|

시장보고서

상품코드

2064509

다양성, 형평성 및 포용성(DEI) 분석 플랫폼 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Diversity, Equity And Inclusion (DEI) Analytics Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

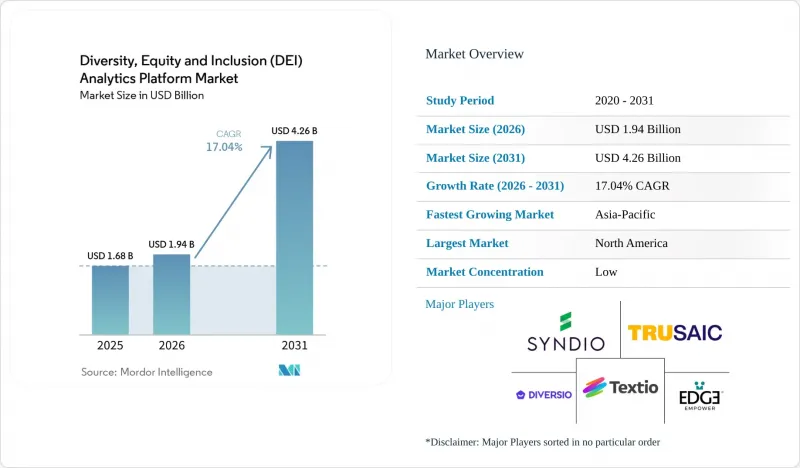

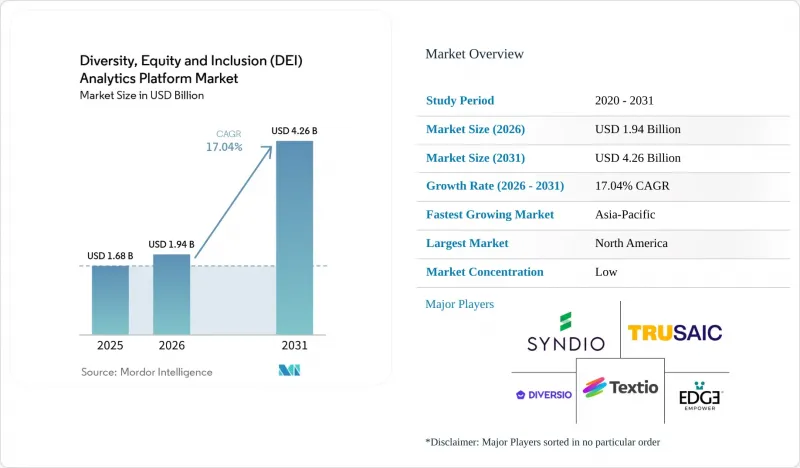

Mordor Intelligence에 의하면, 다양성, 형평성 및 포용성(DEI) 분석 플랫폼 시장 규모는 2025년에 16억 8,000만 달러로 평가되었습니다. 2026년에 19억 4,000만 달러에서 2031년까지 42억 6,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 성장률(CAGR) 17.04%를 나타낼 것으로 전망됩니다.

본 보고서는 도입 형태(클라우드 기반, On-Premise형, 하이브리드형), 기업 규모(대기업 등), 용도(임금 격차 및 보상 분석 등), 최종 사용자 산업 분야(은행, 금융서비스 및 보험(BFSI), 헬스케어 및 생명과학, 정보기술 및 통신 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 다양성, 형평성 및 포용성(DEI) 분석 플랫폼 시장 동향 및 인사이트

임금 투명성 관련 규정 준수 기한이 수요를 가속화

임금 투명성은 단순한 좁은 범위의 정책 과제에서 여러 거점에 직원을 두고 있는 고용주에게 있어 광범위한 업무 요건으로 변화하고 있습니다. EU의 임금 투명성 지침은 회원국들에게 2026년까지 새로운 규정을 국내법에 반영할 것을 의무화하고 있으며, 이에 따라 사업체 및 직급 수준을 아우르는 일관된 임금 격차 기록을 작성할 수 있는 도구의 가치가 높아지고 있습니다. 특정 거점에서 더 엄격한 공시 규정이 도입되면, 많은 고용주들은 그 기준을 전사적인 내부 기준으로 삼게 됩니다. 왜냐하면, 거점마다 서로 다른 임금 산정 방식을 적용하는 것은 법적 및 관리상의 위험을 초래하기 때문입니다. 이러한 변화에 따라 분석 도구의 도입은 컴플라이언스 팀을 넘어 보상 계획, 직무 구조, 그리고 경영진의 검토 주기까지 확대되고 있습니다. DEI 분석 플랫폼 시장에서는 감사 가능한 임금 워크플로우를 갖춘 공급업체가 우위를 점하고 있습니다. 왜냐하면 고용주가 필요로 하는 것은 단순한 요약 대시보드가 아니라, 타당성을 입증할 수 있는 설명과 추적 가능한 기록이기 때문입니다.

인공지능을 활용한 인재 관련 의사결정으로 인해 편향 감시의 필요성이 커지고 있습니다.

현재 AI 도구는 채용, 평가, 승진, 보상 결정에 활용되고 있으며, 편향의 위험은 기존의 채용 소프트웨어의 범위를 훨씬 넘어 확산되고 있습니다. 뉴욕시 지방법 제144호에 따르면, 자동화된 채용 결정 도구에 대한 연례 편향 감사가 이미 의무화되어 있으며, 2025년 12월 뉴욕주 감사관이 실시한 조사 결과, 독립적인 감사 결과와 공식적인 집행 결과 사이에 명백한 괴리가 있는 것으로 나타났습니다. 유럽 차원에서는 고용 관련 AI 시스템이 AI법에 따라 고위험 범주로 분류되어 있으며, 도입 일정이 정책 검토 중임에도 불구하고 인력에 관한 의사결정은 엄격한 규정 준수 감시의 대상이 되고 있습니다. 이는 급여나 채용 결정이 확정되기 전에, 자동화된 추천 사항이 어떻게 생성되고, 테스트되며, 사람에 의해 검토되었는지에 대한 기록을 구매자들이 점점 더 필요로 하고 있음을 의미합니다. 다양성, 형평성 및 포용성(DEI) 분석 플랫폼 시장에서는 수요가 전문 DEI 팀에서 핵심 인적 자본 워크플로우에 AI를 활용하는 모든 조직으로 확대되고 있습니다.

민감한 직원 데이터의 개인정보 보호 및 보안 위험

DEI 분석은 많은 법역에서 민감한 개인 데이터로 취급되는 인구통계학적 항목에 의존하고 있으며, 이로 인해 고용주가 수집할 수 있는 정보와 그 활용 방법은 즉시 제한을 받게 됩니다. 2025년 기사에서는 EU AI법 제10조 제5항이 엄격한 규정 준수 체계 내에서만 편향 완화를 목적으로 한 민감 데이터의 사용을 허용하고 있다고 지적했습니다. 그러나 많은 중견 기업에서는 여전히 그러한 체계가 마련되어 있지 않습니다. 또한, 국경을 넘어 사업을 전개하는 고용주는 또 다른 과제에 직면합니다. 미국의 자진 신고 프로그램에서 일반적으로 적용되는 데이터 처리 관행이 다른 지역에서는 더 제한적일 가능성이 있습니다. 그 결과, 많은 분석 팀은 불완전한 데이터 세트나 임의로 제공된 데이터 세트를 다룰 수밖에 없게 되어, 통계적 신뢰성이 떨어지고, 일부 보고서를 감사에 견딜 수 있는 증거로 취급하기 어려워집니다. 다양성, 형평성 및 포용성(DEI) 분석 플랫폼 시장에서 이 문제는 법적 검토, 사회적 책임, 그리고 직원들의 민감도가 가장 높은 분야에서 도입을 가장 크게 지연시키고 있습니다.

부문별 분석

2025년, 다양성·형평성·포용성(DEI) 분석 플랫폼 시장 점유율에서 클라우드 기반 도입이 68.73%를 차지하며, 분산된 인사 시스템 전반에 걸쳐 신속한 보고서 작성이 필요한 조직에게 명확한 운영 모델로 자리 잡았습니다. 이러한 장점은 도입의 용이성, 일원화된 업데이트, 그리고 급여 규정이 급격히 변경되었을 때 여러 관할 구역에 걸친 보고서 작성에 대한 뛰어난 대응 능력에서 비롯됩니다. 또한, 클라우드 도구는 긴 사내 출시 주기를 기다릴 필요 없이 보상, 채용 및 구성 비율 데이터를 연동하는 데에도 도움이 됩니다. DEI 분석은 매년 수동으로 데이터를 추출하는 방식이 아니라, 데이터가 지속적으로 이동할 때 가장 큰 효과를 발휘하므로, 이는 중요한 점입니다. DEI 분석 플랫폼 업계에서 규정 준수 대응을 신속히 처리하고 대시보드에 대한 광범위한 접근을 원하는 기업들에게 클라우드는 여전히 가장 일반적인 선택지로 자리 잡고 있습니다.

하이브리드 모델은 2031년까지 연평균 성장률(CAGR) 18.73%로 확대될 것으로 예상되며, 다국적 기업들이 속도와 데이터 소재지 관리 간의 균형을 모색함에 따라 이 모델을 위한 다양성, 형평성 및 포용성(DEI) 분석 플랫폼 시장도 성장하고 있습니다. 이 패턴은 식별 가능한 인구통계 데이터를 사내 환경에 보관하면서, 제한된 분석 워크로드만 클라우드로 전송하는 조직에 적합합니다. SAP SuccessFactors는 2026년 4월 릴리스를 통해 EU 임금 투명성 지침을 준수하는 임금 격차 분석 기능을 추가했습니다. 이는 주요 HCM 공급업체들이 이러한 기능을 외부 도구에 전적으로 맡기는 대신, 자사의 클라우드 제품군에 통합하고 있음을 보여줍니다. 따라서, 신규 도입 사례의 상당수가 클라우드 또는 하이브리드 모델을 중심으로 이루어지고 있음에도 불구하고, On-Premise 시스템은 정부 기관, 규제 대상인 금융 업계, 국방 분야에서 여전히 중요한 역할을 수행하고 있습니다.

2025년에는 대기업이 63.41%의 점유율을 차지했으며, 이는 다국적 대규모 고용주들이 가장 큰 보고 및 거버넌스 부담을 안고 있다는 사실을 반영했습니다. 이러한 기업들은 대개 더 많은 직무 체계, 더 많은 급여 등급, 그리고 더 많은 현지 규정 준수 규칙을 관리하고 있어, 수작업에 의한 검토를 유지하기가 어려워지고 있습니다. 또한, EU의 보고 체계는 노동력에 관한 정보 공개가 공식적인 지속가능성 보고서에 가까워짐에 따라 대기업의 플랫폼 투자를 촉진하고 있습니다. 직원 수 1,000명 이상이고 매출액이 4억 5,000만 유로(5억 800만 달러)인 개정된 기준을 초과하는 조직의 경우, 통합형 인력 보고 시스템의 도입이 더욱 시급한 과제가 되고 있습니다. 따라서 주요 고객은 다양성, 형평성 및 포용성(DEI) 분석 플랫폼 시장의 핵심 시장으로 자리매김하고 있습니다.

중소기업(SME) 시장은 2031년까지 연평균 성장률(CAGR) 19.62%로 확대될 것으로 예상되며, 규정 준수 요건이 소규모 고용주에게도 확대됨에 따라 가장 빠르게 성장하는 구매자층이 될 전망입니다. 도입 준비 상황은 여전히 편차가 있는 것으로 나타났으며, 2025년 조사 결과 많은 조직이 EU의 주요 임금 투명성 요건에 대응할 준비가 되어 있지 않은 것으로 드러났고, 보다 광범위한 보상 분석에 대한 준비 상황은 더욱 낮은 것으로 나타났습니다. 이러한 격차로 인해, 도입 초기부터 본격적인 기업 분석 팀이 필요 없는 경량형 구현, 기성 템플릿, 그리고 가이드가 포함된 워크플로우에 대한 수요가 생겨나고 있습니다. 따라서 DEI 분석 플랫폼 업계에서는 대기업의 거버넌스 프로그램에서 시작해, 보다 신속하고 체계적인 규정 준수 지원이 필요한 중소기업으로 수요가 확대되고 있는 것으로 나타납니다.

지역별 분석

2025년, 북미는 41.37%의 점유율을 차지하며 다양성, 형평성 및 포용성(DEI) 분석 플랫폼 시장에서 가장 규모가 큰 지역이 되었습니다. 이 지역은 복잡한 노동 시장 속에서 고용주가 보상 관리, 채용의 공정성 및 정당성을 입증할 수 있는 문서화에 큰 중점을 두고 있다는 점에서 혜택을 보고 있습니다. 뉴욕시의 자동화된 채용 심사 규정은 편향성 심사를 단순한 정책 논쟁에서 자동화된 의사결정 도구를 활용하는 고용주에게 적용되는 운영 요건으로 전환시켰기 때문에 여전히 중요한 위치를 차지하고 있습니다. 또한, 정치적 압력으로 인해 2024년과 2025년에는 일부 기업들이 예산을 설명하는 방식도 변화하여, 명시적인 DEI 용어보다는 ‘인력 인텔리전스’나 ‘리스크 관리’와 같은 표현이 빈번하게 사용되게 되었습니다. 그럼에도 불구하고, 감사 가능한 노동력 데이터에 대한 근본적인 필요성이 사라진 것은 아니었기 때문에 수요는 유지되었습니다.

유럽은 규제 주도형 수요 양상이 가장 두드러지는 지역 중 하나이며, 이 지역의 DEI 분석 플랫폼 시장 규모는 공식적인 공시 및 보고 요건과 밀접한 관련이 있습니다. ESRS S1은 임금 격차, 차별 사례, 이사회 다양성에 관한 감사 가능한 공시를 의무화하고 있으며, 2026년 보고 주기를 앞두고 기업들이 보다 견고한 데이터 파이프라인을 구축하도록 요구하고 있습니다. EU의 임금 투명성 지침 및 관련 성별 보고 규정은 임금 체계와 근로자의 권리 전반에 걸쳐 일관성을 더욱 강력히 요구함으로써 이러한 변화를 뒷받침하고 있습니다. 영국은 여전히 독자적인 길을 걷고 있지만, 성별 임금 격차 보고 의무로 인해 유럽 전역의 사업 환경에서 대규모 고용주들에게 있어 노동력 형평성 분석의 중요성은 여전히 유지되고 있습니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 21.12%를 기록하며 성장할 것으로 예상되며, 예측 기간 동안 가장 빠르게 성장하는 지역 부문이 될 뿐만 아니라, 다양성·형평성·포용성(DEI) 분석 플랫폼 시장에 있어 중요한 신규 수요원이 될 것입니다. 일본은 상장 기업의 성별 정보 공개 규정을 통해 이미 의미 있는 기반을 마련해 놓았으며, 2025년 프레임워크에서는 다양성 관리와 기업의 경쟁력을 연계함으로써 경영진에 의한 보다 광범위한 도입이 촉진되고 있습니다. 인도와 중국은 플랫폼 보급 측면에서 아직 초기 단계에 있지만, 남미, 중동 및 아프리카는 여전히 선택적인 시장이며, 현지 소프트웨어 생태계가 성숙하기 전까지는 다국적 기업의 보고 요구가 수요를 주도하는 경우가 많습니다. 따라서 브라질, 사우디아라비아, 아랍에미리트, 남아프리카공화국, 나이지리아는 현재 시장 규모보다는 디지털 HR 인프라와 보고에 대한 기대가 높아질 때의 장기적인 성장 측면에서 중요해집니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.24According to Mordor Intelligence, the diversity, equity, and Inclusion (DEI) Analytics Platform Market size is projected to be USD 1.68 billion in 2025, USD 1.94 billion in 2026, and reach USD 4.26 billion by 2031, growing at a CAGR of 17.04% from 2026 to 2031.

This report is Segmented by Deployment Mode (Cloud-Based, On-Premises, and Hybrid), Enterprise Size (Large Enterprises, and More), Application (Pay Equity and Compensation Analytics, and More), End-User Industry (BFSI, Healthcare and Life Sciences, Information Technology and Telecom, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Diversity, Equity And Inclusion (DEI) Analytics Platform Market Trends and Insights

Pay Transparency Compliance Deadlines Accelerate Demand

Pay transparency has shifted from a narrow policy issue into a wider operating requirement for employers with multi-location workforces. The EU Pay Transparency Directive requires member states to transpose new rules by 2026, and that raises the value of tools that can create consistent pay gap records across entities and job levels. Once one location adopts a stricter disclosure rule, many employers treat that standard as the internal baseline across the whole company because separate pay logics by location create legal and administrative risk. That change pushes analytics procurement beyond compliance teams and into compensation planning, job architecture, and executive review cycles. In the DEI analytics platform market, vendors with auditable pay workflows benefit because employers need defensible explanations and traceable records, not just summary dashboards.

Artificial Intelligence-Enabled Workforce Decision-Making Expands Need for Bias Monitoring

AI tools are now used in hiring, evaluation, promotion, and compensation, extending bias risk well beyond older recruiting software. New York City's Local Law 144 already requires annual bias audits for automated employment decision tools, and a December 2025 review by the New York State Comptroller showed a clear gap between independent audit findings and formal enforcement outcomes. At the European level, employment-related AI systems fall into the high-risk category under the AI Act, which keeps workforce decision-making under close compliance scrutiny even as the implementation timeline remains under policy review. This means buyers increasingly need a record of how automated recommendations were generated, tested, and reviewed by humans before pay or hiring decisions are finalized. In the diversity, equity, and inclusion (DEI) analytics platform market, demand is broadening from specialist DEI teams to any organization using AI in core human capital workflows.

Sensitive Employee Data Privacy and Security Risks

DEI analytics depends on demographic fields that are treated as sensitive personal data in many jurisdictions, which immediately narrows what employers can collect and how they can use it. A 2025 article noted that Article 10(5) of the EU AI Act permits the use of sensitive data for bias mitigation only within a strict compliance framework, which many mid-sized organizations still lack. Cross-border employers then face another challenge: data practices common in U.S. self-identification programs may be more restricted elsewhere. That leaves many analytics teams working with partial or voluntary datasets, which weakens statistical confidence and makes some reports harder to treat as audit-grade evidence. In the diversity, equity, and inclusion (DEI) analytics platform market, this issue slows adoption most where legal review, public accountability, and workforce sensitivity are highest.

Other drivers and restraints analyzed in the detailed report include:

- Hybrid Workforce Management Increases Need for Equity Visibility

- Board and Investor Scrutiny Elevates Workforce Disclosure Requirements

- Integration Complexity Across Fragmented Human Resources Data Stacks

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-based deployment accounted for 68.73% of the diversity, equity, and inclusion (DEI) analytics platform market share in 2025, making it the clear operating model for organizations that need faster reporting across distributed HR systems. That lead came from easier deployment, centralized updates, and better support for multi-jurisdiction reporting when pay rules changed quickly. Cloud tools also help employers connect compensation, recruiting, and representation data without waiting for long internal release cycles. This matters because DEI analytics works best when data moves continuously rather than through yearly manual extracts. Within the DEI analytics platform industry, cloud remains the default choice for firms that want faster compliance execution and broader dashboard access.

Hybrid deployment is projected to expand at a 18.73% CAGR through 2031, and the diversity, equity, and inclusion (DEI) analytics platform market for this mode is growing as multinationals seek to balance speed with data residency controls. The pattern fits organizations that keep identifiable demographic records inside their own environments while sending limited analytics workloads to the cloud. SAP SuccessFactors added EU Pay Transparency Directive-ready pay gap analysis in its April 2026 release, which shows how major HCM vendors are building these capabilities into their cloud suites rather than leaving them fully to outside tools. On-premises systems, therefore, continue to play a durable role in government, regulated finance, and defense environments, even as most new deployments center on cloud or hybrid models.

Large enterprises held 63.41% share in 2025, reflecting the fact that large, multi-country employers face the highest reporting and governance burden. They usually manage more job structures, more pay bands, and more local compliance rules, which makes manual review hard to sustain. The EU reporting framework also favors platform spending by larger firms because workforce disclosures now sit closer to formal sustainability filings. Organizations above the revised threshold of more than 1,000 employees and EUR 450 million (USD 508 million) turnover face a clearer case for integrated workforce reporting systems. Large accounts, therefore, remain the commercial core of the diversity, equity, and inclusion (DEI) analytics platform market.

SMEs are projected to expand at a 19.62% CAGR through 2031, making them the fastest-growing buyer group as compliance expectations spread to smaller employer thresholds. Readiness remains uneven, and research in 2025 showed that many organizations were not prepared for core EU pay transparency requirements, with weaker readiness on wider compensation analysis. That gap creates space for lighter implementations, pre-built templates, and guided workflows that do not require a full enterprise analytics team from day one. The DEI analytics platform industry is therefore seeing demand widen from large enterprise governance programs toward smaller firms that need faster, more structured compliance support.

Geography Analysis

North America held a 41.37% share in 2025, making it the largest region in the diversity, equity, and inclusion (DEI) analytics platform market. The region benefits from strong employer focus on pay governance, hiring fairness, and defensible documentation across complex labor markets. New York City's automated hiring audit rule remains important because it turned bias review from a policy debate into an operating requirement for employers using automated decision tools. Political pressure also changed how some companies described budgets in 2024 and 2025, with workforce intelligence and risk management used more often than explicit DEI language. Even so, demand held because the underlying need for auditable workforce data did not disappear.

Europe has one of the most regulation-driven demand profiles, and the DEI analytics platform market size in the region is closely tied to formal disclosure and reporting requirements. ESRS S1 requires auditable disclosures on pay gaps, discrimination incidents, and board diversity, pushing companies toward stronger data pipelines for 2026 reporting cycles. The EU Pay Transparency Directive and related gender reporting rules are reinforcing that shift by requiring more consistency across pay structures and employee rights. The United Kingdom still follows its own path, but mandatory gender pay gap reporting keeps workforce equity analytics relevant for large employers across the wider European operating landscape.

Asia-Pacific is projected to grow at a 21.12% CAGR through 2031, making it the fastest-growing regional segment and an important source of new demand for the diversity, equity, and inclusion (DEI) analytics platform market over the forecast period. Japan has already set a meaningful baseline through listed-company gender disclosure rules, and its 2025 framework connected diversity management with corporate competitiveness, which supports wider executive adoption. India and China remain earlier in platform penetration, while South America, the Middle East, and Africa are still more selective markets where multinational reporting needs often lead demand before local software ecosystems deepen. Brazil, Saudi Arabia, the UAE, South Africa, and Nigeria, therefore, matter less for current scale than for long-run expansion once digital HR infrastructure and reporting expectations strengthen.

- Syndio

- First Capitol Consulting, Inc. dba Trusaic

- Diversio

- Textio, Inc.

- Mathison Technologies, Inc.

- Clusivity .

- EDGE Strategy AG

- Sysarb AB

- Aleria PBC

- TheDenominator, Inc.

- Visier Inc.

- Kanarys Inc

- Eskalera, Inc.

- Vault Platform Ltd.

- Be Applied Limited

- Ligilo Inc. d/b/a Inclusively

- Diversance, Inc.

- One Model Inc.

- Focus Orange Technology B.V.

- Aperian Global, Inc.

- Equalture B.V.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Pay Transparency Compliance Deadlines Accelerate Demand

- 4.2.2 Artificial Intelligence-Enabled Workforce Decision-Making Expands Need for Bias Monitoring

- 4.2.3 Hybrid Workforce Management Increases Need for Equity Visibility

- 4.2.4 Board and Investor Scrutiny Elevates Workforce Disclosure Requirements

- 4.2.5 European Sustainability Reporting Disclosures Require Auditable Inclusion Data Infrastructure

- 4.2.6 Employment Algorithm Regulations Increase Bias Audit and Recordkeeping Demand

- 4.3 Market Restraints

- 4.3.1 Sensitive Employee Data Privacy and Security Risks

- 4.3.2 Integration Complexity Across Fragmented Human Resources Data Stacks

- 4.3.3 United States Political and Legal Backlash Slows Explicit Diversity Program Budgets

- 4.3.4 Weak Internal Ownership and Return on Investment Attribution Delay Buying Decisions

- 4.4 Industry Value and Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Deployment Mode

- 5.1.1 Cloud-Based

- 5.1.2 On-Premises

- 5.1.3 Hybrid

- 5.2 By End User Enterprise Size

- 5.2.1 Large Enterprises

- 5.2.2 Small and Medium-sized Enterprises

- 5.3 By Application

- 5.3.1 Pay Equity and Compensation Analytics

- 5.3.2 Hiring, Recruitment and Talent Acquisition Equity Analytics

- 5.3.3 Promotion, Performance and Career Mobility Analytics

- 5.3.4 Inclusion, Belonging and Employee Experience Analytics

- 5.3.5 Workforce Demographic and Representation Analytics

- 5.3.6 Compliance, ESG and Sustainability Reporting Analytics

- 5.3.7 Bias Detection and Workforce Risk Analytics

- 5.3.8 DEI Benchmarking and Organizational Intelligence

- 5.4 By End User Industry

- 5.4.1 BFSI

- 5.4.2 Healthcare and Life Sciences

- 5.4.3 Information Technology and Telecom

- 5.4.4 Retail and E-commerce

- 5.4.5 Industrial Manufacturing

- 5.4.6 Government and Public Sector

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 United Kingdom

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Russia

- 5.5.3.7 Netherlands

- 5.5.3.8 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Australia and New Zealand

- 5.5.4.6 Rest of Asia-Pacific

- 5.5.5 Middle East

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 Rest of Middle East

- 5.5.6 Africa

- 5.5.6.1 South Africa

- 5.5.6.2 Nigeria

- 5.5.6.3 Rest of Africa

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments).

- 6.4.1 Syndio

- 6.4.2 First Capitol Consulting, Inc. dba Trusaic

- 6.4.3 Diversio

- 6.4.4 Textio, Inc.

- 6.4.5 Mathison Technologies, Inc.

- 6.4.6 Clusivity .

- 6.4.7 EDGE Strategy AG

- 6.4.8 Sysarb AB

- 6.4.9 Aleria PBC

- 6.4.10 TheDenominator, Inc.

- 6.4.11 Visier Inc.

- 6.4.12 Kanarys Inc

- 6.4.13 Eskalera, Inc.

- 6.4.14 Vault Platform Ltd.

- 6.4.15 Be Applied Limited

- 6.4.16 Ligilo Inc. d/b/a Inclusively

- 6.4.17 Diversance, Inc.

- 6.4.18 One Model Inc.

- 6.4.19 Focus Orange Technology B.V.

- 6.4.20 Aperian Global, Inc.

- 6.4.21 Equalture B.V.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment