|

시장보고서

상품코드

2063421

기업용 AI 인력 플랫폼 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Enterprise AI Workforce Platforms - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

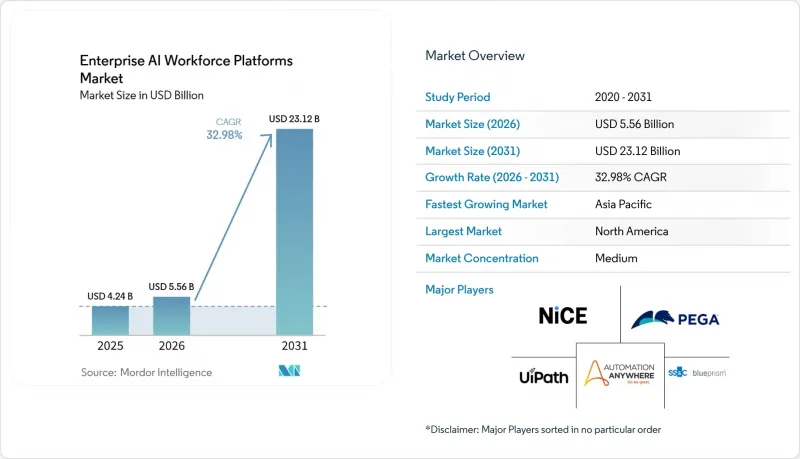

Mordor Intelligence에 의하면, 기업용 AI 인력 플랫폼 시장 규모는 2025년에 42억 4,000만 달러로 평가되었고, 2026년에 55억 6,000만 달러로 추정되고, 2031년까지 231억 2,000만 달러에 이를 것으로 예측됩니다. 2026-2031년 CAGR 32.98%로 성장할 전망입니다.

본 보고서는 도입 형태별(온프레미스, 클라우드, 하이브리드), 구성 요소별(소프트웨어 및 서비스), 최종 사용자 산업별(IT 및 통신, 헬스케어 및 생명과학, 제조, 은행, 금융서비스 및 보험(BFSI), 소매 및 전자상거래, 교육 등), 조직 규모별(대기업 및 중소기업), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 엔터프라이즈 AI 인력 플랫폼 시장 동향 및 인사이트

생성형 AI 코파일럿의 엔터프라이즈 생산성 제품군 통합

익숙한 협업 도구 내에 Copilot을 통합함으로써, 작업 식별과 자동화 사이의 수작업이 필요 없어지며, 직원들은 메인 용도를 벗어나지 않고도 에이전트를 호출할 수 있습니다. 마이크로소프트는 2025년 1월까지 Copilot 유료 구독자가 100만 명에 달했다고 보고했으며, 문서 작성 및 회의 요약 작업에서 29%의 시간 단축 효과를 달성했다고 밝혔습니다. 세일즈포스는 이에 이어 Agentforce를 도입했습니다. 이를 통해 기술적 지식이 없는 직원도 자율적인 고객 서비스 에이전트를 가동할 수 있게 되었으며, 시범 운영에서 문제 해결 시간을 40% 단축했습니다. 밀접한 통합으로 인해 전환 비용이 증가합니다. 이는 기업들이 개별 조달 주기보다 번들형 업그레이드를 선호하기 때문입니다. ISO/IEC 42001과 같은 규정 준수 프레임워크는 공급업체에 임베디드형 코파일럿 인증 획득을 요구하고 있으며, 이로 인해 기존 생산성 제품군 공급업체들이 구매 후보 목록에 더욱 확고히 자리 잡게 될 것입니다. 이러한 동향들이 맞물리면서, 도입 초기 단계에서 수요가 앞당겨지고 프리미엄 가격 책정이 지지를 받게 될 것입니다.

인건비 상승이 자동화의 투자 수익률(ROI)을 가속화합니다.

2025년 인도 IT 서비스 부문의 연 8-10%, 필리핀 콜센터 직원의 연 7-9%에 달하는 임금 상승으로 인해, 인적 노동과 자율형 에이전트 간의 경제적 격차는 줄어들었습니다. 청구서 처리 자동화 계약의 회수 기간은 2023년 24개월에서 2025년에는 14개월로 단축될 것으로 예측됩니다. 이에 대해 베트남 정부는 산업용 AI 도입을 위한 2억 달러 규모의 장려 기금을 조성하여, 기업의 자동화 목표와 정책적 일관성을 보여주었습니다. 그 결과, CFO들은 현재 AI 인재에 대한 투자를 영업이익률을 안정시키는 인플레이션 헤지 수단으로 간주하고 있습니다. 이러한 재정적 논리는 특히 반복적인 업무 흐름이 비용 구조의 상당 부분을 차지하는 백오피스 기능 분야에서 다년간에 걸친 예산 배분을 뒷받침하고 있습니다.

데이터의 소재지 및 주권에 대한 우려가 여전히 뿌리 깊어, 국경을 넘는 도입이 제한되고 있습니다.

EU의 일반 데이터 보호 규정(GDPR(EU 개인정보보호규정)), 중국의 사이버 보안법, 그리고 인도의 디지털 개인 데이터 보호법은 무제한 데이터 전송을 금지하고 있어, 기업들은 주권적 구획을 갖춘 하이브리드 토폴로지를 도입할 수밖에 없습니다. 규정 준수에 따른 간접 비용은 중복된 스택, 계약상 보호 조치, 현지화된 지원 팀이 필요하기 때문에 총 소유 비용(TCO)을 증가시키고 있습니다. 국제개인정보보호전문가협회(IAPP)의 조사에 따르면, 다국적 기업의 58%가 법적 이전 메커니즘에 대한 불확실성이 해소되지 않는다는 이유로 AI를 활용한 업무 지원 시스템 도입을 연기하고 있습니다. 벤더 측은 지역별 제어 플레인 및 엣지 옵션을 통해 대응하고 있지만, 높은 가격 책정과 유지보수의 복잡성으로 인해 클라우드 모델이 약속하는 비용 절감 효과의 일부가 상쇄되고 있습니다. 이러한 분산화의 위험은 의료, 은행, 행정 등 기밀 데이터를 다루는 분야에서 가장 높습니다.

부문별 분석

지능형 오토메이션 스위트는 2025년 매출의 41.37%를 차지했으며, 대부분의 변혁 로드맵에서 첫걸음으로서의 역할을 입증하고 있습니다. 기업들은 이 스위트에 통합된 프로세스 마이닝 및 문서 인텔리전스 모듈을 높이 평가했습니다. 이는 ROI가 높은 이용 사례를 파악하고, 예외 처리를 수행하는 모델에 훈련 데이터를 제공합니다. 각 벤더사는 대화형 AI 업무 지원 도구를 동일한 스택에 통합하고 있으며, 이에 따라 고객 대응 시나리오에서 에이전트형 챗봇을 위한 엔터프라이즈 AI 업무 지원 플랫폼 시장 규모가 급속히 확대되고 있습니다. 한편, 기술 개발 플랫폼은 연평균 성장률(CAGR) 33.98%로 가장 급격한 성장세를 기록하고 있으며, 이는 자동화로 인해 일자리를 잃은 근로자들의 재교육을 위한 전략적 전환을 반영하고 있습니다. Coursera에서는 2025년에 생성형 AI 과정 수강생 수가 180% 급증했습니다. 이러한 급증은 검증된 역량과 사업 부문 간 프로젝트 수요를 연결하는 사내 인재 마켓플레이스에 대한 조직적인 노력을 보여줍니다.

워크포스 애널리틱스 플랫폼은 현재 예측 모델링과 실시간 생산성 텔레메트리 데이터를 결합하여, 이직이나 성과 저하가 발생하기 전에 선제적인 개입을 유도하고 있습니다. 통합형 인재 마켓플레이스는 이러한 인사이트와 단기 프로젝트 형태의 업무 배정을 결합함으로써 유휴 시간을 줄이고 사내 이동을 촉진합니다. Microsoft Viva의 크로스오버 성공(2025년 말까지 월간 활성 사용자 수 4,000만 명)은 고용주들이 학습, 참여도, 분석을 통합적으로 관리할 수 있는 통합 플랫폼을 원하고 있음을 보여줍니다. 스위트 간의 융합이 진행됨에 따라 경쟁은 더욱 치열해지고 있습니다. 왜냐하면 구매자는 여러 포인트 솔루션을 조합하는 것보다 엔드투엔드 프로비저닝을 선호하기 때문입니다. 융합이 진행됨에 따라, 엔터프라이즈 AI 인재 플랫폼 시장에서 독립형 포인트 제품의 점유율은 축소될 가능성이 높습니다.

유연한 종량제 요금 체계와 신속한 도입 덕분에, 2025년에도 클라우드는 63.52%의 점유율을 유지하며 여전히 지배적인 위치를 차지하고 있습니다. 그러나 더욱 엄격해진 로컬라이제이션 법규와 실시간 추론에 대한 수요로 인해 기업들은 하이브리드 솔루션으로 전환하고 있으며, 해당 시장은 연평균 성장률(CAGR) 33.38%로 성장을 지속하고, 있습니다. 금융 기관들은 현재 기밀성이 높은 워크로드를 온프레미스에서 유지하면서, 감독 범위 밖의 분석에는 퍼블릭 클라우드를 활용하고 있습니다. EU AI법에서 규정하는 '고위험' 분류는 유럽의 구매자들이 유사한 분산 아키텍처를 도입하는 계기가 되고 있으며, 이에 따라 공급업체들은 엣지와 클라우드를 아우르는 규정 준수 툴킷을 제공해야 하는 압박을 받고 있습니다.

제조업이나 병원에서는 지연 시간이 중요한 검사 및 진단 업무에 엣지 서버를 도입하여, 익명화된 데이터를 클라우드 클러스터로 전송해 재훈련을 진행하고 있습니다. AI 인재를 채용하는 조직의 상당수가 비용, 규정 준수, 성과 간의 균형을 맞추기 위해 하이브리드 방식을 선호하고 있습니다. Dell Technologies나 HPE와 같은 인프라 벤더들은 AI에 최적화된 하드웨어와 오케스트레이션 소프트웨어를 묶어 제공함으로써, 하이퍼스케일러의 서비스와 연계된 새로운 수익원을 개척하고 있습니다. 구축 형태에 관계없이 단일 화면에서 정책 관리를 제공하는 벤더는 기업들이 사일로화된 관리 콘솔을 피하려는 경향이 있기 때문에 고객 유지율을 더욱 높일 것으로 기대됩니다.

지역별 분석

2025년, 북미는 전 세계 매출의 35.73%를 차지했으며, 시장 내 주도적인 지역으로서의 위상을 유지했습니다. 이러한 우위는 자동화에 대한 수요를 견인하는 높은 임금, 확립되고 성숙한 클라우드 생태계, 생산성 제품군을 위한 코파일럿의 급속한 도입 등 여러 요인에 기인합니다. 이러한 보조 조종사들은 업무 효율을 높이고 업무 흐름을 간소화하기 때문에 해당 지역의 기업들로부터 큰 관심을 받고 있습니다. 또한 북미는 전문적인 오케스트레이션 애드온의 개발과 공급을 적극적으로 지원하는 견고한 벤처 캐피털 생태계의 혜택을 누리고 있습니다. 이러한 애드온은 플랫폼의 기능성과 활용도를 한층 더 높여, 해당 지역 시장에서의 선도적 입지를 확고히 하고 있습니다.

아시아태평양은 가장 빠르게 성장하고 있는 지역으로, 2026-2031년 연평균 성장률(CAGR) 33.98%를 나타낼 것으로 전망됩니다. 기존 아웃소싱 거점에서의 임금 상승으로 인해 인건비 경쟁력이 약화되면서, 인도, 필리핀, 베트남의 기업들은 백오피스 업무의 자동화를 추진하고 있습니다. 정부의 지원책도 수요를 뒷받침하고 있습니다. 인도의 '인공지능 국가 전략'에서는 산업별 AI 도입 인센티브로 12억 달러가 책정된 반면, 일본의 보조금 프로그램에서는 중소 제조업체의 플랫폼 비용 중 최대 50%가 지원됩니다. 중국에서는 현지 벤더들이 AI 업무 지원 도구를 국내 협업 솔루션에 통합하여 외국산 클라우드에 대한 규제를 회피하고 있습니다.

유럽은 더 복잡한 상황에 직면해 있습니다. EU의 AI 법안은 고위험 도입에 대해 적합성 평가, 문서화, 시판 후 감시를 의무화하고 있으며, 이로 인해 6-12개월의 리드타임이 발생하고 규정 준수 예산이 증가하고 있습니다. 그럼에도 불구하고, 신뢰할 수 있는 AI 조사에 대한 공공 자금의 투입으로 인해 기업들은 자동화를 '선택지'가 아닌 '필연'으로 받아들이게 되었습니다. 남미의 성장은 브라질과 아르헨티나에 집중되어 있으며, 양국에서는 통화 변동성으로 인해 CFO들이 생산성 향상을 통해 리스크 헤지를 도모하고 있습니다. 사우디아라비아와 아랍에미리트(UAE)를 중심으로 한 중동의 구매자들은 전자정부 서비스에 AI 에이전트를 도입하여 서비스 제공 수준을 높이고 있습니다. 아프리카는 여전히 개발도상국이지만, 남아프리카공화국과 케냐에서는 지역 시스템 통합사업자와의 제휴를 통해 초기 성장세를 보이고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

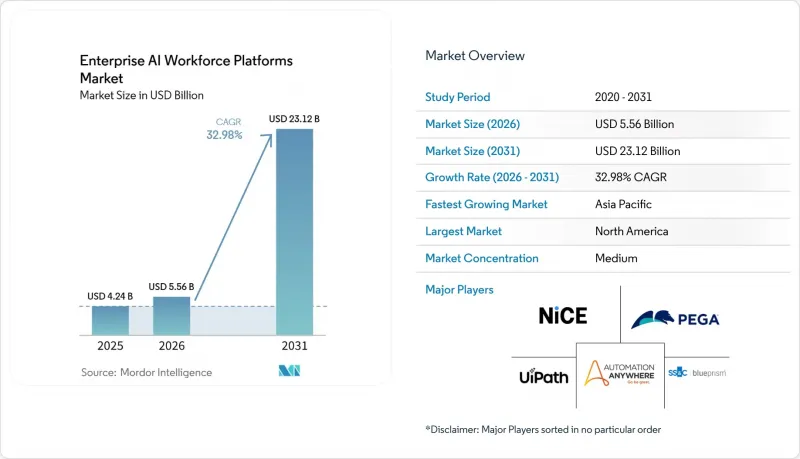

AJY 26.06.22According to Mordor Intelligence, the enterprise AI workforce platforms market size is projected to be USD 4.24 billion in 2025, USD 5.56 billion in 2026, and reach USD 23.12 billion by 2031, growing at a CAGR of 32.98% from 2026 to 2031.

This report is Segmented by Deployment Mode (On-Premise, Cloud, and Hybrid), Component (Software and Services), End-User Industry (IT and Telecom, Healthcare and Life Sciences, Manufacturing, BFSI, Retail and E-Commerce, Education, and More), Organization Size (Large Enterprises and Small and Medium Enterprises), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global Enterprise AI Workforce Platforms Market Trends and Insights

Integration of Generative AI Co-Pilots into Enterprise Productivity Suites

Embedding co-pilots inside familiar collaboration tools removes the hand-off between task identification and automation, allowing workers to invoke agents without leaving the application of record. Microsoft reported 1 million paying Copilot subscribers by January 2025 and indicated 29% time savings on document creation and meeting summarization tasks. Salesforce followed up with Agentforce, enabling non-technical staff to launch autonomous customer service agents that shortened resolution time by 40% in pilots. Tight integration raises switching costs because enterprises prefer bundled upgrades over separate procurement cycles. Compliance frameworks such as ISO/IEC 42001 are pushing vendors to certify embedded co-pilots, further cementing incumbent productivity-suite providers on buyer shortlists. Collectively, these dynamics front-load demand and support premium pricing during the first wave of adoption.

Rising Labor Cost Inflation Accelerating Automation ROI

Annual wage growth of 8-10% in India's IT services sector and 7-9% in the Philippines' call-center workforce during 2025 shrank the economic spread between human labor and autonomous agents. Breakeven periods for invoice-processing automation contracts are projected to decrease from 24 months in 2023 to 14 months in 2025. Vietnam's government reacted by creating a USD 200 million incentive fund for industrial AI deployments, signifying policy alignment with enterprise automation goals. As a result, CFOs now frame AI workforce investments as inflation hedges that stabilize operating margins. The fiscal logic reinforces multi-year budget allocations, especially within back-office functions where repetitive workflows dominate cost structures.

Persistent Data Residency and Sovereignty Concerns Limiting Cross-Border Deployments

The EU General Data Protection Regulation, China's Cybersecurity Law, and India's Digital Personal Data Protection Act prohibit unrestricted data transfer, compelling enterprises to adopt hybrid topologies with sovereign partitions. Compliance overhead elevates the total cost of ownership by requiring redundant stacks, contractual safeguards, and localized support teams. An International Association of Privacy Professionals survey found that 58% of multinationals postponed AI workforce deployments due to lingering uncertainty over legal transfer mechanisms. Vendors have responded with regionalized control planes and edge options, but premium pricing and maintenance complexity neutralize some of the cost savings that cloud models promise. The fragmentation risk is greatest in sectors that hold sensitive data, such as healthcare, banking, and public administration.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Adoption of Low-Code and No-Code AI Orchestration Platforms for Citizen Developers

- Availability of Pre-Built AI Workforce Skill Libraries from Independent ISVs

- Shortage of Domain-Specific AI Training Data for Non-English Knowledge Work

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Intelligent automation suites held 41.37% of 2025 revenue, confirming their role as the first step on most transformation roadmaps. Enterprises value the suites' integrated process mining and document intelligence modules, which surface high-ROI use cases and supply training data to models that handle exceptions. Vendors are folding conversational AI work assistants into the same stack, enabling the enterprise AI workforce platforms market size for agentic chatbots to climb rapidly in customer-facing scenarios. Skill development platforms, however, register the steepest climb at a 33.98% CAGR, reflecting a strategic pivot toward reskilling workers displaced by automation. Coursera logged a 180% enrollment jump in generative AI courses during 2025. That surge signals institutional commitment to internal talent marketplaces that match verified competencies with project needs across business lines.

Workforce analytics platforms now fuse predictive modeling with real-time productivity telemetry, encouraging proactive interventions before attrition or performance dips occur. Integrated talent marketplaces blend these insights with gig-style assignments, reducing idle time and improving internal mobility. Microsoft Viva's crossover success, 40 million monthly active users by late 2025, shows that employers want a unified pane of glass for learning, engagement, and analytics. Cross-suite convergence is intensifying competition,because buyers prefer end-to-end provisioning over stitching together point solutions. As convergence advances, the enterprise AI workforce platforms market share for standalone point products is likely to compress.

Cloud remained dominant at 63.52% in 2025 thanks to elastic consumption billing and rapid onboarding. Yet stricter localization laws and real-time inference needs are pushing organizations toward hybrid solutions, which are registering a 33.38% CAGR. Financial institutions now keep sensitive workloads on-premise while leveraging public clouds for analytics that fall outside supervisory scope. The EU AI Act's high-risk classification is catalyzing European buyers to enact similar split architectures, forcing vendors to offer compliance toolkits that span edge and cloud.

Manufacturers and hospitals are adopting edge servers for latency-critical inspection and diagnostic tasks, forwarding anonymized data to cloud clusters for retraining. A significant portion of AI workforce adopters prefer a hybrid approach to balance cost, compliance, and performance. Infrastructure vendors such as Dell Technologies and HPE are bundling AI-optimized hardware with orchestration software, opening a parallel revenue stream adjacent to hyperscaler services. Vendors that supply single-pane policy management across deployment types stand to gain incremental stickiness as enterprises avoid siloed admin consoles.

Geography Analysis

North America accounted for 35.73% of global revenue in 2025, maintaining its position as a leading region in the market. This dominance is attributed to several factors, including high wages that drive demand for automation, a well-established, mature cloud ecosystem, and the rapid adoption of productivity-suite co-pilots. These co-pilots enhance operational efficiency and streamline workflows, making them highly sought after by enterprises in the region. Additionally, North America benefits from a robust venture capital ecosystem that actively supports the development and supply of specialized orchestration add-ons. These add-ons further enhance platform functionality and utilization rates, solidifying the region's leadership in the market.

Asia-Pacific is the fastest-growing region, with a 33.98% CAGR projected for 2026-2031. Wage inflation in traditional outsourcing centers is shrinking the labor arbitrage cushion, prompting companies in India, the Philippines, and Vietnam to automate back-office tasks. Government programs reinforce demand. India's National Strategy for Artificial Intelligence earmarked USD 1.2 billion for sectoral AI adoption incentives, while Japan's subsidy program reimburses up to 50% of platform costs for small manufacturers. In China, local vendors integrate AI workforce tools into domestic collaboration suites, sidestepping foreign cloud restrictions.

Europe faces a more nuanced path. The EU AI Act imposes conformity assessments, documentation, and post-market monitoring for high-risk deployments, adding six-to-twelve-month lead times and inflating compliance budgets. Still, public funding for trustworthy AI research ensures that enterprises view automation as inevitable, not optional. South America's growth is concentrated in Brazil and Argentina, where currency volatility motivates CFOs to hedge with productivity gains. Middle East buyers, led by Saudi Arabia and the United Arab Emirates, embed AI agents in e-government services to raise service delivery standards. Africa remains nascent, although South Africa and Kenya display early momentum through partnerships with regional system integrators.

- UiPath Inc.

- Automation Anywhere, Inc.

- SS&C Blue Prism Group Ltd.

- WorkFusion, Inc.

- NICE Ltd.

- Pegasystems Inc.

- Kofax Inc.

- Appian Corporation

- AntWorks Pte Ltd.

- EdgeVerve Systems Limited

- IPsoft Inc. (d/b/a Amelia)

- Laiye Technology Ltd.

- Nintex Global Ltd.

- Cognigy GmbH

- Kore.ai, Inc.

- Aisera, Inc.

- Hyperscience Inc.

- Celonis SE

- Capacity LLC

- Soroco India Private Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Integration of Generative AI Co-Pilots into Enterprise Productivity Suites

- 4.2.2 Rising Labor Cost Inflation Accelerating Automation ROI

- 4.2.3 Rapid Adoption of Low-Code and No-Code AI Orchestration Platforms for Citizen Developers

- 4.2.4 Availability of Pre-Built AI Workforce Skill Libraries from Independent ISVs

- 4.2.5 Vendor Transition to Consumption-Based Pricing Aligning with Business Outcomes

- 4.2.6 Emergence of AI Governance Tooling Enabling Large-Scale Workforce Deployment

- 4.3 Market Restraints

- 4.3.1 Persistent Data Residency and Sovereignty Concerns Limiting Cross-Border Deployments

- 4.3.2 Shortage of Domain-Specific AI Training Data for Non-English Knowledge Work

- 4.3.3 Employee Resistance due to Job Displacement Anxiety and Union Pushback

- 4.3.4 High Energy and Carbon Footprint of Inference Workloads Curtailing ESG Ambitions

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Platform

- 5.1.1 Intelligent Automation Suites

- 5.1.2 Conversational AI Work Assistants

- 5.1.3 AI-Driven Skill Development Platforms

- 5.1.4 Workforce Analytics and Optimization Platforms

- 5.1.5 Integrated Talent Marketplace Platforms

- 5.2 By Deployment Model

- 5.2.1 Cloud

- 5.2.2 On-Premise

- 5.2.3 Hybrid

- 5.3 By Organization Size

- 5.3.1 Large Enterprises

- 5.3.2 Small and Medium Enterprises

- 5.4 By End-User Industry

- 5.4.1 IT and Telecom

- 5.4.2 BFSI

- 5.4.3 Healthcare and Life Sciences

- 5.4.4 Retail and E-Commerce

- 5.4.5 Manufacturing

- 5.4.6 Public Sector

- 5.4.7 Other End-User Industries

- 5.5 By Geography

- 5.5.1 North America

- 5.5.1.1 United States

- 5.5.1.2 Canada

- 5.5.1.3 Mexico

- 5.5.2 South America

- 5.5.2.1 Brazil

- 5.5.2.2 Argentina

- 5.5.2.3 Rest of South America

- 5.5.3 Europe

- 5.5.3.1 United Kingdom

- 5.5.3.2 Germany

- 5.5.3.3 France

- 5.5.3.4 Italy

- 5.5.3.5 Spain

- 5.5.3.6 Rest of Europe

- 5.5.4 Asia-Pacific

- 5.5.4.1 China

- 5.5.4.2 Japan

- 5.5.4.3 India

- 5.5.4.4 South Korea

- 5.5.4.5 Rest of Asia-Pacific

- 5.5.5 Middle East and Africa

- 5.5.5.1 Middle East

- 5.5.5.1.1 United Arab Emirates

- 5.5.5.1.2 Saudi Arabia

- 5.5.5.1.3 Rest of Middle East

- 5.5.5.2 Africa

- 5.5.5.2.1 South Africa

- 5.5.5.2.2 Egypt

- 5.5.5.2.3 Rest of Africa

- 5.5.5.1 Middle East

- 5.5.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 UiPath Inc.

- 6.4.2 Automation Anywhere, Inc.

- 6.4.3 SS&C Blue Prism Group Ltd.

- 6.4.4 WorkFusion, Inc.

- 6.4.5 NICE Ltd.

- 6.4.6 Pegasystems Inc.

- 6.4.7 Kofax Inc.

- 6.4.8 Appian Corporation

- 6.4.9 AntWorks Pte Ltd.

- 6.4.10 EdgeVerve Systems Limited

- 6.4.11 IPsoft Inc. (d/b/a Amelia)

- 6.4.12 Laiye Technology Ltd.

- 6.4.13 Nintex Global Ltd.

- 6.4.14 Cognigy GmbH

- 6.4.15 Kore.ai, Inc.

- 6.4.16 Aisera, Inc.

- 6.4.17 Hyperscience Inc.

- 6.4.18 Celonis SE

- 6.4.19 Capacity LLC

- 6.4.20 Soroco India Private Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment