|

시장보고서

상품코드

2063727

인사 정보 시스템(HRIS) 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Human Resource Information System (HRIS) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

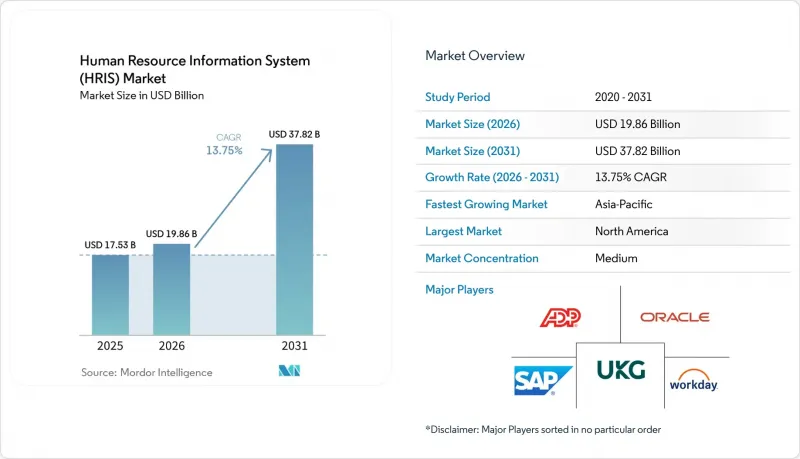

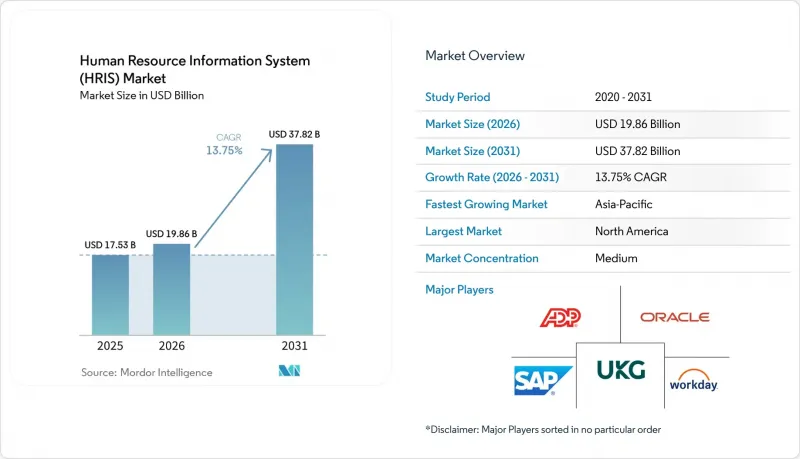

Mordor Intelligence에 의하면, 인사 정보 시스템(HRIS) 시장 규모는 2025년 175억 3,000만 달러에서 2026년에는 198억 6,000만 달러로 확대되어 2031년까지 378억 2,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 13.75%로 성장할 전망입니다.

본 보고서는 구성 요소(소프트웨어 및 서비스), 도입 모델(On-Premise 및 클라우드), 조직 규모(중소기업 및 대기업), 최종 사용자 산업 분야(IT 및 통신, 은행, 금융서비스 및 보험(BFSI), 헬스케어, 제조, 소매 및 전자상거래, 정부 기관 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 인사 정보 시스템(HRIS) 시장 동향과 인사이트

클라우드 기반 HR 플랫폼 도입 확대

조직들이 인프라 소유권을 외부에 위탁하고 전 세계 데이터를 실시간으로 통합함에 따라, 클라우드 구독 시장은 연평균 16.55%의 성장률을 기록하며 HRIS 시장 전체의 성장률을 상회하고 있습니다. 2025년에는 고용주의 69%가 적어도 하나의 핵심 모듈을 SaaS(Software-as-a-Service)로 전환할 것이며, 83%는 2027년까지 완전한 클라우드 도입을 예상하고 있습니다. 아시아태평양의 기업들은 데이터센터가 분산되어 있음에도 불구하고, 정부의 전자 신고 의무화와 저비용 광대역 환경의 지원에 힘입어 2026년까지 AI 기반 HR 도구를 도입할 의향이 70%에 달한다고 보고하고 있습니다. 이에 대해 각 벤더사는 ‘Workday GO’와 같은 중견 기업용 번들 제품으로 대응하고 있으며, 여기에는 미리 구축된 워크플로가 포함되어 있어 도입 기간을 9개월에서 4개월로 단축할 수 있습니다.

워크포스 애널리틱스에 대한 수요 증가

이직률 예측, 초과근무 시간 최적화, 인건비 모델링을 수행하는 예측 대시보드는 프리미엄 추가 기능에서 표준 기능으로 점차 전환되고 있습니다. 2026년에 AI 기반 HR 모듈을 도입할 예정인 조직들은 분석 기능에 평균 160만 달러를 예산으로 책정하고 있으며, 이는 2023년 대비 10배 증가한 수치입니다. 의료 업계에서는 그 성과가 두드러집니다. 400병상 규모의 병원에서 HRIS에 스케줄링 알고리즘을 도입한 결과, 간호사의 초과근무 시간을 18% 줄였습니다. 그러나 전사적인 AI 전문 지식을 갖춘 고용주는 9%에 불과하며, 로우코드 쿼리 도구와 자연어 인터페이스가 도입을 촉진하는 중요한 수단이 되고 있습니다.

멀티테넌트 클라우드에서의 데이터 보안 및 개인정보 보호

2024년, 임차인 간의 구분이 불충분했던 데 기인한 위반에 대해, GDPR(EU 개인정보보호규정)에 근거한 과징금이 29억 2,000만 유로(31억 1,000만 달러)로 급증했습니다. 아시아태평양의 데이터 현지화 법규로 인해 벤더들은 각국에 데이터센터를 구축할 수밖에 없게 되었으며, 퍼블릭 클라우드의 매력을 뒷받침하던 규모의 경제 효과가 약화되고 있습니다. 고객이 암호화 키를 관리하는 단일 테넌트형 옵션은 위험을 줄여주지만, 구독 요금을 최대 50%까지 끌어올리는 요인이 됩니다.

부문별 분석

서비스 매출은 2031년까지 연평균 16.21%의 성장률을 보일 것으로 예상되며, 통합, 변경 관리 및 관리형 운영에 대한 전문 지식을 필요로 하는 구매자들 수요에 힘입어 전체 인사정보시스템(HRIS) 시장의 성장률을 상회할 것으로 전망됩니다. 2025년에는 소프트웨어가 67.12%로 가장 큰 점유율을 유지했으나, 급여 계산 엔진의 상품화로 인해 그 가치는 분석, AI 및 사용자 경험 향상 쪽으로 이동하고 있습니다. 2024년 연구개발비 12억 7,000만 달러를 투입해 개발된 ADP의 기성 커넥터 덕분에 중견 기업의 도입 기간이 9개월에서 4개월로 단축되었으며, 구매자들이 속도를 중요시한다는 사실이 부각되었습니다. 시스템 소유자의 63%가 HR 기술 도입 경험이 3년 미만인 아시아태평양에서는 도입의 추진력을 유지하기 위해 교육 및 지원 계약이 다년 계약에 포함되어 있습니다.

컨설팅 예산은 코드 맞춤화보다 사용자 도입을 더 중시하는 경향이 강해지고 있으며, 이는 딜로이트의 조사 결과?참여도 점수 상위 25%에 속하는 기업에서는 변경 관리에 대한 지출이 40% 더 높다?를 반영하고 있습니다. 클라우드 구독 서비스에서는 호스팅, 패치 적용 및 1단계 지원이월이용료에 포함되어 있어, 기존의 ‘소프트웨어 대 서비스’라는 경계가 모호해지고 있습니다. 그럼에도 불구하고, 승인 절차나 복잡한 노동조합의 취업규칙을 맞춤 설정하는 기업들은 업그레이드 후 발생할 수 있는 문제를 방지하기 위해 여전히 종합적인 지원 서비스를 구매하고 있습니다.

2025년부터 2026년까지 클라우드 인스턴스는 16.55% 증가하며, 한때 인사 정보 시스템 시장의 71.05%를 차지했던 대규모 On-Premise 구축 기반을 서서히 잠식하고 있습니다. 중소기업들은 설비 투자(CAPEX)를 배제하고, 규정 준수 업데이트를 즉시 제공할 수 있는 구독형 번들 서비스로 눈을 돌리고 있습니다. 다국적 기업들은 국경을 넘어 공통된 직종 코드, 보상 범위, 평가 주기를 적용하기 위해 클라우드의 단일 인스턴스 아키텍처를 선호합니다. 그러나 유럽은행감독청(EBA)의 아웃소싱 지침에 따라, 많은 유럽 은행들은 클라우드 기반 인사 관련 애드온과 결합된 On-Premise 급여 계산 핵심 시스템을 유지해야 하는 상황에 놓여 있으며, 이로 인해 공급업체들이 지원을 중단하기 시작한 하이브리드 구성이 생겨나고 있습니다.

On-Premise 환경이 여전히 뿌리 깊게 남아 있는 배경에는 감사 시 지연 관리 및 업그레이드 시기가 있습니다. 그러나 딜로이트의 추산에 따르면, On-Premise형 HRIS에 필요한 IT 인력 수는 클라우드 기반의 2.5배에 달하며, 5년간의 총소유비용(TCO)은 호스팅형 옵션 쪽으로 결정적으로 기울어져 있습니다. 그 결과, 규제 대상인 많은 구매 기업들은 사내 데이터센터에 무기한으로 매달리기보다는 소버린 클라우드의 적용 제외 조항에 대해 협상을 진행하고 있습니다.

지역별 분석

북미는 포춘 500대 기업의 조기 도입과 급여 계산 대행업체로 구성된 탄탄한 생태계 덕분에 2025년 매출의 38.02%를 차지했습니다. 현재 성장은 직원 수 500-2,500명의 중견 기업에 집중되어 있으며, 이러한 기업들은 그동안 외부에 위탁한 급여 계산이나 스프레드시트에 의존해 왔습니다. 2025년 11월에 도입된 ‘Workday GO’는 표준화된 워크플로를 패키지화하여 6주 이내에 도입할 수 있도록 함으로써 이러한 요구에 부응하고 있습니다. 캘리포니아주의 급여 투명성 규제로부터 콜로라도주의 채용 공고 게시 의무에 이르기까지 규정 준수가 점점 더 복잡해짐에 따라, 구매자들은 하드코딩된 로직이 아닌 설정 가능한 규칙 엔진을 요구하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있으며, 연평균 성장률(CAGR) 15.34%를 나타낼 것으로 예측되어 2031년까지 인사 정보 시스템 시장에서 이 지역의 점유율을 끌어올릴 것으로 보입니다. 인도는 ‘비약적인 효과’의 대표적인 사례입니다. 중소기업의 3분의 2는 디지털화에 대한 준비가 되어 있는 것으로 나타났으나, 그 대다수는 급여 계산과 근태 관리에만 시스템 도입을 한정하고 있어, 공급업체의 인식 제고 활동의 필요성이 부각되고 있습니다. 중국에서 사회보험 전자신고 의무화가 시행됨에 따라, 제조업체들은 클라우드로의 전환을 강요받고 있습니다. 한편, 일본과 한국은 On-Premise에서 주권 클라우드 모델로 신중하게 전환하고 있습니다. 호주 및 뉴질랜드는 북미와 비슷한 수준 시장 포화 상태를 보이고 있지만, 페어워크 위원회(Fair Work Commission)의 규정 준수를 보장할 수 있는 공급업체에게는 여전히 성장의 목표 시장이 되고 있습니다.

유럽의 동향은 GDPR(EU 개인정보보호규정) 및 EU AI법의 적극적인 시행으로 특징지어집니다. 2023년부터 2024년까지 벌금이 9배로 급증하면서, 기업들은 동의 관리 대시보드 및 알고리즘 로직의 문서화에 대한 투자를 서둘러야 하는 상황에 처해 있습니다. 2025년 11월 워크데이가 프랑크푸르트와 더블린의 데이터센터에 대해 실시한 1억 7,500만 유로(1억 8,600만 달러) 규모의 확장은 EU 내 데이터 보관을 요구하는 고객들의 요구에 부응하기 위한 것입니다. 남유럽 시장인 스페인, 이탈리아, 그리스는 여전히 분산된 상태이며, 현지 급여 계산 아웃소싱 업체들이 클라우드 신생 기업들에 맞서 시장 점유율을 사수하려 하고 있습니다. 남미, 중동 및 아프리카는 시장 점유율이 작긴 하지만, 각국 정부가 근로자 등록부의 디지털화를 추진하고 다국적 기업들이 전 세계 인사 플랫폼의 표준화를 추진하는 가운데 두 자릿수 성장을 기록하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.23According to Mordor Intelligence, the human resource information system (HRIS) market size is expected to increase from USD 17.53 billion in 2025 to USD 19.86 billion in 2026 and reach USD 37.82 billion by 2031, growing at a CAGR of 13.75% over 2026-2031.

This report is Segmented by Component (Software, and Services), Deployment Model (On-Premise, and Cloud), Organization Size (Small and Medium Enterprises, and Large Enterprises), End-User Industry (IT and Telecom, BFSI, Healthcare, Manufacturing, Retail and E-Commerce, Government, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Human Resource Information System (HRIS) Market Trends and Insights

Growing Adoption of Cloud-Based HR Platforms

Cloud subscriptions are growing 16.55% annually, outpacing overall human resource information system market expansion as organizations offload infrastructure ownership and gain real-time global data consolidation. In 2025, 69% of employers had moved at least one core module to software-as-a-service and 83% expect full cloud adoption by 2027. Asia-Pacific enterprises, despite fragmented data centers, report 70% intent to deploy AI-enabled HR tools by 2026, stimulated by government e-filing mandates and low-cost broadband. Vendors are responding with mid-market bundles such as Workday GO, which ships pre-built workflows that cut launch times from nine months to four.

Rising Demand for Workforce Analytics

Predictive dashboards that forecast attrition, optimize overtime, and model labor costs are shifting from premium add-ons to baseline expectations. Organizations deploying AI-driven HR modules in 2026 budgeted an average of USD 1.6 million for analytics, a tenfold rise since 2023. Healthcare illustrates results: a 400-bed hospital cut nurse overtime by 18% after embedding scheduling algorithms into its HRIS. Yet only 9% of employers possess enterprise-wide AI expertise, making low-code query tools and natural-language interfaces critical adoption levers.

Data Security and Privacy in Multi-Tenant Clouds

GDPR fines surged to EUR 2.92 billion (USD 3.11 billion) in 2024 for breaches linked to inadequate tenant segregation. Asia-Pacific data-localization laws compel vendors to spin up national data centers, diluting the economies of scale that make public clouds attractive. Single-tenant options with customer-managed encryption keys mitigate risk but lift subscription fees by as much as 50%.

Other drivers and restraints analyzed in the detailed report include:

- Expansion of Remote and Hybrid Work Models

- Integration of AI-Powered Chatbots for Employee Self-Service

- High Switching Costs From Legacy Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Services revenue is projected to rise 16.21% a year through 2031, surpassing overall human resource information system (HRIS) market growth as buyers seek integration, change-management, and managed-perations expertise. Software retained the largest slice 67.12% in 2025, yet commoditization of payroll engines is shifting value toward analytics, AI, and user experience enhancements. Pre-built connectors from ADP, funded by USD 1.27 billion in 2024 research spending, have compressed mid-market rollouts from nine months to four, highlighting the premium buyers place on speed. In Asia-Pacific, where 63% of system owners have fewer than three years of HR-tech experience, training and support contracts are bundled into multiyear deals to sustain adoption momentum.

Consulting budgets increasingly emphasize user adoption rather than code customization, reflecting Deloitte findings that top-quartile engagement scores correlate with 40% higher spend on change management. Cloud subscriptions blur the classic software-versus-services line because hosting, patches, and tier-one support are baked into monthly fees. Nevertheless, enterprises customizing approval chains or complex union work rules still purchase white-glove services to guard against post-upgrade breakage.

Cloud instances grew 16.55% in 2025-2026, chipping away at the sizable on-premise installed base that once held 71.05% of the human resource information system market. Small and medium enterprises gravitate to subscription bundles that eliminate capex and deliver immediate compliance updates. Multinationals favor cloud single-instance architectures to enforce common job codes, compensation bands, and review cycles across borders. The European Banking Authority's outsourcing guidelines, however, push many continental banks to retain on-premise payroll cores paired with cloud talent add-ons, creating hybrid topologies that vendors are starting to de-support.

On-premise persistence stems from audit latency control and upgrade timing. Yet Deloitte pegs IT staffing needs for on-premise HRIS at 2.5 X those of cloud, making total cost of ownership tilt decisively toward hosted options over a five-year horizon. As a result, many regulated buyers are negotiating sovereign-cloud carve-outs rather than sticking indefinitely to in-house data centers.

Geography Analysis

North America secured 38.02% of 2025 revenue thanks to early Fortune 500 adoption and a dense ecosystem of payroll bureaus. Growth now concentrates in mid-market firms of 500-2,500 staff that historically relied on outsourced payroll and spreadsheets. Workday GO, introduced in November 2025, speaks to this gap by bundling standardized workflows into packages that implement in under six weeks. Compliance complexity, from California pay-transparency to Colorado job-posting mandates, nudges buyers toward configurable rule engines rather than hard-coded logic.

Asia-Pacific is the fastest climber, with a projected 15.34% CAGR that will lift its slice of the human resource information system market by 2031. India typifies the leapfrog effect: two-thirds of SMEs show digital readiness, yet the vast majority limit purchases to payroll and attendance, underscoring the need for vendor education. China's electronic social-insurance filing requirement is pulling manufacturers into the cloud, while Japan and South Korea tiptoe away from on-premise toward sovereign-cloud models. Australia and New Zealand exhibit North American-style saturation but remain growth targets for vendors that can guarantee Fair Work Commission compliance.

Europe's trajectory is defined by aggressive enforcement of GDPR and the EU AI Act. Fines ballooned nine-fold between 2023 and 2024, prompting companies to invest in consent-management dashboards and documentation of algorithmic logic. Workday's EUR 175 million (USD 186 million) expansion of Frankfurt and Dublin data centers in November 2025 addresses customers that demand EU-based residency. Southern markets, Spain, Italy, and Greece, remain fragmented, with local payroll outsourcers defending share against cloud newcomers. South America, the Middle East and Africa contribute smaller slices but post double-digit growth as governments digitize labor registries and multinationals standardize global HR platforms.

- Workday, Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Paycom Software, Inc.

- Paychex, Inc.

- Ceridian HCM Holding Inc.

- Cornerstone OnDemand, Inc.

- BambooHR LLC

- Gusto, Inc.

- Zoho Corporation Pvt. Ltd.

- Namely, Inc.

- SumTotal Systems, LLC

- Cegid Group SA

- TriNet Zenefits LLC

- PeopleStrategy, Inc.

- isolved HCM LLC

- Rippling People Center Inc.

- Deputy Group Pty Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Adoption of Cloud-Based HR Platforms

- 4.2.2 Rising Demand for Workforce Analytics and Data-Driven Decision Making

- 4.2.3 Increasing Regulatory Complexity Around Workforce Compliance

- 4.2.4 Expansion of Remote and Hybrid Work Models

- 4.2.5 Integration of AI-Powered Chatbots for Employee Self-Service

- 4.2.6 Emergence of Industry-Specific HRIS Verticals

- 4.3 Market Restraints

- 4.3.1 High Switching Costs From Legacy HR Systems

- 4.3.2 Data Security and Privacy Concerns in Multi-Tenant Architectures

- 4.3.3 Shortage of Skilled HR Tech Administrators

- 4.3.4 Limited Budgets Among Small Enterprises in Emerging Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Model

- 5.2.1 On-Premise

- 5.2.2 Cloud

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 Banking, Financial Services and Insurance (BFSI)

- 5.4.3 Healthcare

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-Commerce

- 5.4.6 Government

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Paycom Software, Inc.

- 6.4.7 Paychex, Inc.

- 6.4.8 Ceridian HCM Holding Inc.

- 6.4.9 Cornerstone OnDemand, Inc.

- 6.4.10 BambooHR LLC

- 6.4.11 Gusto, Inc.

- 6.4.12 Zoho Corporation Pvt. Ltd.

- 6.4.13 Namely, Inc.

- 6.4.14 SumTotal Systems, LLC

- 6.4.15 Cegid Group SA

- 6.4.16 TriNet Zenefits LLC

- 6.4.17 PeopleStrategy, Inc.

- 6.4.18 isolved HCM LLC

- 6.4.19 Rippling People Center Inc.

- 6.4.20 Deputy Group Pty Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment