|

시장보고서

상품코드

2073313

결근 관리 소프트웨어 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Absence Management Software - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

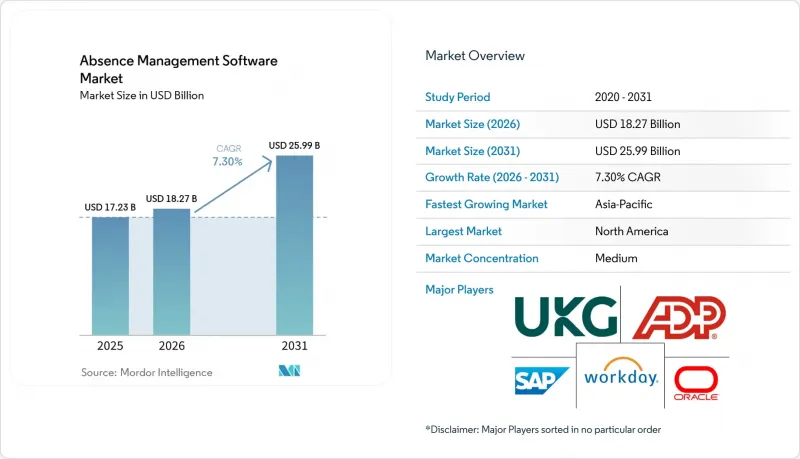

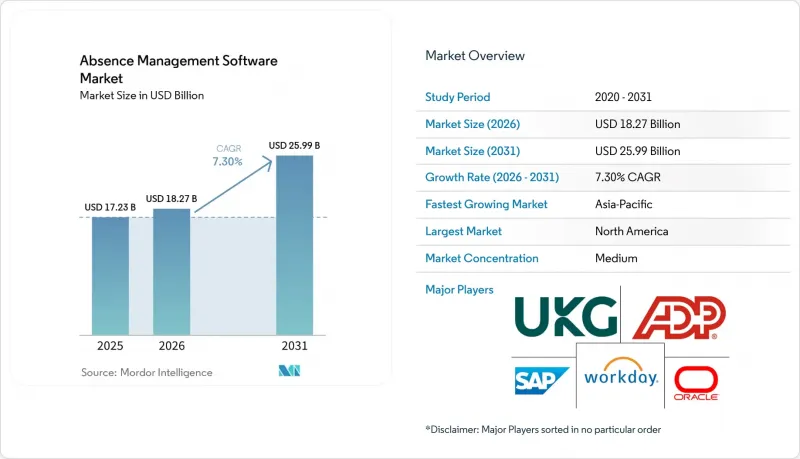

Mordor Intelligence에 의하면, 결근 관리 소프트웨어 시장은 2025년에 172억 3,000만 달러로 평가되었습니다. 2026년에는 182억 7,000만 달러로 확대되어 2031년까지 259억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 7.30%로 성장할 전망입니다.

본 보고서는 배포 방식(소프트웨어 및 서비스), 배포 방식(클라우드 기반, 하이브리드형 등), 최종 사용자의 기업 규모(대기업 및 중소기업), 용도(휴가 관리, 규정 준수 관리 등), 최종 사용자 산업(정보 기술 및 통신 등), 지역별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

세계의 결근 관리 소프트웨어 시장 동향 및 인사이트

여러 관할 구역에 걸친 휴가 및 노동 규정 준수 요건의 강화

관리 소프트웨어가 없는 상황에서 여러 관할 구역에 걸쳐 적용되는 휴가 규정은 인사 부서에게는 단순한 번거로움에 그치던 것이, 고용주에게는 핵심적인 운영상의 과제로 변모하고 있습니다. 2026년에는 델라웨어주, 메인주, 미네소타주, 콜로라도주 및 뉴욕시가 대규모 유급 휴가 제도를 도입하거나 기존의 휴가 권리를 확대했습니다. 이로써 이미 의무적인 PFML(가족·의료 휴가) 제도를 도입한 주와 워싱턴 D.C.를 합쳐 총 15개 관할 구역이 되었습니다. 적용되는 규정은 일반적으로 고용주가 법인을 설립한 주가 아니라, 직원의 실제 근무지를 기준으로 결정됩니다. 즉, 새로운 주에서 원격 근무 직원을 1명 채용할 때마다 새로운 규정 준수 요건이 발생할 가능성이 있습니다. 또한, 고용주는 ADA(미국 장애인법), PWFA(유급 가족 휴가법) 및 각 주의 PFML(유급 가족 의료 휴가)에 관한 의무를 병행하여 관리해야 하며, 이러한 요소들이 결합됨에 따라 스프레드시트를 이용한 워크플로우로는 일관되게 처리할 수 없는 문서화, 증명, 통지 절차가 발생합니다. 관리 소프트웨어 시장이 아직 성숙하지 않은 상황에서 근무지별로 휴가 규정을 자동으로 업데이트할 수 있는 공급업체는 제품 측면에서 뚜렷한 우위를 점할 수 있습니다. 왜냐하면 구매자들은 범용적인 워크플로의 포괄성보다 정확성과 속도를 점점 더 중요하게 여기고 있기 때문입니다.

클라우드 기반 인사 관리 소프트웨어 도입

클라우드 도입은 단순한 비용 측면의 판단에서 기능 측면의 판단으로 진화하고 있으며, 이러한 변화가 결근 관리 소프트웨어 시장의 확대로 이어지고 있습니다. ISG의 2025년 HR 기술 조사에 따르면, 69%의 조직이 이미 SaaS 또는 하이브리드 클라우드 기반 인사 모델을 도입하고 있으며, 83%는 2027년 말까지 도입할 것으로 나타났습니다. 이 조사에 따르면, 2026년 인사 AI 예산의 평균이 160만 달러로 증가할 것으로 나타났으며, 클라우드 플랫폼이 현재 분석, 자동화 및 AI를 활용한 워크플로우 도구의 표준 기반이 되고 있음을 알 수 있습니다. 주요 HCM 벤더들도 보다 광범위한 제품군에 기본 제공되는 결근 관리 기능을 통합하고 있으며, 이에 따라 기업들은 통합, 보고서 작성 및 워크플로우의 연속성에 대한 기대가 높아지고 있습니다. 이러한 움직임에 따라, 결근 관리 소프트웨어 시장의 독립형 벤더들은 파트너십을 강화하고 상호 운용성을 향상시키며, 이전 구매 주기에서 입증해야 했던 것보다 더 명확한 비즈니스 가치를 제시해야 하는 상황에 직면해 있습니다.

기존 급여·인사 시스템과의 통합이 주는 복잡성

레거시 급여 계산 및 인사 시스템과의 통합은 결근 관리 소프트웨어 시장의 확산을 저해하는 가장 두드러진 요인 중 하나로 계속해서 꼽히고 있습니다. ISG는 2025년 인사 설문조사에서 코어 플랫폼과의 통합을 데이터 보안에 이어 두 번째로 중요한 도입 요인으로 꼽았습니다. NFP의 조사에 따르면, 지난 2년 동안 새로운 인사 기술을 도입한 조직 중 도입 후 효율성이 크게 향상되었다고 보고한 곳은 불과 31%에 그쳤으며, 통합상의 문제가 다른 많은 조직에서 성과가 제한적이었던 주된 원인이었습니다. 많은 대기업에서는 여전히 독자적인 데이터 구조를 가진 시스템으로 급여 계산을 수행하고 있기 때문에 결근 잔여 일수, 급여 계산, 휴가 내역 등의 데이터가 기존 환경과 새로운 환경 간에 원활하게 연동되지 않습니다. 이 때문에 결근 관리 소프트웨어 시장의 성장세가 둔화되고 있습니다. 구매 기업은 실제 컴플라이언스 업무 워크플로우에서 시스템을 신뢰할 수 있게 되기까지는 미들웨어나 IT 지원, 그리고 장기간에 걸친 테스트 주기가 필요한 경우가 많기 때문입니다.

부문별 분석

2025년에는 소프트웨어가 매출의 65.12%를 차지하며, 결근 관리 소프트웨어 시장에서 가장 큰 비중을 차지하게 되었습니다. 이러한 위상은 연방, 주, 지방 자치단체 및 고용주별로 제각각인 복잡한 휴가 규정에 유연하게 대응할 수 있는 맞춤형 플랫폼에 대한 기업 수요를 반영하고 있습니다. 대기업의 경우, 컴플라이언스상의 예외 사항마다 고유한 워크플로우 로직, 승인 경로 및 문서 세트가 필요한 경우가 많기 때문에 라이선싱 시스템을 선호하는 경향이 있습니다. 결근 관리 소프트웨어가 없는 경우에도, 기존의 HCM(인사 관리) 및 급여 계산 환경 내에서 세부 설정이 가능한 제품이 여전히 선호되고 있습니다. 그 결과, 많은 구매자가 정책 설정이나 프로세스 실행을 직접 제어하기를 원하기 때문에 소프트웨어가 여전히 주요 지출 항목으로 차지하는 비중이 높습니다.

서비스 분야는 2026년부터 2031년까지 연평균 성장률(CAGR) 10.11%로 확대될 것으로 예측되며, 이는 결근 관리 소프트웨어 시장 전체에서 도입 및 운영 지원의 중요성이 높아지고 있음을 보여줍니다. 구매자들은 플랫폼을 소유한다고 해서 설정 업데이트, 법규 준수 모니터링, 직원과의 소통, 그리고 사례 관리 지원이 더 이상 필요하지 않게 되는 것은 아니라는 점을 점점 더 인식하고 있습니다. 각 주에서 새로운 PFML 규정이 제정될 때마다 추가적인 설정 작업이 발생하기 때문에 인사 팀은 소규모 및 중견 기업의 고용주에게 있어 관리형 서비스 및 자문 지원의 중요성이 점점 더 커지고 있습니다. Oracle이 2026년 2월에 실시한 ‘Absence Management 26A"업데이트에서는 직원의 휴가 신청 처리 시 업로드된 정책 문서를 참조하는 AI 에이전트가 추가되었습니다. 이는 과거 소프트웨어 계층 밖에 있던 업무가 제품 설계에 점차 통합되기 시작하고 있음을 보여줍니다. 그럼에도 불구하고, 고용주들이 더 신속한 도입, 규정 위반 감소, 그리고 정책을 반복 가능한 일상 업무 흐름으로 전환하기 위한 추가적인 지원을 요구하고 있기 때문에 결근 관리 소프트웨어 시장에는 여전히 지속적인 성장 여지가 있습니다.

2025년에는 클라우드 기반 도입이 매출의 55.24%를 차지했으며, 도입 형태별로는 결근 관리 소프트웨어 시장에서 가장 큰 점유율을 기록했습니다. 이러한 우위는 주나 시의 변경으로 인해 수급 자격, 복리후생 제도, 또는 서류 요건에 영향이 발생할 경우, SaaS 공급업체가 법적 규정의 업데이트를 신속하게 반영할 수 있기 때문입니다. 관리 업무를 생략할 경우, 다른 많은 인사 업무보다 이 갱신 속도가 더 중요해집니다. 왜냐하면 오류가 발생하면 급여, 수급 자격, 법적 규정 준수에 동시에 영향을 미칠 가능성이 있기 때문입니다. On-Premise형 시스템은 데이터 보관 장소나 내부 호스팅에 관한 규정이 여전히 엄격한 정부 기관, 국방 기관 및 금융 서비스 업계의 일부에서 여전히 확고한 도입 기반을 유지하고 있습니다. 이로 인해 도입 수요는 제각각이지만, 구매자들이 공급업체에 관리 편의성과 신속성을 모두 지원해 줄 것을 요구하는 경향이 강해지고 있는 이유도 뒷받침되고 있습니다.

클라우드 기반 도입 역시 가장 빠르게 성장하고 있는 선택지이며, 이 부문의 결근 관리 소프트웨어 시장 규모는 2031년까지 연평균 성장률(CAGR) 9.53%로 확대될 것으로 전망됩니다. ISG의 보고서에 따르면, 조직의 83%가 2027년 말까지 클라우드 기반 또는 하이브리드형 인사 모델을 운영할 것으로 예상되며, 이는 호스팅형 결근 관리 플랫폼으로의 전환이 계속되고 있음을 뒷받침합니다. 하이브리드 모델은 직원 포털이나 클라우드 기반 분석 기능을 필요로 하면서도, 일부 기밀성이 높은 건강 관련 데이터에 대해서는 보다 엄격한 내부 관리를 유지하고자 하는 중견 기업 및 유럽의 고용주들 사이에서 지지를 넓혀가고 있습니다. 이러한 구조는 감사 대응 체계, 보안 인증 및 데이터 처리의 투명성을 매우 중요하게 여기는 국가들의 조달 요구 사항과 부합합니다. 따라서, 결근 관리 소프트웨어 시장 전반에서 성숙한 하이브리드 로드맵을 갖춘 벤더는 법규제에 신속하게 대응하는 동시에 보다 보수적인 데이터 거버넌스를 필요로 하는 기업과의 계약을 확보하는 데 있어 더 유리한 입장에 있습니다.

지역별 분석

2025년, 북미는 결근 관리 소프트웨어 시장 점유율의 35.12%를 차지하며, 지역별 최대 수익원이 되었습니다. 미국이 여전히 주요 주도적 역할을 하고 있는 이유는 고용주가 연방 FMLA(가족 의료 휴가법), 주 PFML(유급 가족 의료 휴가) 규정, 지방 자치 단체의 유급 병가 조례, 그리고 ADA(장애인법)에 따른 합리적 편의 제공 요건을 동시에 관리해야 하는 경우가 많기 때문입니다. 2026년에는 일부 주와 지방 자치 단체에서 유급 휴가 제도가 도입되거나 확대됨에 따라, 이미 복잡한 운영 환경이 더욱 복잡해졌습니다. 또한, “근무지 규정"도 중요한 요소가 됩니다. 휴가 의무는 일반적으로 직원의 실제 근무지를 기준으로 결정되기 때문에 분산형 채용은 규정 준수 측면에서 직접적인 요인이 됩니다. 캐나다와 멕시코에서는 주마다 다른 규정 및 제도의 동향에 따라 지역적 수요가 더해지고 있지만, 북미의 결근 관리 소프트웨어 시장의 대부분은 여전히 미국이 차지하고 있습니다.

아시아태평양은 2026년부터 2031년까지 연평균 성장률(CAGR) 11.11%를 기록하며, 결근 관리 소프트웨어 시장 규모 측면에서 가장 빠른 성장세를 보일 것으로 전망됩니다. 이 지역의 상황은 북미와 다릅니다. 인도나 동남아시아의 많은 고용주들은 기존의 휴가 관리 플랫폼을 대체하는 것이 아니라, 처음으로 디지털 인사 시스템을 구축하고 있기 때문입니다. 이로 인해 그린필드 수요가 증가하며, 성숙 시장에서 볼 수 있는 시스템 통합에 따른 부담이 일부 완화됩니다. 호주, 일본, 한국, 중국 역시 노동 규정 준수 기대감의 고조, 디지털 인사 시스템의 보급 확대, 그리고 휴가 및 근로 시간에 대한 의무 이행에 대한 보다 체계적인 감시를 통해 결근 관리 소프트웨어 시장을 뒷받침하고 있습니다.

2025년, 유럽은 독일, 영국, 프랑스를 필두로 여전히 제3의 주요 지역 클러스터로서의 지위를 유지했습니다. 2025년, 유럽의 근로자들은 배정된 근로 시간의 15%를 결근했으며, 이는 연간 37근무일에 해당합니다. 특히 프랑스와 이탈리아에서는 건강 관련 결근 비율이 특히 높아졌습니다. 직원 건강 기록에는 보다 강력한 법적 근거, 보다 엄격한 거버넌스, 그리고 보다 명확한 처리 관리가 요구되므로, GDPR(EU 개인정보보호규정)은 여전히 중요한 선정 요인으로 남아 있습니다. 또한, 이 지역에서는 새로운 보고 의무나 정책 전환의 영향도 받고 있으며, 그로 인해 획일적인 단일 기능 도구보다 설정이 가능한 시스템의 가치가 높아지고 있습니다. 남미, 중동 및 아프리카는 여전히 규모는 작지만, 노동 규제가 정비되고 있는 지역에서는 수요가 증가하고 있으며, 고용주들은 노무 관리 시스템의 데이터 거버넌스 기준 향상에 힘쓰고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.07.08According to Mordor Intelligence, the absence management software market was valued at USD 17.23 billion in 2025, grew to USD 18.27 billion in 2026, and is forecast to reach USD 25.99 billion by 2031, expanding at a CAGR of 7.30% during 2026-2031.

This report is Segmented by Component (Software and Services), Deployment Mode (Cloud-Based, Hybrid, and More), End User Enterprise Size (Large Enterprises and Small and Medium-Sized Enterprises), Application (Leave Management, Compliance Management, and More), End-User Industry (Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Absence Management Software Market Trends and Insights

Stricter Multi-Jurisdiction Leave And Labor Compliance Requirements

Multi-jurisdiction leave rules have shifted from an HR inconvenience to a core operating issue for employers in the absence of management software. In 2026, Delaware, Maine, Minnesota, Colorado, and New York City either launched major paid leave programs or expanded existing entitlements, bringing the total to 15 states and Washington, D.C. that already had mandatory PFML frameworks in place. The applicable rule set usually follows the employee's physical work location, not the employer's state of incorporation, which means each remote hire in a new state can create a new compliance requirement. Employers also need to administer ADA, PWFA, and state PFML obligations in parallel, and that combination creates documentation, certification, and notice steps that spreadsheet workflows do not handle consistently. In the absence of a management software market, vendors that can automatically update leave rules by location gain a clear product advantage because buyers increasingly value accuracy and speed over generic workflow coverage.

Cloud-Based Human Resources Software Adoption

Cloud adoption has evolved into a capability decision rather than a narrow cost decision, and that shift is expanding the absence management software market. ISG's 2025 HR technology survey found that 69% of organizations already operated SaaS or hybrid cloud HR models, and 83% expected to do so by the end of 2027. The same survey showed average HR AI budgets rising to USD 1.6 million in 2026, indicating that cloud platforms are now the default base for analytics, automation, and AI-enabled workflow tools. Large HCM vendors are also embedding native absence functionality into broader suites, raising enterprise expectations for integration, reporting, and workflow continuity. That is pushing standalone vendors in the absence management software market to deepen partnerships, improve interoperability, and show clearer business value than they needed to prove in earlier buying cycles.

Legacy Payroll And Human Resources System Integration Complexity

Integration with legacy payroll and HR systems remains one of the clearest brakes on wider adoption in the absence management software market. ISG ranked core-platform integration as the second-most-important adoption factor in its 2025 HR survey, just behind data security. NFP found that only 31% of organizations that implemented new HR technology during the previous two years reported significant efficiency gains after deployment, and integration problems were a major reason many others saw limited returns. Many large employers still run payroll on systems with proprietary data structures, so absence balances, pay calculations, and leave events do not move cleanly between old and new environments. This slows the absence management software market because buyers often need middleware, IT support, and long testing cycles before they can trust the system in live compliance workflows.

Other drivers and restraints analyzed in the detailed report include:

- Remote And Hybrid Workforce Policy Administration Needs

- Demand For Automation, Analytics, And Employee Self-Service

- Sensitive Workforce Health Data Privacy Risks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software accounted for 65.12% of revenue in 2025, making it the largest component of the absence management software market. That position reflects enterprise demand for configurable platforms that can be adapted to complex federal, state, local, and employer-specific leave rules. Large employers have often preferred licensed systems because each compliance exception can require its own workflow logic, approval path, and documentation set. In the absence of management software, this still favors products that allow deep configuration within existing HCM and payroll environments. The result is a component mix in which software remains the core spending category, as many buyers still want direct control over policy setup and process execution.

Services are forecast to expand at a 10.11% CAGR from 2026 to 2031, showing that implementation and operational support are becoming more important across the absence management software market. Buyers increasingly recognize that owning a platform does not remove the need for configuration updates, legal monitoring, employee communications, and case administration support. Each new state PFML rule creates additional setup work, making managed services and advisory support more relevant for mid-market employers with smaller HR teams. Oracle's February 2026 Absence Management 26A update added AI agents that reference uploaded policy documents during employee leave interactions, demonstrating how product design is beginning to absorb work that once sat outside the software layer. Even so, the absence management software market still offers room for continued growth, as employers seek faster deployment, fewer compliance errors, and more support for translating policy into repeatable daily workflows.

Cloud-based deployment accounted for 55.24% of revenue in 2025, giving it the largest share of the absence management software market by deployment mode. Its lead comes from the fact that SaaS vendors can quickly push statutory rule updates when a state or city change affects eligibility, benefit design, or documentation requirements. That update speed matters more in the absence of administration than in many other HR tasks because errors can affect pay, eligibility, and legal compliance simultaneously. On-premises systems still retain a real installed base in government, defense, and parts of financial services where data residency and internal hosting rules remain strict. This keeps deployment demand mixed, but it also reinforces why buyers increasingly ask vendors to support both control and speed.

Cloud-based deployment is also the fastest-growing option, with the absence management software market size for this segment projected to expand at a 9.53% CAGR through 2031. ISG reported that 83% of organizations expected to operate cloud- or hybrid-HR models by the end of 2027, supporting continued migration toward hosted absence platforms. Hybrid models are gaining ground among mid-market and European employers that want employee portals and cloud-based analytics while keeping some sensitive health-related data under tighter internal control. That structure aligns with procurement needs in countries where buyers place strong emphasis on audit readiness, security certifications, and transparency in data handling. Across the absence management software market, vendors with mature hybrid roadmaps are therefore better placed to win enterprise contracts that require both statutory agility and more conservative data governance.

Complete Report Scope:

- By Component

- Software

- Services

- By Deployment Mode

- Cloud-Based

- On-Premises

- Hybrid

- By End User Enterprise Size

- Large Enterprises

- Small and Medium-Sized Enterprises

- By Application

- Leave Management

- Compliance Management

- Disability and Return-to-Work Management

- Analytics and Reporting

- By End-User Industry

- Information Technology (IT) and Telecom

- Banking, Financial Services and Insurance (BFSI)

- Healthcare and Life Sciences

- Industrial Manufacturing

- Retail and eCommerce

- Government and Public Sector

- Others

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- Germany

- United Kingdom

- France

- Italy

- Spain

- Rest of Europe

- Asia-Pacific

- China

- Japan

- India

- Australia

- South Korea

- Southeast Asia

- Rest of Asia-Pacific

- Middle East

- Saudi Arabia

- United Arab Emirates

- Rest of Middle East

- Africa

- South Africa

- Nigeria

- Rest of Africa

- North America

Geography Analysis

North America held 35.12% of the absence management software market share in 2025, making it the largest regional revenue pool. The United States remains the main driver because employers often have to administer federal FMLA, state PFML rules, local paid sick leave ordinances, and ADA accommodation requirements simultaneously. In 2026, several states and localities launched or expanded paid leave programs, further complicating an already dense operating environment. The work-situs rule also matters because leave obligations usually follow the employee's physical work location, making distributed hiring a direct compliance trigger. Canada and Mexico add regional demand through differing provincial rules and formalization trends, but the North American absence management software market still draws most of its weight from the United States.

Asia-Pacific is projected to record the fastest growth in the absence management software market size, at an 11.11% CAGR from 2026 to 2031. The regional story differs from North America because many employers in India and Southeast Asia are building digital HR systems for the first time rather than replacing older leave platforms. That creates more greenfield demand and reduces some of the integration drag seen in mature markets. Australia, Japan, South Korea, and China are also supporting the absence management software market through tighter labor compliance expectations, broader digital HR adoption, and more formal monitoring of leave and work-hour obligations.

Europe remained the third major regional cluster in 2025, led by Germany, the United Kingdom, and France. European employees missed 15% of assigned working time in 2025, equal to 37 working days per year, and France and Italy posted especially high health-related absence shares. GDPR remains a major selection factor because employee health records require stronger legal justification, tighter governance, and clearer processing controls. The region is also influenced by new reporting obligations and policy shifts that raise the value of configurable systems over rigid point tools. South America, the Middle East, and Africa remain smaller in scale, but demand is rising where labor regulation is formalizing, and employers are improving data governance standards for workforce systems.

- WorkForce Software, LLC

- TimeClock Plus, LLC

- AbsenceSoft

- Qcera Inc.

- Optis

- Stiira Corporation

- Vacation Tracker Technologies Inc.

- Appogee HR Limited

- Calamari sp. z o.o. sp.k.

- absence.io GmbH

- Personio SE and Co. KG

- Timetastic Ltd.

- Venforce Inc.

- DaysPlan, Inc.

- Breathe HR Limited

- Leave Dates Ltd.

- actITIME Inc.

- FINEOS Corporation

- TeamSense Inc.

- tamigo ApS

- Ironflow Technologies Inc.

- Bright HR Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Stricter Multi-Jurisdiction Leave and Labor Compliance Requirements

- 4.3.2 Cloud-Based Human Resources Software Adoption

- 4.3.3 Remote and Hybrid Workforce Policy Administration Needs

- 4.3.4 Demand for Automation, Analytics, and Employee Self-Service

- 4.3.5 Return-to-Office Accommodation Request Growth

- 4.3.6 Five-Generation Workforce Complexity

- 4.4 Market Restraints

- 4.4.1 Legacy Payroll and Human Resources System Integration Complexity

- 4.4.2 Sensitive Workforce Health Data Privacy Risks

- 4.4.3 Uncontrolled Generative Artificial Intelligence Use in Leave Decisions

- 4.4.4 Standalone Vendor Pricing Pressure from Bundled Human Capital Management Suites

- 4.5 Industry Value-Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Software

- 5.1.2 Services

- 5.2 By Deployment Mode

- 5.2.1 Cloud-Based

- 5.2.2 On-Premises

- 5.2.3 Hybrid

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium-Sized Enterprises

- 5.4 By Application

- 5.4.1 Leave Management

- 5.4.2 Compliance Management

- 5.4.3 Disability and Return-to-Work Management

- 5.4.4 Analytics and Reporting

- 5.5 By End-User Industry

- 5.5.1 Information Technology (IT) and Telecom

- 5.5.2 Banking, Financial Services and Insurance (BFSI)

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Industrial Manufacturing

- 5.5.5 Retail and eCommerce

- 5.5.6 Government and Public Sector

- 5.5.7 Others

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Australia

- 5.6.4.5 South Korea

- 5.6.4.6 Southeast Asia

- 5.6.4.7 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 WorkForce Software, LLC

- 6.4.2 TimeClock Plus, LLC

- 6.4.3 AbsenceSoft

- 6.4.4 Qcera Inc.

- 6.4.5 Optis

- 6.4.6 Stiira Corporation

- 6.4.7 Vacation Tracker Technologies Inc.

- 6.4.8 Appogee HR Limited

- 6.4.9 Calamari sp. z o.o. sp.k.

- 6.4.10 absence.io GmbH

- 6.4.11 Personio SE and Co. KG

- 6.4.12 Timetastic Ltd.

- 6.4.13 Venforce Inc.

- 6.4.14 DaysPlan, Inc.

- 6.4.15 Breathe HR Limited

- 6.4.16 Leave Dates Ltd.

- 6.4.17 actiTIME Inc.

- 6.4.18 FINEOS Corporation

- 6.4.19 TeamSense Inc.

- 6.4.20 tamigo ApS

- 6.4.21 Ironflow Technologies Inc.

- 6.4.22 Bright HR Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment