|

시장보고서

상품코드

2063753

클라우드 HCM 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Cloud HCM Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

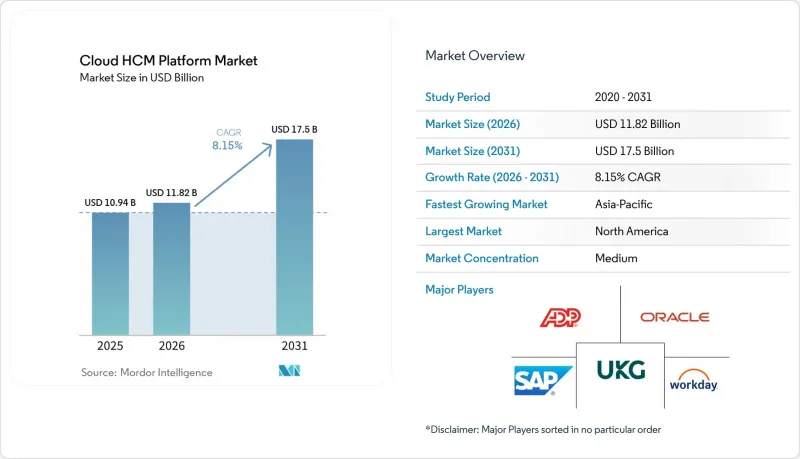

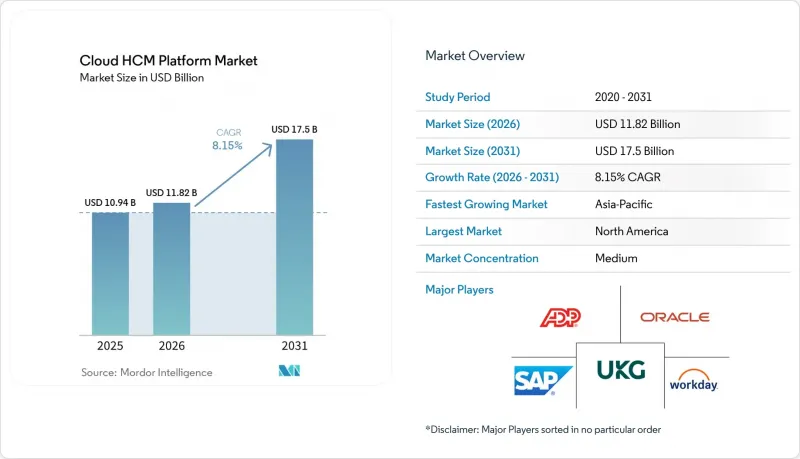

Mordor Intelligence에 의하면, 클라우드 HCM 플랫폼 시장 규모는 2025년 109억 4,000만 달러로 평가되었습니다. 2026년에는 118억 2,000만 달러로 확대되어 2031년까지 175억 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 8.15%로 성장할 것으로 전망됩니다.

본 보고서는 배포 모델(퍼블릭 클라우드, 프라이빗 클라우드, 하이브리드 클라우드), 조직 규모(대기업, 중소기업), 용도(핵심 HR 및 인사 관리, 인재 채용·온보딩 등), 산업 분야(은행 및 금융 서비스·보험 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 클라우드 HCM 플랫폼 시장 동향 및 인사이트

AI를 활용한 역량 매핑 및 인재 인텔리전스의 가속화

주요 플랫폼에 통합된 스킬 추론 엔진은 현재 수십억 건의 트랜잭션 데이터 포인트를 처리하며, 직원의 역량을 자동으로 태그하고, 사내 이동 경로를 제시하며, 채용 주기를 단축하고 있습니다. Workday Skills Cloud만 해도 연간 8,000억 건 이상의 트랜잭션을 분석하고 있으며, 한편 SAP SuccessFactors의 Dynamic Skills 프레임워크는 조직이 틈새 역할에 맞추어 타사 온톨로지를 통합할 수 있도록 지원합니다. Censia나 Phenom과 같은 전문 파트너 기업들은 키워드 검색에 비해 잠재적 후보자 발굴 속도가 40% 빨라진다고 주장하며, 이를 통해 고용주는 기존 직원을 유사한 역량을 요구하는 직무로 재배치하고 채용 비용을 4분의 1로 절감할 수 있게 됩니다. 이러한 효과는 기술, 전문 서비스, 금융 서비스 기업에서 가장 두드러지게 나타나고 있으며, 평균 기술 반감기는 2.5년으로 단축되었고, 역동적인 인재 인텔리전스가 이사회 차원의 최우선 과제로 자리 잡고 있습니다.

대기업에서 기술 기반 인재 계획의 부상

시스코의 직원 3만 명을 대상으로 한 역량 기반 계획으로의 전환과 머크의 전사적 역량 분류 체계는 인재 설계의 단위로서 정적인 직종 대신 역량이 점점 더 중요시되고 있음을 보여줍니다. 조사에 따르면, 역량 기반 조직에서는 우수 직원의 이직률이 98% 감소했으며, 신입 사원의 업무 숙련 기간이 52% 단축되었습니다. 이에 발맞추어 각 플랫폼은 스킬 온톨로지 및 AI 기반 스킬 격차 분석 기능을 핵심 HR 시스템에 직접 통합하고 있습니다. SAP가 2025년에 출시한 ‘Joule Studio’를 통해 인사 팀은 IT 부서의 개입 없이도 기술 격차를 파악하고 교육을 추천하는 맞춤형 에이전트를 구축할 수 있게 됩니다. 제조 현장과 임상 직원을 대상으로 교차 교육을 실시하고 있는 제조·의료 기업에서는 초과 근무 시간과 결원율이 감소하고 있는 것으로 보고되고 있지만, 이러한 성공 여부는 본 가동 전에 레거시 데이터의 정제와 분류 체계 검증을 수행하느냐에 달려 있습니다.

데이터 소재지에 관한 법적 규제가 현지화 비용을 증가시키고 있습니다.

GDPR(EU 개인정보보호규정) 및 각국의 주권에 기반한 규정들이 뒤섞이면서, 국내 호스팅이 의무화됨에 따라 공급업체들은 인프라와 지원 팀을 이중으로 구축할 수밖에 없는 상황에 처해 있습니다. 중국의 사이버 보안법에서는 중국 국내에 독립된 인스턴스를 구축할 것을 요구하고 있으며, 인도와 인도네시아에서도 유사한 규제가 검토되고 있습니다. On-Premise 급여 계산 시스템에 클라우드 기반 인사 관리 모듈을 결합한 하이브리드 아키텍처가 비용 대비 효과가 높은 대안으로 부상하고 있지만, 이중 라이선스 비용과 복잡한 데이터 동기화로 인해 기대했던 비용 절감 효과가 저해되고 있습니다.

부문별 분석

2025년 기준으로 퍼블릭 클라우드는 클라우드 HCM 플랫폼 시장의 56.41%를 차지했으며, 이는 On-Premise 하드웨어가 필요 없고 분기별로 업데이트를 제공하는 Workday의 멀티테넌트 SaaS 모델을 반영한 것입니다. 하이브리드 모델은 기업들이 데이터 주권 관련 법규를 준수하기 위해 퍼블릭 클라우드의 인사 관리 모듈과 On-Premise 급여 계산 시스템을 결합함에 따라 연평균 성장률(CAGR) 10.64%로 성장하며 그 매력이 높아지고 있습니다. 듀얼 라이선스의 경제성은 여전히 미묘하지만, 두 가지를 병행함으로써 대규모 세계 확장에 일반적으로 수반되는 600만-1,200만 달러의 전환 비용을 피할 수 있습니다.

하이브리드 환경에서는 Oracle Human Data Loader나 SAP Integration Suite와 같은 실시간 커넥터에 대한 의존도가 높아지고 있으며, 급여 계산 오류 위험을 줄이면서 매일 동기화를 가능하게 하고 있습니다. 기존 급여 시스템을 대상으로 할인된 유지보수 서비스를 제공하는 제3자 지원 기업들은 비용 대비 효과의 산정 방식을 더욱 변화시키고 있습니다. 가트너는 2028년까지 기업의 85%가 클라우드 중심의 인사 인프라를 운영할 것으로 예측하고 있지만, 규제가 엄격한 업계에서는 장기적으로 하이브리드 모델을 유지할 것으로 보입니다. 따라서 개인정보 보호 규제가 강화됨에 따라, 하이브리드 구성을 위한 클라우드 HCM 플랫폼 시장 규모는 시장 전체의 성장률을 웃도는 추세를 보일 것으로 예측됩니다.

2025년에는 대기업들이 매출 점유율의 68.04%를 차지하며, 전 세계의 급여 계산, 분석, 인력 관리를 아우르는 엔드투엔드 제품군을 구매했습니다. 한편, 중소기업(SME)은 연평균 성장률(CAGR) 11.02%로 성장하고 있으며, 직원 1인당 월 6달러부터 시작하는 가격 정책과 90일 이내에 가동을 시작하겠다는 약속에 매력을 느끼고 있습니다. 중소기업용 클라우드 HCM 플랫폼 시장 규모는 여전히 작지만, 급여 계산, 복리후생, 근태 관리를 통합한 경량형 제품군이 스프레드시트를 대체함에 따라 급속히 확대되고 있습니다.

HiBob, Rippling, Deel 등의 벤더들은 직관적인 모바일 인터페이스, IT와 인사 관리의 융합, 그리고 다국적 규정 준수 기능을 도입함으로써 차별화를 꾀하고 있습니다. 예산이 제한적임에도 불구하고, 68%의 중소기업은 인프라 비용을 절감하기 위해 클라우드 도입을 선호하고 있지만, 46%는 여전히 도입 비용을 걸림돌로 꼽고 있습니다. 프리미엄 방식의 입문형 요금제와 템플릿을 활용한 온보딩을 통해 이러한 장벽이 완화됨에 따라, 대기업에서의 보급이 정체되는 상황에서도 중소기업의 두 자릿수 도입률은 지속될 것으로 전망됩니다.

지역별 분석

북미는 2025년 매출의 37.44%를 차지했으며, 미국 인사관리국(OPM)과의 1억 달러 규모 Workday 계약이나 에너지부의 3,800만 달러 규모 ‘기술 현대화 기금’ 지원을 통한 도입 등 고액 연방 정부 계약이 성장의 견인차 역할을 했습니다. 캐나다와 멕시코에서는 SAP Joule이 제공하는 2025년 스페인어판 급여 명세서 설명 기능을 바탕으로, 도입이 착실히 진행되고 있습니다. 벤더의 지배력은 두드러지며, 직원 수 5,000명 이상의 기업에서 엔터프라이즈 관련 의사결정의 95% 이상을 Workday, SAP, Oracle이 차지하고 있으며, 신규 구매 검토 조사에서는 Workday가 1위를 차지하고 있습니다.

아시아태평양은 연평균 성장률(CAGR) 10.27%를 기록하며 가장 빠르게 성장하고 있는 지역입니다. Darwinbox의 해외 매출이 9배로 급증한 점과 Ramco Systems가 150개국에서 급여 계산 서비스를 제공하고 있다는 사실은 현지 업체들이 지역을 넘어 사업을 확장하고 있음을 보여줍니다. 일본에서는 SmartHR이 7만 개사의 도입 기업을 확보하며 국내 시장 점유율 1위를 차지하고 있지만, 전 세계 서비스 제공업체들은 사이버 보안 프로토콜을 준수하기 위해 중국 시장에 별도의 인스턴스를 운영해야 하므로 현지화 비용이 증가하고 있습니다. 인도에서 시행이 임박한 데이터 보호법과 인도네시아의 규정 71/2019는 규정 준수(컴플라이언스)의 복잡성을 가중시키고 있으며, 구매자들이 국가별 급여 계산 모듈을 갖춘 공급업체를 찾도록 만들고 있습니다.

유럽은 성장세가 둔화되고는 있지만, 여전히 중요한 시장입니다. GDPR(EU 개인정보보호규정) 및 국가 주권에 관한 법령에 따라 국내 데이터센터 설치가 의무화됨에 따라, 워크데이는 이에 발맞추어 유럽 고객을 대상으로 특화된 더블린의 AI 센터에 1억 7,500만 유로(1억 9,700만 달러)를 투자하기로 결정했습니다. SAP는 S/4HANA와의 긴밀한 통합과 50개국 이상에 걸친 현지화된 급여 계산 기능을 통해 독일과 프랑스에서 그 성장세를 이어가고 있습니다. 한편, Oracle이 E.ON사를 인수한 것은 규제 대상인 유틸리티 분야에서 이에 대한 수용도가 높아지고 있음을 보여줍니다. 남미, 중동 및 아프리카는 절대적인 수치로는 뒤처져 있지만, 정부의 디지털화 추진과 모바일 우선 인재 관리를 통해 성장세를 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the cloud HCM platform market size is expected to increase from USD 10.94 billion in 2025 to USD 11.82 billion in 2026 and reach USD 17.50 billion by 2031, growing at an 8.15% CAGR over 2026-2031.

This report is Segmented by Deployment Model (Public Cloud, Private Cloud, and Hybrid Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Application (Core HR and Personnel Administration, Talent Acquisition and Onboarding, and More), Industry Vertical (Banking Financial Services and Insurance, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Cloud HCM Platform Market Trends and Insights

Accelerating AI-Driven Skill Mapping and Talent Intelligence

Skill inference engines embedded in leading platforms now process billions of transactional datapoints to auto-tag employee capabilities, surface internal mobility paths, and shorten hiring cycles. Workday Skills Cloud alone analyzes more than 800 billion transactions annually, while SAP SuccessFactors Dynamic Skills framework lets organizations integrate third-party ontologies for niche roles. Specialized partners such as Censia and Phenom claim 40% faster passive-candidate discovery versus keyword search, enabling employers to redeploy existing staff into skill-adjacent roles and cut recruiting costs by one-quarter. The effect is felt most in technology, professional-services, and financial-services companies where average skill half-life has dropped to 2.5 years, making dynamic talent intelligence a board-level priority.

Rise of Skills-Based Workforce Planning in Large Enterprises

Cisco's 30 000-employee shift to skills-based planning and Merck's enterprise-wide skills taxonomy show how competencies are replacing static jobs as the unit of workforce design. Research indicates skills-based organizations realize 98% higher high-performer retention and 52% faster ramp-up for new hires. Platforms respond by embedding skills ontologies and AI-driven gap analytics directly into core HR. SAP's 2025 launch of Joule Studio enables HR teams to build custom agents that pinpoint skill gaps and recommend training without IT intervention. Manufacturing and healthcare firms that cross-train production or clinical staff report lower overtime and vacancy rates, although success depends on cleansing legacy data and validating taxonomies before go-live.

Data Residency Legislation Increasing Localization Costs

GDPR and a patchwork of national sovereignty rules require in-country hosting, forcing vendors to duplicate infrastructure and support teams. China's cybersecurity laws demand separate Chinese instances, while India and Indonesia contemplate similar mandates. Hybrid architectures, on-premises payroll with cloud talent modules, are emerging as cost-effective workarounds, yet dual licenses and complex data synchronization erode anticipated savings.

Other drivers and restraints analyzed in the detailed report include:

- Integration of Generative AI Copilots Into HCM User Interfaces

- Surge in Global Payroll Compliance Complexity

- Persistent Integration Bottlenecks With Legacy ERP Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Public cloud accounted for 56.41% of the cloud HCM platform market in 2025, reflecting Workday's multi-tenant SaaS model that delivers quarterly updates without on-premises hardware. Hybrid models hold growing appeal, expanding at a 10.64% CAGR as enterprises pair public-cloud talent modules with on-premises payroll to satisfy data-sovereignty statutes. Dual-license economics remain delicate, yet coexistence avoids the USD 6-12 million migration costs typical of large global rollouts.

Hybrid deployments increasingly rely on real-time connectors such as Oracle Human Data Loader and SAP Integration Suite, enabling daily synchronization while mitigating payroll-error risk. Third-party support firms offering discounted maintenance for legacy payroll further shift the cost-benefit calculus. Gartner expects 85% of enterprises to operate cloud-centered HR infrastructure by 2028, but regulated sectors will keep hybrid models for the long term. The cloud HCM platform market size for hybrid setups is therefore positioned to outpace overall growth as privacy mandates tighten.

Large enterprises held 68.04% revenue share in 2025, purchasing end-to-end suites spanning global payroll, analytics, and workforce management. SMEs, however, are growing at 11.02% CAGR, attracted to per-employee pricing that starts at USD 6 monthly and promises go-lives inside 90 days. The cloud HCM platform market size for SMEs is still small, yet rising quickly as lightweight suites bundle payroll, benefits, and time tracking to displace spreadsheets.

Vendors such as HiBob, Rippling, and Deel differentiate via intuitive mobile interfaces, IT-HR convergence, and embedded multi-country compliance. Despite tight budgets, 68% of SMEs prefer cloud deployments to avoid infrastructure costs, with 46% still citing implementation expense as a barrier. Freemium entry tiers and template-driven onboarding lower those hurdles, suggesting sustained double-digit SME adoption even as enterprise penetration plateaus.

Geography Analysis

North America generated 37.44% of 2025 revenue, anchored by high-value federal contracts such as the U.S. Office of Personnel Management's USD 100 million Workday award and the Department of Energy's USD 38 million Technology Modernization Fund-backed rollout. Canada and Mexico show steady uptake, supported by SAP Joule's 2025 Spanish-language payroll explanations. Vendor dominance is stark: Workday, SAP, and Oracle influence over 95% of enterprise decisions at firms with more than 5 000 employees, with Workday leading new-buyer consideration surveys.

Asia-Pacific is the fastest-growing territory at a 10.27% CAGR. Darwinbox's 9-times international revenue surge and Ramco Systems' 150-country payroll reach illustrate home-grown vendors scaling beyond regional borders. Japan's SmartHR leads domestic share with 70 000 tenants, while global providers must operate separate Chinese instances to comply with cybersecurity protocols, inflating localization costs. India's impending data-protection law and Indonesia's Regulation 71/2019 add to compliance complexity, steering buyers toward vendors with country-specific payroll modules.

Europe remains material despite slower expansion. GDPR and national sovereignty statutes compel in-country data centers, prompting Workday to commit EUR 175 million (USD 197 million) to an AI center in Dublin tailored for European customers. SAP's deep integration with S/4HANA and localized payroll spanning 50-plus countries sustains traction in Germany and France, while Oracle's E.ON win underlines growing acceptance in regulated utilities. South America, the Middle East, and Africa trail in absolute value yet gain momentum through government digitization mandates and mobile-first workforce management.

- Workday, Inc.

- SAP SE

- Oracle Corporation

- Automatic Data Processing, Inc.

- UKG Inc.

- Ceridian HCM Holding Inc.

- BambooHR LLC

- Paycom Software, Inc.

- Cornerstone OnDemand, Inc.

- PeopleStrategy, Inc.

- Rippling People Center, Inc.

- TriNet Group, Inc.

- Zenefits (YourPeople, Inc.)

- Gusto, Inc.

- Ramco Systems Limited

- Zoho Corporation Pvt. Ltd.

- The Sage Group plc

- Namely, Inc.

- HiBob Ltd.

- Darwinbox Digital Solutions Pvt. Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerating AI-Driven Skill Mapping and Talent Intelligence

- 4.2.2 Rise of Skills-Based Workforce Planning in Large Enterprises

- 4.2.3 Government Incentives for Cloud Migration of HR Systems

- 4.2.4 Surge in Global Payroll Compliance Complexity

- 4.2.5 Integration of Generative AI Copilots Into HCM User Interfaces

- 4.2.6 Expansion of Industry-Specific Cloud HCM Accelerators

- 4.3 Market Restraints

- 4.3.1 Data Residency Legislation Increasing Localization Costs

- 4.3.2 Persistent Integration Bottlenecks With Legacy ERP Stacks

- 4.3.3 High Total Cost of Ownership for Mid-Market Buyers

- 4.3.4 Vendor Lock-In Concerns Limiting Long-Term Contract Commitments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Public Cloud

- 5.1.2 Private Cloud

- 5.1.3 Hybrid Cloud

- 5.2 By Organization Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium Enterprises (SMEs)

- 5.3 By Application

- 5.3.1 Core HR and Personnel Administration

- 5.3.2 Payroll and Compensation Management

- 5.3.3 Talent Acquisition and Onboarding

- 5.3.4 Workforce Management and Time Tracking

- 5.3.5 Learning and Development

- 5.3.6 Performance and Succession Management

- 5.3.7 HR Analytics and Planning

- 5.4 By Industry Vertical

- 5.4.1 Banking, Financial Services and Insurance

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 IT and Telecommunications

- 5.4.4 Manufacturing

- 5.4.5 Retail and E-Commerce

- 5.4.6 Government and Public Sector

- 5.4.7 Education

- 5.4.8 Hospitality and Travel

- 5.4.9 Other Industry Verticals

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 United Kingdom

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Southeast Asia

- 5.5.4.7 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Kenya

- 5.5.6.4 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday, Inc.

- 6.4.2 SAP SE

- 6.4.3 Oracle Corporation

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 UKG Inc.

- 6.4.6 Ceridian HCM Holding Inc.

- 6.4.7 BambooHR LLC

- 6.4.8 Paycom Software, Inc.

- 6.4.9 Cornerstone OnDemand, Inc.

- 6.4.10 PeopleStrategy, Inc.

- 6.4.11 Rippling People Center, Inc.

- 6.4.12 TriNet Group, Inc.

- 6.4.13 Zenefits (YourPeople, Inc.)

- 6.4.14 Gusto, Inc.

- 6.4.15 Ramco Systems Limited

- 6.4.16 Zoho Corporation Pvt. Ltd.

- 6.4.17 The Sage Group plc

- 6.4.18 Namely, Inc.

- 6.4.19 HiBob Ltd.

- 6.4.20 Darwinbox Digital Solutions Pvt. Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment