|

시장보고서

상품코드

2066669

중동 및 아프리카의 건설용 접착제 및 실란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Middle East And Africa Construction Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

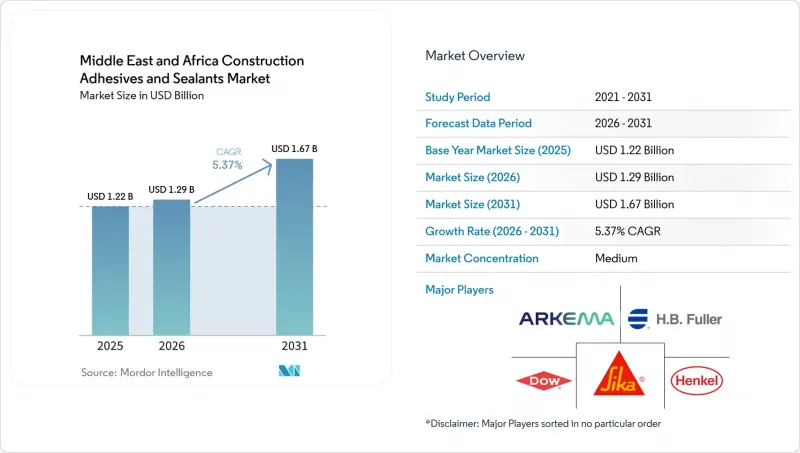

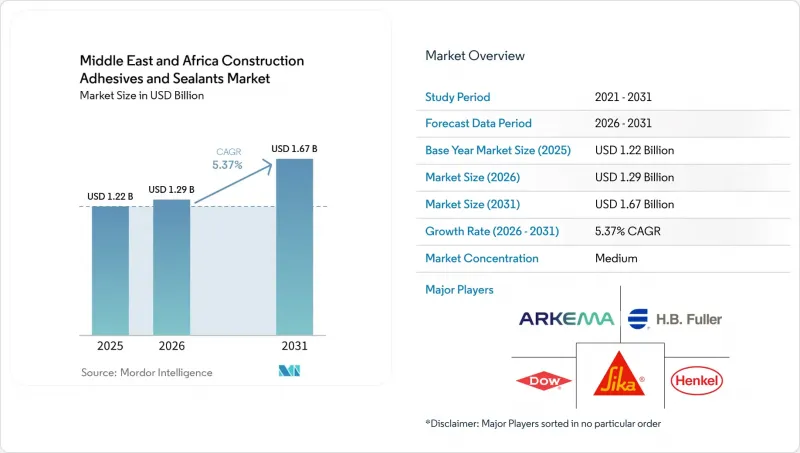

Mordor Intelligence에 의하면, 중동 및 아프리카의 건설용 접착제 및 실란트 시장 규모는 2025년 12억 2,000만 달러로 평가되었습니다. 2026년에는 12억 9,000만 달러로 확대되어 2031년까지 16억 7,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 5.37%로 성장할 전망입니다.

본 보고서는 수지별(아크릴 등), 기술별(핫멜트 등), 용도별(바닥재·타일, 지붕재 등), 최종 용도별(주택, 상업시설 등), 지역별(사우디아라비아, 아랍에미리트, 카타르, 남아프리카, 이집트, 기타 중동 및 아프리카 국가)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중동 및 아프리카의 건설용 접착제 및 실란트 시장 동향 및 인사이트

GCC 지역의 초대형 프로젝트가 급속히 확대되면서 특수 접착제 수요를 견인하고 있습니다.

사우디아라비아의 NEOM 공항 관리 계약(계약액 15억 달러) 및 키디야 육상 경기장(계약액 18억 달러)은 모두 내화성 실란트와 구조용 에폭시 수지가 필요하며, 이로 인해 접착제 소비량이 대폭 증가하여, 일반적인 건설 프로젝트에 비해 3-4배에 달하고 있습니다. 커튼월, 단열 금속 패널, 조립식 모듈을 사용하려면 연속적인 내후성 실링 비드가 필요하기 때문에 다국적 공급업체들은 해당 국가 내에 재고와 기술팀을 배치하고 있습니다. 또한, 2029년까지 286건의 프로젝트를 포함하는 카타르의 810억 카타르 리얄(222억 달러) 규모의 인프라 계획은 최대 50℃의 온도 변동을 견딜 수 있는 실리콘 및 폴리우레탄 재질의 조인트에 대한 수요를 뒷받침하고 있습니다. 높은 자본 집약도가 진입 장벽이 되면서, 소규모 수입업체들은 규제가 완화된 아프리카 시장으로 눈을 돌리고 있습니다. 그 결과, 중동 및 아프리카의 건설용 접착제 및 실란트 시장은 GCC의 기가 프로젝트에 힘입어 판매량 증가와 인증을 받은 고품질 배합으로의 전환이라는 두 가지 혜택을 모두 누리고 있습니다.

GCC의 저VOC 규제가 강화됨에 따라 수성 제품의 도입이 가속화되고 있습니다.

아랍에미리트(UAE)의 2024년 연방 법령 제21호에서는 접착제의 휘발성 유기화합물(VOC)을 1리터당 50그램으로 제한한 반면, 두바이의 TG-04 규정에서는 실런트의 VOC 상한선을 1리터당 250그램으로 낮추고 있으며, 제3자에 의한 감사 의무화를 통해 규정 준수가 철저히 이루어지고 있습니다. 이에 대응하여 BASF는 VOC 배출량을 90% 감축하는 ‘Baxxodur EC 151’을 출시했습니다. 이를 통해 바닥재 시공업체는 규정을 준수하지 않은 로트에 대해 부과되는 5만 디르함의 벌금을 피할 수 있게 됩니다. 그 결과, UAE의 바닥용 접착제 매출에서 수성 아크릴 분산액이 차지하는 비중은 2023년 38%에서 2025년까지 60%로 상승할 것으로 예측됩니다. 각 공급업체는 현재 GCC(걸프협력회의) 국가들의 프로젝트를 위해 규제를 준수하는 프리미엄 제품 라인과, 규제가 비교적 완화된 아프리카 시장을 위한 기존의 용제계 등급으로 제품 포트폴리오를 구성하고 있습니다. 이러한 규제 준수 격차로 인해, 규제 집행이 제한적인 지역에서도 첨단 기술의 도입이 가속화되고 있습니다.

원유 가격 변동과 운임 인상이 이익률을 압박하고 있습니다.

2025년, 브렌트 원유 가격은 배럴당 72-95달러 사이에서 등락을 보였으며, 그 결과 메틸렌디페닐디이소시아네이트(MDI) 및 톨루엔디이소시아네이트(TDI) 가격도 22-28% 변동했습니다. 이러한 변동은 고정가격 프로젝트에 참여하는 도급업체에게 비용 변동 관리가 어려워지는 등 여러 가지 과제를 안겨주고 있습니다. 또한, 홍해를 경유하는 우회로로 인해 컨테이너 1개당 운임이 1,900달러 증가했으며, 아세트산의 리드타임이 최대 6주 연장되었습니다. 이러한 상황으로 인해 아프리카의 유통업체들은 안전 재고 수준을 높일 수밖에 없게 되었습니다. 선물 거래를 통한 헤지가 가능한 다국적 기업들은 이익률을 유지하는 데 성공했지만, 중소규모의 재판매업자들은 시장 점유율 축소를 피할 수 없었습니다.

부문별 분석

실리콘 수지는 2026년부터 2031년까지 연평균 성장률(CAGR) 7.02%를 기록하며 성장할 것으로 전망됩니다. 이는 교량, 터널, 지하철의 이음매 부분에서 응집 파괴를 수반하지 않는 ±25%의 변위 능력에 대한 수요에 힘입은 것입니다. 이러한 성장은 카타르의 교통 인프라 확충 및 이집트의 고층 빌딩 외벽 공사와 관련이 있습니다. 이러한 프로젝트에서는 LEED(에너지 및 환경 설계 리더십) 인증 점수 획득에 기여하는 저탄성 계수의 실란트가 우선적으로 채택되고 있습니다. 2025년, 중동 및 아프리카의 건설용 접착제 및 실란트 시장에서 아크릴 수지는 23.49%의 점유율을 차지했습니다. 이는 걸프협력회의(GCC)의 휘발성 유기화합물(VOC) 규정을 준수하는 바닥재 및 타일 시공 용도에 힘입은 결과입니다. 대형 타일 시공에 필요한 20-30분의 개방 시간을 충족하고, VOC 기준치인 50그램/리터(g/L)를 준수하는 수성 아크릴계 제품은 시공업체들로부터 높은 지지를 얻고 있습니다.

폴리우레탄 수지는 지붕 자재나 단열재로 널리 사용되고 있으며, 그 습기 경화 특성 덕분에 아프리카의 외딴 지역에서의 물류 과정이 간소화되고 있습니다. 에폭시 수지는 프리캐스트 부재의 구조용 접착에 주로 사용되며, ‘Baxxodur EC 151’과 같은 제품을 사용하면 산업용 바닥의 경우 시공 당일에도 통행이 가능합니다. 비닐아세테이트-에틸렌(VAE)/에틸렌-비닐아세테이트(EVA) 에멀전은 비용 효율을 중시하는 이집트와 남아프리카의 주택 프로젝트에서 주류를 이루고 있으며, 아크릴 수지의 접착 강도의 70%를 40% 더 낮은 비용으로 실현하고 있습니다. 하이브리드 실란계 시스템은 염수 분무에 노출되는 연안 지역 프로젝트에서 활용되고 있습니다.

실란트는 2025년 매출의 40.73%를 차지했으며, GCC(걸프협력회의) 입찰에서 지정된 교량 상판, 커튼월 외곽부, 신축 이음매에 대한 용도에 힘입어 연평균 성장률(CAGR) 7.09%를 나타낼 것으로 예측됩니다. 카타르의 지하철 연장 공사나 이집트의 행정 수도 건설 프로젝트에서는 하루 15-20mm(mm)의 처짐을 견디고 열충격에 강한 실리콘 및 폴리우레탄이 요구되고 있습니다. UAE에서는 VOC(휘발성 유기화합물) 함량을 50 g/L 이하로 제한하고, 위반 시 5만 디르함(1만 3,612.3 달러)의 벌금을 부과하는 제21호 정령이 시행됨에 따라, 바닥재 시장에서 수성 접착제의 점유율이 2023년 38%에서 60%로 성장했습니다.

2액형 에폭시 등의 반응성 화학 물질은 10-50°C의 온도 범위에서 2.5 메가파스칼(MPa)을 초과하는 접착 강도를 발휘합니다. 경화 시간이 3초인 핫멜트 접착제는 프리팹 단열 패널에 대한 사용이 확대되고 있으며, 특히 LEED 인증을 목표로 하는 시공업체들 사이에서는 헨켈사의 바이오베이스 함유율 63%인 ‘LOCTITE HB S ECO’가 주목을 받고 있습니다. 용제계 접착제는 규제가 제한적으로 시행되는 시장에서는 여전히 사용되고 있지만, 남아프리카공화국이 2028년까지 VOC 상한치를 75 g/L로 상향 조정함에 따라 시장 점유율이 감소할 것으로 예측됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the middle east and Africa Construction Adhesives and Sealants Market size is expected to increase from USD 1.22 billion in 2025 to USD 1.29 billion in 2026 and reach USD 1.67 billion by 2031, growing at a CAGR of 5.37% over 2026-2031.

This report is Segmented by Resin (Acrylic and More), Technology (Hot Melt and More), Application (Flooring and Tiling, Roofing, and More), End-Use Sector (Residential, Commercial, and More) and Geography (Saudi Arabia, United Arab Emirates, Qatar, South Africa, Egypt, and Rest of Middle East and Africa). The Market Forecasts are Provided in Terms of Value (USD).

Middle East And Africa Construction Adhesives And Sealants Market Trends and Insights

Booming GCC Giga-Projects Drive Specialty Adhesive Demand

Saudi Arabia's NEOM airport management contract, valued at USD 1.5 billion, and Qiddiya's USD 1.8 billion athletics stadium both require fire-rated sealants and structural epoxies, significantly increasing adhesive consumption, up to three-to-four times more than standard construction projects. The use of curtain walls, insulated metal panels, and prefabricated modules necessitates continuous weatherproofing beads, prompting multinational suppliers to position inventories and technical teams within the kingdom. Additionally, Qatar's QAR 81 billion (USD 22.20 billion) infrastructure pipeline, which includes 286 projects through 2029, sustains demand for silicone and polyurethane joints capable of withstanding temperature swings of up to 50 degrees Celsius. High capital intensity creates entry barriers, steering smaller importers toward less-regulated African markets. As a result, the Middle East and Africa construction adhesives and sealants market benefits from both increased volume and a shift toward certified, premium formulations driven by GCC giga-projects.

Stricter GCC Low-VOC Regulations Accelerate Water-Borne Adoption

The United Arab Emirates (UAE) Federal Decree-Law No. 21 of 2024 limits adhesive volatile organic compounds (VOCs) to 50 grams per liter, while Dubai's TG-04 regulation reduces sealant VOC limits to 250 grams per liter, with compliance enforced through mandatory third-party audits. In response, BASF introduced Baxxodur EC 151, which reduces VOC emissions by 90%, enabling flooring contractors to avoid AED 50,000 penalties for non-compliant batches. Consequently, water-borne acrylic dispersions are projected to rise from 38% of UAE flooring-adhesive sales in 2023 to 60% by 2025. Suppliers are now segmenting their portfolios into premium, compliant lines for GCC projects and legacy solvent-borne grades for less-regulated African markets. This compliance gap is accelerating the adoption of advanced technologies, even in regions with limited enforcement.

Petro-Feedstock Volatility & Freight Surcharges Compress Margins

In 2025, Brent crude oil prices fluctuated between USD 72-95 per barrel, resulting in 22-28% price variations for methylene diphenyl diisocyanate (MDI) and toluene diisocyanate (TDI). These fluctuations have created challenges for contractors working on fixed-price projects, as they face difficulties in managing cost changes. Additionally, rerouting through the Red Sea increased freight costs by USD 1,900 per container and extended acetic acid lead times by up to six weeks. This situation has required African distributors to increase their safety stock levels. Multinational companies with the ability to hedge futures have managed to maintain their margins, while smaller resellers have experienced a reduction in market share.

Other drivers and restraints analyzed in the detailed report include:

- Rise of Modular Construction in East Africa Expands Acrylic Volumes

- Localization of Polyurethane Pre-Polymer Production Reduces Supply-Chain Risk

- Fragmented Distribution Networks Hinder Product Penetration

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone resins are projected to grow at a 7.02% compound annual growth rate (CAGR) from 2026 to 2031, driven by demand for +-25% movement capacity in bridge, tunnel, and metro joints without cohesive failure. This growth is linked to Qatar's transportation infrastructure expansion and Egypt's high-rise facades, which prioritize low-modulus sealants that contribute to Leadership in Energy and Environmental Design (LEED) certification points. Acrylic resins held a 23.49% share of the Middle East & Africa construction adhesives and sealants market in 2025, supported by flooring and tiling applications that comply with Gulf Cooperation Council (GCC) volatile organic compound (VOC) regulations. Water-borne acrylics, meeting 20-30 minute open-time requirements for large tiles and adhering to 50 grams per liter (g/L) VOC thresholds, have secured contractor preference.

Polyurethane resins are widely used in roofing and insulation, where moisture-curing simplifies logistics in remote African locations. Epoxy resins are preferred for structural bonding in precast elements, with products like Baxxodur EC 151 enabling same-day traffic on industrial floors. Vinyl acetate ethylene (VAE)/ethylene vinyl acetate (EVA) emulsions dominate cost-sensitive housing projects in Egypt and South Africa, offering 70% of acrylic bond strength at 40% lower cost. Hybrid silane systems are utilized in coastal projects exposed to salt spray.

Sealants accounted for 40.73% of 2025 revenue and are expected to grow at a 7.09% CAGR, driven by applications in bridge decks, curtain-wall perimeters, and expansion joints specified in GCC tenders. Qatar's metro extensions and Egypt's administrative capital projects require thermal-shock-resistant silicones and polyurethanes capable of flexing 15-20 millimeters (mm) daily. Water-borne adhesives have increased their share of UAE flooring sales from 38% in 2023 to 60%, following the implementation of Decree-Law No. 21, which enforces 50 g/L VOC limits and imposes AED 50,000 (USD 13,612.3) fines for non-compliance.

Reactive chemistries, such as two-component epoxies, provide bond strengths exceeding 2.5 megapascals (MPa) across job sites with temperatures ranging from 10-50 °C. Hot melts, with three-second set times, are increasingly used for prefabricated insulated panels, with Henkel's 63% bio-based LOCTITE HB S ECO gaining traction among contractors aiming for LEED certification. Solvent-borne adhesives remain in use in markets with limited regulatory enforcement, but are expected to lose market share as South Africa adopts 75 g/L VOC caps by 2028.

List of Companies Covered in this Report:

- 3M

- Arkema

- Avery Dennison Corp.

- BASF

- Dow

- Fosroc, Inc.

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- MAPEI S.p.A.

- Permoseal

- Pidilite Industries Ltd.

- RPM International Inc.

- Saint-Gobain

- Sika AG

- Soudal Group

- Tremco Construction Products Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Booming GCC giga-projects (e.g., NEOM, Qiddiya)

- 4.2.2 Stricter GCC low-VOC regulations shifting demand to water-borne and reactive chemistries

- 4.2.3 Rise of modular/off-site construction across East Africa

- 4.2.4 Localization of polyurethane pre-polymer production in Saudi Arabia and UAE (cost and lead-time)

- 4.2.5 Carbon-reduction mandates accelerating bio-based formulations adoption

- 4.2.6 Adoption of AI-driven smart-dispensing systems improving application productivity

- 4.3 Market Restraints

- 4.3.1 Petro-feedstock price volatility and Red Sea freight surcharges

- 4.3.2 Fragmented distribution network outside GCC slowing product penetration

- 4.3.3 Delayed harmonization of VOC limits across African countries raises compliance costs

- 4.3.4 Skilled-applicator shortage elevating project re-work risk

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Threat of New Entrants

- 4.5.2 Bargaining Power of Suppliers

- 4.5.3 Bargaining Power of Buyers

- 4.5.4 Threat of Substitutes

- 4.5.5 Industry Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin

- 5.1.1 Acrylic

- 5.1.2 Cyanoacrylate

- 5.1.3 Epoxy

- 5.1.4 Polyurethane

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Water-borne

- 5.2.2 Solvent-borne

- 5.2.3 Reactive

- 5.2.4 Hot-melt

- 5.2.5 Sealants

- 5.3 By Application

- 5.3.1 Flooring and Tiling

- 5.3.2 Roofing

- 5.3.3 Wall Panels and Facades

- 5.3.4 Insulation and Weatherproofing

- 5.3.5 Infrastructure Joints (bridges, tunnels)

- 5.4 By End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Infrastructure

- 5.5 By Geography

- 5.5.1 Saudi Arabia

- 5.5.2 United Arab Emirates

- 5.5.3 Qatar

- 5.5.4 South Africa

- 5.5.5 Egypt

- 5.5.6 Rest of Middle East and Africa

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share/(%)Ranking Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)}

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 Avery Dennison Corp.

- 6.4.4 BASF

- 6.4.5 Dow

- 6.4.6 Fosroc, Inc.

- 6.4.7 H.B. Fuller Company

- 6.4.8 Henkel AG & Co. KGaA

- 6.4.9 Huntsman International LLC

- 6.4.10 ITW Performance Polymers

- 6.4.11 MAPEI S.p.A.

- 6.4.12 Permoseal

- 6.4.13 Pidilite Industries Ltd.

- 6.4.14 RPM International Inc.

- 6.4.15 Saint-Gobain

- 6.4.16 Sika AG

- 6.4.17 Soudal Group

- 6.4.18 Tremco Construction Products Group

- 6.4.19 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment