|

시장보고서

상품코드

2063643

독일의 머시닝 센터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Germany Machining Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

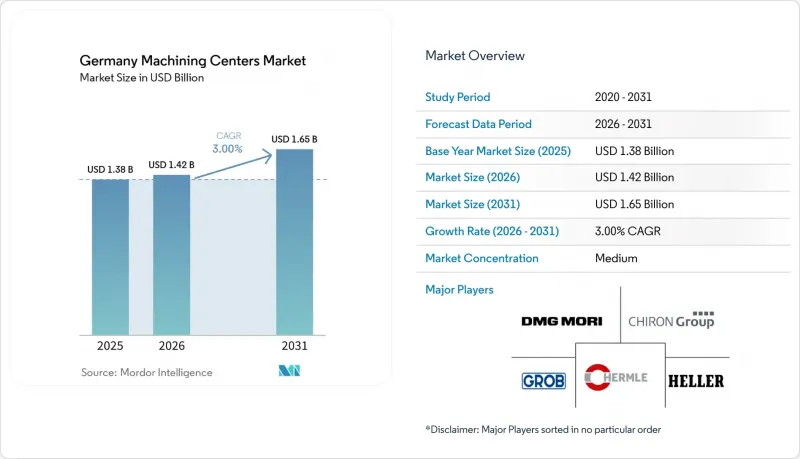

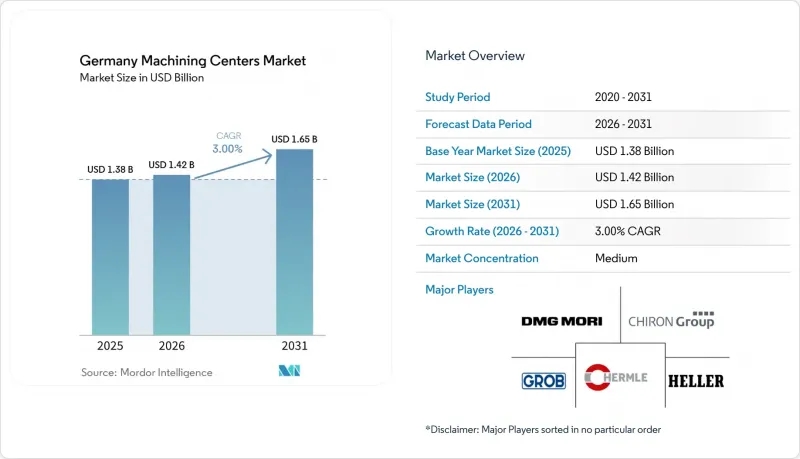

Mordor Intelligence에 의하면, 독일 머시닝 센터 시장 규모는 2025년 13억 8,000만 달러, 2026년 14억 2,000만 달러에서 2031년까지 16억 5,000만 달러로 확대되어 2026년부터 2031년까지 CAGR 3%를 나타낼 것으로 예측됩니다.

본 보고서는 기계 유형(수평형 머시닝 센터, 수직형 머시닝 센터 등), 축 구성(3축, 4축, 5축 이상), 스핀들 배치(수평, 수직, 다축), 구조 유형(컬럼형, 갠트리형, 이동 테이블형), 그리고 최종 사용자 산업(자동차 및 기타)에 따라 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일 머시닝 센터 시장 동향과 인사이트

인더스트리 4.0에 대한 수요가 커지면서, 커넥티드 CNC 머시닝 센터의 도입이 가속화되고 있습니다.

독일의 제조 시설에서는 현재, 제조 X의 핵심 요건인 생산 데이터의 On-Premise 보관을 실현하기 위해 OPC UA(Open Platform Communications Unified Architecture) 및 엣지 모듈을 표준 사양으로 채택하고 있습니다. IEC 62443-4-2 인증을 획득한 보쉬 렉스로스의 ctrlX 자동화 플랫폼은 모션 제어와 인간-기계 인터페이스를 분리하여 랜섬웨어 위험을 85% 줄여줍니다. 지멘스는 2025년에 SINUMERIK 828D 시리즈를 ‘Run MyVirtual Machine’ 기능으로 개편하여, 오프라인 간섭 검사를 통해 설정 시간을 20% 단축했습니다. 연방 정부의 막대한 디지털화 지원금이 설비 현대화를 가속화하고 있어, 중소규모의 수주 생산 공장이 고립된 구형 밀링 머신을 완벽하게 연결된 인더스트리 4.0 대응 대체 장비로 교체할 수 있게 되었습니다. 그 결과, 네이티브 OPC UA 포트나 디지털 트윈 라이선스를 갖추지 않은 기계의 수주량이 감소하는 경향을 보이고 있습니다.

자동차의 전동화가 고정밀 다축 가공의 필요성을 촉진하고 있습니다.

배터리 하우징, 모터 스테이터, 인버터 케이싱의 경우, 냉각 및 전자기 차폐 성능을 최적화하기 위해 50미크론 미만의 공차뿐만 아니라 Ra 1.6 이하의 표면 마감 처리가 요구됩니다. ZF사는 Nagel사의 정밀 연삭기를 도입한 후, 알루미늄 재질의 전동 모터 하우징에서 Ra 0.2 마이크론을 달성했습니다. DMG MORI사의 신형 DMU 65 H monoBLOCK은 열적으로 안정된 주조 본체와 18,000 rpm의 스핀들을 결합하여 배터리 트레이의 사이클 타임을 18% 단축합니다. 독일자동차산업협회는 2028년까지 국내 전기차 생산 대수가 210만 대에 달할 것으로 전망하고 있으며, 이에 따라 약 4,500대의 가공 센터에 대한 추가 수요가 예상됩니다. 다기능 선반·밀링 머신 플랫폼은 한 번의 세팅으로 밀링 가공, 선반 가공, 기어 호브 가공을 결합하여 경쟁력을 높였으며, 1차 공급업체의 재공품 재고를 30% 줄였습니다.

막대한 설비 투자와 금리 인상이 새로운 머시닝 센터에 대한 투자를 억제하고 있습니다.

유럽중앙은행은 2026년 3월 예금 금리를 2.75%로 동결함에 따라, 7년 만기 설비 대출 금리는 여전히 2019년 수준보다 1.5포인트 높은 수준을 유지하고 있습니다. 제조업의 설비 가동률이 현저히 하락한 것은 주로 여전히 높은 수준을 유지하고 있는 차입 비용의 완화를 기다리는 기업들에 의해 주도되는 신중한 설비 투자 환경을 여실히 보여주고 있습니다. 일반적으로 160만 달러로 제시되는 5축 수평형 기계의 투자 회수 기간은 현재 4년으로, 기존 평균인 6년보다 훨씬 짧습니다. 그 결과, 2026년 출하 대수의 42%가 리스 계약에 의한 것으로, 3년 전의 31%에서 증가했습니다. 한편, 중고 기계 판매는 2025년에 19% 급증했습니다. 이러한 높은 자금 조달 비용으로 인해 독일 머시닝 센터 시장의 예상 성장률은 0.5포인트 하락했습니다.

부문별 분석

수직형 머시닝 센터는 구입 가격이 저렴하고, 자동차용 주조품의 재가공 및 금형·다이 가공에 널리 사용되고 있기 때문에 2025년 독일 머시닝 센터 시장에서 45.4%의 점유율을 차지했습니다. 설치가 신속하고, 작업자들도 익숙하기 때문에 공장에서는 이를 선호하여 도입하고 있으며, 도입 대수는 3축 수직 밀링 머신에 크게 쏠려 있습니다. 그러나 항공우주 분야의 주계약업체와 의료기기 하청업체들은 2차 설비 구축을 생략하고, 터빈 블레이드 및 척추 임플란트의 사이클 타임을 최대 22% 단축할 수 있는 범용 및 5축 플랫폼으로 예산을 전환하고 있습니다.

유니버설/5축 머시닝 센터 시장은 2031년까지 연평균 성장률(CAGR) 4.8%를 나타낼 것으로 예측되며, 이는 모든 기계 유형 중 가장 높은 성장률입니다. 이러한 성장의 배경에는 미래 전투 항공 시스템(FCAS)의 동체 패널이나 전기자동차(EV)의 모터 하우징과 같이 높은 정밀도가 요구되는 프로젝트들이 있으며, 이들 모두는 동시 다면 가공이 필요합니다. 갠트리형이나 브리지형 기계는 기존에는 틈새 시장에 국한되어 있었으나, 재생에너지 분야에서 중절삭 수요가 증가함에 따라 현재 새로운 수요가 크게 확대되고 있으며, 고객층 전체가 확대되고 있습니다. 그럼에도 불구하고, 독일의 수직형 머시닝 센터 시장은 여전히 견조한 실적을 유지할 것으로 전망됩니다. 이는 미텔슈탄트(중견 기업)의 위탁 가공업체들이 이를 인더스트리 4.0으로의 전환을 위한 이상적인 출발점으로 계속 인식하고 있기 때문입니다.

3축 가공기는 2025년 도입 대수의 52%를 차지하며, 알루미늄 판의 밀링 가공 및 철골 프레임 제조 분야에서 입문용 주력 기종으로서의 입지를 확고히 하고 있습니다. 한편, 방위 및 의료 분야의 구매자들은 5축 이상의 시스템에 대한 발주를 가속화하고 있으며, 이러한 시스템 시장은 2031년까지 연평균 성장률(CAGR) 5.1%로 확대될 것으로 전망됩니다. 복잡한 티타늄 가공을 위한 첨단 5축 플랫폼에 대한 주요 항공우주 및 방위 산업 계약업체들의 전략적 투자는 항공우주 분야의 엄격한 요구 사항이 이러한 전환을 얼마나 가속화하고 있는지를 보여줍니다.

독일의 5축 머시닝 센터 시장에서는 10마이크론 미만의 반복 정밀도에 대한 수요가 증가하고 있는 추세가 반영되고 있습니다. 오프라인 디지털 트윈 시뮬레이션을 채택한 지멘스의 SINUMERIK ONE 컨트롤러는 간섭이 없는 공구 경로 검증을 대폭 가속화하여, 소규모 수탁 가공 업체의 기술적 진입 장벽을 효과적으로 낮추고 있습니다. 4축 테이블은 캠샤프트나 크랭크샤프트 생산 라인에서 중견 틈새 시장을 유지하고 있지만, 전기차 설계가 보편화됨에 따라 복잡한 내연기관용 부품이 단계적으로 폐지되는 가운데, 그 생산량 증가세는 5축 기계의 급증에는 미치지 못하는 상황입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, germany machining centers market size is projected to expand from USD 1.38 billion in 2025 and USD 1.42 billion in 2026 to USD 1.65 billion by 2031, registering a CAGR of 3% between 2026 and 2031.

This report is Segmented by Machine Type (Horizontal Machining Centers, Vertical Machining Centers, and More), by Axis Configuration (3-Axis, 4-Axis, and 5-Axis & Above), by Spindle Orientation (Horizontal, Vertical, Multi-Spindle), by Structure Type (Column-Type, Gantry-Type, Moving-Table), and by End-User Industry (Automotive and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Machining Centers Market Trends and Insights

Industry 4.0 Demand Accelerates Adoption of Connected CNC Machining Centers

German facilities now specify Open Platform Communications Unified Architecture (OPC UA) and edge modules as standard so that production data stays on-premises, a core Manufacturing-X requirement. Bosch Rexroth's ctrlX Automation platform, certified under IEC 62443-4-2, separates motion control from the human-machine interface and cuts ransomware risk by 85%. Siemens refreshed its SINUMERIK 828D line in 2025 with Run MyVirtual Machine, trimming setup times 20% through offline collision checks. Substantial federal digitalization grants are accelerating equipment modernization, empowering small- to medium-sized job shops to replace their isolated, legacy mills with fully connected, Industry 4.0-ready alternatives. As a result, machines that arrive without native OPC UA ports or digital-twin licenses face shrinking order books.

Automotive Electrification Drives High-Precision Multi-Axis Machining Requirements

Battery housings, motor stators, and inverter casings demand sub-50-micron tolerances plus surface finishes below Ra 1.6 to optimize cooling and electromagnetic shielding. ZF achieved a Ra of 0.2 microns on aluminum e-motor housings after installing Nagel precision grinders. DMG MORI's new DMU 65 H monoBLOCK pairs a thermally stable casting with an 18,000 rpm spindle to shave 18% off battery-tray cycle time. The German Association of the Automotive Industry projects domestic EV output to hit 2.1 million units by 2028, implying the need for roughly 4,500 additional machining centers. Multi-tasking turn-mill platforms broaden appeal by combining milling, turning, and gear hobbing in a single setup, thereby reducing work-in-process inventory by 30% for Tier-1 suppliers.

High CAPEX and Rising Interest Rates Constrain New Machining Center Investments

The European Central Bank kept its deposit rate at 2.75% in March 2026, so seven-year equipment loans are still priced 1.5 percentage points above 2019 levels. A notable decline in manufacturing capacity utilization underscores a cautious capital expenditure environment, driven largely by operators waiting for relief from elevated borrowing costs. A 5-axis horizontal machine, often quoted at USD 1.6 million, now faces a 4-year payback period, well below the historic 6-year norm. Leasing, therefore, covers 42% of 2026 shipments, up from 31% three years earlier, while used-machine sales jumped 19% in 2025. High financing costs thus shave 0.5 percentage points off projected growth in the Germany machining centers market.

Other drivers and restraints analyzed in the detailed report include:

- Replacement of Aging Machine-Tool Base Boosts New Equipment Demand Across Mittelstand

- EU Net-Zero Industry Act Incentives Increase Machining for Renewable-Energy Components

- Shortage of Skilled 5-Axis Programmers and Operators Limits Advanced Machine Usage

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vertical machining centers held a 45.4% of the Germany machining centers market share in 2025, thanks to their lower purchase price and wide use in automotive casting rework and mold-and-die jobs. Shops favor them for quick installation and operator familiarity, so the installed base skews heavily toward three-axis vertical mills. However, aerospace primes and medical-device subcontractors are reallocating budgets toward universal and five-axis platforms that remove secondary setups and cut cycle time by up to 22% on turbine blades and spinal implants.

Universal/five-axis machining centers are projected to register a 4.8% CAGR through 2031, the fastest among all machine types. Their growth rests on tight-tolerance programs for Future Combat Air System fuselage panels and electric-vehicle (EV) motor housings, both of which demand simultaneous multi-face milling. While gantry and bridge-style machines have historically occupied a niche segment, the heavy machining requirements of the renewable energy sector are now driving significant new demand and expanding the overall customer pool. Even so, the Germany machining centers market for vertical models will maintain a robust valuation, as Mittelstand job shops continue to view them as the ideal entry point for Industry 4.0 retrofits.

Three-axis machines represented 52% of 2025 installations, cementing their role as entry-level workhorses for aluminum plate milling and steel frame fabrication. Yet defense and medical buyers are accelerating orders for five-axis and above systems, which are forecast to expand at a 5.1% CAGR to 2031. Strategic investments by major aerospace and defense contractors in advanced five-axis platforms for complex titanium machining demonstrate how heavy aerospace requirements are accelerating this pivot.

The Germany machining centers market for five-axis units reflects heightened demand for sub-10-micron repeatability. Siemens' SINUMERIK ONE controller, which uses offline digital twin simulation, drastically accelerates the verification of collision-free toolpaths, effectively lowering the technical barrier to entry for smaller job shops. Four-axis tables hold their mid-tier niche on camshaft and crankshaft lines, but their volume growth trails the five-axis surge as EV designs phase out complex internal-combustion components.

List of Companies Covered in this Report:

- DMG MORI AG

- TRUMPF GmbH + Co. KG

- CHIRON Group SE

- Gebr. Heller Maschinenfabrik GmbH

- Hermle AG

- Siemens AG

- EMAG GmbH & Co. KG

- INDEX-WERKE GmbH & Co. KG

- GROB-WERKE GmbH & Co. KG

- Knuth Werkzeugmaschinen GmbH

- MAG IAS GmbH

- Spinner Werkzeugmaschinenfabrik GmbH

- Okuma Europe GmbH

- Yamazaki Mazak Deutschland GmbH

- Haas Automation Europe

- Makino Europe GmbH

- FANUC Deutschland GmbH

- Hyundai WIA Europe

- Doosan Machine Tools Europe

- GF Machining Solutions GmbH

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Industry 4.0 demand accelerates adoption of connected CNC machining centers

- 4.2.2 Automotive electrification drives high-precision multi-axis machining requirements

- 4.2.3 Replacement of aging machine-tool base boosts new equipment demand across Mittelstand

- 4.2.4 EU Net-Zero Industry Act incentives increase machining for renewable energy components

- 4.2.5 Manufacturing-X cybersecurity compliance drives adoption of AI-enabled secure CNC controllers

- 4.2.6 Growing aerospace and defense machining demand strengthens advanced multi-axis machine utilization

- 4.3 Market Restraints

- 4.3.1 High CAPEX and rising interest rates constrain new machining center investments

- 4.3.2 Shortage of skilled 5-axis programmers and operators limits advanced machine usage

- 4.3.3 Export-control regulations restrict deployment of cloud-connected CNC systems

- 4.3.4 Semiconductor shortages delay machining center production and delivery timelines

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Machine Type

- 5.1.1 Horizontal Machining Centers (HMC)

- 5.1.2 Vertical Machining Centers (VMC)

- 5.1.3 Universal/5-Axis Machining Centers

- 5.1.4 Multi-Tasking Machining Centers (MTM)

- 5.1.5 Others (Gantry/Bridge-Type Centres, Turn-Mill Centers)

- 5.2 By Axis Configuration

- 5.2.1 3-Axis

- 5.2.2 4-Axis

- 5.2.3 5-Axis & Above

- 5.3 By Spindle Orientation

- 5.3.1 Horizontal

- 5.3.2 Vertical

- 5.3.3 Multi-spindle

- 5.4 By Structure Type

- 5.4.1 Column-Type

- 5.4.2 Gantry-Type

- 5.4.3 Moving-Table

- 5.5 By End-User Industry

- 5.5.1 Automotive

- 5.5.2 Aerospace & Defense

- 5.5.3 Energy (Oil-Gas, Renewables)

- 5.5.4 Medical Devices

- 5.5.5 Mold and Die Manufacturing

- 5.5.6 Others (General Manufacturing, Job Shops, Electronics, etc.)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 DMG MORI AG

- 6.4.2 TRUMPF GmbH + Co. KG

- 6.4.3 CHIRON Group SE

- 6.4.4 Gebr. Heller Maschinenfabrik GmbH

- 6.4.5 Hermle AG

- 6.4.6 Siemens AG

- 6.4.7 EMAG GmbH & Co. KG

- 6.4.8 INDEX-WERKE GmbH & Co. KG

- 6.4.9 GROB-WERKE GmbH & Co. KG

- 6.4.10 Knuth Werkzeugmaschinen GmbH

- 6.4.11 MAG IAS GmbH

- 6.4.12 Spinner Werkzeugmaschinenfabrik GmbH

- 6.4.13 Okuma Europe GmbH

- 6.4.14 Yamazaki Mazak Deutschland GmbH

- 6.4.15 Haas Automation Europe

- 6.4.16 Makino Europe GmbH

- 6.4.17 FANUC Deutschland GmbH

- 6.4.18 Hyundai WIA Europe

- 6.4.19 Doosan Machine Tools Europe

- 6.4.20 GF Machining Solutions GmbH

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment