|

시장보고서

상품코드

2065536

칩 렛 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Chiplet - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

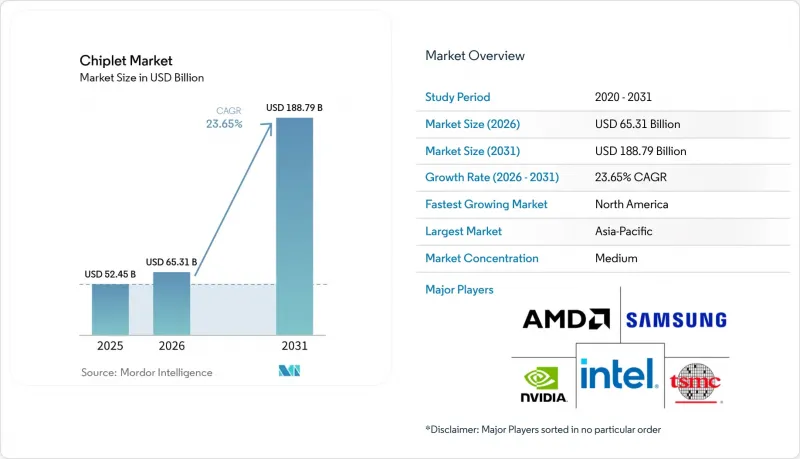

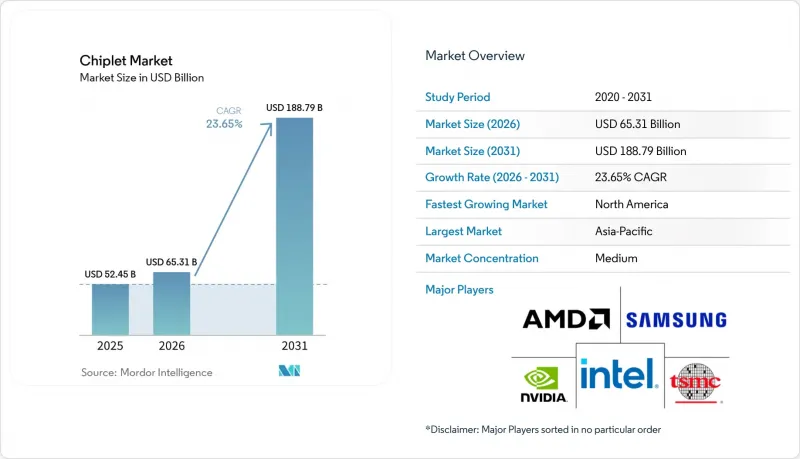

Mordor Intelligence에 의하면, 칩 렛 시장 규모는 2025년에 524억 5,000만 달러로 평가되었고, 2026년에 653억 1,000만 달러로 추정되고, 2031년까지 1,887억 9,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 23.65%로 성장할 전망입니다.

본 보고서는 프로세서 유형별(중앙처리장치(CPU), 그래픽 처리 장치(GPU) 등), 패키징 기술별(2.5D 인터포저 및 브리지 기반 패키징, 3D 적층 및 하이브리드 본딩 패키징 등), 최종 사용자 산업별(데이터센터 및 클라우드 컴퓨팅, 고성능 컴퓨팅, 자동차 및 모빌리티 등), 그리고 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 칩렛 시장 동향 및 인사이트

AI 및 HPC 분야의 레티클 한계 극복

치플렛 시장을 주도하고 있는 것은 최첨단 기술 분야에서 매우 대규모의 AI 및 HPC 프로세서를 단일 모노리식 다이로 구현하는 것이 더 이상 현실적이지 않다는 단순한 사실입니다. 연산 수요가 증가하는 가운데, 멀티다이 통합을 통해 설계자는 모든 기능을 하나의 거대한 실리콘 칩에 집적하지 않고도 로직, 메모리 액세스 및 I/O를 확장할 수 있게 됩니다. 이것이 바로 치플렛 시장이 현재 패키징 혁신뿐만 아니라 서버용 CPU 및 AI 가속기의 로드맵과도 밀접하게 연결되어 있는 이유입니다. AMD는 2026년 5월, 6세대 EPYC Venice 프로세서가 TSMC의 2nm 공정 기술로 양산에 들어갔다고 발표했습니다. 이는 치플렛 기반 CPU 설계가 차세대 서버용 칩을 향한 확실한 길로 자리매김하고 있음을 뒷받침하는 것입니다. 또한, 칩렛 시장은 재사용 가능한 소형 다이를 통해 최첨단 시스템 온 칩(SoC) 프로그램 전체에 자금을 투자할 수 없는 기업들의 경제적 장벽이 낮아진다는 점에서도 이점을 얻고 있습니다. 이러한 비용 및 수율 면에서의 우위 덕분에, 칩렛 설계는 하이엔드 분야의 선택지에서 벗어나, 고성능 컴퓨팅 프로그램 전반에 걸친 핵심 제품 전략으로 변모하고 있습니다.

HBM을 중심으로 한 2.5D 및 3D 패키지의 도입

또한, AI 시스템이 현재 고밀도 패키지 수준의 설계에서 연산 로직과 적층 메모리를 결합하고 있는 점도 치플렛 시장의 성장을 뒷받침하고 있습니다. 실제로 이는 첨단 패키지가 더 이상 보조적인 기능이 아니라, 디바이스 전체 성능의 핵심이 되어가고 있음을 의미합니다. 패키지 아키텍처가 트랜지스터 밀도와 마찬가지로 대역폭, 레이턴시, 확장 효율을 결정하는 요인이 되면서, 치플릿 시장은 이러한 변화의 혜택을 누리고 있습니다. 2025년 8월에 발표된 UCIe 3.0 사양에서는 지원되는 데이터 전송 속도가 48 GT/s 및 64GT/s로 두 배로 증가했으며, 사이드밴드의 도달 거리가 확장되고 새로운 관리 기능이 추가되었습니다. 이를 통해 향후 더욱 까다로운 멀티다이 패키지 설계에 대응하기가 쉬워질 것입니다. 이러한 개선이 중요한 이유는 메모리와 로직이 공정 후반부에 개별적으로 선정되는 것이 아니라, 패키지 수준에서 일체형으로 설계되는 사례가 늘어나고 있기 때문입니다. 그 결과, 치플렛 시장은 가속기 설계자, 패키징 전문가 및 메모리 공급업체 간의 보다 심도 있는 공동 개발 방향으로 나아가고 있습니다.

고밀도 패키지에서 발생하는 열 및 전력 공급의 병목 현상

칩렛 시장에서는 동일한 실적 내에 연산 리소스와 메모리가 더욱 집적됨에 따라, 열 관리 측면에서 명백한 기술적 한계에 직면하고 있습니다. 고밀도 2.5D 및 3D 패키지 설계는 대규모 데이터센터 환경을 제외하고는 표준 냉각 방식으로는 대응하기 어려운 열 부하를 발생시킵니다. 이는 칩렛 시장에 있어 직접적인 제약 요인이 됩니다. 왜냐하면 실리콘 자체는 출하 준비가 완료되었더라도 도입이 지연될 가능성이 있기 때문입니다. 2026년 2월 『Materials』지에 게재된 연구에 따르면, 치플릿 기반 이종 패키지에 대한 지능형 열 최적화를 통해 500 W/cm² 조건에서 열저항이 31%, 압력 손실이 42% 개선된 것으로 나타났으나, 여전히 기존의 냉각 방식이 아닌 내장형 마이크로플루이딕스 구조에 의존하고 있었습니다. 또한, 2025년 7월 『Scientific Reports』지에 게재된 논문에서는 2.5D 전력 네트워크에서 전기적·열적 공동 최적화를 통해 오류율을 4% 미만으로 낮출 수 있음이 밝혀졌으나, 이 방법에는 제조 과정의 복잡성과 비용이 크게 증가한다는 문제가 있습니다. 그 결과, 치플렛 시장은 하이퍼스케일 환경에서 여전히 가장 견조한 모습을 보이고 있는 반면, 보다 광범위한 기업으로의 확대는 여전히 더 우수한 열 관리 및 전원 공급 솔루션에 의존하고 있는 상황입니다.

부문별 분석

2025년 기준으로 CPU는 칩렛 시장 점유율의 34.54%를 차지한 반면, AI 가속기 ASIC은 2031년까지 연평균 성장률(CAGR) 25.43%를 나타낼 것으로 예측됩니다. 이러한 선도적인 위상은 기존 서버용 CPU의 대규모 구조와, 치플릿 기반 CPU 레이아웃이 클라우드 및 엔터프라이즈 환경에서의 도입에 있어 이미 그 효과가 입증되었습니다는 사실을 반영하고 있습니다. 따라서 치플렛 시장은 단기적인 수익원으로서 CPU에 의존하는 한편, 향후 성장의 주축으로 AI ASIC을 활용하고 있습니다. 2026년 5월 TSMC의 2nm 공정으로 ‘Venice’의 양산을 시작할 예정인 AMD의 지속적인 EPYC 로드맵을 통해 볼 때, 최첨단 서버용 CPU가 차세대 노드로 전환되는 과정에서 여전히 칩렛 분할 방식에 의존하고 있음을 알 수 있습니다. 또한, CPU 플랫폼은 구매자에게 익숙한 검증 경로를 제공함으로써, 완전히 새로운 가속기 카테고리에 비해 도입 위험이 줄어든다는 점에서도 칩렛 시장은 혜택을 보고 있습니다.

AI 가속기 ASIC의 확대가 가속화되고 있는 이유는 각 하이퍼스케일러 기업들이 범용 연산뿐만 아니라 특정 훈련 및 추론 워크로드에 최적화된 칩을 요구하고 있기 때문입니다. 이에 따라 칩렛 시장은 맞춤형 연산 타일, 특수한 메모리 구성, 그리고 각 도입 프로파일에 맞춘 보다 정교한 패키지 수준의 최적화 방향으로 나아가고 있습니다. AI 훈련 분야에서 GPU는 여전히 매출의 대부분을 차지하고 있지만, GPU, CPU, DPU, LPU 및 기타 가속기 간의 경계는 점점 더 모호해지고 있습니다. NVIDIA의 Vera Rubin 플랫폼은 하나의 시스템 아키텍처 내에 여러 프로세서 클래스를 통합하고 있으며, 이는 이종 통합을 통해 기존 프로세서 유형 간의 경계가 점차 모호해지고 있음을 보여줍니다. 따라서 치플렛 업계는 단일 카테고리의 순수 제품이 아닌 혼합 프로세서 플랫폼으로 전환되고 있습니다.

지역별 분석

2025년, 아시아태평양은 치플렛 시장 점유율의 35.93%를 차지했으며, 해당 시장에서 가장 규모가 큰 지역 거점이 되었습니다. 이 지역이 주도적인 위치를 차지하고 있는 이유는 대만이 선진적인 파운드리 생산 및 패키징 통합의 중심지로서의 위상을 유지하고 있으며, 한국이 주요 메모리 및 패키징 역량을 보완하고 있기 때문입니다. 또한, 칩렛 시장은 아시아태평양의 OSAT 및 기판 생태계의 발전 수준에 좌우되며, 이 생태계는 다른 지역에서는 거의 찾아볼 수 없는 규모의 양산을 뒷받침하고 있습니다. 2026년 5월 AMD가 발표한 TSMC의 2nm 공정에서 ‘Venice’ 생산에 관한 최신 정보는 대만이 첨단 서버 칩 프로그램의 핵심 실행 거점으로서의 역할을 더욱 공고히 하고 있음을 뒷받침하고 있습니다. 일본 역시 지역 공급망이 첨단 노드 제조 분야로 더욱 깊이 진출함에 따라, 장비, 소재 및 패키징 역량을 통해 치플릿 시장에서의 입지를 강화하고 있습니다. SEAJ의 예측에 따르면, 일본의 국내 반도체 장비 시장은 2026년도에 22% 성장할 것으로 전망되며, 이는 향후 패키징 및 칩 생산 능력을 위한 국내 파이프라인이 강화되고 있음을 시사합니다.

북미는 2031년까지 연평균 성장률(CAGR) 26.41%를 나타낼 것으로 예측되며, 치플렛 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 이러한 성장은 하이퍼스케일러, 팹리스 반도체 기업, 첨단 시스템 설계 기업의 집적, 그리고 국내 반도체 생산 능력에 대한 정책 주도형 투자에 힘입어 이루어지고 있습니다. 칩렛 시장이 북미에서 특히 활발한 이유는 제조가 여전히 아시아태평양에 걸쳐 이루어지고 있더라도 AI 시스템 아키텍처를 정의하는 기업의 상당수가 해당 지역에 거점을 두고 있기 때문입니다. Ayar Labs는 2026년 3월 5억 달러 규모의 시리즈 E 자금 조달을 완료했으며, 이 자금을 코패키지드 옵틱스의 생산 가속화와 대만 내 사업 확장에 사용할 것이라고 발표했습니다. 이는 아시아의 제조 활동과 연계된 설계 및 자본의 중심지로서 이 지역의 역할을 여실히 보여주고 있습니다. 또한, 2026년 3월에 발표된 NVIDIA와 Marvell의 NVLink Fusion 제휴는 맞춤형 XPU, 네트워크, 포토닉스를 중심으로 한 플랫폼 제휴가 북미의 치플릿 시장을 어떻게 형성해 나가고 있는지를 여실히 보여주고 있습니다.

유럽은 칩렛 시장에서 비교적 작은 점유율을 차지하고 있지만, 자동차, 산업, 항공우주, 보안 컴퓨팅과 같은 활용 사례를 통해 그 중요성이 커지고 있습니다. 해당 지역 수요 동향은 단순한 출하 규모보다는 검증된 용도 특화 멀티다이 솔루션을 중시하는 경향을 보이고 있습니다. 남미, 중동 및 아프리카는 칩렛 시장에서 여전히 초기 단계의 참여자로, 수요는 주로 수입된 AI 인프라 및 클라우드 데이터센터 구축과 관련되어 있습니다. 이 지역들은 현재로서는 아직 규모가 작지만, 하이퍼스케일러의 사업 범위가 확대되고 첨단 컴퓨팅 플랫폼이 더 많은 최종 시장에 보급됨에 따라 그 존재감은 점점 더 커질 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the chiplet market size is projected to be USD 52.45 billion in 2025, USD 65.31 billion in 2026, and reach USD 188.79 billion by 2031, growing at a CAGR of 23.65% from 2026 to 2031.

This report is Segmented by Processor Type (Central Processing Units (CPUs), Graphics Processing Units (GPUs), and More), Packaging Technology (2. 5D Interposer/Bridge-Based Packaging, 3D Stacked/Hybrid-Bonded Packaging, and More), End-User Industry (Data Centers and Cloud Computing, High-Performance Computing, Automotive and Mobility, and More), and Geography. The Market Forecasts in Provided in Terms of Value (USD).

Global Chiplet Market Trends and Insights

AI And HPC Reticle-Limit Escape

The chiplet market is being pushed forward by the simple fact that very large AI and HPC processors are no longer practical as single monolithic dies at the leading edge. As compute demand rises, multi-die integration gives designers a way to scale logic, memory access, and I/O without forcing every function onto one oversized piece of silicon. This is why the chiplet market is now closely tied to the server CPU and AI accelerator road map, not just to packaging innovation. AMD said in May 2026 that its 6th Gen EPYC Venice processor entered production on TSMC 2nm technology, which confirms that chiplet-based CPU design remains the proven path into next-generation server silicon. The chiplet market also benefits because smaller reusable dies lower the economic barrier for companies that cannot fund a full leading-edge system-on-chip program. That cost and yield advantage is turning chiplet design from a high-end option into a core product strategy across advanced compute programs.

HBM-Centered 2.5D And 3D Package Adoption

The chiplet market is also being lifted by the way AI systems now combine compute logic with stacked memory in dense package-level designs. In practice, that means advanced packages are no longer a supporting feature, they are becoming the performance center of the full device. The chiplet market gains from this shift because package architecture now decides bandwidth, latency, and scaling efficiency as much as transistor density does. The UCIe 3.0 specification released in August 2025 doubled supported data rates to 48 GT/s and 64 GT/s, extended sideband reach, and added new manageability features, which makes more demanding multi-die package designs easier to support over time. That improvement matters because memory and logic are increasingly being designed together at package level rather than selected separately late in the process. As a result, the chiplet market is moving toward deeper co-development between accelerator designers, packaging specialists, and memory suppliers.

Thermal And Power-Delivery Bottlenecks In Dense Packages

The chiplet market faces a clear engineering limit in thermal management as more compute and memory are packed into the same footprint. Dense 2.5D and 3D package designs create heat loads that standard cooling approaches struggle to handle outside the largest data center environments. This is a direct restraint on the chiplet market because deployment can be delayed even when the silicon itself is ready for shipment. A February 2026 study in Materials showed that intelligent thermal optimization for chiplet-based heterogeneous packages improved thermal resistance by 31% and pressure drop by 42% at 500 W/cm2, but it still depended on embedded microfluidic structures rather than conventional cooling methods. A July 2025 paper in Scientific Reports also showed that electrothermal co-optimization in 2.5D power networks can cut error rates below 4%, though it adds significant manufacturing complexity and cost. The result is that the chiplet market remains strongest in hyperscale settings, while broader enterprise rollout still depends on better thermal and power-delivery solutions.

Other drivers and restraints analyzed in the detailed report include:

- Advanced-Node NRE Reduction Through IP Reuse

- 5G, Cloud, And Networking Demand For Disaggregated Silicon

- Immature Cross-Vendor Interoperability And IP Liability

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

CPUs held 34.54% of chiplet market share in 2025, while AI accelerator ASICs are projected to grow at a 25.43% CAGR through 2031. That leadership reflects the scale of the existing server CPU base and the fact that chiplet-based CPU layouts are already proven in cloud and enterprise deployments. The chiplet market has therefore leaned on CPUs for near-term revenue while using AI ASICs as the main forward growth engine. AMD's continuing EPYC road map, including the May 2026 production ramp for Venice on TSMC 2nm, shows that advanced server CPUs still rely on chiplet partitioning to move into the next node generation. The chiplet market also benefits because CPU platforms give buyers a familiar validation path, which lowers adoption risk when compared with completely new accelerator categories.

AI accelerator ASICs are expanding faster because hyperscalers want silicon tuned for specific training and inference workloads rather than only general-purpose compute. That pushes the chiplet market toward custom compute tiles, specialized memory arrangements, and tighter package-level optimization for each deployment profile. GPUs still retain major revenue weight in AI training, yet the line between GPUs, CPUs, DPUs, LPUs, and other accelerators is becoming less distinct. NVIDIA's Vera Rubin platform combines multiple processor classes inside one system architecture, which shows how heterogeneous integration is blurring the old processor type boundaries. The chiplet industry is therefore moving toward mixed processor platforms rather than clean single-category products.

Geography Analysis

Asia-Pacific held 35.93% of chiplet market share in 2025, which made it the largest regional base for the chiplet market. The region leads because Taiwan remains central to advanced foundry output and package integration, while South Korea adds major memory and packaging capability. The chiplet market also depends on the depth of Asia-Pacific's OSAT and substrate ecosystem, which supports scale production in ways few other regions can match. AMD's May 2026 update on Venice production at TSMC 2nm reinforces Taiwan's role as the core execution hub for advanced server chip programs. Japan is strengthening its position in the chiplet market through equipment, materials, and packaging capacity as the regional supply chain moves deeper into advanced-node manufacturing. SEAJ projected that Japan's domestic semiconductor equipment market would grow 22% in fiscal 2026, which points to a stronger local pipeline for future packaging and chip fabrication capability.

North America is projected to expand at a 26.41% CAGR through 2031, making it the fastest-growing geography in the chiplet market. Growth is being driven by the concentration of hyperscalers, fabless chip companies, advanced system designers, and policy-led investment in domestic semiconductor capacity. The chiplet market is especially active in North America because many of the companies defining AI system architecture are based there, even when manufacturing still spans Asia-Pacific. Ayar Labs closed a USD 500 million Series E round in March 2026 and said it would use the funding to accelerate production of co-packaged optics and expand operations in Taiwan, which captures the region's role as a design and capital center connected to Asian manufacturing execution. The NVIDIA and Marvell NVLink Fusion partnership announced in March 2026 also highlights how the chiplet market in North America is being shaped by platform alliances around custom XPUs, networking, and photonics.

Europe holds a smaller position in the chiplet market, yet it is becoming more relevant through automotive, industrial, aerospace, and secure-compute use cases. The region's demand profile favors validated and application-specific multi-die solutions rather than sheer shipment scale. South America and the Middle East and Africa remain early-stage participants in the chiplet market, with demand tied mostly to imported AI infrastructure and cloud data center build-outs. These regions are still modest today, but they should become more visible as hyperscaler reach expands and advanced compute platforms spread into more end markets.

- Advanced Micro Devices, Inc.

- Intel Corporation

- NVIDIA Corporation

- Broadcom Inc.

- Marvell Technology, Inc.

- Taiwan Semiconductor Manufacturing Company Limited

- Samsung Electronics Co., Ltd.

- International Business Machines Corporation

- MediaTek Inc.

- Achronix Semiconductor Corporation

- Alphawave IP Group plc

- Ayar Labs, Inc.

- Rapidus Corporation

- Renesas Electronics

- Tenstorrent Holdings, Inc.

- SiFive, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 AI and HPC Reticle-limit Escape

- 4.2.2 Hbm-centered 2.5D/3D Package Adoption

- 4.2.3 Advanced-node NRE Reduction Through IP Reuse

- 4.2.4 5G, Cloud, and Networking Demand for Disaggregated Silicon

- 4.2.5 Optical I/O Chiplets for Rack-scale AI Scale-up

- 4.2.6 KGD Testing and UCIe Alliances De-risk Merchant Chiplets

- 4.3 Market Restraints

- 4.3.1 Thermal and Power-delivery Bottlenecks in Dense Packages

- 4.3.2 Immature Cross-vendor Interoperability and IP Liability

- 4.3.3 Yield Compounding and Test-cost Inflation in KGD Flows

- 4.3.4 CoWoS, Interposer, Substrate, and Optical-packaging Bottlenecks

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Rivalry Among Competitors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Processor Type

- 5.1.1 Central Processing Units (CPUs)

- 5.1.2 Graphics Processing Units (GPUs)

- 5.1.3 AI Accelerator ASICs

- 5.1.4 Field-Programmable Gate Arrays (FPGAs) and Adaptive SoCs

- 5.1.5 Networking and Data Processing Units (NPUs/DPUs)

- 5.1.6 Other Chiplet-Based Processor Types

- 5.2 By Packaging Technology

- 5.2.1 2.5D Interposer/Bridge-Based Packaging

- 5.2.2 3D Stacked/Hybrid-Bonded Packaging

- 5.2.3 Fan-Out/RDL-Based Advanced Packaging

- 5.2.4 Organic Substrate-Based Multi-Die Packaging

- 5.2.5 Other Packaging Technologies

- 5.3 By End-user Industry

- 5.3.1 Data Centers and Cloud Computing

- 5.3.2 High-Performance Computing

- 5.3.3 Consumer Computing

- 5.3.4 Automotive and Mobility

- 5.3.5 Telecommunications and Networking

- 5.3.6 Industrial and Edge AI

- 5.3.7 Aerospace and Defense

- 5.3.8 Other End-user Industries

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 Europe

- 5.4.2.1 Germany

- 5.4.2.2 United Kingdom

- 5.4.2.3 France

- 5.4.2.4 Italy

- 5.4.2.5 Rest of Europe

- 5.4.3 Asia-Pacific

- 5.4.3.1 China

- 5.4.3.2 Japan

- 5.4.3.3 South Korea

- 5.4.3.4 Taiwan

- 5.4.3.5 India

- 5.4.3.6 Rest of Asia-Pacific

- 5.4.4 South America

- 5.4.4.1 Brazil

- 5.4.4.2 Argentina

- 5.4.4.3 Rest of South America

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Rest of Middle East and Africa

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Vendor Positioning Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Advanced Micro Devices, Inc.

- 6.4.2 Intel Corporation

- 6.4.3 NVIDIA Corporation

- 6.4.4 Broadcom Inc.

- 6.4.5 Marvell Technology, Inc.

- 6.4.6 Taiwan Semiconductor Manufacturing Company Limited

- 6.4.7 Samsung Electronics Co., Ltd.

- 6.4.8 International Business Machines Corporation

- 6.4.9 MediaTek Inc.

- 6.4.10 Achronix Semiconductor Corporation

- 6.4.11 Alphawave IP Group plc

- 6.4.12 Ayar Labs, Inc.

- 6.4.13 Rapidus Corporation

- 6.4.14 Renesas Electronics

- 6.4.15 Tenstorrent Holdings, Inc.

- 6.4.16 SiFive, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Needs Assessment