|

시장보고서

상품코드

2063931

인적 자본 관리(HCM) 전사적 자원 계획 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Human Capital Management (HCM) Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

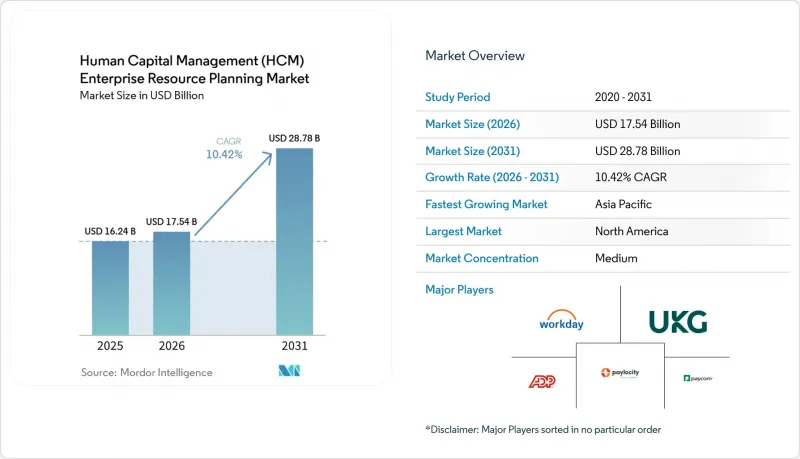

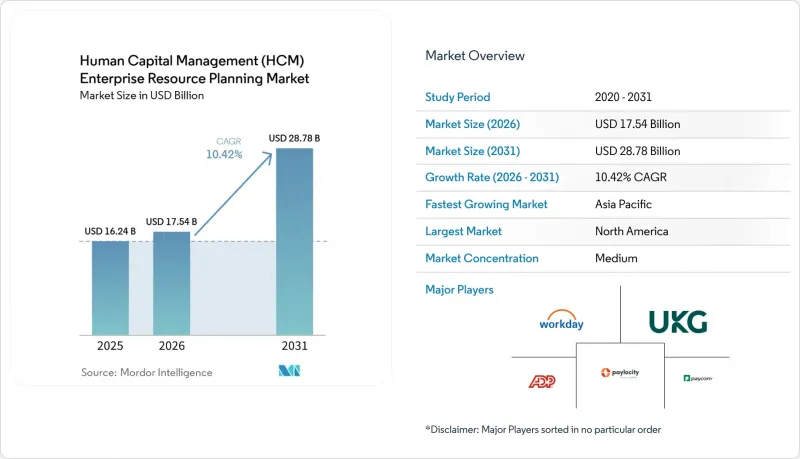

Mordor Intelligence에 의하면, 인적 자본 관리(HCM) 전사적 자원 계획(ERP) 시장 규모는 2026년 175억 4,000만 달러로 추정되고, 2031년까지 287억 8,000만 달러로 확대될 전망이며, 2026-2031년 CAGR 10.42%를 나타낼 것으로 예측됩니다.

본 보고서는 전개 모델별(클라우드, 온프레미스, 하이브리드), 조직 규모별(중소기업, 대기업), 업종별(제조업, 은행, 금융서비스 및 보험(BFSI), 의료, 소매 및 전자상거래, IT 및 통신, 정부 기관, 기타), 컴포넌트 또는 모듈별(핵심 HR, 인재 관리, 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 인적 자본 관리(HCM) 기업 자원 계획(ERP) 시장 동향 및 인사이트

클라우드 네이티브 HR 제품군으로의 전환 가속화

기업들은 온프레미스형 ERP 애드온에서 하드웨어 비용을 절감하고 업그레이드 부담을 줄일 수 있는 클라우드 플랫폼으로 전환하고 있습니다. Oracle은 2025 회계연도에 HCM Cloud의 고객 수가 두 자릿수 증가를 기록했다고 보고했으며, 그 이유로 기존 시스템에서는 18-24개월이 걸리던 도입 주기가 6-9개월로 단축된 점을 꼽았습니다. Workday 2026R1에는 일상적인 문의를 해결해 주는 AI 에이전트가 탑재되어 있어, 인사 담당자가 전략적인 계획 수립에 전념할 수 있도록 지원합니다. 구독형 가격 책정을 통해 설비 투자가 변동성 있는 운영 비용으로 전환되어, 인건비 변동에 따라 지출을 조정할 수 있게 됩니다. ADP의 Lyric 통합 데이터 모델은 통합에 따른 오버헤드를 줄이고 도입 기간을 단축합니다. 그러나 데이터 정제와 관련된 과제 및 워크플로우 재구축으로 인해, 고도로 맞춤형 기업에서는 전환이 지연되고 있습니다.

분석 중심의 인재 계획에 대한 수요

예측 분석은 고용주가 기술 격차를 예측하고, 인건비 예산을 최적화하며, 이직 위험을 파악하는 데 도움이 됩니다. Workday 사용자는 AI 기반 모델을 통해 간호사의 이직률을 50% 개선했습니다. 미국 노동통계국은 2031년까지 190만 명의 정규 간호사가 부족할 것으로 예측하고 있으며, 이에 따라 이직률 분석에 대한 수요가 높아지고 있습니다. 제조업체들은 스킬 인텔리전스를 도입하여 로봇 공학 및 적층 가공에 관한 직원 재교육을 실시함으로써 외부 채용 비용을 절감하고 있습니다. Oracle의 Dynamic Skills는 사내 후보자를 선별함으로써 채용까지 걸리는 기간을 약 30% 단축합니다. 규제 당국은 알고리즘의 편향을 면밀히 주시하고 있으며, EEOC(미국 연방 고용기회균등위원회)는 설명 가능성에 관한 지침을 발표했습니다.

기존 ERP로 인한 높은 전환 비용

데이터 이전에는 6-12개월이 소요되며, 고액의 컨설팅 비용이 필요할 수 있고, 그 비용은 연간 구독료의 15-20%에 달하기도 합니다. 기업은 이미 지불한 라이선스 비용을 손실로 계상하고, 중복되는 구독 요금을 정산하며, 사용자에 대한 재교육을 실시해야 하는데, 이것이 단기적인 전환을 방해하고 있습니다. 제조업 및 의료 부문에서 노조의 근무 일정에 대응하는 것은 시스템 재구축의 난관을 가중시키고, 투자 회수 기간을 길게 만들고 있습니다.

부문별 분석

2025년 기준으로 클라우드 도입은 인적 자본 관리(HCM) ERP 시장의 62.13%를 차지했으며, 2031년까지 연평균 성장률(CAGR) 15.12%를 나타낼 것으로 예측됩니다. Workday의 신규 계약 중 85%가 순수 클라우드 수주로 이루어지고 있으며, 이는 고객들이 지속적인 기능 제공을 선호하는 경향을 반영하고 있습니다. 정부 기관이나 국방 기관에서는 보안 요건을 충족하기 위해 급여 계산 엔진을 온프레미스로 유지하는 하이브리드 전략을 여전히 고수하고 있습니다. 그러나 듀얼 스택을 유지하면 비용 절감 효과가 떨어지기 때문에 각 벤더사는 레거시 버전의 제공을 단계적으로 중단하고 있습니다.

인적 자본 관리(HCM) ERP 시장에서는 이용자 수에 따른 요금 체계를 도입하여, 기업이 경기 사이클에 따라 지출을 유연하게 조정할 수 있는 플랫폼에 대한 평가가 높아지고 있습니다. Oracle HCM Cloud 25A는 온프레미스 고객보다 몇 달 앞서 구독자에게 AI 급여 대조 기능을 제공함으로써 혁신의 차이를 여실히 보여주었습니다. 데이터 소재지에 관한 규제로 인해 유럽 및 아시아태평양에서의 풀스택 도입이 지연될 가능성은 있지만, 많은 다국적 기업들은 하이브리드 구축보다 지역별 현지화를 선호하고 있습니다.

2025년에는 대기업이 매출의 57.23%를 차지한 것으로 평가되었으며, 감사 대응을 위한 통제, 다중 원장 급여 계산, 평균 계약액을 끌어올릴 수 있는 고도의 통합이 필요할 것으로 보입니다. 또한, 관련 학습 및 분석 솔루션도 도입하여 중소기업과의 비교에서 인적 자본 관리 ERP 시장 점유율 격차를 더욱 벌리고 있습니다. 반면, 중소기업은 온보딩 절차를 간소화함으로써 IT 비용을 절감할 수 있어 13.72%라는 더 높은 연평균 성장률(CAGR)을 기록하고 있습니다.

Gusto, BambooHR, HiBob은 90일 이내에 시스템 가동을 완료하는 정액제 패키지를 제공합니다. Workday는 2024년에 중견 기업용 에디션을 출시하며, 직원 수 500-2,500명 규모의 기업 시장에 진출했습니다. 중소기업들은 모바일 앱, 임베디드 결제, 번거롭지 않은 규정 준수 대응을 중요시하고 있지만, 많은 기업이 초기 단계에서 후계자 양성이나 교육 기능을 생략하고 있어 향후 성장 여지가 남아 있습니다. 각 벤더사는 이 부문을 중요하게 여기고 있습니다. 이는 해지율이 낮고 업셀링의 여지가 있으므로, 인적 자본 관리(HCM) ERP 시장 전체에서 고객 생애 가치(LTV)가 향상되기 때문입니다.

지역별 분석

북미는 엄격한 여러 주에 걸친 급여 계산 법규와 클라우드의 조기 도입에 힘입어 2025년 매출의 34.97%를 차지했습니다. 미국 국세청(IRS)이 W-2 전자 신고 기준을 하향 조정함에 따라 중견 기업의 전환이 가속화되었습니다. 대부분의 기업이 1단계 전환을 완료했고, 현재는 전체 제품군이 아닌 AI 애드온을 구매하는 경향이 있어 성장이 정체되고 있습니다.

아시아태평양은 예측 기간 동안 연평균 성장률(CAGR) 13.94%를 기록하며 가장 빠르게 성장하는 지역이 될 것으로 전망됩니다. 상품 및 서비스세(GST)와 사회보험 제도의 개혁으로 인해 급여 관리의 복잡성이 가중됨에 따라, 각국별 맞춤형 급여 계산 엔진의 도입이 필수적입니다. 호주 및 뉴질랜드에서는 클라우드 도입률이 높은 반면, 인도네시아와 베트남에서는 인프라 측면의 과제가 여전히 남아 있어 진전이 더딘 임베디드니다.

유럽의 동향은 규정 준수 중심입니다. GDPR(EU 개인정보보호규정)(일반 데이터 보호 규정)에서는 현지에서 데이터를 처리해야 할 의무가 있으며, 파견 근로자 지침에서는 급여 재계산이 요구되고 있기 때문입니다. 각 벤더사는 독일, 네덜란드, 아일랜드에 지역 데이터센터를 운영하고 있습니다. 폴란드와 루마니아에서 공유 서비스 허브가 확대됨에 따라 동유럽도 그 혜택을 누리고 있습니다. 중동은 ‘사우디 비전 2030’에 따른 노동력 개혁에 힘입어 성장하고 있지만, 아프리카는 남아프리카 공화국과 이집트를 제외하고는 아직 발전 단계에 머물러 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the human capital management (HCM) enterprise resource planning (ERP) market size is projected to expand from USD 17.54 billion in 2026 to USD 28.78 billion by 2031, registering a CAGR of 10.42% over 2026-2031.

This report is Segmented by Deployment Model (Cloud, On-Premise, and Hybrid), Organization Size (Small and Medium Enterprises, and Large Enterprises), Industry Vertical (Manufacturing, BFSI, Healthcare, Retail and E-Commerce, IT and Telecom, Government, and More), Component or Module (Core HR, Talent Management, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Human Capital Management (HCM) Enterprise Resource Planning Market Trends and Insights

Accelerated Transition to Cloud-Native HR Suites

Organizations are migrating from on-premise ERP add-ons to cloud platforms that cut hardware expense and reduce upgrade pain. Oracle reported double-digit HCM Cloud customer growth in fiscal 2025, citing deployment cycles of 6-9 months compared with 18-24 months on legacy stacks. Workday's 2026R1 embedded AI agents that resolve routine queries, freeing HR staff for strategic planning. Subscription pricing converts capital outlays into variable operating costs, aligning spend with headcount volatility. ADP's Lyric unified data model reduces integration overhead and shortens implementation time. Still, data-cleansing challenges and workflow re-engineering slow heavily customized enterprises.

Demand for Analytics-Driven Workforce Planning

Predictive analytics help employers anticipate skills gaps, optimize labor budgets, and flag attrition risk. Workday users achieved 50% better nurse retention via AI-driven models. The U.S. Bureau of Labor Statistics projects a shortfall of 1.9 million registered nurses by 2031, intensifying demand for retention analytics. Manufacturers deploy skills intelligence to retrain workers on robotics and additive manufacturing, lowering external hiring costs. Oracle's Dynamic Skills surfaces internal candidates, cutting time-to-fill by about 30%. Regulators are watching algorithmic bias, and the EEOC has issued guidance on explainability.

High Switching Costs From Legacy ERP

Data migration can last 6-12 months and require costly consultants, reaching 15-20% of annual subscription fees. Enterprises must write off sunk licenses, pay overlapping subscriptions, and retrain users, deterring near-term moves. Customized union scheduling in manufacturing and healthcare raises re-engineering hurdles, stretching payback periods.

Other drivers and restraints analyzed in the detailed report include:

- Compliance Complexity in Multi-Country Payroll

- Rise of Remote and Hybrid Work Models

- Data Privacy and Sovereignty Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud deployments accounted for 62.13% of the human capital management ERP market in 2025 and are expected to grow at a 15.12% CAGR through 2031. Pure cloud bookings represented 85% of Workday's new deals, reflecting customer preference for continuous feature delivery. Hybrid strategies persist for governments and defense agencies that keep payroll engines on-premise to satisfy security mandates. However, maintaining dual stacks undercuts savings, and vendors are phasing out legacy versions.

The human capital management ERP market increasingly rewards platforms that align fees with active headcount, allowing firms to flex spend during cycles. Oracle HCM Cloud 25A pushed AI payroll reconciliation to subscribers months ahead of on-premise clients, underscoring the innovation gap. Data-residency rules may slow full-stack adoption in Europe and Asia-Pacific, but most multinationals prefer localized regions over hybrid builds.

Large enterprises contributed 57.23% revenue in 2025 and require audit-ready controls, multi-ledger payroll, and deep integrations that lift average contract values. They also buy adjacent learning and analytics, widening the human capital management ERP market share gap versus smaller firms. Yet small and medium enterprises post the faster 13.72% CAGR as simplified onboarding trims IT overhead.

Gusto, BambooHR, and HiBob offer flat-rate bundles that complete go-lives in under 90 days. Workday launched a mid-market edition in 2024, entering the 500-2,500 employee band. SMEs value mobile apps, embedded payments, and hands-off compliance, though many skip succession and learning at first pass, leaving expansion potential. Vendors court this segment because low churn and upsell headroom lift lifetime value across the human capital management ERP market.

Geography Analysis

North America contributed 34.97% of 2025 revenue, driven by strict multi-state payroll laws and early cloud adoption. The IRS cut the W-2 e-file threshold, accelerating migration among mid-sized employers. Growth is plateauing as most enterprises finish first-wave migrations and now purchase AI add-ons rather than full suites.

Asia-Pacific is projected to be the fastest-growing region, with a compound annual growth rate (CAGR) of 13.94% during the forecast period. The implementation of in-country payroll engines has become crucial as Goods and Services Tax (GST) and social insurance reforms introduce additional layers of complexity into payroll management. Australia and New Zealand demonstrate high levels of cloud adoption, whereas Indonesia and Vietnam are experiencing slower progress due to persistent infrastructure challenges.

Europe's trajectory is compliance-driven, as the GDPR requires local data processing and the Posted Workers Directive requires payroll recalculations. Vendors run regional data centers in Germany, the Netherlands, and Ireland. Eastern Europe benefits as shared-services hubs grow in Poland and Romania. The Middle East is expanding under Saudi Vision 2030 workforce reforms, whereas Africa remains nascent outside South Africa and Egypt.

- Workday Inc.

- Ultimate Kronos Group, Inc.

- Ceridian HCM Holding Inc.

- Automatic Data Processing, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Cornerstone OnDemand, Inc.

- Bamboo HR LLC

- Namely Inc.

- Zoho Corporation Pvt. Ltd.

- Ramco Systems Limited

- PeopleStrategy, Inc.

- Gusto, Inc.

- TriNet Zenefits LLC

- HiBob Ltd.

- The Sage Group plc

- Epicor Software Corporation

- Unit4 N.V.

- Infor (US), Inc.

- Softworks Workforce Management Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated Transition to Cloud-Native HR Suites

- 4.2.2 Demand for Analytics-Driven Workforce Planning

- 4.2.3 Compliance Complexity in Multi-Country Payroll

- 4.2.4 Rise of Remote and Hybrid Work Models

- 4.2.5 AI-Powered Talent Acquisition and Retention Tools

- 4.2.6 Integration of HCM with IoT-Enabled Workforce Safety Systems

- 4.3 Market Restraints

- 4.3.1 High Switching Costs from Legacy ERP

- 4.3.2 Data Privacy and Sovereignty Concerns

- 4.3.3 Implementation Skill Shortage Among HR-IT Staff

- 4.3.4 Vendor Lock-In Fear in Mid-Market Enterprises

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Impact of Macroeconomic Factors on the Market

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Model

- 5.1.1 Cloud

- 5.1.2 On-Premise

- 5.1.3 Hybrid

- 5.2 By Organization Size

- 5.2.1 Small and Medium Enterprises

- 5.2.2 Large Enterprises

- 5.3 By Industry Vertical

- 5.3.1 Manufacturing

- 5.3.2 BFSI

- 5.3.3 Healthcare

- 5.3.4 Retail and E-commerce

- 5.3.5 IT and Telecom

- 5.3.6 Government

- 5.3.7 Other Industry Verticals

- 5.4 By Component

- 5.4.1 Core HR

- 5.4.2 Payroll

- 5.4.3 Talent Management

- 5.4.4 Workforce Management

- 5.4.5 Learning and Development

- 5.4.6 Other Modules

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 India

- 5.5.4.3 Japan

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 United Arab Emirates

- 5.5.5.2 Saudi Arabia

- 5.5.5.3 Turkey

- 5.5.5.4 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Egypt

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Workday Inc.

- 6.4.2 Ultimate Kronos Group, Inc.

- 6.4.3 Ceridian HCM Holding Inc.

- 6.4.4 Automatic Data Processing, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Cornerstone OnDemand, Inc.

- 6.4.8 Bamboo HR LLC

- 6.4.9 Namely Inc.

- 6.4.10 Zoho Corporation Pvt. Ltd.

- 6.4.11 Ramco Systems Limited

- 6.4.12 PeopleStrategy, Inc.

- 6.4.13 Gusto, Inc.

- 6.4.14 TriNet Zenefits LLC

- 6.4.15 HiBob Ltd.

- 6.4.16 The Sage Group plc

- 6.4.17 Epicor Software Corporation

- 6.4.18 Unit4 N.V.

- 6.4.19 Infor (US), Inc.

- 6.4.20 Softworks Workforce Management Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment