|

시장보고서

상품코드

2065613

AI 네이티브 HCM 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)AI-Native HCM Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

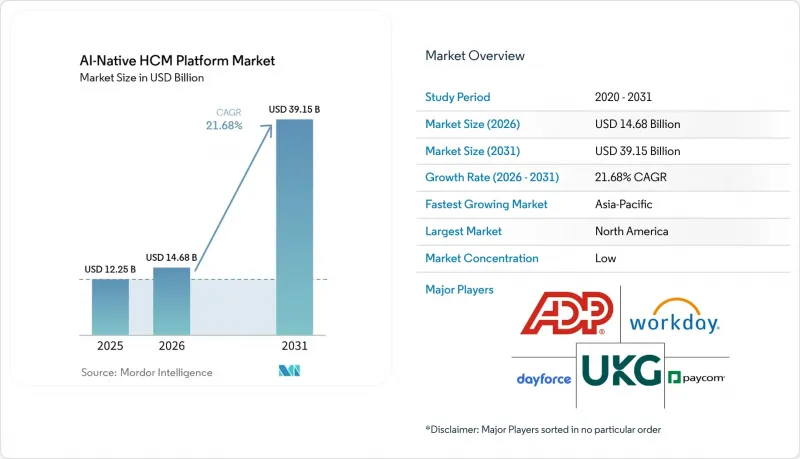

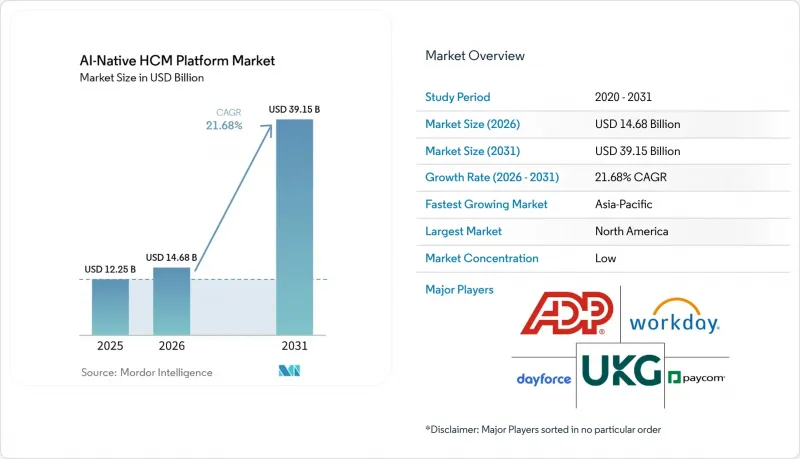

Mordor Intelligence에 의하면, AI 네이티브 HCM 플랫폼 시장 규모는 2025년 122억 5,000만 달러로 평가되었고, 2026년에는 146억 8,000만 달러로 추정되고, 2026-2031년 CAGR 21.68%로 성장을 지속할 전망이며, 2031년에는 391억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 구성 요소별(플랫폼 소프트웨어 및 서비스), 도입 모델별(클라우드, 온프레미스, 하이브리드 도입), 기업 규모별(대기업 및 중소기업), 용도별(인재 채용 등), 최종 사용자 산업별(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 AI 네이티브 HCM 플랫폼 시장 동향 및 인사이트

파일럿 단계에서 ‘시스템 오브 레코드’ 워크플로로 전환하는 AI 코파일럿

AI 네이티브 HCM 플랫폼 시장의 가장 큰 성장 요인은 AI 어시스턴트가 단편적인 이용 사례에서 벗어나 기존의 메뉴 기반 인사 업무 패턴을 대체하는 실제 업무 워크플로로 전환되고 있다는 점입니다. 2026년까지 구매자들은 코파일럿이 질문에 답할 수 있는지 여부만을 따지는 데 그치지 않고, 해당 도구가 명확한 권한과 감사 추적을 바탕으로 시스템 오브 레코드 내에서 다단계 작업을 완료할 수 있는지 여부를 묻게 될 것입니다. SHRM의 조사에 따르면, CHRO의 92%가 2026년에 AI의 추가적인 통합을 기대하고 있으며, 이는 2025년의 83%에서 증가한 수치입니다. 또한, HR 기능의 39%에서 이미 AI가 도입되어 있으며, 그 내역은 채용(27%), HR 기술 관리(21%), 학습 및 개발(17%)이 상위권을 차지하고 있습니다. 이러한 도입 방식은 AI를 일상 업무의 인프라로 전환하는 측면에서 인사 부서가 다른 많은 백오피스 기능보다 더 신속하게 움직이고 있음을 보여줍니다. Workday는 2026년 3월 Sana 세계 출시를 통해 이러한 방향성을 강화했으며, 2026년 5월에는 Sana Self-Service Agent를 Microsoft 365 Copilot에 통합함으로써 해당 모델을 확대했습니다. 이를 통해 직원들은 다른 용도으로 전환할 필요 없이, 평소의 작업 환경 내에서 인사 관련 업무를 수행할 수 있게 되었습니다. 따라서 AI 네이티브 HCM 플랫폼 시장은 단순히 제안하는 데 그치지 않고 실행 가능한 플랫폼으로 전환되고 있으며, 이러한 변화에 따라 계약 갱신 및 확장 결정 시의 기준은 꾸준히 높아지고 있습니다.

기술 기반의 인재 계획이 HCM 도입의 주요 판단 기준이 되어가고 있습니다.

AI 네이티브 HCM 플랫폼 시장에서 역량 기반 인재 계획이 구매 결정의 핵심 요소로 부상하고 있습니다. 이는 정적인 직무 아키텍처로는 기업 전체에서 진행되고 있는 역할 재설계의 속도에 더 이상 대응할 수 없기 때문입니다. 구매 담당자들은 역량을 추론하고, 지속적으로 업데이트되는 분류 체계를 유지하며, 인력 계획을 변화하는 비즈니스 수요와 연계할 수 있는 플랫폼을 더욱 중요하게 여기고 있습니다. 이러한 변화에 따라, 스킬 인텔리전스는 단순한 부가 모듈에서 채용, 사내 이동, 재배치 및 학습을 위한 아키텍처상의 제어 지점으로 그 위상이 변화하고 있습니다. 또한, 재무 책임자나 사업 부문 책임자들이 인재 역량의 가시화를 좁은 의미의 인사 프로세스 문제가 아닌 기업 계획의 틀의 일부로 인식하게 되면서, 구매 결정에 영향을 미치는 인물상도 변화하고 있습니다. 검증된 역량 수급 라이브러리, 더욱 향상된 재배치 로직, 그리고 인재 데이터와 계획 워크플로우 간의 긴밀한 연동을 입증할 수 있는 벤더들이 AI 네이티브 HCM 플랫폼 시장에서 주목받고 있습니다. 이에 따라 제품 로드맵은 내장형 추론 기능, 분류 체계 관리, 그리고 스킬 데이터를 인력 배치 조치로 전환하는 관리자용 도구로 발전해 나가고 있습니다.

기밀성이 높은 인사 데이터에 대한 거버넌스 및 설명 가능성 요건

인사 시스템은 보상, 성과, 휴가, 신상 정보, 직원의 행동 등과 관련된 극히 기밀성이 높은 기록을 다루기 때문에 거버넌스는 여전히 AI 네이티브 HCM 플랫폼 시장에서 가장 뚜렷한 제약 요인으로 남아 있습니다. 조달 팀은 현재 이러한 사항들을 나중에 해결해야 할 법적 세부 사항으로 취급하지 않고, 평가 초기 단계부터 설명 가능성, 문서화, 감사 가능성 및 인적 감독을 통한 관리를 요구하고 있습니다. 보고서에 따르면, AI를 도입하거나 시범 운영 중인 조직의 49%가 직원을 위한 AI 정책을 수립했으나, 그중 해당 정책을 ‘명확하고 미래 지향적’이라고 평가한 비율은 고작 25%에 그쳤습니다. 또한, AI 고용법이 시행되고 있는 미국 인구 상위 19개 주의 인사 담당자 중 57%는 그러한 법이 존재한다는 사실 자체를 알지 못했습니다. 유럽에서는 EU AI법 및 GDPR(EU 개인정보보호규정)이 고용 관련 AI에 대해 보다 엄격한 규제 체계를 규정하고 있으며, 이러한 시스템을 시장에 출시하기 전에 고위험 사용에 대한 관리 조치, 인적 감독, 그리고 데이터에 미치는 영향에 대한 고려 사항이 요구되고 있습니다. AI 네이티브 HCM 플랫폼 시장 역시 중대한 재무적 위험에 직면해 있습니다. 제99조에 따르면, 위반 시 최대 3,500만 유로의 벌금이 부과될 수 있으며, 2025년 IRS 연간 평균 환율을 기준으로 할 때 이는 약 3,790만 달러 또는 전 세계 연간 매출액의 7%에 해당합니다. 이러한 점이 일부 구매 결정을 지연시키고 있는 반면, 조기에 설명 가능성 및 결과 기록 기능을 플랫폼에 통합한 공급업체에게는 이점을 가져다주고 있습니다.

부문별 분석

플랫폼 소프트웨어는 AI 네이티브 HCM 플랫폼 시장에서 여전히 가장 큰 비중을 차지하고 있으며, 2025년 매출의 66.41%를 차지했습니다. 이는 구매자가 인사 기록, 인력 인텔리전스, 자동화 기능을 하나의 플랫폼에 통합할 때, 핵심 제품군이 여전히 지출의 대부분을 차지하고 있음을 의미합니다. 이러한 상황은 기존에는 서로 다른 도구들에 분산되어 있던 워크플로우를 통합하는 AI 기반 HCM 플랫폼 및 의사결정 엔진에 대한 수요를 반영하고 있습니다. 실무적인 관점에서 볼 때, 조직은 우선 인재 데이터, 프로세스 규칙, AI에 의한 조치를 통합할 수 있는 기반 시스템이 필요하기 때문에 소프트웨어가 여전히 기업 구매의 상당 부분을 차지하고 있습니다. 동시에, 인사 분야에서 AI가 기밀성이 높은 직원 기록이나 비즈니스상 중요한 업무 흐름과 관련되기 시작함에 따라, 구매자들은 소프트웨어 계층의 거버넌스 및 보안 기능을 더욱 중요하게 여기게 되었습니다. 그런 의미에서 플랫폼 소프트웨어는 2025년 AI 네이티브 HCM 플랫폼 시장 규모에서 여전히 핵심을 차지하고 있습니다.

한편, 서비스 분야는 2031년까지 연평균 성장률(CAGR) 23.12%로 확대될 것으로 예상되며, 이는 플랫폼 소프트웨어의 성장 속도를 웃도는 수준입니다. 이는 대규모 도입 시 실제로 발생할 수 있는 복잡성을 시사합니다. AI 네이티브 플랫폼은 깨끗한 그린필드 환경이 아닌 다양한 환경에 배포되고 있기 때문에 기업들은 구현 설계, 다국적 배포 지원, 규정 준수 관련 자문, 그리고 모델 거버넌스에 대한 지출을 늘리고 있습니다. 이러한 경향은 워크포스 인텔리전스 모델의 설정이나 인사, IT, 법무, 재무 부서 간에 걸쳐 책임 관리를 수행할 수 있는 역량을 갖춘 사내 팀이 없는 조직에서 특히 두드러집니다. 소프트웨어 시장 점유율과 서비스 성장률 사이에 나타나는 격차는 AI 네이티브 HCM 플랫폼 업계가 여전히 구축 단계에 있으며, 제품 기능과 마찬가지로 운영상의 변화도 매우 중요함을 시사합니다. 또한, 이는 소프트웨어 기능이 점차 통합되어 가는 상황에서도 강력한 서비스 생태계를 갖춘 벤더가 고객 가치를 지킬 수 있음을 의미합니다. AI 네이티브 HCM 플랫폼 시장에서 서비스는 더 이상 소프트웨어를 보완하는 지원 계층이 아니라, 도입 논리 그 자체의 일부가 되었습니다.

AI 네이티브 HCM 플랫폼 시장의 2025년 매출 중 클라우드 도입이 72.41%를 차지했으며, SaaS 우선 구매 행태가 핵심 HR 현대화의 주류 방향을 계속해서 주도하고 있음이 드러나고 있습니다. 클라우드가 여전히 기본적인 선택지로 자리 잡고 있는 이유는 기존의 온프레미스 환경에 비해 구매자에게 더 신속한 출시, 더 폭넓은 통합 옵션, 그리고 AI 기능에 대한 더 쉬운 접근성을 제공하기 때문입니다. 또한, 이는 공통 레코드 계층을 기반으로 셀프 서비스, 분석, 워크플로우 오케스트레이션을 지원할 수 있는 통합 제품군에 대한 광범위한 선호도와도 일치합니다. 클라우드에 대한 수요가 집중되고 있다는 사실은 AI 네이티브 HCM 플랫폼 시장 규모가 여전히 정기적인 업데이트와 지속적인 모델 개선을 목적으로 설계된 플랫폼에 의해 뒷받침되고 있음을 보여줍니다. 구매자들은 모든 환경에서 해당 관계를 로컬에서 재구축할 필요 없이 인사, 급여 및 인력 인텔리전스를 연동하는 가장 실용적인 방법으로 계속해서 클라우드를 인식하고 있습니다.

하이브리드 모델은 여전히 가장 빠르게 성장하고 있는 모델이며, 2031년까지 연평균 성장률(CAGR) 22.68%로 확대될 것으로 전망됩니다. 이는 실제 구매 행동이 단순한 ‘클라우드 퍼스트’라는 이야기가 시사하는 것보다 훨씬 더 다양하다는 것을 의미합니다. 규제가 엄격한 업계나 데이터 주권을 중시하는 시장에서는 예측 기간 내에 모든 급여, 신원 또는 직원 기록을 제3자 인프라로 이전할 수 없는 경우가 종종 있습니다. 또한 대기업의 경우, 프런트엔드 HCM 계층이 조기에 전환되더라도 급여 계산 엔진이나 관련 시스템의 교체를 완료하는 데 수년이 소요될 가능성이 있다는 현실적인 문제에 직면해 있습니다. 이에 따라, 로컬 데이터의 제약 사항을 해결하면서도 클라우드 기반의 AI 추론, 분석 및 사용자 경험을 제공할 수 있는 플랫폼에 대한 수요가 생겨나고 있습니다. 온프레미스 배포의 점유율은 감소 추세를 보이고 있지만, 직원 데이터 처리가 기술적 요인뿐만 아니라 법적 또는 제도적 제약에 의해 규정되는 고객의 경우, 여전히 중요한 위치를 차지하고 있습니다. 따라서 AI 네이티브 HCM 플랫폼 업계에서는 하이브리드 아키텍처를 일시적인 타협안이 아닌 의도적인 제품 전략으로 포지셔닝하는 벤더들이 계속해서 높은 평가를 받고 있습니다.

지역별 분석

북미는 2025년 매출의 40.12%를 차지했으며, AI 네이티브 HCM 플랫폼 시장에서 여전히 가장 큰 비중을 차지하는 지역으로 자리매김했습니다. 이 지역은 이미 AI 프로그램을 적극적으로 도입하고 있는 대기업들이 밀집해 있다는 점과, 평가 및 구매 주기를 신속하게 진행할 수 있는 성숙한 기업 소프트웨어 구매 환경의 혜택을 누렸습니다. 구체적으로, 북미가 2025년 AI 네이티브 HCM 플랫폼 시장 점유율의 40.12%를 차지한 것은 해당 지역의 구매자들이 클라우드 HCM 도입, AI 시범 운영, 그리고 다기능 플랫폼과의 통합 측면에서 다른 지역보다 앞서 있었기 때문입니다. 또한 2026년에는 해당 지역에서 경쟁 구도가 양극화되는 양상을 보였는데, 기존 공급업체들은 대기업의 계약 갱신에서 강세를 유지한 반면, 대응이 빠른 신생 기업들은 도입 기간 단축을 통해 중견기업 및 중소기업 시장에서 입지를 확대했습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 24.47%로 확대될 것으로 예상되며, AI 네이티브 HCM 플랫폼 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이 지역은 성숙한 유럽 및 미국 시장에서 자동화를 지연시키는 레거시 시스템이라는 걸림돌을 많은 구매자가 피할 수 있는 그린필드 방식의 클라우드 HCM 도입 경로라는 장점이 있습니다. 속도와 AI 통합을 중시하는 경영 모델에 대한 재평가가 일본, 한국, 호주, 동남아시아 전역에서 CHRO(최고인사책임자)의 우선순위를 재편하고 있습니다. 인도는 특히 중요한 시장입니다. APAC에서 탄생한 벤더가 순수한 국내 공급업체에 그치지 않고, AI 네이티브 HCM 기능을 해외로 수출하고 있기 때문입니다. 중국은 규모는 크지만 여전히 독자적인 시장으로서 중요하며, 현지 데이터 거주 요건과 정부의 규정 준수 요건이 플랫폼 설계에 영향을 미치고 있습니다. 한편, 호주, 한국 및 동남아시아 국가들에서는 디지털 전환(DX) 프로그램과 최신 인력 관리 시스템에 대한 고용주들 수요가 증가함에 따라 도입이 지속적으로 촉진되고 있습니다.

유럽은 독일, 영국, 프랑스를 필두로, AI 네이티브 HCM 플랫폼 시장에서 2025년 매출의 상당 부분을 차지했습니다. 해당 지역의 단기적인 구매 행태는 단순한 기능 비교라기보다는 공급업체가 EU의 틀에 기반한 급여 투명성 규정, AI 위험 분류 및 데이터 처리 의무에 얼마나 적절히 대응할 수 있는지에 따라 좌우되고 있습니다. 남미, 중동 및 아프리카는 도입 초기 단계에 있는 지역이지만, 기존의 데스크톱형 인사 시스템이 완전히 정착되지 않은 시장에서 모바일 우선이며 AI가 통합된 플랫폼이 세를 넓혀가고 있는 중요한 성장 지역으로 자리매김하고 있습니다. 브라질과 사우디아라비아는 각 하위 지역에서 핵심 시장으로서의 역할을 수행하고 있는 반면, 아프리카 전역에서는 다국적 기업들이 인재 관리 현대화 프로그램을 통해 1차 클라우드 기반 HCM 도입을 지속적으로 지원하고 있어, 나이지리아와 남아프리카공화국이 두드러지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSH 26.06.24According to Mordor Intelligence, the aI-Native hCM platform market size is expected to grow from USD 12.25 billion in 2025 to USD 14.68 billion in 2026 and is forecast to reach USD 39.15 billion by 2031 at 21.68% CAGR over 2026-2031.

This report is Segmented by Component (Platform Software, and Services), Deployment Model (Cloud, On-Premises, and Hybrid Deployment), Enterprise Size (Large Enterprises, and Small and Medium Enterprises), Application (Talent Acquisition, and More), End-User Industry (BFSI, Healthcare and Life Sciences, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global AI-Native HCM Platform Market Trends and Insights

Artificial Intelligence Copilots Moving From Pilot To System Of Record Workflows

The strongest growth force in the AI-Native HCM Platform Market is the shift of AI assistants from isolated use cases into production workflows that replace older menu-based HR interaction patterns. By 2026, buyers are no longer asking only whether copilots can answer questions; they are asking whether those tools can complete multistep tasks inside systems of record with clear permissions and audit trails. SHRM noted that 92% of CHROs expected further AI integration in 2026, up from 83% in 2025, and AI was already deployed in 39% of HR functions, led by recruiting at 27%, HR technology administration at 21%, and learning and development at 17%. That adoption pattern shows HR moving faster than many other back-office functions in turning AI into day-to-day operating infrastructure. Workday reinforced this direction in March 2026 with the global release of Sana, and then expanded the model in May 2026 by bringing Sana Self-Service Agent into Microsoft 365 Copilot, placing HR actions within an employee's normal work environment rather than requiring a switch back to a separate application. The AI-Native HCM Platform Market is therefore moving toward platforms that can execute, not just suggest, and that shift is steadily raising the bar for renewal and expansion decisions.

Skills-Based Workforce Planning Becoming A Core HCM Buying Criterion

Skills-based workforce planning has moved closer to the center of buying decisions in the AI-Native HCM Platform Market because static job architectures no longer support the pace of role redesign taking place across enterprises. Buyers are placing more emphasis on platforms that can infer skills, maintain living taxonomies, and connect workforce planning to changing business demand. That change is making skills intelligence less of a side module and more of an architectural control point for hiring, internal mobility, redeployment, and learning. It also changes who influences purchases, because finance leaders and business unit heads now view workforce capability visibility as part of enterprise planning discipline rather than a narrow HR process issue. Vendors that can show verified skills supply and demand libraries, better redeployment logic, and tighter links between workforce data and planning workflows are gaining more attention in the AI-Native HCM Platform Market. This is also pushing product roadmaps toward embedded inference, taxonomy management, and manager-facing tools that translate skills data into staffing actions.

Sensitive HR Data Governance And Explainability Requirements

Governance remains the clearest restraint on the AI Native HCM Platform Market because HR systems handle highly sensitive records tied to compensation, performance, leave, identity, and employee behavior. Procurement teams are now asking for explainability, documentation, auditability, and human oversight controls at the start of evaluation rather than treating them as legal details to resolve later. Reports show that 49% of organizations using or piloting AI had workforce AI policies, yet only 25% of that group described those policies as clear and future-proof, and 57% of HR professionals in the 19 most populous U.S. states with active AI employment laws were unaware that those laws existed. In Europe, the EU AI Act and the GDPR set a stricter regulatory framework for employment-related AI and require controls on high-risk uses, human oversight, and data impact considerations before those systems can be placed on the market. The AI Native HCM Platform Market also faces a significant financial risk threshold, as Article 99 allows penalties of up to EUR 35 million, which the 2025 IRS yearly average exchange rate reference places at approximately USD 37.9 million, or 7% of global annual turnover for non-compliance. This is slowing some purchase decisions, but it is also rewarding vendors that built explainability and outcome logging into their platforms earlier.

Other drivers and restraints analyzed in the detailed report include:

- Cloud HR Modernization And Suite Consolidation Favoring AI-Embedded Platforms

- Demand For Continuous Employee Self-Service And Manager Assistants

- Legacy Payroll And Identity Stacks Slowing End-To-End Automation

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Platform software remained the largest component in the AI-Native HCM Platform Market and held 66.41% of 2025 revenue, which means core suites still capture most spending when buyers consolidate HR records, workforce intelligence, and automation capabilities in one platform. That position reflects demand for AI core HCM platforms and decision engines that unify workflows previously spread across separate tools. In practical terms, software still anchors most enterprise purchasing because organizations first need the base system where people data, process rules, and AI actions can sit together. At the same time, buyers are placing greater weight on governance and security features within the software layer, as AI use in HR now touches sensitive employee records and business-critical workflows. In that sense, platform software continues to define the operating center of the AI-Native HCM Platform Market size in 2025.

Services, however, are projected to expand at a 23.12% CAGR through 2031, faster than platform software, which points to the real complexity of deployment at scale. Enterprises are spending more on implementation design, multi-country rollout support, compliance advisory, and model governance because AI-native platforms are being deployed across varied environments rather than in clean, greenfield settings. This pattern is especially visible in organizations that lack internal teams capable of configuring workforce intelligence models or managing cross-functional ownership between HR, IT, legal, and finance. The gap between software share and service growth suggests that the AI-Native HCM Platform Industry is still in a build-out phase, where operating change matters almost as much as product functionality. It also means that vendors with strong service ecosystems can protect account value even as software features converge. In the AI-Native HCM Platform Market, services are no longer a support layer around software; they are part of the adoption logic itself.

Cloud deployment accounted for 72.41% of 2025 revenue in the AI-Native HCM Platform Market, underscoring that SaaS-first buying behavior continues to define the mainstream direction of core HR modernization. Cloud remained the default because it offers buyers faster releases, broader integration options, and easier access to AI capabilities than older on-premises environments. It also aligns with the broader preference for unified suites that can support self-service, analytics, and workflow orchestration from a common record layer. The concentration of demand in cloud shows that the AI-Native HCM Platform Market size still rests on platforms designed for regular updates and continuous model improvement. Buyers continue to view the cloud as the most practical way to connect HR, payroll, and workforce intelligence without rebuilding those relationships locally in every environment.

Hybrid deployment is still the fastest-growing model and is projected to expand at a 22.68% CAGR through 2031, which means real buying behavior is more mixed than a simple cloud-first story would suggest. Regulated sectors and data-sovereign markets often cannot move every payroll, identity, or worker record into third-party infrastructure within the forecast window. Large enterprises also face the practical problem that payroll engines and adjacent systems may take years to replace, even when the front-end HCM layer moves earlier. This creates demand for platforms that can address local data constraints while still providing cloud-based AI inference, analytics, and user experience. On-premises deployment is losing share, but it remains important in accounts where worker data handling is governed by legal or institutional limits rather than by technology alone. The AI-Native HCM Platform Industry, therefore, continues to reward vendors that treat hybrid architecture as a deliberate product path rather than a temporary compromise.

Geography Analysis

North America held 40.12% of 2025 revenue and remained the largest regional contributor to the AI Native HCM Platform Market. The region benefited from a dense base of large enterprises already active in AI programs and from a mature enterprise software-buying environment that enabled faster evaluation and purchasing cycles. In practical terms, North America accounted for 40.12% of the AI Native HCM Platform Market share in 2025 because buyers there were further along in cloud HCM adoption, AI experimentation, and multi-function platform consolidation. The region also showed a split competitive pattern in 2026, with incumbents retaining strength in large enterprise renewals while faster-moving challengers gained traction in mid-market and SME accounts through shorter deployment windows.

Asia Pacific is projected to expand at a 24.47% CAGR through 2031, making it the fastest-growing regional bloc in the AI Native HCM Platform Market. The region benefits from greenfield cloud HCM deployment paths that let many buyers bypass the legacy drag that slows automation in mature Western markets. CEO reassessment of operating models for speed and AI integration is reshaping CHRO priorities across Japan, South Korea, Australia, and Southeast Asia. India is especially important because vendors born in APAC are exporting AI native HCM capabilities rather than remaining purely domestic suppliers. China remains important as a large but distinct market where local data residency and government compliance requirements shape platform design, while Australia, South Korea, and Southeast Asian economies continue to support adoption through digital transformation programs and rising employer demand for modern workforce systems.

Europe accounted for meaningful 2025 revenue in the AI Native HCM Platform Market, led by Germany, the United Kingdom, and France. The region's near-term buying behavior is being shaped less by feature comparison alone and more by how well vendors can handle pay transparency rules, AI risk classification, and data processing obligations under the EU framework. South America, the Middle East, and Africa are earlier-stage regions, but they remain important growth territories where mobile-first and AI-embedded platforms are gaining traction in markets that did not fully institutionalize older desktop HR stacks. Brazil and Saudi Arabia serve as anchor markets in their respective sub-regions, while Nigeria and South Africa stand out across Africa as multinational employers continue to support first-wave cloud HCM adoption through workforce modernization programs.

- Workday, Inc.

- Dayforce, Inc.

- UKG Inc.

- ADP, Inc.

- Paycom Software, Inc.

- Paylocity Holding Corporation

- Paychex, Inc.

- Paycor HCM, Inc.

- BambooHR LLC

- Personio SE and Co. KG

- HiBob Ltd.

- Darwinbox Digital Solutions Private Limited

- Rippling, Inc.

- Deel Inc.

- Remote Technology, Inc.

- Factorial HR, S.L.

- Employment Hero Pty Ltd

- PayFit SAS

- Humaans Ltd

- ZingHR India Private Limited

- Namely, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Artificial Intelligence Copilots Moving From Pilot to System of Record Workflows

- 4.2.2 Skills-Based Workforce Planning Becoming a Core HCM Buying Criterion

- 4.2.3 Cloud HR Modernization and Suite Consolidation Favoring AI-Embedded Platforms

- 4.2.4 Demand for Continuous Employee Self-Service and Manager Assistants

- 4.2.5 Need to Harmonize Fragmented Skills Taxonomies Across Enterprises

- 4.2.6 Real-Time Employment Data and Worker Record Modernization Improving AI Context

- 4.3 Market Restraints

- 4.3.1 Sensitive HR Data Governance and Explainability Requirements

- 4.3.2 Legacy Payroll and Identity Stacks Slowing End-to-End Automation

- 4.3.3 EU AI Act and Works Council Obligations Extending Sales Cycles

- 4.3.4 Interoperability Gaps Across Skills Ontologies and Labor Data Standards

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Bargaining Power of Suppliers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Component

- 5.1.1 Platform Software

- 5.1.1.1 AI Core HCM Platforms

- 5.1.1.2 AI Copilots and Conversational HR Assistants

- 5.1.1.3 Workforce Intelligence and Decision Engines

- 5.1.1.4 Skills Intelligence Platforms

- 5.1.1.5 Autonomous HR Workflow Automation Platforms

- 5.1.1.6 AI Governance, Security and Compliance Platforms

- 5.1.2 Services

- 5.1.1 Platform Software

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premises

- 5.2.3 Hybrid Deployment

- 5.3 By End User Enterprise Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By Application

- 5.4.1 Talent Acquisition, Recruiting and Candidate Intelligence

- 5.4.2 Workforce Administration and Employee Intelligence

- 5.4.3 Payroll, Compensation and Benefits Intelligence

- 5.4.4 Workforce Planning, Analytics and Decision Intelligence

- 5.4.5 Learning, Skills Intelligence and Internal Mobility

- 5.4.6 Employee Experience, HR Service Delivery and AI Assistants

- 5.4.7 Autonomous HR Workflow Automation

- 5.4.8 AI Governance, Compliance and Workforce Risk Management

- 5.5 By End-user Industry

- 5.5.1 BFSI

- 5.5.2 Healthcare and Life Sciences

- 5.5.3 Information Technology and Telecom

- 5.5.4 Retail and E-commerce

- 5.5.5 Industrial Manufacturing

- 5.5.6 Government and Public Sector

- 5.5.7 Other End-user Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 Germany

- 5.6.3.2 United Kingdom

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Netherlands

- 5.6.3.8 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia and New Zealand

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Workday, Inc.

- 6.4.2 Dayforce, Inc.

- 6.4.3 UKG Inc.

- 6.4.4 ADP, Inc.

- 6.4.5 Paycom Software, Inc.

- 6.4.6 Paylocity Holding Corporation

- 6.4.7 Paychex, Inc.

- 6.4.8 Paycor HCM, Inc.

- 6.4.9 BambooHR LLC

- 6.4.10 Personio SE and Co. KG

- 6.4.11 HiBob Ltd.

- 6.4.12 Darwinbox Digital Solutions Private Limited

- 6.4.13 Rippling, Inc.

- 6.4.14 Deel Inc.

- 6.4.15 Remote Technology, Inc.

- 6.4.16 Factorial HR, S.L.

- 6.4.17 Employment Hero Pty Ltd

- 6.4.18 PayFit SAS

- 6.4.19 Humaans Ltd

- 6.4.20 ZingHR India Private Limited

- 6.4.21 Namely, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment