|

시장보고서

상품코드

2073311

OKR 및 목표 관리 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)OKR and Goal Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

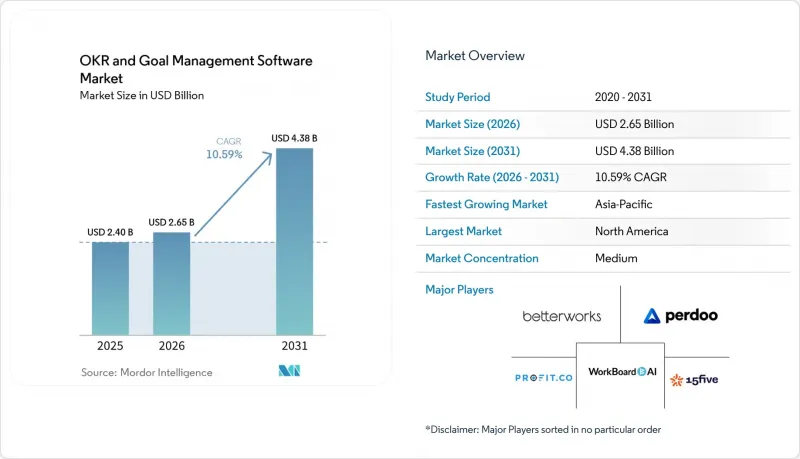

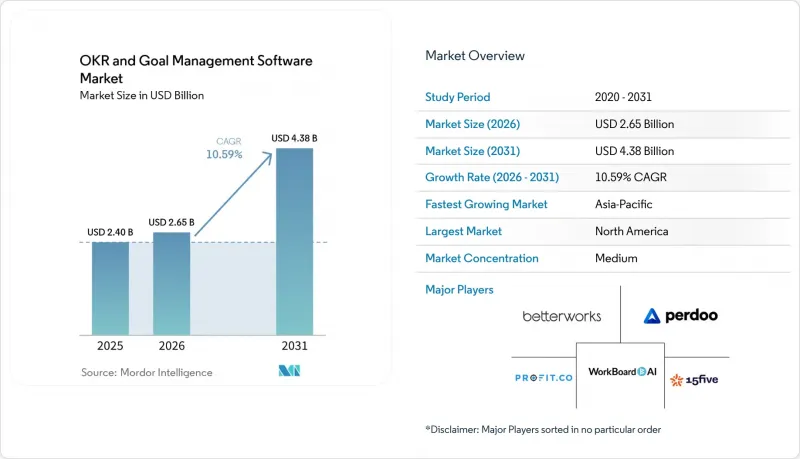

Mordor Intelligence에 의하면, OKR 및 목표 관리 소프트웨어 시장 규모는 2025년 24억 달러로 평가되었습니다. 2026년에는 26억 5,000만 달러로 확대되어 2031년까지 43억 8,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 10.59%로 성장할 전망입니다.

본 보고서는 기능별(추적·가시화, 연계·협업, 성과 분석 등), 배포 유형별(클라우드 기반, On-Premise형), 조직 규모별(중소기업, 대기업), 업종별(IT 및 통신 등) 및 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 OKR 및 목표 관리 소프트웨어 시장 동향 및 인사이트

애자일 및 원격 근무 문화의 확산

북미와 유럽에서는 하이브리드 근무의 보급률이 60%를 넘어섰으며, 연간 목표 주기의 한계가 드러나고 있습니다. 마이크로소프트는 2025년, Ally.io의 목표 및 핵심 성과(OKR) 추적 기능을 Teams에 통합하여 직원들이 일상적인 협업 허브 내에서 목표를 확인할 수 있도록 함으로써, 이 기능의 대규모 활용을 가속화했습니다. 이어 WorkBoard는 자사 플랫폼을 Microsoft Copilot과 연동하여, 사용자가 자연어로 진행 상황을 조회할 수 있도록 했습니다. 이로써 큰 마찰 요인이 해소되었습니다. Betterworks는 2026년, 체크인을 자동화하는 400개 이상의 AI 워크플로를 추가한 ‘ NextGen"를 발표하여 이에 대응했습니다. 이러한 움직임은 전반적으로 분산형 팀이 비동기적인 가시성과 지속적인 협업을 추구하고 있음을 보여주며, OKR 및 목표 관리 소프트웨어 시장의 중기적 성장을 뒷받침하고 있습니다.

실시간 성과 시각화에 대한 수요 증가

경영진은 분기 단위로 지연되는 대시보드를 더 이상 용납하지 않게 되었습니다. 2026년 5월에 출시된 Betterworks의 “AI-Powered Talent Intelligence"는 주요 성과에 대한 진행 상황과 역량 격차를 연계하여, 목표 미달이 발생하기 전에 경영진에게 경고를 보냅니다. API 우선 아키텍처를 통해 CRM, 프로젝트 관리, 재무 시스템에서 데이터를 직접 스트리밍함으로써 지연을 더욱 단축하고 있습니다. 2026년 4월 330만 달러 규모의 자금 조달을 막 완료한 스타트업 브레브(Brev)는 Slack 스레드, Jira 티켓, 회의록에서 주요 성과를 자동으로 업데이트하여, 기업의 90%에서 걸림돌이 되고 있는 수동 입력의 필요성을 없애고 있습니다. 따라서 실시간 인사이트는 특히 경쟁 주기가 급속히 단축되고 있는 기술 주도형 산업에서 단기적인 성장의 촉매제가 됩니다.

클라우드 도입에 따른 데이터 보안 및 개인정보 보호에 대한 우려

GDPR(EU 개인정보보호규정), PIPL, 업계별 규제 등 엄격한 규제 체계로 인해 많은 구매자들이 On-Premise 환경을 유지하고 있습니다. Perdoo는 인프라를 아일랜드에 구축하고 있으며, Weekdone은 에스토니아에서 호스팅 서비스를 제공하고, Profit.co는 금융 및 의료 업계 고객을 대상으로 지역별 클라우드 서비스 외에도 On-Premise 버전도 제공합니다. 그러나 플랫폼이 늘어날수록 감사 대상 범위가 확대되면서 IT 부서의 거부감도 커지고 있습니다. 2024년부터 2025년에 걸쳐 발생한 주목할 만한 정보 유출 사건들이 이러한 우려를 현실로 만들었기 때문에 보안 문제는 OKR 및 목표 관리 소프트웨어 시장에서 클라우드 전환을 가로막는 단기적인 걸림돌로 계속 작용하고 있습니다.

부문별 분석

2025년에는 “추적 및 가시화"가 OKR 및 목표 관리 소프트웨어 시장 규모를 견인했으나, “통합 및 자동화"는 2031년까지 연평균 성장률(CAGR) 12.01%를 나타낼 것으로 예측됩니다. 이러한 변화는 시간을 낭비하고 데이터의 일관성을 해치는 수동 업데이트를 줄이고자 하는 고객의 요구를 반영한 것입니다. Brev의 AI 에이전트는 Slack, Jira, Salesforce에서 주요 성과 데이터를 자동으로 업데이트합니다. 이러한 기술 혁신을 통해 직원 500명을 둔 기업은 연간 최대 200만 달러의 비용을 절감할 수 있게 됩니다. 경영진은 여전히 진행 상황을 명확하게 시각화할 것을 요구하고 있기 때문에 대시보드는 계속 사용되고 있지만, 현재는 독립형 모듈로 판매되는 것이 아니라 통합 레이어에 통합되어 있습니다.

성과 분석은 목표와 업무상의 촉발 요인을 연결하는 가교 역할을 하며 그 중요성이 부각되고 있습니다. Betterworks는 지연이 실패로 이어지기 전에 예측 플래그를 통해 관리자에게 주의를 환기시킵니다. 하이브리드 팀이 비동기적인 조정이 필요한 상황에서 협업 및 조정 도구는 꾸준히 성장하고 있습니다. 반면, 규제 대상 산업에서는 감사 추적을 위해 보고서 및 인사이트 기능이 여전히 필수적입니다. 게이미피케이션과 같은 틈새 기능은 참여도를 중시하는 구매자들을 끌어들이지만, 수익은 그리 크지 않습니다. 그 결과, 기능 세트는 엔드투엔드 실행을 중심으로 통합되는 추세이며, OKR 및 목표 관리 소프트웨어 시장에서 주요 구매 동기는 통합 기능으로 나타나고 있습니다.

2025년 기준으로 On-Premise형 도입은 OKR 및 목표 관리 소프트웨어 시장 점유율의 67.41%를 차지했으나, 클라우드 기반 솔루션은 연평균 성장률(CAGR) 12.89%로 성장하고 있습니다. 규정 준수가 On-Premise 도입의 주요 결정 요인으로 작용하고 있습니다. 예를 들어, 독일의 은행들은 BaFin이 현지 호스팅을 권장하는 지침을 근거로 들고 있습니다. 각 벤더사는 하이브리드형 제어 기능을 제공함으로써 이에 대응하고 있습니다. Profit.co는 미국 연방 정부 수요를 개척하기 위해 FedRAMP Ready 인증을 획득했으며, Quantive는 기업이 데이터를 격리하기 위해 AWS 리전을 선택할 수 있도록 지원하고 있습니다. 그럼에도 불구하고, 중소기업들은 SaaS가 설비 투자(Capex)를 줄이고, 도입을 신속하게 하며, 자동 업그레이드를 보장하기 때문에 SaaS를 선호하고 있습니다.

앞으로는 인프라의 광범위한 현대화를 통해 균형이 변화해 나갈 것입니다. 마이크로소프트가 Ally.io를 Viva Goals에 통합함에 따라, 수백만 명의 Teams 사용자가 네이티브 클라우드 OKR을 이용할 수 있게 되었으며, 원격 호스팅이 점차 보편화되고 있습니다. 그렇긴 하지만, 규제 당국이 지침을 세분화하고 기존 기업들이 전환 로드맵을 완료해 나감에 따라 클라우드의 성장은 점차 가속화될 것입니다. 따라서 OKR 및 목표 관리 소프트웨어 시장에서는 적어도 2031년까지는 두 모델이 공존할 것으로 보입니다.

지역별 분석

북미는 2025년에 37.34%의 점유율을 유지했습니다. 이는 2026년 미국의 소프트웨어 지출이 15.2% 증가할 것으로 전망된다는 점에 근거한 것입니다. 업계의 통합이 진행되고 있음이 분명합니다. 마이크로소프트가 Ally.io를 흡수하고, WorkBoard가 Quantive를 인수한 것은 급속한 사용자 확보보다 제품군 간의 시너지를 우선시하는 성숙 단계에 접어들었음을 보여줍니다. 캐나다와 멕시코에서는 지역 부문이 보고의 표준화를 도모하기 위해 미국의 플랫폼과 연계하려는 움직임이 나타나고 있으며, 이에 따라 틈새 수요가 발생하고 있습니다.

아시아태평양은 2026년부터 2031년에 걸쳐 연평균 성장률(CAGR) 12.45%를 기록하며 가장 빠른 성장세를 보이고 있습니다. 중국 중견·대기업을 대상으로 한 78.3%의 보급률은 국가 주도의 디지털화를 여실히 보여주고 있지만, 데이터 현지화 규제로 인해 국내 공급업체들이 우대받고 있습니다. 인도의 아웃소싱 거점은 전 세계 고객과의 결과물 일관성을 유지하기 위해 OKR에 의존하고 있는 반면, 일본의 거버넌스 개혁은 성과 프레임워크와 조화를 이루는 투명성을 촉진하고 있습니다. 동남아시아 국가들에서는 지역 내 유니콘 기업들이 OKR 스위트를 조기에 도입함에 따라 급속히 추격세를 보이고 있습니다.

유럽은 중간 정도 시장 점유율을 차지하고 있으며, 독일, 영국, 프랑스가 주도적인 역할을 하고 있습니다. GDPR(EU 개인정보보호규정)에 따라 EU 지역 내에서 호스팅되는 클라우드에 대한 수요가 증가하고 있으며, Weekdone은 에스토니아에서 Perdoo는 아일랜드에서 사업을 전개하고 있습니다. 각국마다 다른 규제로 인해 규정 준수 비용이 증가하면서, 여러 국가에서의 사업 확장이 주춤하고 있습니다. 남미 시장은 규모가 작습니다. 브라질과 아르헨티나가 주도적인 입장에 있지만, 통화 변동과 현지화의 한계에 직면해 있습니다. 중동 및 아프리카에서의 도입은 디지털 경제 로드맵과 다국어 플랫폼의 확대에 힘입어 낮은 수준에서 점차 확대되고 있습니다. 그러나 언어의 장벽과 대역폭의 제약이 여전히 OKR 및 목표 관리 소프트웨어 시장의 추가적인 확산을 저해하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the OKR and goal management software market size is expected to increase from USD 2.40 billion in 2025 to USD 2.65 billion in 2026 and reach USD 4.38 billion by 2031, growing at a CAGR of 10.59% over 2026-2031.

This report is Segmented by Functionality (Tracking and Visualization, Alignment and Collaboration, Performance Analytics, and More), Deployment Type (Cloud-Based, and On-Premises), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (IT and Telecommunications, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global OKR and Goal Management Software Market Trends and Insights

Rising Adoption of Agile and Remote Work Cultures

Hybrid work now exceeds 60% penetration in North America and Europe, exposing the limits of annual goal cycles. Microsoft embedded Ally.io's Objectives and Key Results (OKR) tracker into Teams in 2025, allowing staff to review objectives inside their everyday collaboration hub and accelerating usage at scale. WorkBoard followed by wiring its platform to Microsoft Copilot, letting users query progress in natural language, which removes a major friction point. Betterworks responded in 2026 with a NextGen release that adds more than 400 AI workflows to automate check-ins. Collectively, these moves prove that distributed teams demand asynchronous visibility and continuous alignment, fuelling medium-term growth for the OKR and goal management software market.

Increasing Need for Real-Time Performance Visibility

Boardrooms no longer accept quarter-lag dashboards. Betterworks' AI-Powered Talent Intelligence, launched in May 2026, correlates key-result health with skill gaps, alerting leaders before misses occur.API-first architectures further shorten latency by streaming data directly from CRM, project-management and finance systems. Start-up Brev, fresh from a USD 3.3 million raise in April 2026, auto-updates key results from Slack threads, Jira tickets and meeting transcripts, eliminating the manual entry that derails 90% of enterprises. Real-time insight is therefore a short-term catalyst, especially in tech-driven verticals where competitive cycles compress quickly.

Data Security and Privacy Concerns in Cloud Deployments

Strict regimes such as GDPR, PIPL and sector-specific rules keep many buyers on-premises. Perdoo places infrastructure in Ireland, Weekdone hosts in Estonia and Profit.co offers regional clouds plus on-premises editions for finance and healthcare clients. Yet each extra platform expands the audit surface, deepening IT resistance. High-profile breaches during 2024-2025 crystallized these fears, so security remains a short-term drag on cloud conversion inside the OKR and goal management software market.

Other drivers and restraints analyzed in the detailed report include:

- Growing Investments in Digital Transformation Initiatives

- Integration of OKR Tools With Existing Enterprise Software Ecosystems

- Resistance to Cultural Change in Traditional Enterprises

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Tracking and Visualization led the OKR and goal management software market size in 2025, but Integrations and Automation is expected to record a 12.01% CAGR through 2031. The pivot reflects customer demand to cut manual updates that waste hours and skew data integrity. Brev's AI agents refresh key results from Slack, Jira and Salesforce, an advance that could save a 500-person firm up to USD 2 million annually. Executives still want clear progress visuals, so dashboards persist, yet they are now embedded within integration layers rather than sold as standalone modules.

Performance Analytics has emerged as the bridge between goals and operational triggers; Betterworks uses predictive flags to prompt managers before slippage turns into failure. Alignment and Collaboration tools grow steadily as hybrid teams need asynchronous coordination, while Reporting and Insights remain vital in regulated industries for audit trails. Niche features such as gamification attract engagement-oriented buyers but hold modest revenue. The net result is a feature stack converging around end-to-end execution, with integrations as the primary purchase driver for the OKR and goal management software market.

On-Premises installations owned 67.41% of OKR and goal management software market share in 2025, yet Cloud-Based solutions are expanding at a 12.89% CAGR. Compliance dictates many on-premises decisions; German banks, for example, cite BaFin guidance that prefers local hosting. Vendors are reacting with hybrid controls. Profit.co achieved FedRAMP Ready status to unlock U.S. federal demand, and Quantive lets enterprises choose AWS regions to isolate data. Nonetheless, SMEs gravitate to SaaS because it cuts capex, speeds deployment and ensures automatic upgrades.

Over time, broader infrastructure modernisation will tilt the balance. Microsoft's embedding of Ally.io into Viva Goals exposes millions of Teams users to native cloud OKRs, normalising remote hosting. Still, cloud growth will play out gradually as regulators refine guidelines and incumbents complete migration roadmaps. The coexistence of both models is therefore assured through at least 2031 inside the OKR and goal management software market.

Complete Report Scope:

- By Functionality

- Tracking and Visualization

- Alignment and Collaboration

- Performance Analytics

- Integrations and Automation

- Reporting and Insights

- Other Functionalities

- By Deployment Type

- Cloud-Based

- On-Premises

- By Organization Size

- Small and Medium Enterprises (SMEs)

- Large Enterprises

- By Industry Vertical

- IT and Telecommunications

- BFSI

- Healthcare and Life Sciences

- Manufacturing

- Retail and eCommerce

- Other Industry Verticals

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- South Korea

- Australia and New Zealand

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America retained 37.34% share in 2025, buoyed by the United States' software spending growth forecast of 15.2% for 2026. Consolidation is evident: Microsoft absorbed Ally.io, and WorkBoard bought Quantive, signalling a maturity phase that prioritises cross-suite synergies over rapid user acquisition. Canada and Mexico add niche demand as regional divisions align with U.S. platforms to standardise reporting.

Asia-Pacific enjoys the fastest expansion at a 12.45% CAGR over 2026-2031. China's 78.3% penetration in mid-to-large enterprises exemplifies state-supported digitalisation, though data-localisation rules favour domestic vendors. India's outsourcing hubs rely on OKRs to keep deliverables aligned with global clients, while Japan's governance reforms promote transparency that resonates with outcome frameworks. Southeast Asian economies are catching up as regional unicorns adopt OKR suites early.

Europe contributes mid-tier share, with Germany, the United Kingdom and France leading. GDPR drives demand for EU-hosted clouds, prompting Weekdone to operate from Estonia and Perdoo from Ireland. Divergent national rules raise compliance costs, slowing multi-country rollouts. South America is modest; Brazil and Argentina dominate but face currency volatility and limited localisation. Adoption in the Middle East and Africa grows from a small base, fueled by digital-economy roadmaps and multilingual platform expansions, yet language gaps and bandwidth constraints still hinder broader penetration of the OKR and goal management software market.

- WorkBoard Inc.

- Quantive Technologies Inc.

- Betterworks Systems Inc.

- 15Five Inc.

- Perdoo GmbH

- Profit.co Inc.

- Weekdone OU

- Ally Technologies Inc.

- Koan Inc.

- Atiim Inc.

- Peoplebox Inc.

- Engagedly Inc.

- Fitbots OKRs Consulting and Software Private Limited

- Elate Inc.

- Mooncamp Software GmbH

- Zokri Limited

- Cascade Strategy Pty Ltd

- Huminos Technologies Private Limited

- Rhythm Systems Inc.

- Corvisio LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Adoption of Agile and Remote Work Cultures

- 4.2.2 Increasing Need for Real-Time Performance Visibility

- 4.2.3 Growing Investments in Digital Transformation Initiatives

- 4.2.4 Integration of OKR (Objectives and Key Results) Tools with Existing Enterprise Software Ecosystems

- 4.2.5 Expansion of Outcome-Based Contracting in Professional Services

- 4.2.6 Surge in Venture-Funded Startups Standardizing OKRs Pre-Series B

- 4.3 Market Restraints

- 4.3.1 Data Security and Privacy Concerns in Cloud Deployments

- 4.3.2 Resistance to Cultural Change in Traditional Enterprises

- 4.3.3 Overlapping Functionality with Existing Performance Management Suites Leading to Tool Fatigue

- 4.3.4 Limited Local Language Support Hindering Adoption in Non-English-Speaking Markets

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Functionality

- 5.1.1 Tracking and Visualization

- 5.1.2 Alignment and Collaboration

- 5.1.3 Performance Analytics

- 5.1.4 Integrations and Automation

- 5.1.5 Reporting and Insights

- 5.1.6 Other Functionalities

- 5.2 By Deployment Type

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.3 By Organization Size

- 5.3.1 Small and Medium Enterprises (SMEs)

- 5.3.2 Large Enterprises

- 5.4 By Industry Vertical

- 5.4.1 IT and Telecommunications

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Manufacturing

- 5.4.5 Retail and eCommerce

- 5.4.6 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 WorkBoard Inc.

- 6.4.2 Quantive Technologies Inc.

- 6.4.3 Betterworks Systems Inc.

- 6.4.4 15Five Inc.

- 6.4.5 Perdoo GmbH

- 6.4.6 Profit.co Inc.

- 6.4.7 Weekdone OU

- 6.4.8 Ally Technologies Inc.

- 6.4.9 Koan Inc.

- 6.4.10 Atiim Inc.

- 6.4.11 Peoplebox Inc.

- 6.4.12 Engagedly Inc.

- 6.4.13 Fitbots OKRs Consulting and Software Private Limited

- 6.4.14 Elate Inc.

- 6.4.15 Mooncamp Software GmbH

- 6.4.16 Zokri Limited

- 6.4.17 Cascade Strategy Pty Ltd

- 6.4.18 Huminos Technologies Private Limited

- 6.4.19 Rhythm Systems Inc.

- 6.4.20 Corvisio LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment