|

시장보고서

상품코드

2066384

북미의 LED 패키지 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

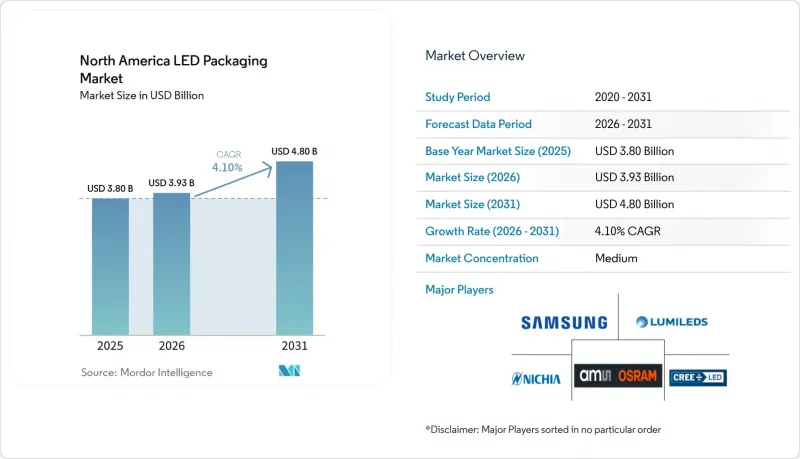

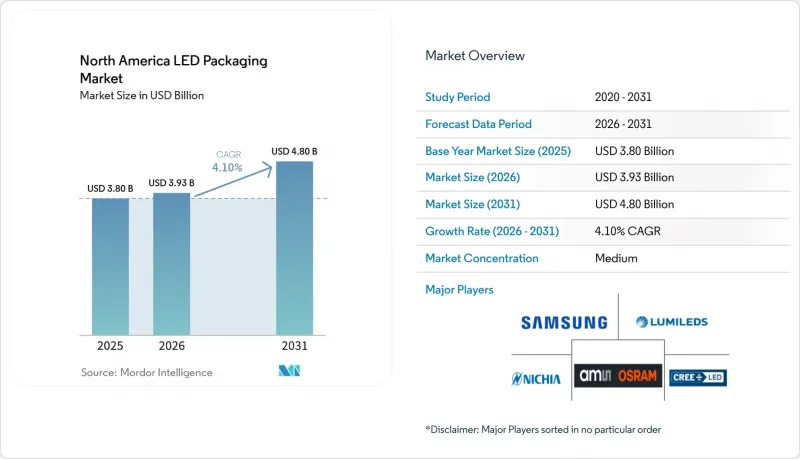

Mordor Intelligence에 의하면, 북미 LED 패키지 시장 규모는 2025년 38억 달러, 2026년 39억 3,000만 달러에서 2031년까지 48억 달러로 확대한다고 예측되고 있어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 4.10%를 나타낼 전망입니다.

본 보고서는 패키징 형태(SMD, COB, CSP, 플립칩, DIP 등), 전력 등급(저, 중, 고, 초고), 발광 유형(가시광선, 적외선, 자외선), 재료 화학(기판, 봉지재, 접합재, 형광체), 용도(일반 조명, 자동차, 디스플레이 등), 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 LED 패키지 시장 동향 및 분석

미니 LED 백라이트 수요의 급증

각 TV 및 모니터 브랜드는 2026년 1월에 개최된 소비자 가전 전시회(CES)에서 2,000만 대 이상의 미니 LED 백라이트 탑재 모델을 발표했습니다. 이는 디스플레이 1대당 10,000개 이상의 구역을 지원하는 패널 내 로컬 디밍을 실현하는 고밀도 LED 매트릭스의 급속한 보급을 뒷받침하는 것입니다. 미니 LED는 0.5 mm 미만의 피치로 배열된 100-200µm 크기의 극소형 다이를 사용하기 때문에 북미의 각 패키징 제조업체들은 높은 처리량의 본딩이 가능한, 정밀도 10µm 미만의 픽 앤 플레이스 시스템으로 설비를 교체하고 있습니다. 브리지럭스(BridgeLux)에 따르면, 디스플레이 통합 제조업체들이 칩 스케일 설계로 전환하는 가운데, 이 회사의 CSP2727 제품군은 현재 북미 CSP 출하량의 약 30%를 차지하고 있다고 합니다. 2025년 1월부터 시행되는 ‘Energy Star 9.0’ 규정에 따라 65인치 이상과 화면의 켜진 상태 전력 소비 기준이 강화되었으나, 미니 LED는 사용되지 않는 영역의 밝기를 99% 이상 낮출 수 있는 기능을 갖추고 있어, 제조업체는 최대 밝기를 낮추지 않고도 규정을 준수할 수 있습니다. 이러한 아키텍처의 전환은 리드 프레임을 제거하고, 패키지 높이를 1mm 미만으로 줄이며, 열 확산성을 향상시키는 칩 온 보드(COB) 모듈에도 유리하게 작용하고 있습니다. 부품 수가 급증하는 가운데, 백엔드 광학 보정이 병목 현상으로 대두되면서 백라이트 패널 전체를 60초 이내에 처리할 수 있는 자동 측광 테스트 스테이션에 대한 관심이 높아지고 있습니다.

자동차 헤드램프의 매트릭스 LED로의 전환

2022년, 어댑티브 드라이빙 빔 시스템이 FMVSS 108에 따라 미국 규제 당국의 승인을 획득함에 따라, 각 OEM 업체들은 매트릭스 헤드램프 도입을 급속히 가속화했습니다. 테슬라는 2025년형 ‘모델 Y’에 매트릭스 헤드램프를 탑재했으며, 리비안은 2024년 8월 R1T 및 R1S 트럭을 대상으로 무선 업데이트를 통해 이 기능을 활성화했습니다. ams OSRAM이 CES 2026에서 발표한 ‘EVIYOS 3.0’ 칩은 개별적으로 제어 가능한 2만 5,600개의 픽셀을 탑재하고 있어, 교통 상황에 맞추어 고해상도의 ‘라이트 카펫’을 생성하고 노면에 내비게이션 안내를 투사합니다. 이러한 모듈에는 접합부 온도가 125°C 이상인 플립칩 패키지 외에도, -40°C에서 +105°C 범위 내에서 색온도를 ±200 K 이내로 유지하는 광학 코팅이 필요합니다. 2024년에 공표된 ISO 26262 기능 안전 규격에서는 중복된 다이 아키텍처와 실시간 고장 감지가 의무화되어 있으며, 이로 인해 부품 원가가 최대 20% 증가하지만, 페일-사일런트 동작이 보장됩니다. 캐나다와 멕시코에서 규제 조화가 진행되는 가운데, 1차 조명 부품 공급업체들은 물류 비용과 환율 리스크를 최소화하기 위해 북미에서의 조립을 현지화하고 있습니다.

가격 하락이 매출총이익률을 압박하고 있습니다.

2025년, 범용 중출력 SMD LED의 평균 판매 가격은 전년 대비 8-12% 하락했습니다. 이는 아시아의 수탁 조립 제조업체들이 90%가 넘는 가동률로 생산을 진행하면서, 과잉 생산분을 시장에 대량으로 공급했기 때문입니다. 북미 기업들은 매출총이익률이 200-300 베이시스 포인트 하락함에 따라, 제조 거점 통합 및 구형 픽 앤 플레이스 설비의 감가상각을 앞당길 수밖에 없었습니다. CSP 및 플립칩 설계로의 전환으로 인해 리드 프레임 및 플라스틱 봉지 비용이 절감되므로 이러한 부담은 부분적으로 완화되겠지만, 대당 200만-300만 달러에 달하는 새로운 다이 부착 장비는 많은 지역 전문 제조업체들에게 감당하기 어려운 가격입니다. 업계 소문에 따르면, 특히 프리미엄 평균 판매 가격(ASP)을 유지할 수 있는 독자적인 형광체나 광학 코팅을 보유하지 않은 기업을 중심으로, 향후 18개월 동안 새로운 합병이나 자산 매각의 물결이 일어날 가능성이 높다고 합니다.

부문별 분석

표면 실장 소자는 기존의 픽 앤 플레이스 조립 라인의 방대한 도입 기반에 원활하게 부합하기 때문에 2025년 매출의 44.28%를 차지했으나, 칩 스케일 패키지(CSP)는 2031년까지 연평균 성장률(CAGR) 4.68%를 기록하며, 모든 경쟁 제품을 능가하는 성장이 예상됩니다. 북미의 CSP용 LED 패키지 시장 규모는 열저항이 30-40% 감소했다는 장점 덕분에, 실외용 조명 기구 제조업체들이 능동 냉각에 의존하지 않고도 구동 전류를 높일 수 있게 된 점이 호재로 작용하고 있습니다. 실제로 로스앤젤레스와 토론토의 가로등 설계자들로부터, 반사경의 깊이를 줄인 CSP 기판으로 전환함으로써 조명 기구의 무게가 최대 15% 감소했다는 보고가 접수되고 있습니다. 와이어 본딩이 필요 없는 플립 칩 방식도, 1,000 cd/mm²의 휘도와 마이크로초 단위의 조광이 요구되는 자동차 헤드램프 분야에서 보급이 확대되고 있습니다. 한편, 자동 표면 실장 라인이 보급됨에 따라 기존의 듀얼 인라인(DIL) 및 스루홀 패키지의 출하 점유율은 3% 미만으로 축소되었습니다.

2세대 CSP에서는 과도 전압 억제 다이오드와 패키지 내장 서미스터가 더욱 통합되어, 각 OEM 업체에 예측 정비를 위한 실시간 상태 데이터를 제공합니다. 이 기능은 조명 공급업체가 수년에 걸쳐 루멘 출력을 보장하는 ‘Lighting-as-a-Service(조명 서비스)’ 계약의 추세를 뒷받침하고 있습니다. 각 플립칩 제조업체들은 솔더 범프 위에 광도파로를 적층함으로써 적응형 드라이빙 빔 픽셀의 조립 과정을 간소화하고 있습니다. 이는 최고 수준의 안전 평가를 목표로 하는 자동차 제조업체에게 있어 필수적인 기능입니다. 한편, 칩 온 보드(COB) 공급업체들은 핫스팟을 형성하지 않고 100W의 열을 알루미늄 기판 전체에 분산시키는 능력을 바탕으로 원예 및 경기장 조명 시장에서 여전히 지배적인 위치를 유지하고 있지만, 베퍼 챔버 방식의 하이브리드 제품들이 이 틈새 시장에 서서히 진출하기 시작하고 있습니다.

0.5W에서 1W 사이의 중출력 LED는 2025년 매출의 39.18%를 차지하고 있으며, 개조용 전구 및 트로퍼 분야에서 Energy Star의 ‘1달러당 루멘’ 목표를 달성하기 위한 가장 경제적인 수단으로 자리매김하고 있습니다. 고출력 1-3W급 제품은 엄격한 비닝이 적용된 고플럭스 다이(die)가 필요한 매트릭스 방식 헤드램프 어레이 수요에 힘입어 연평균 성장률(CAGR) 4.99%를 나타낼 것으로 전망됩니다. 북미 LED 패키지 시장에서 고출력 디바이스의 점유율은 상승할 것으로 전망됩니다. 이는 전기차(EV) 플랫폼이 기존의 내연기관 차량에 비해 조명에 할당하는 전력 예산을 늘리고 있기 때문입니다. 저출력 표시기용 부품은 밝기보다 배터리 수명이 우선시되는 웨어러블 기기나 대시보드 아이콘 등에서 여전히 수요가 있습니다. 한편, 3W를 초과하는 초고출력 패키지는 경기장의 투광 조명이나 원예용 재배 랙에 도입되고 있습니다.

열 설계의 성패가 승자와 패자를 가르는 요인이 됩니다. 고출력 다이에서는 접합부의 온도를 110°C 이하로 유지하기 위해 증기 챔버 기판이나 소결 구리 베이스가 필요하지만, 이러한 재료는 BOM 비용을 20-30% 가중시킵니다. 방열 문제를 해결하지 못하는 공급업체는 실제 가동 주기에 따라 모듈이 3만 시간 이내에 L70을 초과할 경우, 보증 청구 위험에 직면하게 됩니다. Tier 1 공급업체들이 조달 시 열 임피던스 보고서 제출을 의무화하는 사례가 늘어나고 있으며, 이러한 변화는 대중화된 중출력 제품 라인에는 불리하게 작용하는 반면, 전문성이 높은 고출력 공급업체의 고객 유지율을 높이고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.29According to Mordor Intelligence, the north america lED packaging market size is projected to expand from USD 3.80 billion in 2025 and USD 3.93 billion in 2026 to USD 4.80 billion by 2031, registering a CAGR of 4.10% between 2026 to 2031.

This report is Segmented by Packaging Architecture (SMD, COB, CSP, Flip-Chip, DIP, and More), Power Class (Low, Mid, High, and Ultra-High), Emission Type (Visible, Infrared, and Ultraviolet), Material Chemistry (Substrates, Encapsulation, Bonding, and Phosphors), Application (General Lighting, Automotive, Display, and More), and Country. The Market Forecasts are Provided in Terms of Value (USD).

North America LED Packaging Market Trends and Insights

Surge In Mini-LED Backlighting Demand

Television and monitor brands unveiled more than 20 million mini-LED backlit units at the January 2026 Consumer Electronics Show, underscoring rapid adoption of dense LED matrices that deliver in-panel local dimming exceeding 10,000 zones per display. Mini-LEDs use dies as small as 100-200 µm placed on pitches below 0.5 mm, so North American packagers are re-tooling with sub-10 µm-accuracy pick-and-place systems capable of high-throughput bonding. Bridgelux reported its CSP2727 family now accounts for roughly 30% of the company's continental CSP shipments as display integrators migrate to chip-scale designs. Energy Star 9.0 limits, effective January 2025, tightened on-mode power for screens larger than 65 inches, and mini-LED's ability to dim unused zones by more than 99% helps manufacturers stay compliant without lowering peak brightness. The architectural shift also favors chip-on-board (COB) modules that eliminate lead frames, reduce package height under 1 mm, and improve thermal spreading. As component counts balloon, backend optical calibration emerges as a bottleneck, spurring interest in automated photometric testing stations that can process entire backlight panels in under 60 seconds.

Automotive Headlamp Shift To Matrix LED

Adaptive-driving-beam systems gained U.S. regulatory clearance under FMVSS 108 in 2022, and original equipment manufacturers quickly accelerated matrix headlamp rollouts. Tesla integrated matrix headlights into the 2025 Model Y, and Rivian activated the feature via over-the-air update in August 2024 for its R1T and R1S trucks. ams OSRAM's EVIYOS 3.0 chip, launched at CES 2026, packs 25,600 individually addressable pixels to create high-resolution light carpets that adapt to traffic and project navigation prompts onto pavement. These modules require flip-chip packages rated for junction temperatures above 125 °C, as well as optical coatings that hold color temperature within +-200 K from -40 °C to +105 °C. ISO 26262 functional-safety rules published in 2024 force redundant die architectures and real-time fault detection, adding up to 20% in bill-of-material cost but ensuring fail-silent behavior. As regulations harmonize across Canada and Mexico, tier-one lighting suppliers are localizing assembly in North America to minimize logistics overhead and currency-exchange exposure.

Price Erosion Pressuring Gross Margins

Average selling prices for commodity mid-power SMD LEDs fell 8-12% year-over-year in 2025 as Asian contract assemblers ran at utilization rates above 90% and flooded the market with excess output. North American players saw gross margins compress by 200-300 basis points, forcing manufacturing consolidation and accelerated depreciation of legacy pick-and-place assets. Migrating to CSP and flip-chip designs partially offsets the squeeze because lead-frame and plastic encapsulation costs disappear, but new die-attach tools priced at USD 2-3 million each are beyond reach for many regional specialists. Industry chatter suggests a new wave of mergers and asset sales is likely over the next 18 months, especially among firms lacking proprietary phosphors or optical coatings that can defend premium ASPs.

Other drivers and restraints analyzed in the detailed report include:

- U.S. CHIPS Act Incentives For Domestic LED Supply Chain

- Rapid Adoption Of CSP In High-Lumen Outdoor Fixtures

- Thermal-Management Challenges Beyond 3 W Packages

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount devices held 44.28% of 2025 revenue because they drop seamlessly into the vast installed base of pick-and-place assembly lines, yet chip-scale packages are forecast to outpace all rivals at a 4.68% CAGR through 2031. The North America LED Packaging market size for CSPs benefits from a 30-40% lower thermal resistance that lets outdoor fixture makers push drive currents without resorting to active cooling. In practice, streetscape engineers in Los Angeles and Toronto report fixture weight declines of up to 15% after switching to CSP boards that shrink reflector depth. Wire-bond-free flip-chip formats are also ascending in automotive headlamps where designers need 1,000 cd/mm2 intensity and microsecond dimming. Meanwhile, legacy dual-in-line and through-hole packages have retreated to fewer than 3% of shipments as automated surface-mount lines become universal.

Second-generation CSPs further integrate transient-voltage suppression diodes and on-package thermistors, giving OEMs real-time health data for predictive maintenance. This functionality supports the trend toward lighting-as-a-service contracts in which fixture vendors guarantee lumen output over multi-year periods. Flip-chip makers are layering optical waveguides atop solder bumps to simplify assembly of adaptive-driving-beam pixels, a feature essential for automakers chasing top safety ratings. Chip-on-board suppliers, meanwhile, continue to dominate horticultural and stadium lighting thanks to their ability to spread 100 W across aluminum substrates without hotspot formation, though vapor-chamber hybrids are beginning to nibble at that niche.

Mid-power LEDs between 0.5 W and 1 W controlled 39.18% of 2025 revenue as they remain the cheapest path to meet Energy Star lumen-per-dollar targets in retrofit bulbs and troffers. The high-power 1-3 W class is projected to chart a 4.99% CAGR, fueled by matrix headlamp arrays that need tightly binned, high-flux dies. The North America LED Packaging market share for high-power devices is set to climb as electric-vehicle platforms allocate larger electrical budgets to lighting than their internal-combustion predecessors. Low-power indicator parts hang on in wearables and dashboard icons where battery life trumps intensity, whereas ultra-high-power packages above 3 W are entering stadium floodlights and horticulture grow racks.

Thermal budgets separate winners from laggards. High-power dies demand vapor-chamber substrates or sintered copper bases to maintain junctions below 110 °C, yet those materials add 20-30% to BOM. Vendors that cannot solve heat extraction risk warranty claims when real-world duty cycles push modules past L70 in under 30,000 h. Tier-ones increasingly mandate thermal-impedance reports during sourcing, a shift that disadvantages commoditized mid-power lines but enhances the stickiness of specialized high-power suppliers.

List of Companies Covered in this Report:

- Nichia Corporation

- Cree LED, Inc.

- Samsung Electronics Co., Ltd.

- ams-OSRAM AG

- Lumileds Holding B.V.

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- Epistar Corporation

- Lextar Electronics Corp.

- Everlight Electronics Co., Ltd.

- Dominant Opto Technologies Sdn Bhd

- Stanley Electric Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lite-On Technology Corporation

- NationStar Optoelectronics Co., Ltd.

- Rohinni LLC

- Brightek Optoelectronic Co., Ltd.

- Loyal Group (Refond)

- Genesis Photonics Inc.

- Lumens Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Industry Value-Chain Analysis

- 4.3 Regulatory Landscape

- 4.4 Technological Outlook

- 4.5 Impact of Macroeconomic Factors

- 4.6 Porter's Five Forces Analysis

- 4.6.1 Bargaining Power of Suppliers

- 4.6.2 Bargaining Power of Buyers

- 4.6.3 Threat of New Entrants

- 4.6.4 Threat of Substitutes

- 4.6.5 Intensity of Competitive Rivalry

- 4.7 Market Drivers

- 4.7.1 Surge in Mini-LED Backlighting Demand

- 4.7.2 Automotive Headlamp Shift to Matrix LED

- 4.7.3 U.S. CHIPS Act Incentives for Domestic LED Supply Chain

- 4.7.4 Rapid Adoption of CSP in High-Lumen Outdoor Fixtures

- 4.7.5 Integration of UV-C LEDs in HVAC for Pathogen Control

- 4.7.6 Emerging Micro-LED Use in AR/VR Wearables

- 4.8 Market Restraints

- 4.8.1 Price Erosion Pressuring Gross Margins

- 4.8.2 Thermal-Management Challenges Beyond 3 W Packages

- 4.8.3 Dependence on Asia-Pacific Contract Packaging

- 4.8.4 Supply Risk of Rare-Earth Phosphors

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-line Package (DIP / Through-hole)

- 5.1.6 Others, Packaging Architecture

- 5.2 By Power Class

- 5.2.1 Low Power (Less Than 0.5 W)

- 5.2.2 Mid Power (0.5 to 1 W)

- 5.2.3 High Power (1 to 3 W)

- 5.2.4 Ultra-High Power (More Than 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared LED Packages

- 5.3.3 Ultraviolet LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display and Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

- 5.6 By Country

- 5.6.1 United States

- 5.6.2 Canada

- 5.6.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Cree LED, Inc.

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 ams-OSRAM AG

- 6.4.5 Lumileds Holding B.V.

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 Epistar Corporation

- 6.4.9 Lextar Electronics Corp.

- 6.4.10 Everlight Electronics Co., Ltd.

- 6.4.11 Dominant Opto Technologies Sdn Bhd

- 6.4.12 Stanley Electric Co., Ltd.

- 6.4.13 Toyoda Gosei Co., Ltd.

- 6.4.14 Lite-On Technology Corporation

- 6.4.15 NationStar Optoelectronics Co., Ltd.

- 6.4.16 Rohinni LLC

- 6.4.17 Brightek Optoelectronic Co., Ltd.

- 6.4.18 Loyal Group (Refond)

- 6.4.19 Genesis Photonics Inc.

- 6.4.20 Lumens Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment