|

시장보고서

상품코드

2063640

아시아태평양의 머시닝 센터 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Asia-Pacific Machining Centers - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

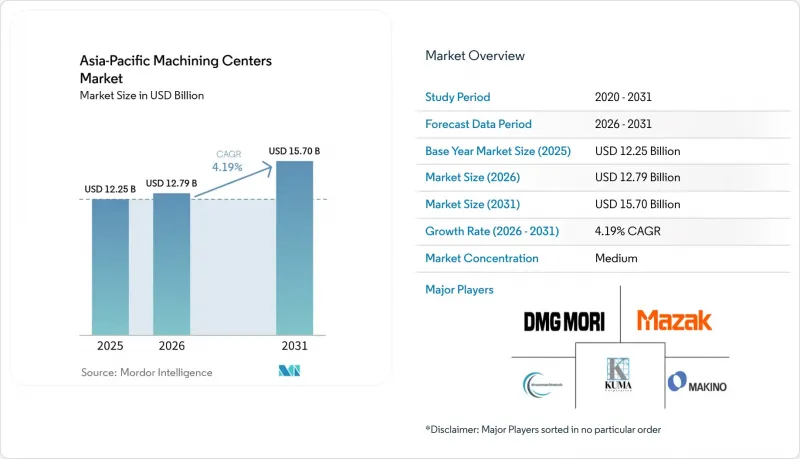

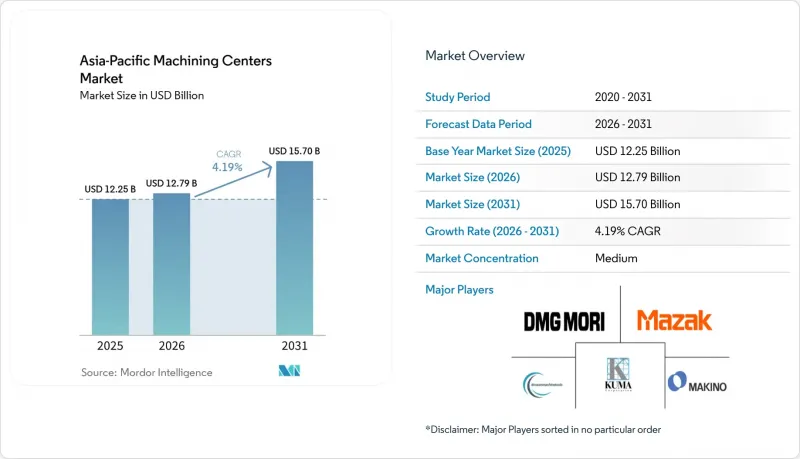

Mordor Intelligence에 의하면, 아시아태평양 머시닝 센터 시장 규모는 2025년에 122억 5,000만 달러로 평가되었고 2026년 127억 9,000만 달러에서 2031년까지 157억 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.19%를 나타낼 전망입니다.

본 보고서는 기계 유형별(수평형 머시닝 센터 등), 축 구성별(3축, 4축, 5축 이상), 주축 방향별(수평형, 기타), 구조 유형별(컬럼형, 갠트리형, 이동 테이블형), 최종 사용자 산업별(자동차, 기타), 국가(중국, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제공됩니다.

아시아태평양 머시닝 센터 시장 동향 및 분석

아시아태평양에서의 전자기기 제조 재유입이 정밀 가공 수요를 가속화하고 있습니다.

전자기기 조립 제조업체와 인쇄회로기판 제조업체들이 사업 거점을 다각화하는 가운데, 새로운 생산 라인 구축에 따라 필수적인 금형, 지그, 다이를 제조하기 위한 정밀 밀링 가공 및 선반 가공 설비에 대한 수요가 증가하고 있습니다. 베트남에서는 삼성의 6개 주요 생산 거점과 북부 여러 성에 위치한 견고한 애플 공급업체 집적지가 주요 전자기기 제조 허브를 형성하고 있으며, 이러한 요인들이 맞물려 소형 수직 머시닝 센터에 대한 현재 및 향후 수주량을 끌어올리고 있습니다. 한편, 인도에서는 확대되는 하이테크 공급망의 일환으로 첸나이에 월 120만 대 생산을 목표로 하는 3,000만 달러 규모의 알루미늄 케이스 제조 시설이 신설되면서, 유연성이 높은 가공 셀에 대한 수요가 높아지고 있음이 부각되었습니다. 또한 남쪽의 태국에서는 투자위원회가 2025년까지 전자기기 및 가전 분야에 총 89억 1,000만 달러 규모의 투자를 승인했습니다. 이러한 급증은 첨단 커넥터 가공용 공구에 대응하는 고속 스핀들 플랫폼에 크게 좌우될 것입니다. 전반적으로 조달 동향은 기존의 대량 생산에서 다품종 소량 생산 능력으로 전환되고 있으며, 이에 따라 지역 머시닝 센터 시장은 더욱 가속화되고 있습니다. 이러한 수익성이 높은 첨단 기술 공급망에 진입하기 위해서는 ISO 9001 품질 감사 인증을 취득해야 하므로, 중견 기계 가공 업체들조차 구식 설비를 업그레이드할 수밖에 없는 실정입니다.

내연기관(ICE)에서 전기차(EV)로의 파워트레인 전환이 자동차 업계 전반에 걸쳐 다축 가공의 도입을 촉진하고 있습니다.

내연기관에서 배터리 구동 방식으로의 전환에 따라 많은 기존 부품이 불필요해지는 한편, 모터 하우징, 배터리 트레이, 감속 기어 등 동시 5축 가공이 필요한 새로운 정밀 가공 수요가 대두되고 있습니다. 우노 민다(Uno Minda)사는 알루미늄 배터리 트레이 전용 5축 가공 셀을 도입하기 위해 푸네 공장에 5,100만 달러를 투자하고, 2026년에 생산을 시작할 예정입니다. 일본 경제산업성이 시행한 첨단 5축 컨트롤러에 대한 수출 규제는 이 기술의 전략적 가치를 여실히 보여주고 있습니다. 전기차 판매량이 증가함에 따라, 공급업체들이 3축 라인에 회전 테이블을 추가해 업그레이드하거나 완전한 다축 플랫폼을 구매하는 추세로 인해 아시아태평양의 머시닝 센터 시장이 혜택을 보고 있습니다. 또한, 자동차 업계가 배터리의 막대한 무게를 대형 알루미늄 구조 주조품으로 상쇄하려는 노력에 따라, 넓은 가공 범위와 높은 토크를 갖춘 다축 머시닝 센터에 대한 수요가 가속화되고 있습니다. 이러한 구조적 변화로 인해, 수익성이 높은 장기적인 EV 플랫폼 계약 확보를 목표로 하는 1차 공급업체들의 지속적인 설비 투자가 확실해지고 있습니다.

막대한 초기 설비 투자(CAPEX)와 긴 회수 기간이 신규 설비 투자를 제한하고 있습니다.

중급급 5축 머시닝 센터의 가격은 최대 80만 달러에 달할 수 있으며, 설치비와 공구비를 포함한 5년간의 총 소유 비용은 종종 120만 달러를 초과합니다. 베트남과 태국의 중소기업들은 순이익률이 8% 미만에 그치고 있어, 정부의 공동 출자 없이는 은행 대출을 확보하는 데 어려움을 겪고 있습니다. 현재 기계 제조업체들은 모듈식 설계를 추진하고 있으며, 구매자는 먼저 3축 프레임부터 도입한 뒤 나중에 회전 테이블을 추가함으로써 자금 지출을 수년까지 분산할 수 있습니다. 인도나 인도네시아에서는 리스나 스핀들 가동 시간에 따른 과금 모델이 등장하면서 진입 장벽은 낮아졌지만, 벤더의 가동률 보장에 대한 의존도가 높아지고 있습니다. 자금 조달 조건이 완화될 때까지, 이러한 제약은 아시아태평양의 머시닝 센터 시장, 특히 2차 공급업체들에게 부담이 될 것입니다.

부문별 분석

2025년, 아시아태평양 지역의 머시닝 센터 시장 점유율 중 38%를 수직형 머시닝 센터가 차지했습니다. 이는 엔진 블록이나 금형 베이스와 같은 일반적인 직육면체 부품을 스핀들 시간당 비용이 가장 낮게 가공할 수 있기 때문입니다. 중국, 인도, 태국 전역에 걸쳐 구축된 딜러 지원 체계를 통해 유지보수 비용을 낮게 유지할 수 있으며, 위탁 가공 업체는 신속하게 생산 능력을 확대할 수 있습니다. 베트남이나 말레이시아의 가전제품 공급업체로부터의 수주에서도, 제한된 설치 공간에 적합하고 중력을 이용해 절삭 부스러기를 배출함으로써 알루미늄 하우징의 표면 마감을 유지할 수 있는 수직형 모델이 선호되고 있습니다. 아시아태평양의 머시닝 센터 시장은 태국에서 진행 중인 47건의 전자기기 프로젝트로부터 추가적인 견인력을 얻고 있으며, 이들 프로젝트의 상당수는 커넥터 가공용으로 고속 VMC 셀을 지정하고 있습니다.

아시아태평양의 멀티태스킹 머시닝 센터 시장 규모는 구매자들이 바닥 면적을 절약하기 위해 밀링 가공과 선반 가공을 통합하려는 추세에 힘입어 2026년부터 2031년까지 연평균 성장률(CAGR) 6.20%로 확대될 것으로 전망됩니다. DMG 모리의 NTX 시리즈, ACCUWAY의 선반 및 밀링 머신 라인, 그리고 톤타이의 3터렛 플랫폼을 통해 항공우주 및 의료 관련 공장에서는 단 한 번의 세팅으로 복잡한 부품의 마무리 가공이 가능해지며, 재공품을 최대 40%까지 줄일 수 있습니다. 이러한 기계에는 두 가지 G코드 계열 모두에 정통한 작업자가 필요하지만, 아세안 지역에서는 그러한 인력이 부족하기 때문에 제조업체들은 도입을 가속화하기 위해 시뮬레이션 소프트웨어와 원격 지원을 세트로 제공합니다. 자동차 부품 공급업체들이 전기차용 배터리 트레이의 생산 체계를 재구축함에 따라, 동일한 플랫폼에서 거친 가공, 정밀 가공, 프로브 측정을 결합한 멀티태스킹 기능을 요구하는 사례가 증가하고 있으며, 이것이 성장세를 뒷받침하고 있습니다.

3축 시스템은 프로그래밍을 단순하게 유지하면서도 대부분의 강재 및 알루미늄 부품에 허용되는 공차를 실현할 수 있기 때문에 2025년 아시아태평양 머시닝 센터 시장 점유율의 46%를 차지했습니다. 자동차 및 가전제품 분야의 2차 공급업체들은 최소한의 작업자 교육만으로 짧은 납기일을 맞출 수 있도록 이러한 기계에 의존하고 있습니다. 또한 중국과 인도의 재생업체들도 신제품 가격의 60% 수준에 중고 3축 유닛을 공급하고 있어, 그 보급 범위를 더욱 확대되고 있습니다.

5축 플랫폼 시장은 2031년까지 연평균 성장률(CAGR) 6.80%로 성장하고 있으며, 이는 동시 윤곽 가공이 필요한 터빈 블레이드, 항공우주용 브래킷, 전기차용 모터 하우징에 대한 수요를 반영한 것입니다. Yumoto Denki사의 32팔레트 자동 셀에서는 현재 5축 머신을 18시간 동안 무인 가동하고 있으며, 정교한 설정을 통해 생산성을 향상시킬 수 있음을 입증하고 있습니다. 일본에서 3미크론 미만의 정밀도를 가진 부품에 대한 수출 규제는 지역 내 조달을 강화하고, 기술 지원 및 교육을 일본, 한국, 대만에 집중시키는 요인이 되고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the asia-Pacific machining centers market size was valued at USD 12.25 billion in 2025 and is estimated to grow from USD 12.79 billion in 2026 to reach USD 15.70 billion by 2031, at a CAGR of 4.19% during the forecast period (2026-2031).

This report is Segmented by Machine Type (Horizontal Machining Centers, and More), by Axis Configuration (3-Axis, 4-Axis, 5-Axis & Above), by Spindle Orientation (Horizontal, and More), by Structure Type (Column-Type, Gantry-Type, and Moving-Table), by End-User Industry (Automotive, and More), and by Country (China, and More). The Market Forecasts are Provided in Terms of Value (USD).

Asia-Pacific Machining Centers Market Trends and Insights

Electronics Manufacturing Reshoring in Asia-Pacific Accelerates Precision Machining Demand

As electronics assemblers and printed circuit board manufacturers diversify their geographic footprints, the establishment of new production lines is driving the need for precision milling and turning equipment to produce essential molds, jigs, and dies. In Vietnam, Samsung's six major manufacturing complexes and the robust Apple supplier corridors in the northern provinces have established a dominant electronics manufacturing hub, collectively boosting current and forward-looking orders for compact vertical machining centers. Meanwhile, India's expanding tech supply chain saw the addition of a USD 30 million aluminum-housing facility in Chennai, designed to produce 1.2 million units per month, underscoring the growing need for flexible machining cells. Further south, Thailand's Board of Investment approved a total of USD 8.91 billion in electronics and electrical appliance investments for 2025. This surge will heavily depend on high-speed spindle platforms for advanced connector tooling. Overall, procurement trends are shifting away from traditional mass production toward high-mix, small-batch capabilities, further accelerating the regional machining centers market. Because mandatory ISO 9001 quality audits are required to enter these lucrative tech supply chains, even mid-tier machine shops are being compelled to upgrade their legacy equipment.

Internal Combustion Engine (ICE)-to-Electric Vehicle (EV) Powertrain Shift Drives Multi-Axis Machining Adoption Across Automotive Sector

Shifting from internal-combustion engines to battery power removes many legacy parts yet introduces new precision needs for motor housings, battery trays, and reduction gears that call for simultaneous five-axis cutting. Uno Minda invested USD 51 million in its Pune plant to install 5-axis cells dedicated to aluminum battery trays, with production slated for 2026. Japan's trade ministry's export controls on advanced five-axis controllers underscore the technology's strategic value. As EV volumes rise, the Asia-Pacific machining centers market benefits as suppliers either upgrade three-axis lines with rotary tables or buy full multi-axis platforms. Furthermore, the automotive push to offset the massive weight of batteries with large-scale aluminum structural castings is accelerating demand for large-envelope, high-torque multi-axis centers. This structural shift ensures sustained capital expenditure from Tier 1 suppliers eager to secure lucrative, long-term EV platform contracts.

High Upfront Capital Expenditure (CAPEX) and Long Payback Periods Limit New Equipment Investments

A mid-range five-axis machining center can cost up to USD 800,000, while total ownership over five years often exceeds USD 1.2 million, including installation and tooling. Small firms in Vietnam and Thailand run on net margins below 8% and struggle to secure bank financing without state co-investment. Machine builders now push modular designs so buyers can start with a three-axis frame and bolt on rotary tables later, spreading cash outlay across several years. Leasing and pay-per-spindle-hour models are emerging in India and Indonesia, lowering barriers yet creating dependence on vendor uptime guarantees. Until financing terms ease, this restraint will weigh on the Asia-Pacific machining centers market, especially among tier-2 suppliers.

Other drivers and restraints analyzed in the detailed report include:

- Smart Factory Incentives in China Japan and South Korea Boost Computer Numerical Control (CNC) Automation Investments

- Dark Factory Expansion in China and Singapore Drives Automated Machining Center Deployment

- Skilled Labor Shortages Across ASEAN Hinder Machining Center Utilization

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Vertical machining centers accounted for 38% of the Asia-Pacific machining centers market share in 2025 because they cut common prismatic parts such as engine blocks and mold bases at the lowest cost per spindle hour. Widespread dealer support across China, India, and Thailand keeps maintenance costs low and lets job shops add capacity quickly. Orders from consumer-electronics suppliers in Vietnam and Malaysia also favor vertical formats that fit tight floor plans and evacuate chips by gravity, preserving surface finish on aluminum housings. The Asia-Pacific machining centers market gains additional pull from Thailand's 47 electronics projects, many of which specify high-speed VMC cells for connector tooling.

The Asia-Pacific machining centers market size for multi-tasking machining centers is projected to expand at a 6.20% CAGR between 2026 and 2031 as buyers consolidate milling and turning to save floor space. DMG Mori's NTX series, ACCUWAY turn-mill lines, and Tongtai's three-turret platform enable aerospace and medical shops to finish complex parts in a single setup, reducing work-in-process by up to 40%. These machines demand operators fluent in both G-code families, which is scarce across ASEAN, so builders bundle simulation software and remote support to speed adoption. As automotive suppliers retool for electric-vehicle battery trays, they increasingly specify multi-tasking capability to combine roughing, finishing, and probing on the same platform, reinforcing the growth trajectory.

Three-axis systems held 46% of the Asia-Pacific machining centers market share in 2025 because they achieve tolerances acceptable for most steel and aluminum parts while keeping programming simple. Tier-2 automotive and appliance vendors rely on these machines to meet short delivery windows with minimal operator training. Chinese and Indian refurbishers also supply used three-axis units at 60% of new-machine prices, further extending their footprint.

Five-axis platforms are advancing at a 6.80% CAGR through 2031, reflecting demand for turbine blades, aerospace brackets, and electric-vehicle motor housings that require simultaneous contouring. Yumoto Denki's 32-pallet automated cell now runs five-axis machines 18 hours unattended, proving the productivity boost achievable with advanced setups. Export controls on sub-3-micron accuracy units from Japan reinforce regional sourcing, concentrating technical support and training in Japan, South Korea, and Taiwan.

List of Companies Covered in this Report:

- Yamazaki Mazak Corporation

- DMG Mori Co., Ltd.

- Okuma Corporation

- Makino Milling Machine Co., Ltd.

- Doosan Machine Tools Co., Ltd.

- Hyundai WIA Corporation

- Haas Automation, Inc.

- JTEKT Corporation

- Fanuc Corporation

- Fair Friend Group

- Hurco Companies, Inc.

- MHI Machine Tool Co., Ltd.

- Chongqing Machine Tool Co., Ltd.

- Guangdong Taikan NC Machine Co., Ltd.

- Dalian Machine Tool Group

- Brother Industries, Ltd.

- Kiwa Japan Co., Ltd.

- Hwacheon Machine Tools Co., Ltd.

- Ace Micromatic Group

- Shanghai THREEGUN Machine Tool Co., Ltd.

- Shenyang Machine Tool Co., Ltd.

- Nidec Machine Tool Corporation

- Sodick Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electronics manufacturing reshoring in Asia-Pacific accelerates precision machining demand

- 4.2.2 ICE-to-EV powertrain shift drives multi-axis machining adoption across automotive sector

- 4.2.3 Smart factory incentives in China, Japan, and South Korea boost CNC automation investments

- 4.2.4 Asia-Pacific space start-ups increase demand for advanced precision machining capabilities

- 4.2.5 Dark factory expansion in China and Singapore drives automated machining center deployment

- 4.2.6 Titanium implant manufacturing growth in India raises need for high-precision machining

- 4.3 Market Restraints

- 4.3.1 High upfront CAPEX and long payback periods limit new equipment investments

- 4.3.2 Skilled labor shortages across ASEAN hinder machining center utilization

- 4.3.3 Semiconductor capex volatility disrupts machining equipment demand cycles

- 4.3.4 Retrofit preference over new machine purchases in Japan slows market growth

- 4.4 Value/Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Industry Attractiveness - Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Machine Type

- 5.1.1 Horizontal Machining Centers (HMC)

- 5.1.2 Vertical Machining Centers (VMC)

- 5.1.3 Universal/5-Axis Machining Centers

- 5.1.4 Multi-Tasking Machining Centers (MTM)

- 5.1.5 Others (Gantry/Bridge-Type Centers, Turn-Mill Centers)

- 5.2 By Axis Configuration

- 5.2.1 3-Axis

- 5.2.2 4-Axis

- 5.2.3 5-Axis & Above

- 5.3 By Spindle Orientation

- 5.3.1 Horizontal

- 5.3.2 Vertical

- 5.3.3 Multi-spindle

- 5.4 By Structure Type

- 5.4.1 Column-Type

- 5.4.2 Gantry-Type

- 5.4.3 Moving-Table

- 5.5 By End-User Industry

- 5.5.1 Automotive

- 5.5.2 Aerospace & Defense

- 5.5.3 Energy (Oil-Gas, Renewables)

- 5.5.4 Medical Devices

- 5.5.5 Mold and Die Manufacturing

- 5.5.6 Others (General Manufacturing, Job Shops, Electronics, etc.)

- 5.6 By Country

- 5.6.1 China

- 5.6.2 Japan

- 5.6.3 India

- 5.6.4 Australia

- 5.6.5 South Korea

- 5.6.6 Rest of Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Yamazaki Mazak Corporation

- 6.4.2 DMG Mori Co., Ltd.

- 6.4.3 Okuma Corporation

- 6.4.4 Makino Milling Machine Co., Ltd.

- 6.4.5 Doosan Machine Tools Co., Ltd.

- 6.4.6 Hyundai WIA Corporation

- 6.4.7 Haas Automation, Inc.

- 6.4.8 JTEKT Corporation

- 6.4.9 Fanuc Corporation

- 6.4.10 Fair Friend Group

- 6.4.11 Hurco Companies, Inc.

- 6.4.12 MHI Machine Tool Co., Ltd.

- 6.4.13 Chongqing Machine Tool Co., Ltd.

- 6.4.14 Guangdong Taikan NC Machine Co., Ltd.

- 6.4.15 Dalian Machine Tool Group

- 6.4.16 Brother Industries, Ltd.

- 6.4.17 Kiwa Japan Co., Ltd.

- 6.4.18 Hwacheon Machine Tools Co., Ltd.

- 6.4.19 Ace Micromatic Group

- 6.4.20 Shanghai THREEGUN Machine Tool Co., Ltd.

- 6.4.21 Shenyang Machine Tool Co., Ltd.

- 6.4.22 Nidec Machine Tool Corporation

- 6.4.23 Sodick Co., Ltd.

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment