|

시장보고서

상품코드

2064544

임시 인력 관리 플랫폼 시장 : 시장 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Contingent Workforce Management Platform - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

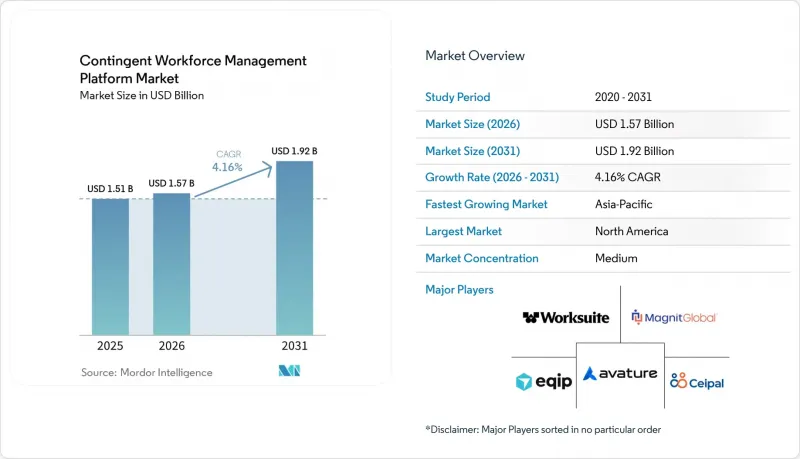

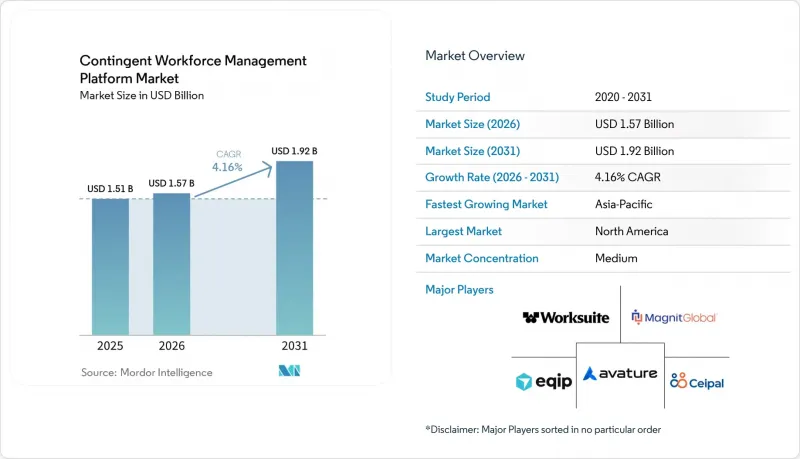

Mordor Intelligence에 의하면, 임시 인력 관리 플랫폼 시장 규모는 2025년에 15억 1,000만 달러로 평가되었고, 2026년에 15억 7,000만 달러로 추정되고, 2031년까지 19억 2,000만 달러에 이를 것으로 예측됩니다.

2026-2031년 연평균 성장률(CAGR) 4.16%로 성장할 것으로 전망됩니다.

본 보고서는 구성 요소별(소프트웨어, 서비스), 기능별(벤더 관리 시스템(VMS) 등), 배포 방식별(클라우드 기반 등), 조직 규모별(대기업 등), 최종 사용자 산업별(IT 및 통신, 소매업·전자상거래 등), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 임시 인력 관리 플랫폼 시장 동향 및 인사이트

유연한 인력 및 프로젝트 기반 인력에 대한 기업의 의존도 증가

유연한 인력은 현재 계획적인 사업 운영 모델의 일부가 되고 있습니다. 특히, 납기, 기술적 요구 사항, 비용 압박이 정규직 채용 주기가 대응할 수 있는 속도보다 빠르게 변화하는 업계에서 이러한 현상이 두드러집니다. 이러한 변화로 인해, 공통 거버넌스 계층을 통해 근로자 유형, 공급업체 활용, 승인, 온보딩, 계약 관리 및 지급 워크플로를 관리할 수 있는 시스템의 가치가 높아지고 있습니다. 기업들이 이메일이나 스프레드시트를 통한 단편적인 계약자 관리 대신, 프로그램 수준의 가시성과 일관된 정책 적용을 요구함에 따라, 임시 인력 관리 플랫폼 시장이 그 혜택을 누리고 있습니다. 또한, 임시 리더나 전문 컨설턴트 등 부가가치가 더 높은 외부 인력의 경우, 세무 처리, 지적 재산권, 계약 가치 및 국가별 계약 규칙에 관한 보다 철저한 관리가 요구됩니다. 따라서 구매 담당자들은 외부 인재 채용의 전 과정을 관리하고, 여러 인재 확보 채널에 걸쳐 감사 가능한 기록을 유지할 수 있는 플랫폼을 선호합니다. 2025년 6월 Beeline이 MBO Partners를 인수한 것은 독립 계약자, 컨설턴트, 긱 워커, 급여 계산 대상 전문직 등 보다 광범위한 외부 인력을 단일 규정 준수 환경 내에서 포괄해야 할 필요성을 반영한 것입니다.

AI를 활용한 시각화, 매칭 및 지출 최적화

AI는 임시 인력 관리 플랫폼 시장에서 단순한 제품 차별화 요소에서 기본적인 요건으로 자리 잡았습니다. 기업들은 현재 일상적인 프로그램 관리에 직접 통합된, 보다 신속한 매칭, 명확한 지출 가시화, 보상 수준 벤치마킹, 워크플로우 제안, 그리고 더 정확한 예측을 요구하고 있습니다. Beeline은 2025년 4월, 자사의 비상근 인력 데이터 인프라를 기반으로 구축된, 기술 적합성 평가, 에이전트 기능 및 자동화된 규정 준수 정책 관리 기능을 갖춘 ‘Beeline AI’를 도입했습니다. SAP Fieldglass는 2026년 5월 릴리스를 통해 AI를 활용한 이력서 평가, AI를 이용한 SOW(작업 명세서) 공동 작성 기능, 그리고 SOW의 상세 정보를 기반으로 한 근로자 역할 자동 제안 등을 통해 이러한 방향성을 강화했습니다. 이러한 도구는 인재 확보 및 채용 과정에서 발생하는 마찰을 줄여주지만, 동시에 외부 인재 기용과 관련된 의사결정에 대해 설명 가능성, 감독, 명확한 감사 추적 기록에 대한 구매자의 기대도 높이고 있습니다. 조달, 인사, 법무 각 팀은 관리 권한을 포기하지 않으면서도 신속성을 추구하기 때문에 자동화와 인적 검토를 결합한 벤더들이 주목받고 있습니다.

HRIS, ERP, 조달, 급여 계산 시스템과의 복잡한 통합

통합은 임시 인력 관리 플랫폼 시장에서 여전히 가장 뿌리 깊은 도입 장벽으로 남아 있습니다. 비정규직 근로자 프로그램은 일반적으로 별도로 구축된 인사, 조달, 재무, 급여 계산 시스템에 걸쳐 있으며, 근로자 유형, 원가 센터, 공급업체 데이터, 청구 규칙에 대해 서로 다른 정의가 적용되는 경우가 많습니다. Beeline사는 자사의 플랫폼이 845건의 HCM 및 ERP 통합을 지원하고 있으며, 그 내역은 Oracle 500건, SAP 440건, Workday 405건이라고 밝혔는데, 이는 기술적 환경이 얼마나 광범위해졌는지를 보여줍니다. 해당 자료에서는 구매자가 실시간 API 작동을 기대하고 있음에도 불구하고, 기존의 배치 처리 아키텍처에서는 여전히 타이밍 차이나 검증상의 문제가 발생할 수 있다고 지적하고 있습니다. 통합에 드는 비용과 복잡성은 도입 결정을 지연시키는 요인이 될 수 있습니다. 특히, 기업이 국가마다 다른 현지 세제, 청구, 공급업체 및 근로자에 관한 규정을 조율해야 하는 경우에는 더욱 그렇습니다. 그럼에도 불구하고, 자동화를 미루는 조직에서는 단편화된 기록이 쌓이고 감사 대응 능력이 지속적으로 저하되는 경우가 많으며, 그 결과 향후 전환이 더욱 어려워질 가능성이 있습니다.

부문별 분석

2025년 기준으로 소프트웨어는 임시 인력 관리 플랫폼 시장의 67.22%를 차지했으나, 서비스 부문은 2031년까지 연평균 성장률(CAGR) 6.72%로 확대될 것으로 전망됩니다. 구매자들은 여전히 채용 요청, 근로자 데이터, 공급업체 목록, 승인 규칙, 근무 시간표, 청구서, 보고서를 단일 운영 계층 내에서 통합하는 ‘시스템 오브 레코드’를 원하고 있기 때문에 소프트웨어는 여전히 수익의 핵심으로 남아 있습니다. 또한, 설정 가능한 소프트웨어는 외부 인력의 관리 방식이 서로 다를 수 있는 각 사업 부문에서 재직 기간 제한, 온보딩 절차, 역할 승인 및 보상률 관리에 관한 정책을 철저히 이행할 수 있는 실용적인 수단을 기업에 제공합니다. 따라서 소프트웨어의 비중이 여전히 높은 것은 특히 관리 대상인 지출 규모가 큰 세계 기업들에서 정식 비정규직 근로자 프로그램 운영의 근간으로서의 그 역할을 반영하고 있습니다. 그러나 서비스의 성장 속도가 더욱 빨라지고 있다는 점은 많은 기업이 복잡한 도입, 통합 및 정책 일관성을 자체적으로만 관리하기를 원하지 않는다는 것을 보여줍니다.

세계의 다양한 프로그램과 시스템을 아우르는 복잡성을 안고 있는 구매자들에게 있어, 도입, 통합 및 관리형 지원은 표준 구매 패키지의 일부로 자리 잡고 있습니다. 또한 서비스 구성도 일회성 설정 작업에서 규정 준수 모니터링, 공급업체 성과 관리, 분석 검토, 사용자 관리, 프로그램 최적화 등 지속적인 지원으로 전환되고 있습니다. 이러한 변화는 임시 인력 관리 플랫폼 업계에서 중요한 의미를 지닙니다. 플랫폼이 가동되고 사내 책임 체계가 성숙해지면, 서비스 팀이 일상적인 거버넌스의 한 축을 담당하는 경우가 많아지기 때문입니다. 이를 통해 수익 기반의 안정성이 높아지고, 서비스가 소프트웨어의 지속적인 이용을 촉진하는 동시에, 신속한 표준화가 어려운 다국간 운영 모델에 대한 대응을 구매자가 보다 수월하게 수행할 수 있게 됩니다. 그 결과, 엔드투엔드 벤더와 그 파트너들은 라이선스 수익 증가에만 의존하지 않고, 매니지드 서비스 역량을 확대되고 있습니다. 특히, 규정 준수, 채용률, 지출 현황의 가시화 등 측정 가능한 성과를 요구하는 구매자의 경우, 이러한 경향이 두드러집니다.

VMS는 2025년에 35.66%의 시장 점유율을 유지했으나, 인재 확보 및 직접 소싱의 통합 시장은 2031년까지 연평균 성장률(CAGR) 5.99%로 성장할 전망입니다. VMS는 채용, 공급업체, 승인, 근무 시간 기록, 청구, 보고서를 단일하고 체계적으로 관리되는 워크플로우로 통합하여, 여러 도구나 이메일 교환에 분산되는 것을 방지하기 위해 여전히 기반이 되는 계층으로 자리 잡고 있습니다. 대기업의 프로그램에서는 여전히 이러한 핵심 기능에 의존하여, 여러 지역, 비용 센터, 인력 파견 파트너에 걸친 지출 관리 및 정책 이행을 철저히 수행하고 있습니다. 따라서 VMS 플랫폼이 제공하는 광범위한 관리 기능을 포인트 솔루션이 여전히 대체하지 못하고 있다는 점을 고려할 때, 그 압도적인 시장 점유율은 단순한 구매자의 관성이 아니라 지속적인 중요성을 반영한다고 할 수 있습니다. 동시에, 직접 소싱의 성장이 가속화되고 있다는 사실은 구매자들이 현재 플랫폼에 대해 인재 확보 및 관리 방식의 개선을 요구하고 있음을 보여줍니다.

기업들은 더 광범위한 공급업체 네트워크에 수요를 개방하기 전에, 채용 대행사의 마진을 줄이고 사전 심사를 거친 인재 풀의 재사용률을 높이려고 하고 있습니다. SAP Fieldglass는 2026년 5월, AI를 활용한 업무 범위 정의(SOW) 공동 작성 기능과 근로자 역할 자동 제안 기능을 추가했습니다. 이는 소싱 기능이 과거와 같이 독립적으로 운영되는 것이 아니라, 계획 및 인수 워크플로우와 더욱 긴밀하게 연계되고 있음을 보여줍니다. 또한, 분류 기준이 엄격해지고 구매자가 계약 결정이 일관되게 적용되었습니다는 점을 입증할 수 있는 더 강력한 증거를 요구하게 됨에 따라, 규정 준수 및 리스크 관리 모듈의 중요성도 커지고 있습니다. 기업들이 사업 부서 전반에 걸쳐 계약자의 가격 책정, 마진, 공급업체의 성과에 대해 보다 명확한 가시성을 요구함에 따라, 지출 관리 및 요금 벤치마킹 도구가 재무 부서의 주목을 받고 있습니다. AOR(에이전트 오브 레코드) 및 EOR(고용주 오브 레코드) 모델을 통해 외부 인력 구성에 참여하는 독립 전문 인력이 포함됨에 따라, 계약자 라이프사이클 관리가 확대되고 있습니다. 한편, DEI(다양성·공정성·포용성) 추적이나 모바일 우선 방식의 현장 근로자 지원과 같은 다른 모듈들은 임시 인력 관리 플랫폼 업계가 기존의 VMS(벤더 관리 시스템)의 핵심 기능을 넘어 그 영역을 확장해 나가고 있음을 보여줍니다.

지역별 분석

2025년, 북미는 임시 인력 관리 플랫폼 시장 점유율의 37.65%를 차지했으며, 여전히 지역별 매출 규모에서 가장 큰 비중을 유지했습니다. 해당 지역의 많은 대기업들이 조달, 인사, 재무, 법무, 공급업체 관리를 단일 운영 모델로 통합한 공식적인 임시 고용 프로그램을 이미 운영하고 있기 때문에 미국이 수요의 중심이 되고 있습니다. 또한, 이 지역의 구매 담당자들은 복잡한 분류 및 공동 고용 위험에 직면해 있으며, 이로 인해 거버넌스 기능이 구매의 최우선 과제로 자리매김하고, 공식적인 기록 관리 시스템에 대한 지속적인 투자가 뒷받침되고 있습니다. 캘리포니아주의 AB5 지침은 2026년에도 문서화된 하도급업체 판정 및 일관된 분류 워크플로우의 필요성을 계속해서 강조하고 있습니다. 다국적 기업들이 각국의 예외 규정에 따라 관리하는 대신 북미 전역에 공통된 거버넌스 기준을 적용하게 됨에 따라, 캐나다와 멕시코도 프로그램 설계에서 더욱 중요한 위치를 차지하게 되었습니다.

유럽은 임시 인력 관리 플랫폼 시장에서 규제 주도형 성장 영역으로 자리매김하고 있습니다. EU의 플랫폼 근로 지침은 지휘·감독이 인정되는 경우 고용 관계가 존재한다는 반증 가능한 추정 원칙을 도입하고 있으며, 회원국들은 2026년 12월 2일까지 이 규정을 국내법에 반영해야 합니다. 이러한 법적 압박은 각국의 서로 다른 규정과 법인 조직을 아우르며, 분류, 재직 기간, 승인 및 근로자의 신분을 모니터링할 수 있는 플랫폼에 대한 수요를 뒷받침하고 있습니다. 영국은 공급업체가 EU의 규정뿐만 아니라 독자적인 오프 페이롤(급여등) 규정 준수 요건도 충족해야 하기 때문에 여전히 중요한 시장입니다. 한편, 독일은 규정 준수를 중시하는 파견 근로 환경과 체계적으로 관리되는 외부 인력 프로세스에 대한 수요가 두드러집니다.

아시아태평양은 2031년까지 연평균 성장률(CAGR) 6.31%를 나타낼 것으로 예측되며, 이는 임시 인력 관리 플랫폼 시장에서 지역별 가장 높은 성장률입니다. 중국, 인도, 일본 및 동남아시아에서는 프로젝트 기반 또는 플랫폼을 통한 일자리 수요가 확대되고 있으며, 이에 따라 현지 기업과 다국적 기업들의 공식적인 거버넌스 체계 구축 및 기술 투자가 증가하고 있습니다. 인도는 주요 성장 거점으로서 두각을 나타내고 있습니다. 이는 전 세계 기업들이 IT 및 디지털 서비스 제공 과정에서 다수의 계약직 직원을 지속적으로 관리하고 있으며, 공급업체 및 업무 계약 전반에 걸친 가시성 향상이 요구되고 있기 때문입니다. 중동에서는 도입이 아직 초기 단계이지만, UAE와 사우디아라비아에서는 다양화 노력의 일환으로 외국인 근로자 프로그램이 확대됨에 따라 외부 노동력에 대한 체계적인 감독 체제 구축이 진행되고 있습니다. 남미와 아프리카는 여전히 성숙도가 낮은 편이지만, 브라질과 남아프리카공화국은 보다 일관된 임시 인력 관리와 명확한 감사 추적을 요구하는 다국적 기업들의 주요 지역 거점으로 자리 잡고 있습니다.

기타 혜택 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장률 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.26According to Mordor Intelligence, the contingent workforce management platform market size is projected to be USD 1.51 billion in 2025, USD 1.57 billion in 2026, and reach USD 1.92 billion by 2031, growing at a CAGR of 4.16% from 2026 to 2031.

This report is Segmented by Component (Software, and Services), Functionality (Vendor Management System [VMS], and More), Deployment Mode (Cloud-Based, and More), Organization Size (Large Enterprises, and More), End-User Industry (Information Technology and Telecommunications, Retail and E-Commerce, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Contingent Workforce Management Platform Market Trends and Insights

Rising Enterprise Reliance on Flexible and Project-Based Labor

Flexible labor is now part of planned operating models, especially in sectors where delivery timelines, technology needs, and cost pressures change faster than permanent hiring cycles can adjust. That change raises the value of systems that can manage worker type, supplier use, approvals, onboarding, contract controls, and payment workflows with a common governance layer. The contingent workforce management (WFM) platform market benefits because enterprises want program-level visibility and consistent policy enforcement, rather than local contractor administration handled via email and spreadsheets. Higher-value external roles, including interim leaders and specialist consultants, also require stronger controls around tax treatment, intellectual property, contract value, and country-specific engagement rules. Buyers are therefore favoring platforms that can manage the full external worker journey and maintain auditable records across multiple talent channels. Beeline's June 2025 acquisition of MBO Partners reflected this need for broader external talent coverage, including independent contractors, consultants, gig workers, and payrolled professionals, within a single, compliant environment.

AI-Enabled Visibility, Matching, and Spend Optimization

AI has moved from optional product differentiation to a baseline expectation in the contingent workforce management platform market. Enterprises now want faster matching, cleaner spend visibility, rate benchmarking, workflow suggestions, and better forecasting built directly into everyday program management. Beeline introduced Beeline AI in April 2025 with skills-proximity scoring, agentic capabilities, and automated compliance policy management built on its contingent labor data foundation. SAP Fieldglass strengthened the same direction in its May 2026 release through AI-assisted resume assessment, AI-enhanced statement-of-work collaboration, and automated worker role suggestions from SOW details. These tools reduce sourcing and intake friction, but they also raise buyer expectations around explainability, oversight, and clear audit trails for decisions that affect external talent engagement. Vendors that combine automation with human review are gaining ground because procurement, HR, and legal teams want speed without giving up control.

Complex Integration with HRIS, ERP, Procurement, and Payroll Stacks

Integration remains the most persistent adoption barrier in the contingent workforce management platform market. Contingent labor programs usually cut across HR, procurement, finance, and payroll systems that were built separately and often use different definitions for worker type, cost center, supplier data, and invoicing rules. Beeline states that its platform supports 845 HCM and ERP integrations, including 500 Oracle, 440 SAP, and 405 Workday connections, which shows how broad the technical landscape has become. The same material notes that legacy batch-processing architectures can still create timing gaps and validation issues when buyers expect real-time API behavior. Integration cost and complexity can delay deployment decisions, especially when enterprises also need local tax, billing, supplier, and worker rules aligned across countries. Even so, organizations that postpone automation often continue to accumulate fragmented records and weaker auditability, which can make later transitions even harder.

Other drivers and restraints analyzed in the detailed report include:

- Tightening Worker Classification and Labor Compliance Requirements

- Need for Faster Access to Specialized Digital and Professional Skills

- Data Privacy, Cybersecurity, and Cross-Border Data Transfer Risk

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Software held 67.22% of the contingent workforce management platform market share in 2025, while services are projected to expand at a 6.72% CAGR through 2031. Software remains the core revenue engine because buyers still want a system of record that centralizes requisitions, worker data, supplier lists, approval rules, timesheets, invoices, and reporting within a single operating layer. Configurable software also gives enterprises a practical way to enforce policies around tenure limits, onboarding steps, role approvals, and rate controls across business units that may otherwise manage external talent differently. The continued weight of software therefore reflects its role as the operational backbone of formal contingent labor programs, especially in global organizations with large spend under management. Yet the faster growth in services shows that many enterprises do not want to manage complex rollouts, integrations, and policy alignment on their own.

Implementation, integration, and managed support are becoming part of the standard buying package for buyers with global programs and cross-system complexity. The services mix is also moving beyond one-time setup work toward recurring support around compliance monitoring, supplier performance, analytics review, user administration, and program optimization. That change matters in the contingent workforce management platform industry because service teams often become part of day-to-day governance after the platform goes live and internal ownership matures. It creates a stickier revenue profile, with services reinforcing software retention and helping buyers handle multi-country operating models that are difficult to standardize quickly. The result is that end-to-end vendors and their partners are broadening their managed-service capabilities rather than relying solely on license growth, especially where buyers want measurable outcomes tied to compliance, fill rates, and spend visibility.

VMS retained a 35.66% share in 2025, while talent sourcing and direct sourcing integration are set to expand at a 5.99% CAGR through 2031. VMS remains the foundational layer because it connects requisitions, suppliers, approvals, timesheets, invoicing, and reporting into a single, governed workflow, rather than leaving them spread across several tools and email chains. Large enterprise programs still depend on this core capability to control spend and enforce policy across many geographies, cost centers, and staffing partners. Its leading share, therefore, reflects continued relevance rather than simple buyer inertia, since point solutions still struggle to replace the breadth of control that VMS platforms provide. At the same time, the faster growth of direct sourcing shows that buyers now want platforms to improve talent access and administration.

Enterprises are trying to reduce agency markup and improve reuse of pre-vetted talent pools before opening demand to the wider supplier network. SAP Fieldglass added AI-enhanced statement-of-work collaboration and automated worker role suggestions in May 2026, showing how sourcing features are moving closer to planning and intake workflows rather than staying separate from them. Compliance and risk management modules are also gaining weight as classification rules tighten and buyers want stronger evidence that engagement decisions were applied consistently. Spend management and rate benchmarking tools are attracting more finance attention as enterprises seek clearer visibility into contractor pricing, markups, and supplier performance across business lines. Contractor lifecycle management is expanding as external talent mixes now include independent professionals engaged through AOR and EOR models, while other modules, such as DEI tracking and mobile-first field labor support, show how the contingent workforce management platform industry is broadening beyond the historic VMS core.

Geography Analysis

North America held 37.65% of the contingent workforce management platform market share in 2025 and remained the largest regional revenue base. The United States anchors demand because many large enterprises in the region already run formal contingent programs that integrate procurement, HR, finance, legal, and supplier management into a single operating model. Buyers in this region also face complex classification and co-employment exposures, which keep governance features high on the purchase agenda and support continued investment in formal systems of record. California's AB5 guidance continued to reinforce the need for documented contractor tests and consistent classification workflows in 2026. Canada and Mexico are also becoming more relevant to program design as multinational employers extend common governance standards across North America instead of managing each country through local exceptions.

Europe is becoming a regulation-led growth area for the contingent workforce management platform market. The EU Platform Work Directive introduced a rebuttable presumption of employment where direction and control are found, and member states must transpose the rules by December 2, 2026. That legal pressure supports demand for platforms that can monitor classification, tenure, approvals, and worker status across different national rules and corporate entities. The United Kingdom remains important as vendors must support separate off-payroll compliance needs alongside the EU framework, while Germany stands out for its compliance-heavy temporary labor environment and strong demand for governed external workforce processes.

Asia-Pacific is forecast to grow at a 6.31% CAGR through 2031, the fastest regional rate in the contingent workforce management platform market. China, India, Japan, and Southeast Asia are expanding the pool of project-based and platform-mediated work, which is drawing more formal governance and technology investment from local firms and multinational employers. India stands out as a major growth point because global enterprises continue to manage large contractor populations in IT and digital services delivery, and need better visibility across suppliers and engagements. The Middle East is still early in adoption, but the UAE and Saudi Arabia are creating space for structured oversight of external workforces as non-national labor programs expand under diversification efforts. South America and Africa remain less mature, yet Brazil and South Africa serve as the main regional anchors for multinational buyers seeking more consistent contingent workforce control and clearer audit trails.

- Beeline

- Magnit, LLC

- Avature Limited

- CXC Global

- Worksuite Inc.

- VectorVMS1 LLC

- Pixid

- Eqip AG

- Netive VMS

- Prosperix

- Ceipal Corp.

- Flextrack Inc.

- Simplify Workforce

- StafferLink

- Trio Workforce Solutions

- Flentis Corporation

- DirectSkills

- Worksome ApS

- MBO Partners

- 3 Story Software LLC

- i-Resource Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Enterprise Reliance on Flexible and Project-Based Labor

- 4.2.2 Tightening Worker Classification and Labor Compliance Requirements

- 4.2.3 AI-Enabled Visibility, Matching, and Spend Optimization

- 4.2.4 Need for Faster Access to Specialized Digital and Professional Skills

- 4.2.5 Expansion of Direct Sourcing and Private Talent Pool Strategies

- 4.2.6 Convergence of Services Procurement and Contingent Labor Workflows

- 4.3 Market Restraints

- 4.3.1 Complex Integration With HRIS, ERP, Procurement, and Payroll Stacks

- 4.3.2 Data Privacy, Cybersecurity, and Cross-Border Data Transfer Risk

- 4.3.3 Rising Identity Fraud and Worker Verification Burden in Remote Hiring

- 4.3.4 Governance Friction Across HR, Procurement, Legal, and Finance Stakeholders

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Buyers

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By component

- 5.1.1 Software

- 5.1.2 Services

- 5.1.2.1 Implementation and Integration

- 5.1.2.2 Support and Maintenance

- 5.2 By Functionality

- 5.2.1 Vendor Management System (VMS)

- 5.2.2 Contractor Lifecycle Management

- 5.2.3 Talent Sourcing and Direct Sourcing Integration

- 5.2.4 Compliance and Risk Management

- 5.2.5 Spend Management and Rate Benchmarking

- 5.2.6 Other Functionalities

- 5.3 By Deployment Mode

- 5.3.1 Cloud-Based

- 5.3.2 On-Premises

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium-sized Enterprises

- 5.5 By End-User Industry

- 5.5.1 Information Technology and Telecommunications

- 5.5.2 Banking, Financial Services, and Insurance

- 5.5.3 Healthcare and Life Sciences

- 5.5.4 Manufacturing

- 5.5.5 Retail and E-commerce

- 5.5.6 Other End-User Industries

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Italy

- 5.6.3.5 Spain

- 5.6.3.6 Russia

- 5.6.3.7 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 South Korea

- 5.6.4.5 Australia

- 5.6.4.6 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Nigeria

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Beeline

- 6.4.2 Magnit, LLC

- 6.4.3 Avature Limited

- 6.4.4 CXC Global

- 6.4.5 Worksuite Inc.

- 6.4.6 VectorVMS1 LLC

- 6.4.7 Pixid

- 6.4.8 Eqip AG

- 6.4.9 Netive VMS

- 6.4.10 Prosperix

- 6.4.11 Ceipal Corp.

- 6.4.12 Flextrack Inc.

- 6.4.13 Simplify Workforce

- 6.4.14 StafferLink

- 6.4.15 Trio Workforce Solutions

- 6.4.16 Flentis Corporation

- 6.4.17 DirectSkills

- 6.4.18 Worksome ApS

- 6.4.19 MBO Partners

- 6.4.20 3 Story Software LLC

- 6.4.21 i-Resource Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and unmet-need assessment