|

시장보고서

상품코드

2066473

LED 패키징 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)LED Packaging - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

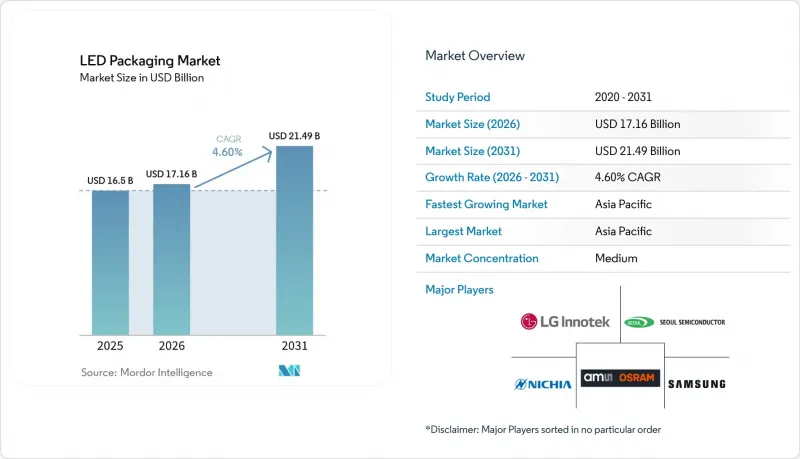

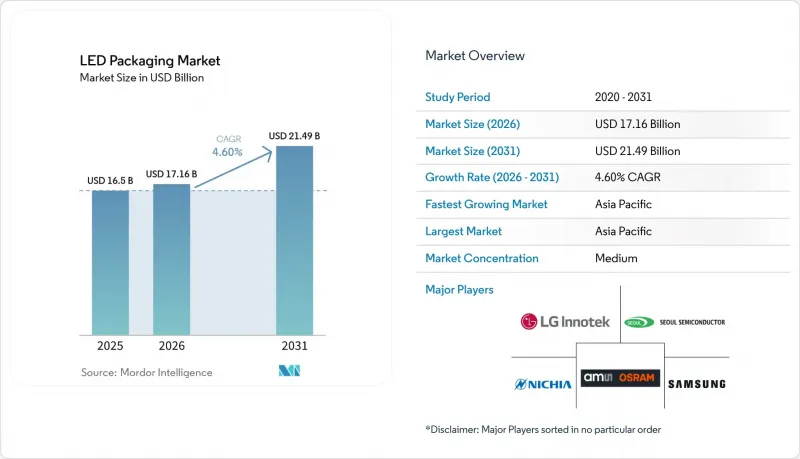

Mordor Intelligence에 의하면, LED 포장 시장 규모는 2025년 165억 달러로 평가되었고, 2026년 171억 6,000만 달러로 추정되고, 2031년까지 214억 9,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 4.60%를 나타낼 전망입니다.

본 보고서는 패키징 아키텍처별(칩 온 보드, 글라스 온 보드 등), 전력 등급별(중전력(0.5-1 W), 고전력(1-3 W) 등), 발광 유형별(가시광선 LED 패키징, 적외선 LED 패키징 등), 재료 화학별(기판, 봉지재 등), 용도별(일반 조명 등) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 LED 패키징 시장 동향 및 인사이트

IT 제품에서 Mini-LED 백라이트 채택이 급증하고 있습니다.

슬림형 노트북, 선명한 모니터, 고대비 태블릿에 대한 수요가 증가함에 따라 미니 LED 백라이트는 주류 생산 기술로 도약했습니다. 직접 라이트 방식의 패널 1장당에는 기존의 엣지 라이트 방식에 비해 5배에서 10배의 다이(die)가 필요하기 때문에 평균 판매 가격이 하락하고 있음에도 불구하고 총 소비량은 증가하고 있습니다. CSP 패키지는 1mm 미만의 피치, 낮은 Z축 높이, 그리고 정밀한 파장 비닝을 실현하고 있으며, 이러한 사양들은 현재 프리미엄 디스플레이 브랜드들이 기본 사양으로 지정하고 있습니다. 기가픽셀 단위의 처리량으로 광학 검사를 자동화하고, 미리 비닝 처리가 완료된 어레이를 출하하는 패키징 제조업체들이 가장 큰 가치를 창출하고 있는 반면, 수동 픽 앤 플레이스 플랫폼에 의존하는 기존 SMD 공급업체들은 경쟁에서 고전하고 있습니다.

자동차 업계에서 어댑티브 매트릭스 LED 헤드램프로의 전환이 가속화되고 있습니다.

자동차 OEM 업체들은 눈부심을 유발하지 않으면서 운전자의 시인성을 높이기 위해 매트릭스 및 픽셀 조명을 우선적으로 채택하고 있습니다. 아우디의 25,600픽셀 헤드램프 프로토타입은 차량용 발광 소자 수의 비약적인 증가를 상징하며, -40°C에서 +150°C의 온도 사이클을 견뎌내며, AEC-Q102를 준수하는 고출력 CSP 및 플립칩 패키지에 대한 수요를 촉진하고 있습니다. 유럽에서는 규정 123에 따라 가장 빠르게 보급이 진행되고 있어 지역 공급업체에 조기에 수익을 가져다주고 있는 반면, 미국에서는 국가도로교통안전국(NHTSA)의 눈부심 허용치에 대한 최종 결정을 기다리고 있는 상황입니다. 자동차 등급의 품질 관리 시스템을 갖춘 공급업체는 설계 채택을 확보하고, 수년에 걸친 생산 계약을 확실하게 따내고 있습니다.

플립칩 설계를 둘러싼, 장기화된 ‘특허 얽힘’ 소송으로 인한 비용

에버라이트, 닛야 화학공업, 서울반도체, 루미레즈는 계속해서 국경을 초월한 특허 침해 소송을 제기하고 있으며, 건당 평균 소송 비용은 500만 달러에 달할 전망입니다. 일실이익과 적정 로열티를 둘러싼 손해배상 논쟁은 불확실성을 높임으로써, 중소 진출기업들이 연구개발에 투자하기보다는 충당금을 계상할 수밖에 없게 만들고 있습니다. 기존 기업들 간의 교차 라이선싱은 장벽이 되어 신규 진입을 지연시킬 뿐만 아니라, 이미 확립된 포트폴리오의 수익화를 미루게 하고 있습니다.

부문별 분석

2025년, 표면 실장 소자 방식은 LED 패키징 시장 점유율의 43.45%를 차지한 것으로 평가되었으며, 이러한 우위는 수십 년에 걸친 자동 조립 인프라 구축에 기반을 두고 있습니다. CSP(칩 스케일 패키지)의 대체 기술은 리드 프레임과 성형 컴파운드를 배제하고, 두께를 0.5mm 미만으로 줄이는 동시에 광 추출 효율을 향상시킵니다. CSP의 매출액은 얇은 모듈이 필요한 미니 LED 백라이트 및 웨어러블 기기의 성장에 힘입어 연평균 성장률(CAGR) 5.11%로 증가하고 있습니다. 자동차 및 산업 분야의 구매 담당자들은 우수한 방열 경로를 확보하기 위해 칩 온 보드(COB) 및 플립 칩 배치를 유지하고 있지만, 소송 비용으로 인해 신속한 전환이 저해되고 있습니다. 통합 모듈 장치는 드라이버 IC와 이미터 어레이를 결합하여 부품 비용을 절감함으로써, 공급망 간소화를 중시하는 조명 기구 OEM 제조업체들로부터 지지를 받고 있습니다.

SMD 공급업체는 빠른 픽 앤 플레이스 처리 능력과 폭넓은 소켓 호환성을 통해 시장 점유율을 유지하고 있습니다. 그렇긴 하지만, 중국의 과잉 생산 능력으로 인한 가격 하락이 이익률을 압박하고 있어, CSP나 플립칩 패키지가 대량 생산에서 성능과 비용 면 모두에서 여유를 제공하는 고신뢰성 틈새 시장으로의 전환이 가속화되고 있습니다. 기존의 스루홀 및 듀얼 인라인 형식은 실외용 표시기나 특수한 개조 용도에서 점차 사라지고 있습니다.

중출력(0.5-1 W) 패키지는 일반 조명 개조 수요에 힘입어 2025년에는 LED 패키징 시장 규모의 37.67%를 차지했습니다. 고출력(1-3 W) 장치는 연평균 성장률(CAGR) 4.98%로 성장하고 있으며, 이는 적응형 매트릭스 헤드램프와 공장용 머신 비전 조명 기구가 각각 100루멘을 초과하는 개별 발광 소자와 고속 스위칭을 필요로 한다는 점을 반영한 것입니다. 3W를 초과하는 초고출력 유닛은 경기장, 원예 및 산업용 베이 분야에 널리 보급되고 있지만, 접합부에서 케이스까지의 열 목표치가 2°C/W 미만이기 때문에 소재는 구리 기판, 다이아몬드와 유사한 계면층, 나아가 마이크로채널 쿨러로 전환되고 있습니다.

소비 전력이 0.5 W인 표시등은 점점 더 대중화되어 가고 있으며, 가격이 대폭 하락하고 있습니다. AEC-Q102 인증이나 3,000회의 열 사이클을 견딜 수 있는 능력 등 엄격한 요건이 특징인 자동차 분야는 일반 소비자용 제품 라인과는 뚜렷이 구별됩니다. 이러한 차별화로 인해 제조업체는 각 전력 범주의 특정 요구 사항을 충족하기 위해 생산 공정을 정교화하고 최적화해야 합니다. 그 결과, 이러한 접근 방식을 통해 각 시장의 다양한 요건을 준수하기 위해 자본이 서로 다른 신뢰성 기준에 배분되게 됩니다.

지역별 분석

2025년, 아시아태평양은 LED 패키징 시장 점유율의 68.55%를 차지했으며, 에피택시 및 최종 모듈 조립을 동일한 거점에서 수행하는 중국 광둥성과 장쑤성의 수직 통합형 클러스터가 이를 주도했습니다. BOE Huacan사에 20억 위안(2억 8,000만 달러) 이상, Qianzhao Optoelectronics사에 대한 2억 1,557만 위안(3,000만 달러)의 투자는 다이당 비용을 절감하는 규모의 경제를 보여주는 한편, 지역 내 경쟁을 심화시키고 있습니다. 일본은 닛야 화학공업의 280nm 생산 라인과 아헨 자동차 혁신 센터를 통해 유럽의 OEM 제조업체들과의 제휴를 활용하여, 고효율 UV 및 자동차용 패키지에 주력하고 있습니다. 한국의 Samsung Electronics와 LG이노텍은 프리미엄 디스플레이 및 차량용 모듈을 겨냥한 플립칩 볼 그리드 어레이(BGA) 생산 라인에 6,000억 원(4억 5,000만 달러)을 투자하고 있습니다. 동남아시아에서 기업들이 지리적 리스크를 분산시키는 가운데, 말레이시아에 8,388만 달러를 투자한 아오얀 순창 공장이 가동을 시작했습니다.

북미에서는 규제 중심의 개조 및 특수 용도가 중시되고 있습니다. 2026년 1월 캐나다에서 수은 램프 사용이 금지됨에 따라 전국적으로 LED로의 급속한 전환이 요구되는 한편, 미국에서는 적응형 주행 빔에 관한 규제가 최종 확정되었습니다. 국내 패키징 기업들은 자동차, UV-C 살균, 그리고 산업용 신뢰성이라는 틈새 시장에 주력하고 있습니다. 유럽의 엄격한 에코디자인 규제와 어댑티브 헤드램프의 조기 승인으로 인해, 고출력 자동차용 인증을 받은 패키지에 대한 수요가 견조한 추세를 보이고 있습니다. 독일은 자동차 부품 조달 거점으로서 중요한 역할을 하고 있으며, 현지 1차 조명 제조업체가 일본 및 한국의 다이 공급업체와 공동으로 모듈을 개발하고 있습니다.

남미, 중동 및 아프리카의 경우, 합산하면 시장 점유율은 다소 낮은 편이지만, 상황에 따라 수요가 급증할 수 있습니다. 브라질에서는 건설업의 회복에 힘입어 일반 조명 판매량이 증가하고 있는 반면, 석유 자원이 풍부한 걸프 연안 국가들에서는 메가 프로젝트에 고루멘 패키지가 도입되고 있습니다. 남아프리카에서는 광업 및 산업 단지를 대상으로 내환경성이 뛰어난 IP65 규격의 모듈 사용이 의무화되어 있으며, 이집트에서는 전력망 제약이 있는 농촌 지역을 위해 저전력 태양광 가로등이 선호되고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.24According to Mordor Intelligence, the lED packaging market size is projected to expand from USD 16.50 billion in 2025 and USD 17.16 billion in 2026 to USD 21.49 billion by 2031, registering a CAGR of 4.60% between 2026 and 2031.

This report is Segmented by Packaging Architecture (Chip-On-Board, Glass-On-Board, and More), Power Class (Mid Power (0. 5 - 1 W), High Power (1 - 3 W), and More), Emission Type (Visible LED Packages, Infrared LED Packages, and More), Material Chemistry (Substrates, Encapsulation, and More), Application (General Lighting, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Global LED Packaging Market Trends and Insights

Surging Adoption of Mini-LED Backlights in IT Products

Demand for thinner laptops, vivid monitors, and high-contrast tablets has vaulted mini-LED backlighting into mainstream production. Each direct-lit panel requires five to ten times as many dies as its edge-lit predecessors, increasing total unit consumption even as average selling prices decline. CSP packages offer sub-millimeter pitch, low z-height, and tight wavelength binning, which premium display brands now specify as baseline. Packaging houses that automate optical inspection at gigapixel throughput and ship pre-binned arrays capture the most value, while legacy SMD suppliers reliant on manual pick-and-place platforms struggle to compete.

Accelerated Automotive Shift to Adaptive Matrix LED Headlamps

Automotive original equipment manufacturers (OEMs) have prioritized matrix and pixel lighting to improve driver visibility without glare. Audi's 25,600-pixel headlamp prototype exemplifies the jump in on-board emitter count, pushing high-power CSP and flip-chip packages that withstand -40 °C to +150 °C cycles and meet AEC-Q102. Europe advances fastest under Regulation 123, giving regional suppliers early revenue, while the United States awaits final glare thresholds from the National Highway Traffic Safety Administration. Suppliers with automotive-grade quality systems win design-ins and lock multi-year production contracts.

Persistent Patent-Thicket Litigation Costs for Flip-Chip Designs

Everlight, Nichia, Seoul Semiconductor, and Lumileds continue to file cross-border infringement suits, averaging USD 5 million in legal spend per case. Damages debates over lost profits versus reasonable royalties elevate uncertainty and force smaller entrants to allocate reserves rather than fund research and development. Cross-licensing among incumbents creates barriers that slow new entrants and extend monetization for established portfolios.

Other drivers and restraints analyzed in the detailed report include:

- Government Bans on Mercury-Based Lighting Products

- Rapid Fab Capacity Build-Out in China for Advanced CSP Lines

- Supply Tightness of High-CRI Red Phosphors

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Surface-mount device formats commanded 43.45% of the LED packaging market share in 2025, a lead built on decades of automated assembly infrastructure. CSP alternatives eliminate lead frames and mold compounds, shrinking profiles below 0.5 mm and boosting optical extraction. CSP sales climb on a 5.11% CAGR, pushed by mini-LED backlighting and wearable devices that demand thin modules. Automotive and industrial buyers retain chip-on-board and flip-chip arrangements for superior thermal paths, yet litigation costs temper rapid migration. Integrated-module devices combine driver integrated circuits with the emitter array, reducing the bill of materials and appealing to luminaire OEMs that favor supply-chain simplification.

SMD suppliers defend their share through high-speed pick-and-place throughput and pervasive socket compatibility. Nonetheless, price erosion from surplus Chinese capacity compresses margins, accelerating the shift toward high-reliability niches where CSP and flip-chip packages provide both performance and cost headroom at volume. Legacy through-hole and dual-in-line formats fade in outside indicator and specialty retrofits.

Mid-power 0.5-1 W packages captured 37.67% of the LED packaging market size in 2025, buoyed by general lighting retrofits. High-power 1-3 W devices expand at a 4.98% CAGR, reflecting adaptive matrix headlamps and factory machine-vision luminaires that each need individual emitters exceeding 100 lumens with rapid switching. Ultra-high-power units above 3 W penetrate stadium, horticulture, and industrial bays but carry junction-to-case thermal targets under 2 °C/W, steering materials toward copper substrates, diamond-like interface layers, or even microchannel coolers.

Indicators with a power consumption of 0.5 W are increasingly subject to commoditization and substantial price reductions. The automotive sector, characterized by its stringent requirements such as AEC-Q102 certification and the ability to withstand 3,000 thermal cycles, distinctly separates itself from consumer-grade product lines. This differentiation necessitates that manufacturers refine and optimize their production processes to cater to the specific demands of each power category. Consequently, this approach results in the allocation of capital to distinct reliability standards, ensuring compliance with the varying requirements of these markets.

Geography Analysis

Asia-Pacific retained 68.55% of the LED packaging market share in 2025, led by China's vertically integrated clusters in Guangdong and Jiangsu, which collocate epitaxy with final module assembly. Investments topping RMB 2 billion (USD 280 million) at BOE Huacan and RMB 215.57 million (USD 30 million) at Qianzhao Optoelectronics illustrate scale economies that lower per-die costs while intensifying regional price competition. Japan focuses on high-efficiency UV and automotive packages, leveraging Nichia's 280 nm line and its alliance with European OEMs through the Aachen Automotive Innovation Center. South Korea's Samsung Electronics and LG Innotek channel 600 billion won (USD 450 million) into flip-chip ball-grid-array lines that target premium displays and vehicle modules. Southeast Asia welcomes Malaysia's USD 83.88 million Aoyang Shunchang plant as firms diversify geographic risk.

North America emphasizes regulatory-driven retrofits and specialty applications. The January 2026 Canadian mercury lamp ban compels rapid LED conversions countrywide, while the United States finalizes adaptive driving beam regulations. Domestic packaging houses focus on automotive, UV-C sterilization, and industrial reliability niches. Europe's stringent Ecodesign rules and early adaptive headlamp approvals are driving steady demand for high-power, automotive-qualified packages. Germany anchors automotive sourcing, with local Tier-1 lighting firms co-developing modules with Japanese and Korean die suppliers.

South America, the Middle East, and Africa collectively represent modest shares but deliver situational spikes. Brazil's construction rebound lifts general lighting unit sales, while oil-rich Gulf states deploy high-lumen packages in mega-projects. South Africa mandates ruggedized IP65 modules for mining and industrial zones, while Egypt prefers low-power solar streetlights for grid-constrained rural districts.

- Nichia Corporation

- Samsung Electronics Co. Ltd.

- Seoul Semiconductor Co. Ltd.

- CreeLED Inc.

- Ams-Osram AG

- Lumileds Holding B.V.

- Everlight Electronics Co. Ltd.

- LG Innotek Co. Ltd.

- NationStar Optoelectronics Co. Ltd.

- Lextar Electronics Corp.

- Epistar Corporation

- Dominant Opto Technologies Sdn Bhd

- Toyoda Gosei Co. Ltd.

- Lite-On Technology Corporation

- Hongli Zhihui Group Co. Ltd.

- MLS Co. Ltd.

- Refond Optoelectronics Co. Ltd.

- Bridgelux Inc.

- San'an Optoelectronics Co. Ltd.

- Everlight Americas Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of Mini-LED Backlights in IT Products

- 4.2.2 Accelerated Automotive Shift to Adaptive Matrix LED Headlamps

- 4.2.3 Government Bans on Mercury-Based Lighting Products

- 4.2.4 Rapid Fab Capacity Build-Out in China for Advanced CSP Lines

- 4.2.5 On-Device Opto-Biometric Sensors Driving IR LED Demand

- 4.2.6 Emerging Horticulture Solid-State UV-B Illumination Systems

- 4.3 Market Restraints

- 4.3.1 Persistent Patent-Thicket Litigation Costs for Flip-Chip Designs

- 4.3.2 Supply Tightness of High-CRI Red Phosphors

- 4.3.3 Thermal-Management Challenges Above 3 W Ultra-High-Power Class

- 4.3.4 Price Erosion from Over-Capacity in Low-Power SMD Packaging

- 4.4 Industry Value-Chain Analysis

- 4.5 Technology Analysis

- 4.6 Regulatory Landscape

- 4.7 Impact of Macroeconomic Factors

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Packaging Architecture

- 5.1.1 Surface Mount Device (SMD)

- 5.1.2 Chip-on-Board (COB)

- 5.1.3 Chip Scale Package (CSP)

- 5.1.4 Flip-Chip LED Packages

- 5.1.5 Dual In-Line Package (DIP / Through-Hole)

- 5.1.6 Integrated Module Device (IMD)

- 5.1.7 Glass-on-Board (GOB)

- 5.1.8 Mini-LED Display Packaging

- 5.2 By Power Class

- 5.2.1 Low Power (Below 0.5 W)

- 5.2.2 Mid Power (0.5-1 W)

- 5.2.3 High Power (1-3 W)

- 5.2.4 Ultra-High Power (Above 3 W)

- 5.3 By Emission Type

- 5.3.1 Visible LED Packages

- 5.3.2 Infrared LED Packages

- 5.3.3 Ultraviolet LED Packages

- 5.4 By Material Chemistry

- 5.4.1 Substrates

- 5.4.2 Encapsulation

- 5.4.3 Bonding / Die-Attach

- 5.4.4 Phosphors / Coatings

- 5.5 By Application

- 5.5.1 General Lighting

- 5.5.2 Automotive Lighting

- 5.5.3 Display and Backlighting

- 5.5.4 Consumer Electronics

- 5.5.5 Industrial and Specialty

- 5.6 By Geography

- 5.6.1 North America

- 5.6.1.1 United States

- 5.6.1.2 Canada

- 5.6.1.3 Mexico

- 5.6.2 South America

- 5.6.2.1 Brazil

- 5.6.2.2 Argentina

- 5.6.2.3 Rest of South America

- 5.6.3 Europe

- 5.6.3.1 United Kingdom

- 5.6.3.2 Germany

- 5.6.3.3 France

- 5.6.3.4 Rest of Europe

- 5.6.4 Asia-Pacific

- 5.6.4.1 China

- 5.6.4.2 Japan

- 5.6.4.3 India

- 5.6.4.4 Southeast Asia

- 5.6.4.5 Rest of Asia-Pacific

- 5.6.5 Middle East

- 5.6.5.1 Saudi Arabia

- 5.6.5.2 United Arab Emirates

- 5.6.5.3 Turkey

- 5.6.5.4 Rest of Middle East

- 5.6.6 Africa

- 5.6.6.1 South Africa

- 5.6.6.2 Egypt

- 5.6.6.3 Rest of Africa

- 5.6.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co. Ltd.

- 6.4.3 Seoul Semiconductor Co. Ltd.

- 6.4.4 CreeLED Inc.

- 6.4.5 Ams-Osram AG

- 6.4.6 Lumileds Holding B.V.

- 6.4.7 Everlight Electronics Co. Ltd.

- 6.4.8 LG Innotek Co. Ltd.

- 6.4.9 NationStar Optoelectronics Co. Ltd.

- 6.4.10 Lextar Electronics Corp.

- 6.4.11 Epistar Corporation

- 6.4.12 Dominant Opto Technologies Sdn Bhd

- 6.4.13 Toyoda Gosei Co. Ltd.

- 6.4.14 Lite-On Technology Corporation

- 6.4.15 Hongli Zhihui Group Co. Ltd.

- 6.4.16 MLS Co. Ltd.

- 6.4.17 Refond Optoelectronics Co. Ltd.

- 6.4.18 Bridgelux Inc.

- 6.4.19 San'an Optoelectronics Co. Ltd.

- 6.4.20 Everlight Americas Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment