|

시장보고서

상품코드

2066665

건설용 접착제 및 실란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Construction Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

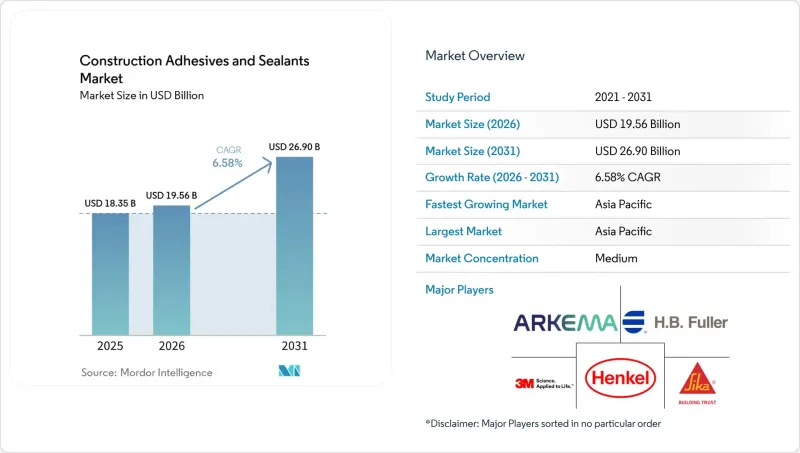

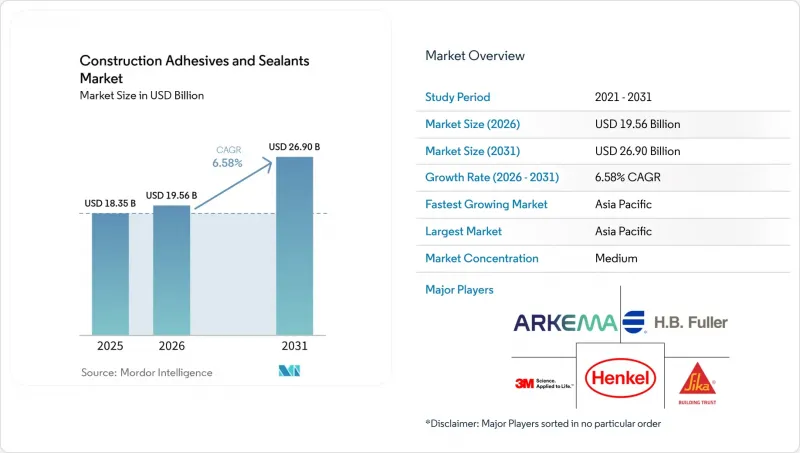

Mordor Intelligence에 의하면, 건설용 접착제 및 실란트 시장 규모는 2025년에 183억 5,000만 달러로 평가되었습니다. 2026년에 195억 6,000만 달러에 달하고, 2031년까지 269억 달러에 이를 것으로 예측되며, 2026년부터 2031년에 걸쳐 CAGR 6.58%로 성장할 전망입니다.

본 보고서는 수지(아크릴, 시아노아크릴레이트, 에폭시 등), 기술(수성, 용제계 등), 용도(바닥재·타일, 지붕재 등), 최종 용도(주택, 상업시설 등), 지역(아시아태평양, 북미, 유럽, 남미, 중동 및 아프리카)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계의 건설용 접착제 및 실란트 시장 동향 및 인사이트

그린빌딩 인증의 급증으로 저VOC 접착제 수요가 증가

2025년 전 세계 LEED 인증 획득 프로젝트 수는 전년 대비 14% 증가한 11만 건을 넘어섰으며, BREEAM 인증을 획득한 건물 수는 62만 동을 돌파했고, WELL 인증 획득 건수는 2023년 수준보다 3배 증가했습니다. 이들 모두는 접착제의 VOC 함량을 용제계 제품의 기준치보다 훨씬 낮게 유지하도록 의무화하고 있습니다. 2025년 중반에 시행될 캘리포니아주 규정 제1168호는 PVC, CPVC, ABS용 접착제의 VOC 상한치를 강화하여, 배합 제조업체들이 수성 및 반응형 시스템으로 전환하도록 유도하고 있습니다. EU는 2025년 4분기에 2026년 중반 시행을 목표로 하는 유사한 VOC 제한 조치를 발표했습니다. 이로 인해 프탈산계 가소제(pCBtF)의 단계적 폐지 및 t-부틸아세테이트 등의 용매가 배제됨에 따라, 사용 가능한 용매의 유형이 더욱 줄어들게 됩니다. 이에 대응하여 헨켈과 시카는 2025년 3월 공동 개발한 에폭시 경화제 시스템을 출시하여, 기존 제품에 비해 VOC 배출량을 90% 줄였습니다. 이러한 추세에 따라, 건설용 접착제 및 실란트 시장의 신규 상업 및 공공 프로젝트에서는 저VOC 화학 기술이 표준적인 선택지로 자리 잡고 있습니다.

미국, EU, 인도의 인프라 부양책

인도의 2026-27 회계연도 연방 예산에서는 인프라 정비에 11조 2,100억 루피(1,330억 달러)가 편성되어 전년 대비 11.4% 증가했습니다. 2026년 초에 착공된 36억 달러 규모의 개보수 공사인 브렌트 스펜스 교량 회랑 프로젝트에서는 ISO 11600 및 ASTM C920의 변위 내성 기준을 충족하는 고성능 이음매용 실란트 및 구조용 접착제가 필요합니다. 유럽 전역에서 에너지 효율 향상을 위한 개보수 의무화가 파사드용 실란트 수요를 견인하고 있으며, 헨켈이 2026년 2월에 웨더비 라록의 지분 과반수를 인수한 것도 이러한 개보수 붐을 염두에 둔 조치입니다. 대규모 유틸리티으로 인해 사양 기준이 상향 조정되면서 고가대의 배합 제품에 대한 수요가 증가하는 한편, 건설용 접착제 및 실란트 시장 전체의 가치 성장이 촉진되고 있습니다.

원유 가격에 연동되는 원자재 가격의 변동

MDI(메틸렌디페닐디이소시아네이트) 및 TDI(톨루엔디이소시아네이트)의 가격은 2026년 1월까지의 6개월 동안 약 40% 상승했습니다. 한편, 브렌트 원유 가격의 상승과 유럽의 가스 가격이 기준가의 3-4배 수준을 유지함에 따라, 폴리올 가격도 20-30% 상승하여 중소규모 배합 제조업체의 매출총이익률을 5-10퍼센트 포인트 하락시켰습니다. BASF와 같은 통합형 제조업체들은 자체 조달한 원료를 활용해 헤지 전략을 펼치고 있지만, 그럼에도 배럴당 20-30달러의 원유 가격 변동에 수익이 민감하게 반응한다는 점을 지적하고 있습니다. 이러한 가격 변동으로 인해 대두유나 재생 PET 유래 폴리올로의 원료 변경이 가속화되고 있지만, 지속가능성을 중시하는 고객들은 10-15%의 추가 비용을 부담하게 될 것입니다.

부문별 분석

2025년에 24.82%의 시장 점유율을 차지한 아크릴계 제품은 바닥재 및 실내 마감재 분야에서 여전히 비용 효율성이 뛰어난 선택지로 자리 잡고 있습니다. 폴리우레탄은 구조용 접합 분야에서 여전히 지배적인 위치를 차지하고 있지만, 이소시아네이트 표기를 피할 수 있는 하이브리드 폴리머에 의한 시장 잠식을 겪고 있습니다. 에폭시 수지는 하중을 지탱하는 보수 분야에서 틈새 시장을 유지하고 있는 반면, 바이오 리그닌 및 탄닌 계열 시스템은 5% 미만에 그치지만 두 자릿수 성장을 이룰 기반을 다지고 있습니다. 실리콘 제품은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.22%를 기록하며 성장할 것으로 예상되며, 이는 건설용 접착제 및 실란트 시장 전체의 성장률을 상회할 전망입니다. 이 제품의 ±50% 변형 능력과 극한 온도에 대한 내성은 초고층 빌딩이나 경기장의 커튼월 및 방수 용도에 대한 요구 사항을 충족시키고 있습니다. 다우(Dow)사가 2025년에 출시한 ‘DOWSIL 791’은 VOC 함량이 45 g/L이며, 사용 후 소비자 재활용 카트리지를 채택함으로써 제품에 내재된 탄소 배출량을 30% 감축했습니다.

실리콘의 높은 가격대는 수명 주기 비용을 절감해 주는 25년 보증으로 상쇄되고 있습니다. 고온 다습한 지역에서는 용제계 시스템의 조기 고장이 잇따르자, 건축가들이 폴리우레탄보다 실리콘을 지정하는 경향이 강해지고 있습니다. 한편, 저모노머 함량을 요구하는 규제 움직임에 따라 공급업체들은 폴리우레탄 프리폴리머의 재설계를 추진하고 있으며, 이러한 조치로 인해 실리콘과의 성능 격차는 줄어들고 있지만 비용은 상승하고 있습니다. 이러한 변화들이 맞물리면서, 건설용 접착제 및 실란트 시장에서 실리콘의 점유율 확대가 가속화되고 있습니다.

수성 화학제품은 2025년에 59.27%의 시장 점유율을 차지했으며, 캘리포니아주의 ‘규칙 1168’과 EU의 2026년 VOC 상한 규제의 영향으로 2031년까지 연평균 6.75%의 성장률을 기록하며 확대될 것으로 전망됩니다. 헨켈이 2026년 1월, 제품 포트폴리오의 90%가 수성 제품인 ATP Adhesive Systems를 인수한 것은 이 플랫폼으로의 자본 이동을 여실히 보여주고 있습니다. 용제계 제품은 배출 규제 준수에 비해 경화 속도가 더 중요시되는 산업용 틈새 시장으로 후퇴하고 있습니다. 반응형 시스템, 특히 2액형 폴리우레탄이나 에폭시 수지는 고하중 구조용 접착 분야에서 여전히 필수적이지만, 핫멜트는 자동화된 모듈식 공장에서 점차 입지를 넓혀가고 있습니다.

수성화로 전환하기 위해서는 스테인리스 스틸 혼합 탱크와 온도 조절이 가능한 보관 시설이 필요하며, 이러한 설비 투자는 소규모 기업보다는 대형 도급업체나 모듈 제조업체에 유리하게 작용합니다. 그 대가로, 도급업체는 가연성 물질 감소 및 VOC 노출량 감소에 따라 보험료 인하라는 혜택을 얻을 수 있습니다. 이러한 구조적 우위가 건설용 접착제 및 실란트 시장에서 수성 기술이 타 기술을 앞서는 실적을 올리고 있는 배경이 되고 있습니다.

지역별 분석

아시아태평양은 2025년 기준으로 건설용 접착제 및 실란트 시장의 46.74%에 불과했으나, 2031년까지 연평균 성장률(CAGR) 6.89%를 나타낼 것으로 전망됩니다. 중국 주택 시장의 침체로 인해 2025년 12월 투자액이 전년 동월 대비 17.2% 감소했고, 가격이 2021년 정점 대비 40% 하락한 것이 수요를 위축시키고 있습니다. 한편, 인도의 1,330억 달러 규모의 인프라 투자와 동남아시아의 도시화가 구조용 실란트 및 방수재의 소비를 견인하고 있습니다. 또한, 에너지 효율 및 내진 기준을 충족하기 위한 일본과 한국의 개보수 공사는 고급 실리콘 제품의 판매를 더욱 촉진하고 있으며, 피디라이트사는 신규 생산 능력 확대를 통해 국내 주택 시장의 성장을 기대하고 있습니다.

북미에서는 주택 착공 건수의 견조한 증가세와 모듈식 건축의 확산에 힘입어 시장이 명목상 속도로 확대되고 있습니다. 2025년에 완료된 헨켈사의 미시시피주 브랜든에서 진행된 3,000만 달러 규모의 설비 현대화 사업과, 2026년 1월에 발표된 시카사의 텍사스주 실리에서 진행될 9,000만 달러 규모의 확장 계획이 해당 지역의 생산 능력을 강화하고 있습니다. 36억 달러 규모의 브렌트 스펜스 다리 사례는 메가 프로젝트가 실런트 수요를 어떻게 확대시키는지를 보여주고 있는 반면, 규정 1168과 같은 VOC 규제는 제품의 재조성 및 설비 업그레이드를 촉진하고 있습니다.

유럽은 에너지 비용의 압박에 직면해 있지만, ‘Fit-for-55’ 목표에 따라 꾸준한 개조 수요를 누리고 있습니다. EU가 2026년 중반에 도입할 VOC 상한 규제로 인해 수성 도료로의 전환이 가속화되고 있으며, 헨켈이 웨더비 라록의 지분을 인수함에 따라 노후화된 주택 재고의 외관 보수에 대비한 체제가 갖춰졌습니다. 시카사가 튀르키예에 본사를 둔 아킴사를 2억 2,000만 스위스 프랑(2억 6,554만 달러)에 인수함으로써, 동유럽, 중동 및 아프리카 시장을 대상으로 한 비용 효율성이 뛰어난 거점이 구축되었습니다. 남미 및 GCC(걸프협력회의) 지역에서는 주택 건설의 확대와 고성능 실란트가 필요한 혹독한 기후에 노출된 인프라 회랑의 구축을 통해 추가적인 성장이 예상됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the construction adhesives & sealants market size is projected to be USD 18.35 billion in 2025, USD 19.56 billion in 2026, and reach USD 26.90 billion by 2031, growing at a CAGR of 6.58% from 2026 to 2031.

This report is Segmented by Resin Type (Acrylic, Cyanoacrylate, Epoxy, and More), Technology (Water-Borne, Solvent-Borne, and More), Application (Flooring and Tiling, Roofing, and More), End-Use Sector (Residential, Commercial, and More), and Geography (Asia-Pacific, North America, Europe, South America, and Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Global Construction Adhesives And Sealants Market Trends and Insights

Surge in Green-Building Certifications Driving Low-VOC Adhesive Demand

Global LEED certifications topped 110,000 projects in 2025, up 14% year over year, while BREEAM certifications surpassed 620,000 buildings, and WELL certifications tripled from 2023 levels, each mandating adhesive VOC levels well below solvent-borne thresholds. California's Rule 1168, effective mid-2025, tightened VOC caps for PVC, CPVC, and ABS cements, pushing formulators toward water-borne and reactive systems. The EU announced parallel VOC limits in Q4 2025 for mid-2026 enforcement, eliminating phthalate plasticizers such as phase-out of phthalate-based plasticizers (pCBtF) and solvents like t-butyl acetate, further shrinking the solvent palette. In response, Henkel and Sika launched joint epoxy hardener systems in March 2025, delivering 90% lower VOC emissions than incumbent products. These developments position low-VOC chemistries as the default for new commercial and institutional projects in the Construction Adhesives and Sealants market.

Infrastructure Stimulus Packages in the US, EU, and India

India's FY 2026-27 Union Budget earmarked INR 11.21 trillion (USD 133 billion) for infrastructure, up 11.4% year over year. The Brent Spence Bridge Corridor, a USD 3.6 billion overhaul begun in early 2026, will require high-performance joint sealants and structural adhesives that meet ISO 11600 and ASTM C920 movement ratings. Across Europe, energy-efficiency retrofit mandates are driving facade-sealant demand, and Henkel's February 2026 majority stake in Wetherby Laroc targets this renovation wave. Large public works elevate specification standards, reinforcing premium-priced formulations and lifting overall value growth in the Construction Adhesives and Sealants market.

Crude-Oil-Linked Raw-Material Price Volatility

MDI (Methylene Diphenyl Diisocyanate) and TDI (Toluene Diisocyanate) prices climbed roughly 40% in the six months to January 2026, while polyols rose 20-30% as Brent crude rallied and European gas settled at 3-4 times baseline, slicing 5-10 percentage points from gross margins of smaller formulators. Integrated producers such as BASF hedge through captive feedstocks, yet even they flag earnings sensitivity to USD 20-30/barrel oil swings. The volatility accelerates reformulation toward soybean-oil and recycled-PET polyols, albeit at 10-15% cost premiums borne by sustainability-minded customers.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Uptake of Off-Site Modular Construction

- 3D-Printed Concrete Requiring Tailormade Bonding Agents

- Tightening Global VOC Emission Limits on Solvent-Borne Systems

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Acrylics, which held 24.82% share in 2025, remain the cost-effective choice for flooring and interior trim. Polyurethanes still dominate structural joints but face encroachment from hybrid polymers that avoid isocyanate labeling. Epoxies retain a niche in load-bearing repairs, while bio-based lignin and tannin systems occupy a sub-5% but double-digit-growth foothold. Silicone products are projected to grow at 7.22% CAGR during 2026-2031, eclipsing the broader construction adhesives & sealants market. Their +-50% movement capability and extreme-temperature resilience meet the demands of curtain-wall and weatherproofing applications in skyscrapers and stadiums. Dow's DOWSIL 791, released in 2025, delivers VOC at 45 g/L and uses post-consumer-recycled cartridges that cut embodied carbon by 30%.

Silicone's premium pricing is offset by 25-year warranties that reduce life-cycle cost. Architects in hot-humid geographies increasingly specify silicone over polyurethane after early failures of solvent-borne systems. Meanwhile, regulatory momentum behind low-monomer content is prompting suppliers to re-engineer polyurethane prepolymers, a step that narrows the benchmark gap with silicone but raises costs. Collectively, these shifts reinforce silicone's climb within the Construction Adhesives and Sealants market.

Water-borne chemistries captured 59.27% share in 2025 and are forecast to compound at 6.75% through 2031, aided by California's Rule 1168 and the EU's 2026 VOC ceiling. Henkel's January 2026 deal for ATP Adhesive Systems, whose portfolio is 90% water-based, illustrates the capital pivot toward this platform. Solvent-borne lines retreat to industrial niches where cure speed overrides emissions compliance. Reactive systems, especially two-component polyurethanes and epoxies, remain essential for heavy-duty structural bonds, while hot-melts gain ground in automated modular factories.

The water-borne shift demands stainless-steel mixing tanks and climate-controlled storage, upgrades that favor large contractors and module fabricators over small firms. In return, contractors gain lower insurance premiums tied to reduced flammability and VOC exposure. These structural advantages underpin the outperformance of water-borne technology within the Construction Adhesives and Sealants market.

Geography Analysis

Asia-Pacific held only 46.74% of the Construction Adhesives and Sealants market in 2025, yet is forecast to post 6.89% CAGR to 2031. China's residential downturn, investment down 17.2% year over year in December 2025 and prices off 40% from 2021 peaks, dampens demand. Offsetting this, India's USD 133 billion infrastructure outlay and Southeast-Asian urbanization spur structural-sealant and waterproofing consumption. Japanese and Korean retrofits to meet energy-efficiency and seismic codes further buoy premium silicone sales, while Pidilite's new capacity targets domestic housing growth.

North America is expanding at a nominal pace, lifted by housing-start resilience and modular construction. Henkel's USD 30 million Brandon, Mississippi, upgrade, completed in 2025, and Sika's USD 90 million Sealy, Texas, expansion announced in January 2026, reinforce regional capacity. The USD 3.6 billion Brent Spence Bridge illustrates how megaprojects amplify sealant requirements, while VOC rules such as Rule 1168 drive reformulations and equipment upgrades.

Europe faces energy-cost pressure yet enjoys steady renovation demand under Fit-for-55 targets. The EU's mid-2026 VOC ceiling accelerates water-borne migration, and Henkel's Wetherby Laroc stake positions it for facade upgrades in aging housing stock. Sika's CHF 220 million (USD 265.54 million) purchase of Turkey-based Akkim builds a cost-efficient hub for Eastern Europe, the Middle East, and Africa. South America and the GCC (Gulf Cooperation Council) add incremental growth via residential expansion and infrastructure corridors exposed to extreme climates that need high-performance sealants.

- 3M

- Aica Kogyo Co. Ltd.

- Arkema

- Astral Adhesives

- BASF

- Dow

- DAP Global Inc.

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- MAPEI S.p.A.

- Momentive

- Pidilite Industries Ltd.

- PPG Industries Inc.

- RPM International

- Saint-Gobain

- Shin-Etsu Chemical Co., Ltd.

- Sika AG

- Soudal Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surge in green-building certifications driving low-VOC adhesive demand

- 4.2.2 Infrastructure stimulus packages in the US, EU and India

- 4.2.3 Rapid uptake of off-site modular construction

- 4.2.4 3D-printed concrete requiring tailormade bonding agents

- 4.2.5 Low-monomer PU prepolymers to meet indoor-air labels

- 4.2.6 Smart-sensor-embedded sealants for structural-health monitoring

- 4.3 Market Restraints

- 4.3.1 Crude-oil linked raw-material price volatility

- 4.3.2 Tightening global VOC emission limits on solvent-borne systems

- 4.3.3 Skilled-applicator shortage causing hybrid-sealant failures

- 4.3.4 Bio-adhesive uptake in engineered-wood construction

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value and Volume)

- 5.1 By Resin Type

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Reactive

- 5.2.4 Hot-melt

- 5.2.5 Sealants (1K and 2K)

- 5.3 By Application

- 5.3.1 Flooring and Tiling

- 5.3.2 Roofing

- 5.3.3 Wall Panels and Facades

- 5.3.4 Insulation and Weatherproofing

- 5.3.5 Infrastructure Joints (bridges and tunnels)

- 5.4 By End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Infrastructure

- 5.5 By Geography

- 5.5.1 Asia-Pacific

- 5.5.1.1 China

- 5.5.1.2 Japan

- 5.5.1.3 India

- 5.5.1.4 South Korea

- 5.5.1.5 Indonesia

- 5.5.1.6 Australia

- 5.5.1.7 Malaysia

- 5.5.1.8 Thailand

- 5.5.1.9 Singapore

- 5.5.1.10 Rest of Asia-Pacific

- 5.5.2 North America

- 5.5.2.1 United States

- 5.5.2.2 Canada

- 5.5.2.3 Mexico

- 5.5.3 Europe

- 5.5.3.1 Germany

- 5.5.3.2 France

- 5.5.3.3 Italy

- 5.5.3.4 Spain

- 5.5.3.5 United Kingdom

- 5.5.3.6 Russia

- 5.5.3.7 Rest of Europe

- 5.5.4 South America

- 5.5.4.1 Brazil

- 5.5.4.2 Argentina

- 5.5.4.3 Rest of South America

- 5.5.5 Middle East and Africa

- 5.5.5.1 Saudi Arabia

- 5.5.5.2 United Arab Emirates

- 5.5.5.3 South Africa

- 5.5.5.4 Rest of Middle East and Africa

- 5.5.1 Asia-Pacific

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Aica Kogyo Co. Ltd.

- 6.4.3 Arkema

- 6.4.4 Astral Adhesives

- 6.4.5 BASF

- 6.4.6 Dow

- 6.4.7 DAP Global Inc.

- 6.4.8 Franklin International

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers

- 6.4.13 MAPEI S.p.A.

- 6.4.14 Momentive

- 6.4.15 Pidilite Industries Ltd.

- 6.4.16 PPG Industries Inc.

- 6.4.17 RPM International

- 6.4.18 Saint-Gobain

- 6.4.19 Shin-Etsu Chemical Co., Ltd.

- 6.4.20 Sika AG

- 6.4.21 Soudal Group

- 6.4.22 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment