sophisticated industrial base and sustainability-driven capex cycles, while consolidation enhances OEM capabilities. The Middle East and Africa are gradually expanding through diversification and energy investments, though reliance on imported machine tools remains high. Overall, Asia Pacific anchors growth, while North America and Europe provide stable demand across high-value and regulated sectors.

- DMG MORI

- Yamazaki Mazak

- Okuma Corporation

- Haas Automation

- Makino Milling Machine

- Doosan Machine Tools

- GF Machining Solutions

- Hyundai WIA

- Hurco Companies

- Fives Group

- Hardinge Inc.

- Chiron Group

- Brother Industries

- Jingdiao Group

- JTEKT (Toyoda)

- Spinner Maschinenbau

- Kitamura Machinery

- Emco Group

- Sodick Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Aerospace Component Manufacturing Capacity Expansion

- 4.2.2 Medical Device Manufacturing Precision Requirements

- 4.2.3 Electric Vehicle Powertrain Component Production

- 4.2.4 Mold and Die Industry Growth in Emerging Markets

- 4.2.5 Replacement Demand for Aging Machine Tool Fleets

- 4.2.6 Contract Manufacturing Outsourcing by OEMs

- 4.3 Market Restraints

- 4.3.1 High Capital Investment Barriers for Small Job Shops

- 4.3.2 Skilled CNC Operator and Programmer Shortage

- 4.3.3 Long Lead Times from Japanese and German Manufacturers

- 4.3.4 Economic Uncertainty Delaying Capital Equipment Purchases

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

- 4.8 Shift Toward Machine-as-a-Service Financing Models

- 4.9 Growing Preference for Horizontal Machining Centers in Automotive

5 Market Size & Growth Forecasts (Value, In USD Billion)

- 5.1 By Machine Type

- 5.1.1 Horizontal Machining Centres (HMC)

- 5.1.2 Vertical Machining Centres (VMC)

- 5.1.3 Universal / 5-Axis Machining Centres

- 5.1.4 Multi-Tasking Machining Centers (MTM)

- 5.1.5 Others (Gantry / Bridge-Type Centres, Turn-Mill Centers)

- 5.2 By Axis Configuration

- 5.2.1 3-Axis

- 5.2.2 4-Axis

- 5.2.3 5-Axis & Above

- 5.3 By Spindle Orientation

- 5.3.1 Horizontal

- 5.3.2 Vertical

- 5.3.3 Multi-spindle

- 5.4 By Structure Type

- 5.4.1 Column-Type

- 5.4.2 Gantry-Type

- 5.4.3 Moving-Table

- 5.5 By End-User Industry

- 5.5.1 Automotive

- 5.5.2 Aerospace & Defense

- 5.5.3 Energy (Oil-Gas, Renewables)

- 5.5.4 Medical Devices

- 5.5.5 Mold and Die Manufacturing

- 5.5.6 Others (General Manfacturing, Job Shops, Electronics, etc.)

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Peru

- 5.6.2.4 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.6.3.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 India

- 5.6.4.3 Japan

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 ASEAN (Indonesia, Thailand, Philippines, Malaysia, Vietnam)

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East and Africa

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Qatar

- 5.6.5.4 Kuwait

- 5.6.5.5 Turkey

- 5.6.5.6 Egypt

- 5.6.5.7 South Africa

- 5.6.5.8 Nigeria

- 5.6.5.9 Rest of Middle East and Africa

- 5.6.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DMG MORI

- 6.4.2 Yamazaki Mazak

- 6.4.3 Okuma Corporation

- 6.4.4 Haas Automation

- 6.4.5 Makino Milling Machine

- 6.4.6 Doosan Machine Tools

- 6.4.7 GF Machining Solutions

- 6.4.8 Hyundai WIA

- 6.4.9 Hurco Companies

- 6.4.10 Fives Group

- 6.4.11 Hardinge Inc.

- 6.4.12 Chiron Group

- 6.4.13 Brother Industries

- 6.4.14 Jingdiao Group

- 6.4.15 JTEKT (Toyoda)

- 6.4.16 Spinner Maschinenbau

- 6.4.17 Kitamura Machinery

- 6.4.18 Emco Group

- 6.4.19 Sodick Co.

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-Need Assessment