|

시장보고서

상품코드

2063958

GPU 침지 냉각 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)GPU Immersion Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

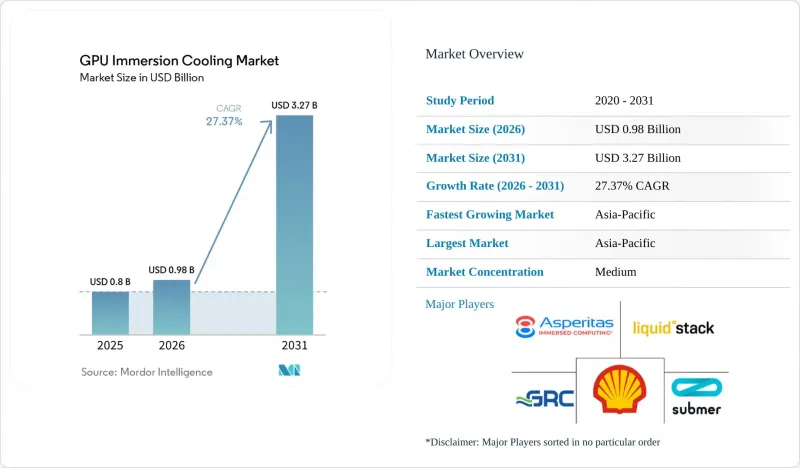

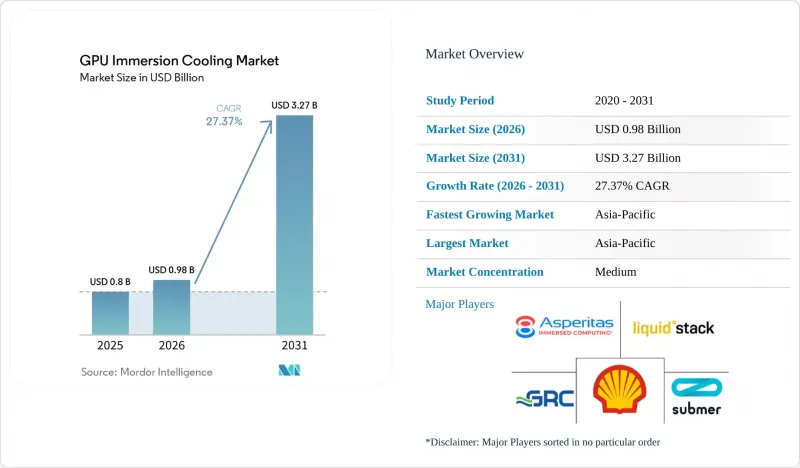

Mordor Intelligence에 의하면, GPU 침지 냉각 시장 규모는 2025년 8억 달러로 평가되었고, 2026년에는 9억 8,000만 달러로 추정되고, 2031년까지 32억 7,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 27.37%로 성장할 전망입니다.

본 보고서는 침지형별(단상 침지 냉각 및 2상 침지 냉각), 용액형별(침지 냉각 탱크 및 시스템, 유전체 유체, 침지 냉각 최적화 GPU 서버 시스템), 적용 분야별(하이퍼스케일 및 클라우드, 엔터프라이즈, 기타), GPU 전력 밀도별(300W 미만, 300W-700W, 700W 이상), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 GPU 침지 냉각 시장 동향 및 인사이트

AI 훈련 시설의 랙 전력 밀도 증가

NVIDIA의 내부 로드맵에 따르면, 현재 132kW를 공급하고 있는 이 회사의 GB200 NVL72 랙은 2028년까지 랙당 240-800kW 범위로 대폭 확장될 것으로 예측됩니다. 그러나 이러한 높은 부하에 대응하기 위해서는 대형 플레넘이나 보조 핸들러 도입 등, 공조 인프라를 대폭 강화해야 합니다. 이러한 구성 요소들은 시설의 전력 소비량 중 상당 부분을 차지하며, 전체 에너지 사용량의 약 40-50%를 차지할 수 있습니다. 반면, 액체 침지 냉각 솔루션은 에너지 효율이 더 높은 대안으로, 전력 사용 효율(PUE)을 1.02라는 낮은 수준으로 유지할 수 있게 해줍니다. 이 접근 방식은 10메가와트 용량의 시설에서 연간 에너지 소비량을 최대 40%까지 줄일 수 있는 잠재력을 지니고 있어, 고성능 컴퓨팅 환경에 이를 도입해야 할 강력한 근거가 되고 있습니다.

데이터센터의 지속가능성에 관한 규제 강화

2026년부터 유럽 에너지 효율 지침에 따라 에너지 소비량이 1메가와트를 초과하는 시설에서는 열 재사용이 의무화됩니다. 이 규제로 인해 유럽의 도시 지역에서 액체 냉각 시스템이 사실상 표준 솔루션으로 자리 잡게 될 것입니다. 독일에서는 해당 지침에 따라 최소 30%의 열 회수가 의무화되어 있으며, 에너지 효율이 높은 방식으로의 전환이 더욱 강조되고 있습니다. 마찬가지로, 워싱턴주는 2027년까지 전력 사용 효율(PUE)을 1.2 미만으로 낮추겠다는 엄격한 목표를 설정했으며, 중국에서는 2026년까지 신설되는 하이퍼스케일 데이터센터에 대해 PUE를 1.25 미만으로 유지하도록 의무화하는 규제를 도입했습니다. 이러한 구속력 있는 규제 체계가 침지 냉각 기술의 광범위한 도입을 촉진하고 있으며, 전 세계 에너지 효율 기준에 큰 변화를 가져오고 있습니다.

침지 냉각 시스템 분야의 현장 서비스 기술 부족

액침 냉각 방식에서는 기술자가 절연액의 화학적 특성을 관리하고, 용존 가스 분석을 모니터링하며, 액체로 채워진 케이스 내에서 서버의 핫스왑 유지보수를 수행해야 하지만, 이러한 역량은 기존 데이터센터 교육 과정에는 포함되어 있지 않습니다. 기기 제조업체들은 이에 대응하여 인증 프로그램을 시작했습니다. Green Revolution Cooling사는 2022년에 ‘ElectroSafe Partner Program’을 도입하여 2025년까지 전 세계에서 200명 이상의 기술자를 인증했지만, 그럼에도 불구하고 예상되는 도입 계획을 뒷받침하기에는 부족합니다. 이러한 기술 격차는 데이터센터 인프라가 급속히 확장되고 있는 반면 기술 교육 인프라가 이를 따라가지 못하고 있는 신흥 시장에서 가장 심각합니다. 인도 전자·정보기술부는 업계 단체와 협력하여 침지 냉각 교육 모듈을 개발하고 있지만, 본격적인 도입은 2027년까지는 이루어지지 않을 것으로 보입니다.

부문별 분석

2025년, 단상 기술은 GPU(그래픽 처리 장치)의 침지 냉각 시장 점유율의 79.22%를 차지했으며, 운영이 간편하고 유체 비용이 저렴하다는 점에서 지지를 받고 있습니다. 이 기술은 기존의 칠러와 통합이 가능하며, 기업의 기존 설비에 사후 설치하기에 적합합니다. 2상 침지 냉각은 잠열 비행을 이용하며, 랙당 150kW 이상을 처리할 수 있어 연평균 성장률(CAGR) 27.54%가 예상됩니다. 이는 단상 방식이 열적 한계에 도달하는 최첨단 AI 클러스터에 가장 적합합니다.

마이크로소프트의 GB300 클러스터와 같은 하이퍼스케일 시범 사례에서는 2상식 랙이 펌프를 제거한 상태에서 PUE 1.06으로 가동되고 있음이 확인되었습니다. 과제로는 불소계 유체의 높은 가격과 다가오는 PFAS 규제를 들 수 있습니다. 그럼에도 불구하고, 랙의 전력 밀도 증가와 능동형 펌프 구동의 제거로 인해 전력 비용이 높은 지역에서는 2상 방식의 도입이 급증할 것으로 예측됩니다.

2025년에는 탱크 및 외부 시스템이 GPU 침지 냉각 시장의 총 매출의 56.45%를 차지한 것으로 평가되었고, 상용 서버 수용에 특화되어 설계된 모듈형 포드에 대한 선호도가 높아지고 있음이 부각되었습니다. 이러한 추세는 데이터센터 인프라 분야에서 유연하고 확장 가능한 솔루션에 대한 수요가 증가하고 있음을 반영하고 있습니다. 유전성 유체는 안정적이고 지속적인 수익원이 되고 있지만, 시장 전체 가치에서 차지하는 비중은 여전히 비교적 작은 임베디드니다. OEM 각사가 공장 출하 시 밀봉형 섀시를 채택하고 있는 것을 배경으로, 액체 침지 냉각에 최적화된 그래픽 처리 장치(GPU) 서버는 27.66%라는 상당한 연평균 성장률(CAGR)을 달성할 것으로 전망됩니다. 이 섀시는 타사 탱크를 사용할 필요가 없게 하여 설치 과정을 효율화할 뿐만 아니라, 이미 설치된 시스템에서 10-15%의 비용 절감을 실현합니다.

Supermicro의 HGX B300과 Dell, HPE, Lenovo의 동급 제품에는 커패시터 및 드립리스 퀵 디스커넥트와 같은 첨단 기능이 통합되어 있습니다. 그러나 이러한 혁신은 독자적인 액체 냉각 생태계의 구축으로 이어져 상호 운용성을 제한할 가능성이 있습니다. 예측 유지보수 분석 및 열 재이용 기능을 솔루션에 통합한 벤더들은 경쟁 우위를 확보해 나가고 있습니다. 이러한 기능 강화는 수직 통합으로 향하는 시장의 흐름과 부합하며, 경쟁이 치열해지는 환경에서 기업이 차별화를 꾀할 수 있게 해줍니다.

지역별 분석

아시아태평양은 2025년에 67.34%의 점유율로 그래픽 처리 장치(GPU) 수냉 시장을 주도한 것으로 평가되었으며, 2031년까지 연평균 성장률(CAGR) 28.05%를 기록할 전망입니다. 중국이 2026년까지 PUE 1.25 미만을의무화함에 따라, 10메가와트를 초과하는 신규 건설 시설에서는 액체 냉각 방식의 도입이 필수로 되었습니다. 일본의 ‘그린 트랜스포메이션 리그’는 수냉 방식에 대해 세액 공제를 제공하는 반면, 싱가포르의 ‘그린마크’는 증발수를 제거할 경우 보너스 점수를 부여하고 있습니다. 인도에서는 2027년 이후 도입될 것으로 예상되는 수냉식 인센티브를 포함한 별점 평가 제도를 마련 중입니다.

북미는 미국의 하이퍼스케일러를 주축으로 2위를 차지하고 있습니다. 워싱턴주의 PUE 1.2 미만 법안과 캘리포니아주의 개정판 ‘타이틀 24’ 에너지 규정은 신규 프로젝트에서 수냉식 시스템의 도입을 촉진하고 있습니다. 마이크로소프트의 132kW 랙은 PUE 1.06을 달성하며 상업적 실현 가능성을 입증했습니다. 캐나다와 멕시코도 이에 뒤이어 시범 도입을 추진하고 있습니다.

유럽의 동향은 법정 폐열 재활용 의무와 톤당 60-90유로(70-105달러)의 탄소 비용에 의해 형성되고 있습니다. 독일은 폐열 회수율 30%를 의무화하고 있으며, 영국은 PUE 공개 의무화에 대해 협의 중이고, 프랑스는 지방자치단체의 열 통합에 자금을 지원하고 있습니다. 남미, 중동 및 아프리카은 아직 발전 단계에 있지만, 높은 전력 가격, 물 부족, 국가 주도의 AI 프로그램이 추진력으로 작용하고 있으며, 브라질에서는 요금 우대 방안이 검토되고 있고, UAE에서는 국가 AI 전략의 일환으로 침지 냉각 방식의 시범 도입이 진행되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the gPU immersion cooling market size is expected to increase from USD 0.80 billion in 2025 to USD 0.98 billion in 2026 and reach USD 3.27 billion by 2031, growing at a CAGR of 27.37% over 2026-2031.

This report is Segmented by Immersion Type (Single-Phase Immersion Cooling, and Two-Phase Immersion Cooling), Solution Type (Immersion Cooling Tanks/Systems, Dielectric Fluids, and Immersion-Optimized GPU Server Systems), Deployment (Hyperscale/Cloud, Enterprise, and More), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global GPU Immersion Cooling Market Trends and Insights

Increasing Rack Power Density In AI Training Facilities

NVIDIA's internal roadmaps indicate that its GB200 NVL72 rack, which currently delivers 132 kilowatts, is expected to scale up significantly to a range of 240-800 kilowatts per rack by 2028. However, supporting these higher loads requires substantial enhancements to air infrastructure, including the implementation of oversized plenums and auxiliary handlers. These components can consume a considerable portion of a facility's power, accounting for approximately 40-50% of total energy usage. In contrast, immersion cooling solutions offer a more energy-efficient alternative, enabling the maintenance of Power Usage Effectiveness (PUE) values as low as 1.02. This approach has the potential to reduce annual energy consumption by up to 40% for facilities with a 10-megawatt capacity, presenting a compelling case for its adoption in high-performance computing environments.

Accelerated Data-Center Sustainability Mandates

Beginning in 2026, the European Energy Efficiency Directive will require the reuse of heat for sites with energy consumption exceeding 1 megawatt. This regulation effectively establishes liquid cooling systems as the default solution in urban areas across Europe. In Germany, the directive mandates a minimum of 30% heat recovery, further emphasizing the shift toward energy-efficient practices. Similarly, Washington state has set a stringent target of achieving a Power Usage Effectiveness (PUE) of less than 1.2 by 2027, while China has introduced a regulation requiring new hyperscale data center builds to meet a PUE threshold of below 1.25 by 2026. These binding regulatory frameworks are driving the widespread adoption of immersion cooling technologies, marking a significant transformation in energy efficiency standards globally.

Limited Field Service Skill Sets For Immersion Systems

Immersion cooling requires technicians to manage dielectric fluid chemistry, monitor dissolved-gas analysis, and perform hot-swap server maintenance within liquid-filled enclosures, competencies absent from traditional data center training curricula. Equipment manufacturers are responding by launching certification programs; Green Revolution Cooling introduced its ElectroSafe Partner Program in 2022, certifying over 200 technicians globally by 2025, yet this remains insufficient to support the projected deployment pipeline. The skill gap is most acute in emerging markets, where data center infrastructure is expanding rapidly but technical education infrastructure lags. India's Ministry of Electronics and Information Technology has partnered with industry associations to develop immersion-cooling training modules, though widespread deployment is not expected until 2027.

Other drivers and restraints analyzed in the detailed report include:

- Water Scarcity Driving Liquid-Free Cooling Adoption

- Declining Cost Curve Of Synthetic Dielectric Fluids

- Long Qualification Cycles For Tier-1 Cloud Providers

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase technology carried 79.22% of the GPU (Graphics Processing Unit) immersion cooling market share in 2025, favored for operational simplicity and lower fluid cost. It integrates with existing chillers and suits enterprise retrofits. Two-phase immersion delivers latent-heat boiling that handles >150 kilowatts per rack and is projected for a 27.54% CAGR, ideal for frontier AI clusters where single-phase approaches thermal ceilings.

Hyperscale pilots, such as Microsoft's GB300 cluster, show two-phase racks operating at 1.06 PUE while eliminating pumps. The trade-off remains the high price of fluorinated fluids and looming PFAS regulations. Even so, rising rack power density and the elimination of active pumping are expected to pull two-phase adoption sharply higher in high-electricity jurisdictions.

In 2025, tanks and external systems accounted for 56.45% of total revenue of the GPU immersion cooling market, highlighting the growing preference for modular pods specifically designed to accommodate off-the-shelf servers. This trend reflects the increasing demand for flexible and scalable solutions in data center infrastructure. While dielectric fluids contribute to a steady and recurring revenue stream, their share of the overall value remains comparatively smaller. Immersion-optimized Graphics Processing Unit servers are projected to achieve a significant 27.66% CAGR, driven by the adoption of factory-sealed chassis by OEMs. These chassis eliminate the need for third-party tanks, streamlining the installation process and delivering cost savings of 10-15% on installed systems.

Supermicro's HGX B300, along with equivalent offerings from Dell, HPE, and Lenovo, integrates advanced features such as condensers and drip-less quick disconnects. However, these innovations result in the establishment of proprietary fluid ecosystems, which may limit interoperability. Vendors that incorporate predictive maintenance analytics and heat-reuse integration into their solutions are gaining a competitive edge. These enhancements align with the market's shift toward vertical integration, enabling companies to differentiate themselves in an increasingly competitive landscape.

Geography Analysis

Asia-Pacific led the Graphics Processing Unit immersion cooling market with 67.34% share in 2025 and will likely post a 28.05% CAGR to 2031. China's mandate for sub-1.25 PUE by 2026 forces liquid adoption for new builds above 10 megawatts. Japan's Green Transformation League grants tax credits for liquid cooling, while Singapore's Green Mark adds bonus points for eliminating evaporative water. India is drafting star-ratings that include immersion incentives expected post-2027.

North America ranks second, anchored by U.S. hyperscalers. Washington state's sub-1.2 PUE law and California's updated Title 24 energy code encourage immersion in new projects. Microsoft's 132-kilowatt racks reached 1.06 PUE, proving commercial viability; Canada and Mexico follow with pilot deployments.

Europe's trajectory is shaped by statutory heat-reuse and carbon costs of EUR 60-90 (USD 70-105) per metric ton. Germany demands 30% waste-heat capture, the U.K. is consulting on mandatory PUE disclosure, and France funds municipal heat integrations. South America and the Middle East and Africa are nascent but motivated by high electricity prices, water scarcity, and sovereign AI programs, with Brazil exploring tariff incentives and the UAE piloting immersion for its national AI strategy.

- Submer Technologies SL

- Green Revolution Cooling Inc.

- LiquidStack Inc.

- Asperitas B.V.

- Midas Immersion Cooling

- Engineered Fluids LLC

- Shell plc (Immersion Fluids)

- ZutaCore

- Hypertec Immersion Cooling

- Fujitsu Limited

- Dell Technologies Inc. (OEM Immersion-Ready Servers)

- Lenovo Group Limited

- Hewlett Packard Enterprise Company

- NVIDIA Corporation (Reference Designs)

- Super Micro Computer Inc.

- Gigabyte Technology Co., Ltd.

- Wiwynn Corporation

- Allied Control Ltd.

- DCX - The Liquid Cooling Company

- ExaScaler Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Increasing Rack Power Density in AI Training Facilities

- 4.2.2 Accelerated Data-Center Sustainability Mandates

- 4.2.3 Water Scarcity Driving Liquid-Free Cooling Adoption

- 4.2.4 Declining Cost Curve of Synthetic Dielectric Fluids

- 4.2.5 OEM Release of Immersion-Ready GPU Reference Designs

- 4.2.6 Carbon-Pricing Policies Elevating TCO Gap vs. Air Cooling

- 4.3 Market Restraints

- 4.3.1 Limited Field Service Skill Sets for Immersion Systems

- 4.3.2 Long Qualification Cycles for Tier-1 Cloud Providers

- 4.3.3 Regulatory Ambiguity Around New PFAS-Free Coolants

- 4.3.4 High Up-Front CAPEX for Retro-Fit Deployments

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Immersion Type

- 5.1.1 Single-Phase Immersion Cooling

- 5.1.2 Two-Phase Immersion Cooling

- 5.2 By Solution Type

- 5.2.1 Immersion Cooling Tanks / Systems

- 5.2.2 Dielectric Fluids

- 5.2.3 Immersion-Optimized GPU Server Systems

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 Europe

- 5.5.2.1 Germany

- 5.5.2.2 United Kingdom

- 5.5.2.3 France

- 5.5.2.4 Italy

- 5.5.2.5 Rest of Europe

- 5.5.3 Asia-Pacific

- 5.5.3.1 China

- 5.5.3.2 Japan

- 5.5.3.3 South Korea

- 5.5.3.4 India

- 5.5.3.5 Southeast Asia

- 5.5.3.6 Rest of Asia-Pacific

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Submer Technologies SL

- 6.4.2 Green Revolution Cooling Inc.

- 6.4.3 LiquidStack Inc.

- 6.4.4 Asperitas B.V.

- 6.4.5 Midas Immersion Cooling

- 6.4.6 Engineered Fluids LLC

- 6.4.7 Shell plc (Immersion Fluids)

- 6.4.8 ZutaCore

- 6.4.9 Hypertec Immersion Cooling

- 6.4.10 Fujitsu Limited

- 6.4.11 Dell Technologies Inc. (OEM Immersion-Ready Servers)

- 6.4.12 Lenovo Group Limited

- 6.4.13 Hewlett Packard Enterprise Company

- 6.4.14 NVIDIA Corporation (Reference Designs)

- 6.4.15 Super Micro Computer Inc.

- 6.4.16 Gigabyte Technology Co., Ltd.

- 6.4.17 Wiwynn Corporation

- 6.4.18 Allied Control Ltd.

- 6.4.19 DCX - The Liquid Cooling Company

- 6.4.20 ExaScaler Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment