|

시장보고서

상품코드

2066674

북미의 건설용 접착제 및 실란트 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Construction Adhesives And Sealants - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

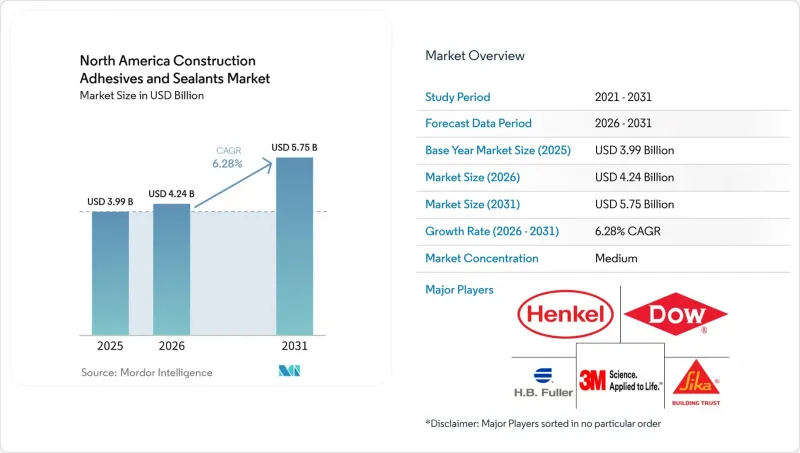

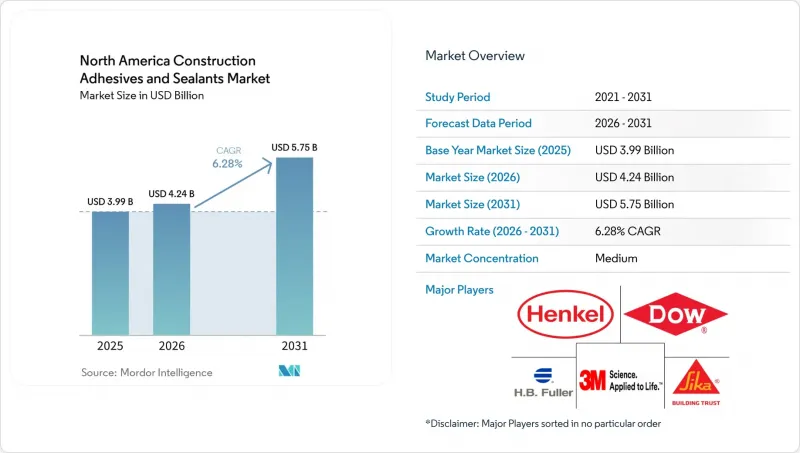

Mordor Intelligence에 의하면, 북미의 건설용 접착제 및 실란트 시장 규모는 2025년 39억 9,000만 달러로 평가되었습니다. 2026년에는 42억 4,000만 달러로 확대되어 2031년까지 57억 5,000만 달러에 이를 것으로 예상되며 2026년부터 2031년에 걸쳐 CAGR 6.28%로 성장할 전망입니다.

본 보고서는 수지(폴리우레탄, 아크릴 등), 기술(실란트, 수성 등), 용도(바닥재·타일, 지붕재, 벽 패널·파사드 등), 최종 용도(주택, 상업, 산업, 인프라), 지역(미국, 캐나다, 멕시코)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 건설용 접착제 및 실란트 시장 동향 및 인사이트

저VOC 건축자재에 대한 수요 급증

VOC 함량을 50-250 g/L로 제한하는 캘리포니아주 SCAQMD 규정 1168에 따라, 용제계 화학물질에서 벗어나기 위한 광범위한 배합 변경이 진행되고 있습니다. 메릴랜드주, 매사추세츠주, 텍사스주 및 기타 OTC 주에서 시행되는 유사한 규제로 인해 규제 환경이 세분화되고 있으며, 이에 대응할 수 있는 폭넓은 제품 포트폴리오를 보유한 공급업체들이 혜택을 보고 있습니다. 2025년 3월, BASF와 Sika는 VOC 배출량을 최대 90%까지 줄이고, 5-10°C의 저온에서도 경화되는 ‘Baxxodur EC 151’을 출시했습니다. 개질 실란계 하이브리드 제품은 이소시아네이트 노출을 방지하면서도 접착 요건을 충족시키기 때문에 시장 점유율을 확대되고 있습니다. 사양 수립자들은 저VOC라는 실적과 수명 주기 전반에 걸친 내구성을 점점 더 통합해 나가고 있으며, 환경 규정 준수를 단순한 규제상의 형식적 요건으로 취급하지 않고 입찰 사양서에 반영하고 있습니다.

오프사이트 모듈식 건축의 급속한 성장

영구형 모듈식 건축 시장 규모는 2024년에 146억 달러에 달했으며, 이는 10년 전의 43억 달러에 비해 크게 증가한 수치입니다. 이는 통제된 환경에서의 조립으로의 전환을 반영한 것입니다. 공장 작업 공정에서는 예측 가능한 경화 특성을 갖추고, 로봇 디스펜서와 연동할 수 있는 접착제가 필요합니다. 예를 들어, ‘SikaWall-3000 Rapid Bond’는 교차 적층 목재(CLT) 생산 라인에서 1시간 이내에 경화되므로 생산성을 향상시킵니다. 마찬가지로, 키일트사의 ‘Pro SW’ 접착제는 CLT의 접착 시간을 30% 단축하여 사이클 타임의 효율을 높이고 있습니다. 모듈식 유닛은 공장에서 완성되기 때문에 현장용 지연 경화형 접착제에 대한 수요가 감소하고 있으며, 북미의 건설용 접착제 및 실란트 시장은 공장 사용에 최적화된 배합으로 전환되고 있습니다.

석유 유래 원자재 가격의 변동

2026년 3월 20일까지 일주일 동안, 벤젠 원자재 가격의 급등에 따라 MDI 가격이 5.86% 상승했으며, 코베스트로와 헌츠맨은 톤당 220-260달러의 가격 인상을 발표했습니다. 원자재는 접착제 제조 비용의 약 75%를 차지하기 때문에 가격이 1%만 변동해도 중견 제조업체의 순이익에 1,330만 달러의 영향이 발생합니다. 원료 제조업체들은 바이오 유래 폴리올과 재생 수지의 활용 방안을 모색하고 있지만, 건축기준법에 따른 재인증 절차에 최대 2년이 소요되기 때문에 중소규모 기업들은 이익률 압박에 시달리고 있습니다.

부문별 분석

실리콘 수지는 파사드 엔지니어들이 자외선 노출 및 열 사이클 조건 하에서 보여주는 장기적인 탄력성을 높이 평가하고 있어, 2031년까지 연평균 성장률(CAGR) 6.43%로 성장할 것으로 전망됩니다. 폴리우레탄은 바닥재 및 스프레이 폼 단열재로의 사용이 주도되면서 2025년 북미의 건설용 접착제 및 실란트 시장 점유율의 24.38%를 차지했으나, 이소시아네이트 원자재 가격 변동으로 인해 비용 측면에서 어려움을 겪고 있습니다. 아크릴 계열은 실외 내구성보다는 세척의 용이성과 비용 면이 우선시되는 실내 마감 용도로 선호되고 있습니다. 에폭시 계열은 내구성이 뛰어난 바닥재나 내화학성 접착에 활용되고 있으며, Baxxodur EC 151과 같은 저온·저VOC 경화제 등의 기술 발전 덕분에 한랭 지역에서의 용도에서도 그 유용성이 보장되고 있습니다.

실리콘의 내후성 우수성은 40년에 걸친 실외 시험을 통해 입증되었습니다. 이 시험을 통해 주기적인 자외선, 염수 분무 및 온도 변동 조건 하에서 폴리우레탄 및 아크릴계 실란트에 비해 탄성 계수의 저하가 최소화됨이 입증되었습니다. 현재 건축 기준 당국은 커튼월의 사양서에 실리콘을 포함시키고 있으며, 교량 관리 당국도 내구 연한이 75년인 구조물에 대해 2액형 실리콘 접합부를 승인하고 있습니다. 페놀·레조르시놀계 수지는 구조용 집적재의 적층 과정에서 여전히 필수적이지만, 한편 변성 실란계 하이브리드 수지는 실리콘의 내구성과 폴리우레탄의 접착성을 모두 갖추고 있습니다. 여러 수지 포트폴리오에 대한 전문 지식을 갖춘 공급업체는 북미의 건설용 접착제 및 실란트 시장에서 이종 재료 접착이라는 과제를 해결하는 데 있어 더 유리한 입장에 있습니다.

수성 기술은 엄격한 VOC 제한을 부과하는 SCAQMD 규정 1168 및 OTC 모델 규정 등의 규제 조치에 힘입어, 2031년까지 연평균 성장률(CAGR) 6.43%라는 가장 높은 성장률을 보일 것으로 예측됩니다. 2025년에는 실란트가 기술별 매출의 42.01%를 차지했으며, 성능에 대한 요구가 높아짐에 따라 콘크리트와 FRP, 금속과 유리, 목재와 폴리머의 접합 등 특정 용도를 위한 틈새 시장용 배합이 개발되었습니다.

용제계 제품은 동결·해동이 반복되거나 다공성 기재와 같은 문제로 인해 수계 대체품이 적합하지 않은 용도에서 여전히 입지를 유지하고 있지만, 그 시장 점유율은 계속 하락하고 있습니다. 에폭시, 폴리우레탄, 메타크릴레이트 등의 반응성 화학 물질은 혼합 과정이 복잡한 경우나 고강도 구조용 접착에 사용됩니다. 핫멜트 접착제는 창문 및 단열 패널의 공장 생산 현장에서 활발히 사용되고 있으며, 아르케마(Arkema)는 모듈식 건축 수요에 부응하기 위해 2024년에 UV 아크릴계 제품의 생산 능력을 확대했습니다. 수성 제품의 저VOC라는 장점과 반응성 접착제의 강도를 결합한 하이브리드 기술은 북미의 건설용 접착제 및 실란트 시장에서 주요 성장 분야로 부상하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.29According to Mordor Intelligence, the north america construction adhesives and sealants market size is expected to increase from USD 3.99 billion in 2025 to USD 4.24 billion in 2026 and reach USD 5.75 billion by 2031, growing at a CAGR of 6.28% over 2026-2031.

This report is Segmented by Resin (Polyurethane, Acrylic, and More), Technology (Sealants, Water-Borne, and More), Application (Flooring and Tiling, Roofing, Wall Panels and Facades, and More), End-Use Sector (Residential, Commercial, Industrial, and Infrastructure), and Geography (United States, Canada, and Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Construction Adhesives And Sealants Market Trends and Insights

Surging Demand for Low-VOC Construction Materials

California's SCAQMD Rule 1168, which limits VOC content to 50-250 g/L, has driven widespread reformulation away from solvent-based chemistries. Similar regulations in Maryland, Massachusetts, Texas, and other OTC states have created a fragmented regulatory environment that benefits suppliers with extensive compliant product portfolios. In March 2025, BASF and Sika introduced Baxxodur EC 151, which reduces VOC emissions by up to 90% and cures at temperatures as low as 5-10 °C. Modified-silane hybrids are gaining market share as they eliminate isocyanate exposure while meeting adhesion requirements. Specifiers are increasingly integrating low-VOC credentials with lifecycle durability, embedding environmental compliance into bid specifications rather than treating it as a regulatory formality.

Rapid Growth of Off-Site Modular Construction

Permanent modular construction reached USD 14.6 billion in 2024, up from USD 4.3 billion a decade earlier, reflecting a shift toward controlled-environment assembly. Factory workflows require adhesives that cure predictably and integrate with robotic dispensers. For instance, SikaWall-3000 Rapid Bond cures within one hour on cross-laminated timber (CLT) production lines, enhancing throughput. Similarly, Kiilto's Pro SW adhesive reduces CLT bond times by 30%, improving cycle-time efficiency. Since modular units are completed in factories, demand for field-focused slow-cure adhesives is declining, steering the North America construction adhesives and sealants market toward factory-optimized formulations.

Volatility in Petro-Derived Raw Material Prices

MDI prices rose by 5.86% in the week ending March 20, 2026, following a spike in benzene feedstock costs, with Covestro and Huntsman announcing price increases of USD 220-260 per ton. Raw materials account for approximately 75% of adhesive production costs, so a 1% price change can impact net income by USD 13.3 million for mid-sized producers. While formulators are exploring bio-based polyols and recycled resins, the requalification process for building codes can take up to two years, leaving smaller firms exposed to margin pressures.

Other drivers and restraints analyzed in the detailed report include:

- Infrastructure Stimulus Packages in the U.S. and Canada

- Adhesive Formulation Innovations Enabling Mixed-Material Bonding

- Stricter REACH and TSCA Compliance Costs

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Silicone resins are projected to grow at a CAGR of 6.43% through 2031, as facade engineers value their long-term elasticity under UV exposure and thermal cycling. Polyurethane accounted for 24.38% of the North America construction adhesives and sealants market share in 2025, driven by its use in flooring and spray-foam insulation, though it faces cost challenges due to fluctuating isocyanate feedstock prices. Acrylics are preferred for interior applications where ease of cleanup and cost are prioritized over exterior durability. Epoxies are utilized in heavy-duty flooring and chemical-resistant bonds, with advancements such as low-temperature, low-VOC hardeners like Baxxodur EC 151 ensuring their relevance in cold-climate applications.

Silicone's weathering advantage is supported by a 40-year outdoor study that demonstrated minimal modulus loss compared to polyurethane or acrylic sealants under cyclic UV, salt fog, and temperature variations. Code officials now include silicone in curtain-wall specifications, and bridge authorities approve two-part silicone joints for 75-year assets. Phenol-resorcinol remains critical for structural mass-timber laminations, while modified-silane hybrids combine silicone's durability with polyurethane's adhesion. Suppliers with expertise in multi-resin portfolios are better positioned to address the mixed-material bonding challenges in the North America construction adhesives and sealants market.

Water-borne technology is expected to grow at the highest CAGR of 6.43% through 2031, driven by regulatory measures such as SCAQMD Rule 1168 and OTC model rules, which impose strict VOC limits. Sealants accounted for 42.01% of technology revenue in 2025, with performance demands leading to niche formulations for specific applications like concrete-to-FRP, metal-to-glass, and wood-to-polymer joints.

Solvent-borne products maintain a presence in applications where freeze-thaw cycles or porous substrates challenge water-based alternatives, though their market share continues to decline. Reactive chemistries, including epoxies, polyurethanes, and methacrylates, are used for high-strength structural bonds despite their mixing complexity. Hot-melt adhesives are thriving in factory settings for windows and insulated panels, with Arkema expanding UV acrylic capacity in 2024 to meet modular construction demand. Hybrid technologies that combine water-borne low-VOC benefits with reactive strength are emerging as a key growth area in the North America construction adhesives and sealants market.

List of Companies Covered in this Report:

- 3M

- Arkema

- ATP adhesive systems AG

- Avery Dennison

- BASF

- Carlisle Construction Materials

- Dow

- Franklin International

- H.B. Fuller Company

- Henkel AG & Co. KGaA

- Huntsman International LLC

- ITW Performance Polymers

- MAPEI S.p.A.

- Momentive

- PARKER HANNIFIN CORP

- Pecora Corporation

- RPM International Inc.

- Sika AG

- Soudal Group

- Wacker Chemie AG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging demand for low-VOC construction materials

- 4.2.2 Rapid growth of off-site modular construction

- 4.2.3 Infrastructure stimulus packages in the U.S. and Canada

- 4.2.4 Adhesive formulation innovations enabling mixed-material bonding

- 4.2.5 Rising multi-story timber buildings adoption

- 4.2.6 Widespread reroofing linked to extreme-weather events

- 4.3 Market Restraints

- 4.3.1 Volatility in petro-derived raw material prices

- 4.3.2 Stricter REACH and TSCA compliance costs

- 4.3.3 Skilled-labor shortages for correct sealant application

- 4.3.4 Competition from mechanical fastening alternatives in roofing

- 4.4 Value Chain Analysis

- 4.5 Porter's Five Forces

- 4.5.1 Bargaining Power of Suppliers

- 4.5.2 Bargaining Power of Buyers

- 4.5.3 Threat of New Entrants

- 4.5.4 Threat of Substitutes

- 4.5.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Resin Type

- 5.1.1 Polyurethane

- 5.1.2 Acrylic

- 5.1.3 Cyanoacrylate

- 5.1.4 Epoxy

- 5.1.5 Silicone

- 5.1.6 VAE/EVA

- 5.1.7 Other Resins

- 5.2 By Technology

- 5.2.1 Sealants

- 5.2.2 Water-borne

- 5.2.3 Solvent-borne

- 5.2.4 Reactive

- 5.2.5 Hot-melt

- 5.3 By Application

- 5.3.1 Flooring and Tiling

- 5.3.2 Roofing

- 5.3.3 Wall Panels and Facades

- 5.3.4 Insulation and Weatherproofing

- 5.3.5 Infrastructure Joints (bridges, tunnels)

- 5.4 By End-use Sector

- 5.4.1 Residential

- 5.4.2 Commercial

- 5.4.3 Industrial

- 5.4.4 Infrastructure

- 5.5 By Geography

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share (%)/Ranking Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Products and Services, and Recent Developments)

- 6.4.1 3M

- 6.4.2 Arkema

- 6.4.3 ATP adhesive systems AG

- 6.4.4 Avery Dennison

- 6.4.5 BASF

- 6.4.6 Carlisle Construction Materials

- 6.4.7 Dow

- 6.4.8 Franklin International

- 6.4.9 H.B. Fuller Company

- 6.4.10 Henkel AG & Co. KGaA

- 6.4.11 Huntsman International LLC

- 6.4.12 ITW Performance Polymers

- 6.4.13 MAPEI S.p.A.

- 6.4.14 Momentive

- 6.4.15 PARKER HANNIFIN CORP

- 6.4.16 Pecora Corporation

- 6.4.17 RPM International Inc.

- 6.4.18 Sika AG

- 6.4.19 Soudal Group

- 6.4.20 Wacker Chemie AG

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment