|

시장보고서

상품코드

2072662

북미의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

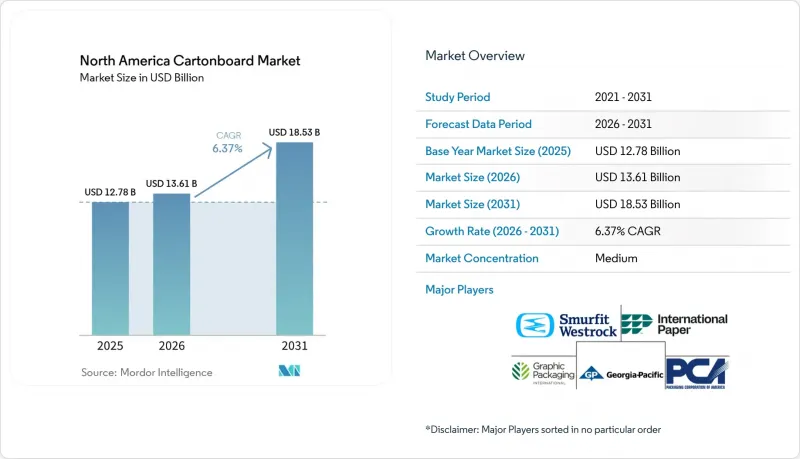

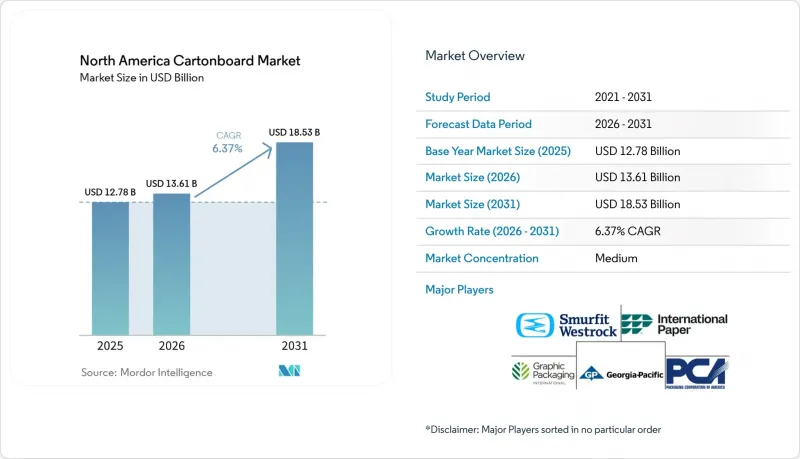

Mordor Intelligence에 의하면, 북미의 카톤 보드 시장 규모는 2025년 127억 8,000만 달러로 평가되었고, 2026년 136억 1,000만 달러로 추정되고, 2031년까지 185억 3,000만 달러로 확대될 것으로 예측되며, 2026-2031년 연평균 복합 성장률(CAGR)은 6.37%를 나타낼 전망입니다.

본 보고서는 제품 등급별(솔리드 표백카톤 보드, 솔리드 미표백카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드 서비스용 카톤 보드), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 최종 사용자 산업별(식품, 음료 등), 지역별(미국 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 카톤 보드 시장 동향 및 분석

플라스틱 포장을 대체할 지속 가능한 대안

지속 가능한 대안은 북미의 카톤 보드 시장에서 가장 확실한 장기적 성장 동력 중 하나입니다. 이는 포장 디자인의 변화가 브랜드 선호도와 마찬가지로 규제 준수에 의해서도 형성되기 때문입니다. 주 및 주 차원의 포장 규제로 인해 브랜드 소유자들은 1차 포장 및 2차 포장을 모두 재검토할 수밖에 없게 되었으며, 그 결과 외식 산업, 소비재, 소매 진열 용도에서 카톤 보드의 역할이 확대되고 있습니다. 이러한 변화는 단순히 한 가지 포장을 다른 것으로 바꾸는 데 그치지 않습니다. 대부분의 전환 과정에서는 SBS나 코팅되지 않은 미표백 크라프트지 등 특정 등급의 원지가 필요하기 때문에 단위당 카톤 보드 매수와 평량 요건이 모두 증가하기 때문입니다. 2025년 1월, FDA가 종이 및 카톤 보드로 만든 식품 포장재에 포함된 PFAS 함유 내유제에 관한 35건의 식품 접촉 통지 사항이 모두 더 이상 유효하지 않음을 확인함에 따라, 미국에서 새로운 규격 제정 작업이 가속화되었습니다. 이러한 변화로 인해 식품 접촉 용도에서 PFAS가 포함되지 않은 배리어 보드에 대한 수요도 증가했습니다. 현재 바이어들은 과도기적인 소재가 아닌, 검증된 대체품을 필요로 하고 있습니다. 또한, 컵 소재를 플라스틱에서 종이로 전환함에 따라, 폴리머 층을 제거한 후에도 강도를 유지하기 위해 더 두꺼운 카톤 보드가 필요하게 되면서, 북미의 카톤 보드 시장도 그 혜택을 보고 있습니다. 이로 인해 단순한 단위 대체에 그치지 않는 톤수 기준 수요 증가로 이어지고 있습니다.

포장 식품 및 음료 수요 증가

북미의 카톤 보드 시장은 카톤 보드가 식료품, 냉동식품, 냉장식품 및 외식 산업의 포장 시스템에 깊이 뿌리내리고 있기 때문에 포장 식품 및 음료에 대한 수요로부터 계속해서 안정적인 지지를 받고 있습니다. 2025년에는 식품이 매출의 36.19%를 차지할 것으로 예상되며, 시각적 연출과 운송 성능이 동시에 중요한 브랜드화된 진열용 포맷에서 이 소재가 널리 사용되고 있음이 부각되었습니다. 전미레스토랑협회는 2026년에도 지속적인 수요가 레스토랑 업계 동향을 좌우할 것이라고 밝혔으며, 이는 브랜드화된 외식 체인 전체에서 포장재의 시범 도입 및 보충 수요를 뒷받침하는 요인이 될 것입니다. 클리어워터 페이퍼(Clearwater Paper)사는 2026년 1분기 실적 발표에서 접이식 카톤 보드 수요가 견조한 추세를 보이고 있으며, 외식 산업용 컵 및 접시용 등급 제품도 호조를 보이고 있다고 밝히며, 식품 접촉용 카톤 보드 분야에 대한 수요가 지속되고 있음을 시사했습니다. 이러한 수요는 북미 카톤 보드 시장에 있어 중요합니다. 왜냐하면 테이크아웃 용기, 컵 소재, 라미네이트 트레이는 대체품으로 단기간 내에 대체하기 어려운, 소비 빈도가 높은 소비 패턴과 밀접하게 관련되어 있기 때문입니다. 또한, 브랜드 소유자가 라인 적합성 평가 작업을 완료하면, 식품 및 음료의 포장 형태는 장기간에 걸친 생산 기간 동안 고정되는 경우가 많기 때문에 카톤 보드 제조업체 입장에서는 수년에 걸친 공급 계약을 체결하기 위한 보다 안정적인 기반이 됩니다.

변동이 심한 섬유, 에너지, 화학 원료의 투입 비용

원자재 및 유틸리티 가격 변동이 계약 가격 주기에 맞추어 재설정되지 않기 때문에 투입 비용의 변동은 여전히 북미 카톤 보드 시장 전체의 수익을 제약하는 주요 요인으로 작용하고 있습니다. 스마핏 웨스트록(SmartFit Westlock)은 2026년 1분기에 주로 북미에서 기상 요인으로 인한 EBITDA 영향이 6,500만 달러에 달했다고 보고하는 한편, 가중되는 비용 압박을 상쇄하기 위해 두 번째 가격 인상을 추진하고 있습니다. 그래픽 패키징사는 2026년 1분기 조정 후 EBITDA가 전년 동기 3억 6,500만 달러에서 2억 3,200만 달러로 감소했다고 보고하며, 그 감소분 중 3,700만 미달러는 원자재비 및 기타 비용 상승에 기인한 것이라고 밝혔습니다. 캐스케이드사도 2026년 1분기 실적 발표에서 원자재 가격 상승 압력이 지속되고 있음을 지적하며, 제지 공장의 구조가 다르더라도 재생 펄프 공급망은 마찬가지로 광범위한 비용 압박에 직면해 있음을 시사했습니다. 이러한 압력은 북미의 카톤 보드 원지 시장에서 중요한 의미를 지닙니다. 왜냐하면, 자사에서 펄프를 생산하고 내부에서 가공을 수행하는 수직 통합형 제조업체의 우위를 더욱 확대할 수 있기 때문입니다. 또한, 소규모 제지 공장이나 독립 사업자들은 에너지, 재생 펄프, 특수 코팅 분야의 가격 상승이 뒤늦게 나타나거나 비용이 급격히 상승할 때 이를 흡수할 여력이 제한적이기 때문에 이는 업계 재편을 가속화하는 요인이 되기도 합니다.

부문별 분석

2025년, 액체 포장용 카톤 보드(LPB)는 북미 카톤 보드 시장에서 28.44%의 점유율을 차지했으며, 해당 지역에서 가장 큰 비중을 차지하는 제품 등급이 되었습니다. 이러한 입지는 유제품, 식물성 음료, 주스, 수프의 포장을 뒷받침하는 고도로 통합된 무균 포장 및 게이블탑 공급망에 의해 지탱되고 있습니다. 이러한 분야에서는 충진 라인의 통합으로 인해 장기적인 조달 주기가 고정되는 경향이 있습니다. 따라서 북미 카톤 보드 시장에서 LPB는 안정적인 수요 기반을 갖추고 있으며, 많은 선택적 소비재 포장 용도에 비해 갑작스러운 규격 변경의 영향을 덜 받는 상황입니다. 접이식 카톤 보드는 여전히 프리미엄 소비재에 사용되고 있으며, 두께의 균일성, 높은 백색도, 그리고 뛰어난 인쇄 품질은 브랜드 이미지 구축에 있어 여전히 중요한 요소로 작용하고 있습니다. 무표백 카톤 보드와 코팅지(뒷면 백색)는 비용 효율을 중시하는 음료 멀티팩 및 일반적인 소매 포장 용도로 계속해서 사용되고 있지만, 지속가능성에 대한 요구가 높아짐에 따라 등급 선정 및 섬유 인증에 대한 심사가 더욱 엄격해지고 있습니다.

북미의 카톤 보드 업계에서는 기존의 주력 등급과 식품 접촉 용도 가공과 관련된 새로운 성장 등급 사이에 뚜렷한 양극화가 나타나고 있습니다. 외식업용 보드는 플라스틱 사용 금지 조치, 퇴비화 가능한 포장재에 대한 수요, 그리고 테이크아웃 및 배달 소비의 꾸준한 증가에 힘입어 2031년까지 연평균 성장률(CAGR) 7.14%로 성장할 것으로 전망됩니다. 클리어워터 페이퍼(Clearwater Paper)사는 2026년 1분기 실적 설명회에서 컵 및 폴리 코팅된 접이식 카톤 보드용 등급을 포함한 압출 성형 제품이 완판되었다고 밝히며, 제품 재설계 및 가공 활동과 관련된 식품 접촉 용도 분야에서 공급이 부족함을 시사했습니다. 이러한 상황이 중요한 이유는 PFAS 및 PE가 포함되지 않은 솔루션으로의 전환이 단순히 화학 성분을 바꾸는 것뿐만 아니라, 많은 경우 두께, 가공률, 그리고 톤당 부가가치에도 변화를 가져오기 때문입니다. 따라서 북미의 카톤 보드 업계에서는 차단 성능, 규제 준수, 그리고 높은 수율 효율을 단일 제품으로 실현하는 등급으로 제품 구성이 변화하고 있습니다. 또한, 경량형 중저가 시장용 SBS 대체재의 등장은 가공업체들이 단순히 카톤 보드 표면 가격에만 의존하지 않고, 실질적인 생산량과 인쇄 성능을 비교 검토하는 등 보다 선택적인 구매 패턴을 시사하고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the north america cartonboard market size is projected to expand from USD 12.78 billion in 2025 and USD 13.61 billion in 2026 to USD 18.53 billion by 2031, registering a CAGR of 6.37% between 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, and More), and Geography (United States, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America Cartonboard Market Trends and Insights

Sustainable Substitution From Plastic Packaging

Sustainable substitution has become one of the clearest long-run supports for the North America cartonboard market because packaging changes are now being shaped by compliance as much as by brand preference. State and provincial packaging rules have pushed brand owners to reassess both primary and secondary formats, thereby widening the role of cartonboard in foodservice, consumer goods, and retail display applications. The shift is not limited to replacing one package with another, because many conversions require specific grades, such as SBS and coated unbleached kraft, which increase both carton counts and basis-weight requirements per unit. The FDA's confirmation in January 2025 that all 35 food contact notifications for PFAS-containing grease-proofing agents in paper and paperboard food packaging were no longer effective accelerated new specification work across the United States. That change also strengthened demand for PFAS-free barrier board in food-contact applications, where buyers now need validated alternatives rather than transitional materials. The North America cartonboard market also benefits when plastic-to-paper conversions in cup stock require heavier board to preserve strength after the polymer layer is removed, thereby raising tonnage demand beyond simple unit substitution.

Growth In Packaged Food And Beverage Demand

The North America cartonboard market continues to draw stable support from packaged food and beverage demand because cartonboard remains deeply embedded in grocery, frozen, chilled, and foodservice packaging systems. Food accounted for 36.19% of revenue in 2025, underscoring the material's widespread use across branded shelf-ready formats where visual presentation and transport performance matter simultaneously. The National Restaurant Association stated that enduring demand would continue to shape restaurant activity in 2026, which supports ongoing packaging trials and replenishment needs across branded foodservice chains. Clearwater Paper said in its first-quarter 2026 commentary that folding carton demand remained solid and that foodservice cup and plate grades showed strength, which points to sustained pull for food-contact paperboard applications. That demand is important for the North America cartonboard market because carry-out containers, cup stock, and laminated trays are tied to high-frequency consumption patterns that are difficult for alternatives to displace quickly. It also gives board producers a steadier path to multi-year supply agreements, since food and beverage pack formats often remain fixed for long production runs once brand owners complete their line qualification work.

Volatile Fiber, Energy, And Chemical Input Costs

Input-cost volatility remains the main earnings constraint across the North America cartonboard market because raw material and utility movements do not reset in line with contract pricing cycles. Smurfit Westrock reported a weather-related EBITDA impact of USD 65 million in the first quarter of 2026, largely in North America, while also pursuing a second wave of price increases to offset rising cost pressure. Graphic Packaging reported adjusted EBITDA of USD 232 million in the first quarter of 2026, down from USD 365 million a year earlier, and said input and other cost inflation accounted for USD 37 million of that decline. Cascades also pointed to continued upward pressure on input costs in its first-quarter 2026 results, indicating that recycled fiber networks are exposed to the same broad cost pressures even when mill structures differ. These pressures matter in the North America cartonboard market because they widen the advantage of vertically integrated producers with captive pulp and internal conversion assets. They also accelerate consolidation because smaller mills and independent operators have less room to absorb lagged pricing or sudden cost spikes in energy, recovered fiber, and specialty coatings.

Other drivers and restraints analyzed in the detailed report include:

- E-Commerce And Club Retail Secondary Packaging Demand

- PFAS-Free And PE-Free Barrier Board Innovation

- Competition From Flexible Packaging And Alternative Formats

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid Packaging Board held 28.44% of the North America cartonboard market share in 2025, making it the largest product grade in the regional mix. Its position rests on highly consolidated aseptic and gable-top supply chains that support dairy, plant-based beverage, juice, and broth packaging, where filling-line integration tends to lock in long procurement cycles. In the North America cartonboard market, this gives LPB a stable demand base that is less exposed to sudden format changes than many discretionary consumer packaging uses. Folding Boxboard still serves premium consumer goods where caliper consistency, high whiteness, and strong print results remain central to brand presentation. Solid Unbleached Board and White-Lined Chipboard continue to serve cost-sensitive beverage multipacks and general retail packaging, although sustainability requirements have heightened scrutiny of grade selection and fiber credentials.

The North America cartonboard industry also shows a clear split between legacy scale grades and newer growth grades tied to food-contact conversion. The Food Service Board is projected to expand at a 7.14% CAGR through 2031, driven by plastic bans, demand for compostable formats, and the steady rise in off-premise consumption. Clearwater Paper said in its first-quarter 2026 commentary that extruded products, including cup and polycoated folding carton grades, were sold out, signaling tight supply in food-contact applications linked to reformulation and conversion activity. That condition matters because the move toward PFAS-free and PE-free solutions does not just change chemistry; it often changes caliper, conversion rates, and the value captured per ton. The North America cartonboard industry is therefore seeing product architecture shift toward grades that deliver barrier performance, regulatory compliance, and stronger yield economics in a single offer. The launch of lightweight mid-market SBS alternatives also points to a more selective buying pattern, in which converters are comparing usable output and print performance rather than relying solely on headline board prices.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- By Country

- United States

- Canada

- Mexico

List of Companies Covered in this Report:

- Graphic Packaging Holding Company

- Smurfit Westrock plc

- International Paper Company

- Georgia-Pacific LLC

- Packaging Corporation of America

- Clearwater Paper Corporation

- Sonoco Products Company

- Cascades Inc.

- Metsa Board Corporation

- Mayr-Melnhof Karton Aktiengesellschaft

- Billerud Aktiebolag (publ)

- Stora Enso Oyj

- Tetra Pak International S.A.

- SIG Group AG

- Huhtamaki Oyj

- CCL Industries Inc.

- Diamond Packaging

- American Carton Company

- Keystone Folding Box Co.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Sustainable Substitution from Plastic Packaging

- 4.2.2 Growth in Packaged Food and Beverage Demand

- 4.2.3 Premium Print and Shelf Appeal Demand in Beauty and Personal Care

- 4.2.4 E-commerce and Club Retail Secondary Packaging Demand

- 4.2.5 PFAS-Free and PE-Free Barrier Board Innovation

- 4.2.6 Pharmaceutical Serialization and Biologics Carton Complexity

- 4.3 Market Restraints

- 4.3.1 Volatile Fiber, Energy, and Chemical Input Costs

- 4.3.2 Competition from Flexible Packaging and Alternative Formats

- 4.3.3 State-Level PFAS Compliance Retrofits and Qualification Cycles

- 4.3.4 Canadian Cartonboard Capacity Tightness and Import Dependence

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Graphic Packaging Holding Company

- 6.4.2 Smurfit Westrock plc

- 6.4.3 International Paper Company

- 6.4.4 Georgia-Pacific LLC

- 6.4.5 Packaging Corporation of America

- 6.4.6 Clearwater Paper Corporation

- 6.4.7 Sonoco Products Company

- 6.4.8 Cascades Inc.

- 6.4.9 Metsa Board Corporation

- 6.4.10 Mayr-Melnhof Karton Aktiengesellschaft

- 6.4.11 Billerud Aktiebolag (publ)

- 6.4.12 Stora Enso Oyj

- 6.4.13 Tetra Pak International S.A.

- 6.4.14 SIG Group AG

- 6.4.15 Huhtamaki Oyj

- 6.4.16 CCL Industries Inc.

- 6.4.17 Diamond Packaging

- 6.4.18 American Carton Company

- 6.4.19 Keystone Folding Box Co.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment