|

시장보고서

상품코드

2062470

상업 및 산업용 에너지 저장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Commercial and Industrial Energy Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

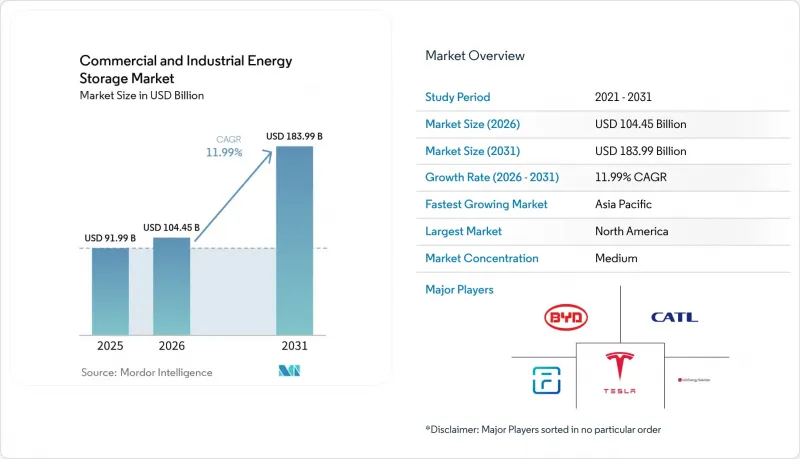

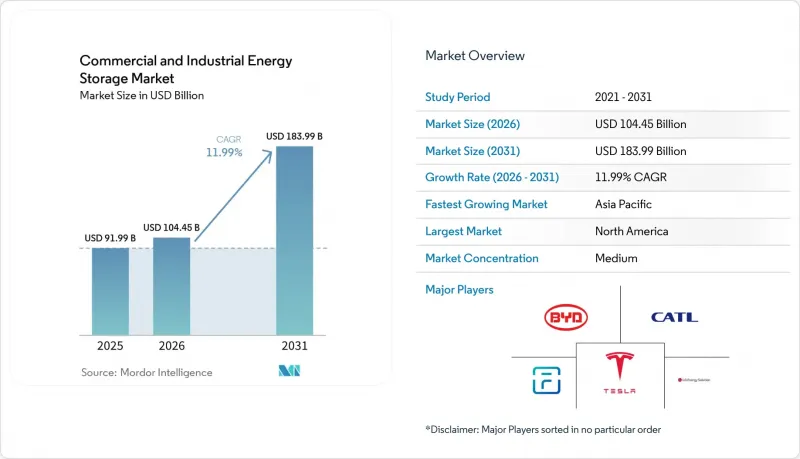

Mordor Intelligence에 의하면, 상업 및 산업용 에너지 저장 시장 규모는 2025년 919억 9,000만 달러로 평가되었습니다. 2026년에는 1,044억 5,000만 달러로 확대되어 2031년까지 1,839억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 11.99%로 성장할 전망입니다.

본 보고서는 기술별(리튬 이온, 나트륨 이온, 납축전지, 플로우 배터리, 기타), 용도별(피크 부하 절감, 부하 이동, 백업 전원/UPS, 기타), 최종 사용자별(상업용 빌딩, 데이터센터, 기타), 지역별(북미, 아시아태평양, 유럽, 남미, 중동 및 아프리카)로 분류되어 있습니다. 시장 전망은 금액(달러) 단위로 제시되어 있습니다.

세계의 상업 및 산업용 에너지 저장 시장 동향 및 인사이트

리튬 이온 배터리의 비용 곡선이 90달러/kWh 미만의 수준에 근접

2025년 고정형 배터리 팩의 가격은 kWh당 평균 70달러로, 2020년 대비 35% 하락하여, 전기 요금이 높은 지역의 상업시설에서 3-5년 내에 투자 회수가 일반적인 수준에 도달했습니다. 중국 내 생산 규모 확대와 코발트가 포함되지 않은 LFP 화학 조성으로의 전환을 통해 재료 비용이 최대 20% 절감되었습니다. 설비 투자 비용의 감소로 인해 대상 고객층이 하이퍼스케일 사용자에서 중규모 산업 플랜트로 확대되면서, 상업 및 산업용 에너지 저장 시장에서 새로운 수요가 창출되고 있습니다. LG 에너지솔루션과 테슬라 간의 43억 달러 규모의 LFP 계약 등 주요 공급 계약들은 향후 18개월 동안 가격이 하락할 것이라는 전망을 시사하고 있습니다. 나트륨 이온 배터리 및 초기 단계의 전고체 배터리 시범 생산 라인을 통해 2026년 말까지 평균 설치 비용이 kWh당 350달러 미만으로 떨어질 것으로 예상되며, 이에 따라 비용에 민감한 부문에서의 보급이 더욱 확대될 것입니다.

전 세계 재생에너지 의무화 및 기업의 RE100 목표

400개 이상의 다국적 기업이 100% 재생 가능 전력으로의 전환을 공약하고 있으며, 이들의 총 소비량은 연간 380TWh 이상에 달하고, 이는 독일의 전력 수요와 거의 맞먹는 수준입니다. 이러한 공약에 따라 대규모 시설은 낮 시간대의 태양광 발전과 야간 풍력 발전으로 발생한 잉여 전력을 저장해 두었습니다가 저녁 시간대의 피크 시간대에 공급해야 할 필요에 직면하게 되었으며, 이에 따라 변동하는 발전 출력을 조절 가능한 공급원으로 전환하고 있습니다. 2025년 중반부터 가동 중인 구글의 미네소타주 300MW/30GWh 규모 프로젝트는 화석연료를 이용한 피크 대응 발전에 대한 의존도를 85% 줄였으며, 기업의 대규모 도입을 보여주는 좋은 사례가 되고 있습니다. 유럽에서는 ‘REPowerEU’ 계획에 따라 2030년까지 전력의 45%를 재생에너지로 충당해야 할 의무가 부과되어 있으며, 에너지 저장 목표와 송전망 혼잡 완화가 명확하게 연계되어 있습니다. 현재 독일의 산업 사업자들에게는 1MWh당 100유로에 육박하는 출력 제한 벌금이 부과되고 있어, 배터리는 비용 대비 효과가 높은 리스크 헤지 수단이 되고 있습니다.

디젤 발전기와의 비교 : 높은 설비 투자 비용

설치 비용이 280-580달러/kWh인 반면, 디젤 발전기의 초기 비용은 500-1,000달러/kW로, 수명 주기 비용 측면에서 우수함에도 불구하고, 저비용 자금 조달 수단을 갖추지 못한 중소기업에게는 여전히 장벽으로 작용하고 있습니다. EaaS(Energy-as-a-service) 계약은 자본 측면의 장벽을 완화하는 데 도움이 되지만, 거래의 복잡성을 가중시킵니다.

부문별 분석

2025년 기준으로 리튬이온 기술은 상업 및 산업용 에너지 저장 시장의 80.4%를 차지했습니다. 이는 80% 방전 깊이에서 6,000회 이상의 사이클 수명과 열 폭주 위험이 낮다는 점이 주된 이유입니다. CATL과 BYD가 상용화한 나트륨 이온 플랫폼은 풍부한 원자재와 고정형 용도 분야에서 LFP(인산철리튬)에 비해 가격 경쟁력이 높아, 2031년까지 연평균 성장률(CAGR) 37.5%로 성장하고 있습니다. 에너지 밀도는 NMC(니켈-망간-카바라이저)보다 낮지만, 창고 옥상이나 지상 설치형 야드에는 충분한 공간이 있어 상업용 사용자에게는 이러한 단점이 상쇄되고 있습니다. 납축전지는 통신용 백업이라는 틈새 시장에 남아 있지만, 환경 폐기물 규제로 인해 그 시장 점유율은 해마다 감소하고 있습니다. 흐름 전지, 특히 바나듐 레독스 및 철 흐름 전지는 4시간을 초과하는 장시간 방전 용도에서 그 입지를 다져가고 있으며, ESS는 2025년에 산업용 마이크로그리드에 500MWh를 공급할 예정입니다. 하이브리드 슈퍼커패시터는 PJM 등 시장에서 주파수 조정 계약을 확보하고 있지만, 에너지 밀도가 낮기 때문에 대상 시장 규모에는 한계가 있습니다. 전고체 전지는 여전히 실증 단계에 머물러 있으며, 제조 규모의 확대와 관련된 과제가 해결되지 않았기 때문에 2028년 이전에 광범위하게 도입되기는 어려울 것으로 보입니다. 현재 미국이나 유럽에서 일반적으로 적용되고 있는 UL 9540A 규격의 필수 시험은 프로젝트당 3만-5만 달러의 추가 비용이 소요되지만, 보험료를 최대 25% 절감할 수 있으므로 해당 규격을 준수하는 공급업체에게는 수명 주기 비용 측면에서 이점이 있습니다.

잔여 용량(SOH)이 70-80%인 폐차용 자동차 배터리 팩은 가치를 중시하는 구매자들의 관심을 끌고 있으며, 신규 시스템에 비해 40-50% 저렴한 총 비용을 제공합니다. 그러나 표준화는 더딘 임베디드니다. 보증 제도, 셀의 추적성, 그리고 화학 조성의 다양성이 통합을 복잡하게 만들고 있습니다. 그 결과로 발생하는 뒤죽박죽인 상황은 광범위한 보급을 지연시키고 있지만, 스페인과 캘리포니아에서 진행 중인 지역 한정 시범 사업은 가격에 민감한 상업용 사용자에게 미래 가능성을 보여주고 있습니다. 전반적으로, 기술의 다양화는 선택의 폭을 넓히는 한편, 리튬 이온의 기존 우위를 강화하여 상업 및 산업용 에너지 저장 시장에서 그 주도적인 위치를 유지하고 있습니다.

지역별 분석

2025년, 북미는 전 세계 설치량의 36.5%를 차지했으며, 독립형 에너지 저장 시스템에 대한 투자 세액 공제(ITC)로 인해 병설 요건이 폐지됨에 따라 미국이 그 대부분을 차지했습니다. 캘리포니아주가 주도적인 역할을 맡고 있는 가운데, 1kWh당 최대 200달러를 환급해 주는 ‘자가 발전 인센티브 프로그램’에 따라 2025년 말까지 3GW를 넘는 상업용 설비를 도입했습니다. 텍사스주가 그 뒤를 잇습니다. ERCOT의 순수 에너지 시장에서는 여름철 피크 시간대에 kWh당 0.20달러 이상의 가격 변동이 발생하기 때문에 도매 차익거래에 가장 적합하기 때문입니다. 캐나다의 성장은 온타리오주와 앨버타주에 집중되어 있으며, 주 정부의 인센티브와 마이크로그리드에 대한 수요가 맞물리고 있습니다. 멕시코는 여전히 개발도상국 단계에 있습니다. 저렴한 비용과 자금 조달의 어려움이 도입을 제한하고 있지만, 몬테레이의 제조업 구역에서는 시범 프로젝트가 진행 중입니다. 아시아태평양은 가장 빠르게 성장하는 지역으로, 2031년까지의 연평균 성장률(CAGR)은 23.3%로 예측됩니다. 중국의 수직 통합형 대기업이 전 세계 상용 출하량의 절반 이상을 공급하고 있으며, 평균 시스템 비용을 유럽 및 미국의 동급 제품보다 20-30% 낮게 유지하고 있습니다. 인도에서는 500kW를 초과하는 상업용 태양광 발전 시설에 대해 2시간 분량의 전력 저장을 의무화하고 있으며, 구자라트주와 마하라슈트라주에서 관련 활동이 활발해지고 있습니다. 일본과 한국은 자연재해나 공급망 혼란에 대한 회복탄력성을 최우선으로 삼고 있으며, 도요타와 같은 기업 구매자들이 자사 부지 내에 배터리 저장 설비를 설치하도록 장려하고 있습니다. 아세안 각국의 진전 상황은 제각각이며, 태국이나 베트남에서는 축전 시스템을 도입하는 외국계 공장이 유치되고 있는 반면, 인도네시아에서는 디젤 연료에 대한 보조금이 도입 진전을 늦추고 있습니다. 호주 및 뉴질랜드에서는 소매 전기 요금이 비싸고, 지붕 위 태양광 발전이 널리 보급되어 있어 자가 소비의 이점이 커짐에 따라 적극적으로 도입이 추진되고 있습니다.

독일의 산업 단지에서는 재생에너지로 인해 연간 200일 이상 현물 가격이 마이너스가 되는 상황에서 출력 제한 요금을 피하기 위해 축전지가 도입되고 있습니다. 영국의 용량 시장 경매에서는 수 시간 동안 가동 가능한 자산이 우대받기 때문에 슈퍼마켓 체인이나 택배 센터들이 12년 계약으로 에너지 저장 설비를 도입하는 움직임이 활발해지고 있습니다. 프랑스, 스페인, 이탈리아에서는 증가하는 태양광 발전 프로젝트를 통합하고, ‘Fit for 55’의 탈탄소화 목표를 달성하기 위해 도입 규모를 확대되고 있습니다. 북유럽 국가들에서는 풍력 발전과 수력 발전을 통해 전력 균형을 조정하고 있지만, 그럼에도 주파수 안정화와 송전망 혼잡 완화를 위해 축전지를 도입하고 있습니다. 러시아는 낮은 요금과 인센티브 부족으로 인해 뒤처져 있으며, 도입은 외딴 지역의 광산이나 석유 및 가스 전초기지로 한정되어 있습니다. 남미, 중동 및 아프리카에서는 브라질, 아랍에미리트, 남아프리카공화국이 쇼핑몰과 통신 시설에서 시범 사업을 전개하고 있습니다. 지역 간 격차는 존재하지만, 현재 모든 대륙에서 상업용 프로젝트가 보고되고 있어 상업 및 산업용 에너지 저장 시장의 지리적 확대가 부각되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the commercial and industrial energy storage market size is expected to increase from USD 91.99 billion in 2025 to USD 104.45 billion in 2026 and reach USD 183.99 billion by 2031, growing at a CAGR of 11.99% over 2026-2031.

This report is Segmented by Technology (Lithium-Ion, Sodium-Ion, Lead-Acid, Flow Batteries, and Others), Application (Peak Shaving, Load Shifting, Backup Power/UPS, and More), End-User (Commercial Building, Data Centers, and More), and Geography (North America, Asia-Pacific, Europe, South America, and Middle East and Africa). Market Forecasts are Provided in Value (USD).

Global Commercial and Industrial Energy Storage Market Trends and Insights

Li-ion Cost Curve Approaching Sub-USD 90/kWh

Stationary battery pack prices averaged USD 70 per kWh in 2025, a 35% drop from 2020, crossing the point where three-to-five-year paybacks become common for commercial facilities in high-tariff regions. Manufacturing scale in China and the pivot to cobalt-free LFP chemistries have trimmed material costs by up to 20%. Lower capex broadens the addressable base from hyperscale users to mid-sized industrial plants, stimulating fresh demand for the commercial and industrial energy storage market. Major supply contracts, such as LG Energy Solution's USD 4.3 billion LFP deal with Tesla, signal sustained downward pricing over the next 18 months. Pilot lines for sodium-ion and early solid-state designs are expected to push average installed costs beneath USD 350 per kWh by late 2026, deepening penetration across cost-sensitive sectors.

Global Renewable Mandates & Corporate RE100 Targets

More than 400 multinational firms have pledged 100% renewable electricity, together consuming upwards of 380 TWh annually, roughly Germany's load. These commitments force large facilities to store surplus midday solar and nighttime wind for evening peaks, converting variable output into dispatchable supply. Google's 300 MW / 30 GWh Minnesota project, operational since mid-2025, cuts fossil peaker reliance by 85% and exemplifies large-scale corporate adoption. In Europe, the REPowerEU plan mandates that 45% of electricity be renewable by 2030, explicitly linking storage targets to congestion relief. Industrial operators in Germany now face curtailment penalties approaching EUR 100 per MWh, making batteries a cost-effective hedge.

High CAPEX vs Diesel Gensets

Installed costs of USD 280-580/kWh still exceed a diesel generator's USD 500-1,000/kW upfront, deterring smaller enterprises lacking low-cost finance, despite superior lifetime economics. Energy-as-a-service contracts help mitigate capital barriers but add transaction complexity.

Other drivers and restraints analyzed in the detailed report include:

- Stand-alone Storage ITC & Equivalent Global Incentives

- Rising Global C&I Peak-Demand Charges

- Critical-Mineral Supply-Chain Volatility

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Lithium-ion technologies controlled 80.4% of the commercial and industrial energy storage market in 2025, thanks to cycle lives exceeding 6,000 cycles at 80% depth of discharge and lower thermal-runaway risk. Sodium-ion platforms, commercialized by CATL and BYD, are expanding at a 37.5% CAGR through 2031, enabled by abundant raw materials and parity pricing with LFP for stationary duties. Although energy density trails NMC, warehouse rooftops and ground-mount yards offer ample space, softening the penalty for commercial users. Lead-acid remains in telecom backup niches, but environmental disposal rules erode its share each year. Flow batteries, especially vanadium redox and iron-flow variants, are carving out long-duration roles beyond four-hour discharge, with ESS Inc. delivering 500 MWh to industrial microgrids in 2025. Hybrid supercapacitors secure frequency-regulation contracts in markets like PJM, though low energy density caps their addressable segment. Solid-state chemistries linger in pilot stages; wide deployment before 2028 appears unlikely, given unresolved manufacturing scale-up hurdles. Mandatory UL 9540A testing, now common in the United States and Europe, adds USD 30,000-50,000 per project but cuts insurance costs by up to 25%, improving lifecycle economics for compliant suppliers.

Second-life automotive packs, retired at 70-80% state of health, entice value-oriented buyers, offering landed costs 40-50% below new systems. Standardization, however, lags: warranty schemes, cell traceability, and varying chemistries complicate integration. The resulting patchwork slows widespread adoption, but localized pilots in Spain and California illustrate promise for price-sensitive commercial users. On balance, technology diversification widens choice yet reinforces lithium-ion's incumbency, sustaining its leading position in the commercial and industrial energy storage market.

Geography Analysis

North America captured 36.5% of global installations in 2025, with the United States accounting for the lion's share after the standalone-storage Investment Tax Credit removed co-location requirements. California leads, exceeding 3 GW of commercial deployments by the end of 2025 under the Self-Generation Incentive Program that rebates up to USD 200 per kWh. Texas follows as ERCOT's energy-only market swings more than USD 0.20 per kWh during summer peaks, ideal for wholesale arbitrage. Canada's growth centers on Ontario and Alberta, where provincial incentives and microgrid needs intersect. Mexico remains nascent; lower tariffs and scarce financing limit adoption, though pilot projects are underway in Monterrey manufacturing zones. Asia-Pacific is the fastest-growing region, projected at a 23.3% CAGR through 2031. China's vertically integrated giants supply more than half of worldwide commercial shipments, keeping average system costs 20-30% below Western equivalents. India mandates two-hour storage for commercial solar above 500 kW, igniting activity in Gujarat and Maharashtra. Japan and South Korea prioritize resilience against natural disasters and supply-chain shocks, prompting corporate buyers like Toyota to install on-site batteries. ASEAN states advance unevenly, Thailand and Vietnam attract FDI-backed factories that embrace storage, but diesel subsidies in Indonesia slow progress. Australia and New Zealand deploy aggressively because high retail tariffs and prolific rooftop solar heighten self-consumption benefits.

Germany's industrial hubs deploy batteries to dodge curtailment fees when renewables drive spot prices negative more than 200 days each year. The United Kingdom's capacity-market auctions reward multi-hour assets, spurring supermarket chains and parcel depots to contract storage under twelve-year agreements. France, Spain, and Italy scale installations to integrate growing solar pipelines and comply with Fit-for-55 decarbonization targets. The Nordics pair wind with hydropower balancing, yet still adopt batteries for frequency support and grid congestion relief. Russia lags due to low tariffs and limited incentives; deployments are confined to remote mines and oil-and-gas outposts. In South America, the Middle East & Africa, Brazil, the UAE, and South Africa exhibit pilot activity in malls and telecom sites. Regional disparities notwithstanding, every continent now records commercial projects, underscoring the broad geographic spread of the commercial and industrial energy storage market.

- Tesla Inc.

- Fluence Energy

- LG Energy Solution

- BYD Co. Ltd.

- CATL

- Panasonic Holdings Corp.

- Saft (TotalEnergies)

- Samsung SDI

- Sungrow Power Supply

- Powin Energy

- Wartsila

- Eos Energy Enterprises

- ABB

- Schneider Electric

- Eaton

- Enphase Energy

- Hitachi Energy

- Generac Power Systems

- Kokam

- ESS Inc.

- EnerSys

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Li-ion cost curve approaching sub-$90/kWh

- 4.2.2 Global renewable mandates & corporate RE100 targets

- 4.2.3 Stand-alone storage ITC (US) & equivalent global incentives

- 4.2.4 Rising global C&I peak-demand charges

- 4.2.5 Hyperscale data-centre grid-deferral demand

- 4.2.6 Surge in synthetic PPAs needing dispatchable load-shifting

- 4.3 Market Restraints

- 4.3.1 High CAPEX vs diesel gensets

- 4.3.2 Critical-mineral supply-chain volatility

- 4.3.3 Fragmented interconnection & permitting rules

- 4.3.4 Urban fire-code compliance costs for indoor BESS

- 4.4 Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.6.1 Advances in Battery Chemistries

- 4.6.2 Role of AI & IoT in EMS/DERMS

- 4.6.3 Second-life Battery Applications

- 4.6.4 Emerging Hybrid & Long-Duration Systems

- 4.7 Porters Five Forces Analysis

- 4.7.1 Supplier Power

- 4.7.2 Buyer Power

- 4.7.3 Threat of Substitutes

- 4.7.4 Threat of New Entrants

- 4.7.5 Competitive Rivalry

- 4.8 Pricing Analysis

- 4.9 Impact of Macroeconomic & Geopolitical Factors

- 4.9.1 Supply-chain disruptions

- 4.9.2 Tariff & trade-policy shifts

- 4.9.3 Investment & interest-rate trends

5 Market Size & Growth Forecasts

- 5.1 By Technology

- 5.1.1 Lithium-ion (LFP, NMC/NCA, LCO)

- 5.1.2 Sodium-ion

- 5.1.3 Lead-acid (VRLA, Flooded)

- 5.1.4 Flow Batteries (Vanadium-Redox, Zinc-Bromine)

- 5.1.5 Hybrid Super-capacitor Systems

- 5.1.6 Other Emerging Chemistries (Solid-state, Metal-air)

- 5.2 By Application

- 5.2.1 Peak Shaving

- 5.2.2 Load Shifting

- 5.2.3 Backup Power/UPS

- 5.2.4 Renewable Integration

- 5.2.5 Ancillary Services (Frequency Regulation)

- 5.2.6 Demand-charge Management

- 5.2.7 EV Fast-charging Support

- 5.2.8 Microgrid Stabilisation

- 5.3 By End-user

- 5.3.1 Commercial Buildings (Retail, Offices)

- 5.3.2 Industrial Facilities (Manufacturing, Warehousing)

- 5.3.3 Data Centres

- 5.3.4 Educational Institutions

- 5.3.5 Healthcare Facilities

- 5.3.6 Telecom BTS and Edge Sites

- 5.3.7 EV-fleet Operators and Charging Hubs

- 5.3.8 Public Infrastructure (Airports, Rail)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 United Kingdom

- 5.4.2.2 Germany

- 5.4.2.3 France

- 5.4.2.4 Spain

- 5.4.2.5 Nordic Countries

- 5.4.2.6 Russia

- 5.4.2.7 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 India

- 5.4.3.3 Japan

- 5.4.3.4 South Korea

- 5.4.3.5 ASEAN Countries

- 5.4.3.6 Australia and New Zealand

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Colombia

- 5.4.4.4 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Egypt

- 5.4.5.5 Rest of Middle East and Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves (M&A, Partnerships, PPAs)

- 6.3 Market Share Analysis (Market Rank/Share for key companies)

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products & Services, and Recent Developments)

- 6.4.1 Tesla Inc.

- 6.4.2 Fluence Energy

- 6.4.3 LG Energy Solution

- 6.4.4 BYD Co. Ltd.

- 6.4.5 CATL

- 6.4.6 Panasonic Holdings Corp.

- 6.4.7 Saft (TotalEnergies)

- 6.4.8 Samsung SDI

- 6.4.9 Sungrow Power Supply

- 6.4.10 Powin Energy

- 6.4.11 Wartsila

- 6.4.12 Eos Energy Enterprises

- 6.4.13 ABB

- 6.4.14 Schneider Electric

- 6.4.15 Eaton

- 6.4.16 Enphase Energy

- 6.4.17 Hitachi Energy

- 6.4.18 Generac Power Systems

- 6.4.19 Kokam

- 6.4.20 ESS Inc.

- 6.4.21 EnerSys

7 Market Opportunities & Future Outlook

- 7.1 White-space & unmet-need assessment