|

시장보고서

상품코드

2072785

베트남의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Vietnam Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

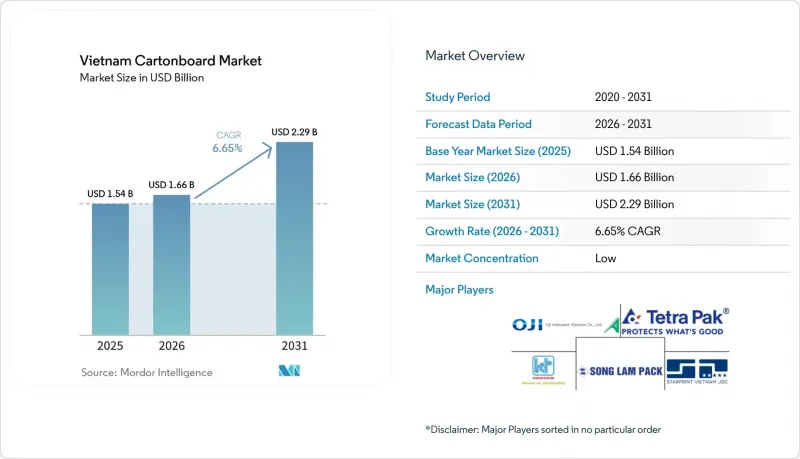

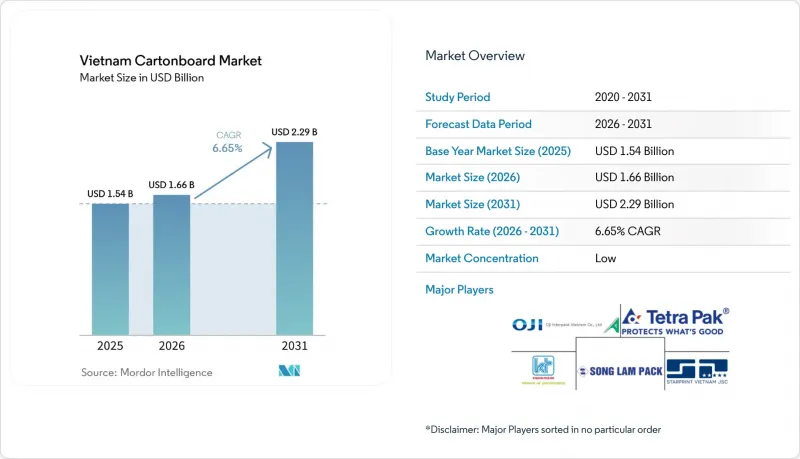

Mordor Intelligence에 의하면, 베트남의 카톤 보드 시장 규모는 2025년에 15억 4,000만 달러로 평가되었고, 2026년 16억 6,000만 달러로 추정되고, 2031년까지 22억 9,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 6.65%를 나타낼 전망입니다.

본 보고서는 제품 등급별(고형 표백 카톤 보드, 고형 미표백 카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드서비스용 카톤 보드), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 그리고 최종 사용자 산업별(식품, 음료, 제약 및 헬스케어, 담배, 화장품 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

베트남의 카톤 보드 시장 동향 및 분석

가공식품 및 음료 소비 확대

베트남의 식품 및 음료 부문은 2025년에 726조 5,000억 VND(279억 4,000만 달러) 시장 규모를 기록하였고, 2026년에는 760조 VND(292억 3,000만 달러)에 달할 것으로 예측됩니다. 이로 인해 우유용 카톤, 건조식품용 카톤, 냉동식품용 포장재 및 기타 2차 가공 카톤 보드 제품에 대한 폭넓은 수요 기반이 유지되고 있습니다. 이러한 소비 동향은 베트남 카톤 보드 시장에 있어 중요한 의미를 지닙니다. 이는 단일 최종 용도 분야에 의존하는 것이 아니라, 여러 유형의 카톤 보드 등급에 걸친 수요를 동시에 뒷받침하고 있기 때문입니다. 가정에서의 구매가 포장된 브랜드 식품으로 더욱 전환됨에 따라, 가공업체들은 현대 소매 및 외식 산업 채널에서 라벨 표시, 운송 중 보호, 진열대에서의 시각적 전시가 주도하는 재구매 수요의 혜택을 누리고 있습니다. 또한, 이러한 수요 동향은 긴 리드타임이나 인쇄 품질의 편차 없이 음료, 유제품, 냉동식품, 건조식품 등 각 생산 라인에 걸친 다양한 프로젝트에 대응할 수 있는 공급업체에게도 유리하게 작용합니다. 그 결과, 접이식 카톤 보드 상자, 외식 산업용 포장재, 액체용 카톤 보드 제품의 수주가 더욱 안정화되었으며, 저부가가치의 범용 포맷이 지속적인 가격 압박을 받고 있음에도 불구하고 베트남의 카톤 보드 시장은 성장을 유지하고 있습니다.

전자상거래 및 소매업용 패키지 확대

베트남의 전자상거래 시장은 2025년에 458조 1,600억 VND(165억 8,000만 달러)의 GMV를 기록했으며, 2026년 1분기 매출액은 전년 동기 대비 32.74% 증가한 134조 6,000억 VND(51억 9,000만 달러)에 달했습니다. 또한, 산업통상부의 디지털 경제 플랫폼에 따르면, 베트남의 전자상거래 시장은 2026년까지 370억 달러를 목표로 하고 있으며, 이는 소비자에게 직접 배송하거나 브랜드 포장재에 대한 수요가 계속해서 확대될 것임을 시사합니다. 이러한 변화는 베트남의 카톤 보드 시장을 뒷받침할 것입니다. 왜냐하면 포장재는 운송 중 상품을 보호할 뿐만 아니라, 구매자나 소매업체에 도착했을 때 그대로 진열할 수 있는 상태여야 한다는 요구가 점점 더 커지고 있기 때문입니다. 이러한 변화로 인해 디지털 인쇄 및 UV 오프셋 인쇄 능력을 갖춘 가공 업체의 입지가 강화될 것입니다. 이는 소량 생산, 디자인의 다양화, 제품 리뉴얼 주기의 단축이 점차 일반화되고 있기 때문입니다. 또한, 가치 구성도 단순한 운송용 포장재에서 리소라미네이트 가공이나 고품질의 마감 처리가 적용된 접이식 카톤 보드 상자로 전환되고 있으며, 이에 따라 베트남의 카톤 보드 시장은 단순한 수량 증가만으로는 예측할 수 없을 정도로 견고한 수익 구조를 구축하고 있습니다.

재생 섬유 가격의 변동성과 수입 의존도

베트남이 혼합지 수입을 금지함에 따라, 오래된 카톤 보드 용기가 주요 수입 재생섬유 등급으로 남아 있어, 이로 인해 국내 제지 공장은 국제 무역 흐름과 재생섬유 가격 변동의 영향을 계속 받고 있습니다. 미국의 폐지 단가는 2020년 톤당 167달러에서 2024년에는 204달러로 상승했는데, 이는 투입 비용의 변동이 공급망 전체에 급속히 파급된 후 다시 안정화되기까지의 과정을 보여줍니다. 이는 베트남의 카톤 보드 시장에 있어 직접적인 문제입니다. 왜냐하면 화이트 라이닝 칩보드가 여전히 가장 큰 제품 등급 부문이며, 그 원가 구조는 재생 섬유 층에 의존하고 있기 때문입니다. 섬유 원가가 급격히 변동할 경우, 제지 회사나 가공업체는 특히 식품 및 FMCG(일용소비재) 분야에서 고정 가격 계약이나 가격 변동에 민감한 계약을 체결한 고객에 대해, 그 변동분을 반드시 전가할 수 있는 것은 아닙니다. 그 결과, 이익률이 지속적으로 압박을 받게 되고, 가치 성장이 둔화되며, 계획의 가시성이 떨어집니다. 또한, 범용 제품에 중점을 두는 공급업체는 고객과의 유대 관계가 강한 특수 등급 제품 업체에 비해 계속해서 취약한 입장에 놓여 있습니다.

부문별 분석

2025년, 화이탈리아닝 칩보드는 베트남 카톤 보드 시장에서 36.27%의 점유율을 차지했으며, 식품, 음료, 일용소비재(FMCG) 포장 분야에서 수용 가능한 인쇄 품질과 비용 효율성의 균형을 유지함으로써 선두 자리를 지켰습니다. 이 등급은 여전히 베트남 카톤 보드 시장의 핵심을 이루고 있으며, 국내 구매자들은 대량 생산되는 2차 카톤 보드 및 멀티팩 용도에서 원자재 비용을 여전히 신중하게 검토하고 있습니다. 무표백 카톤 보드와 접이식 카톤 보드는 의약품, 화장품, 고급 식품 등 더 엄격한 요건이 요구되는 포장 분야에서 계속해서 활용되고 있습니다. 이러한 분야에서는 표면 마감, 브랜딩 품질, 그리고 더욱 청결한 인상을 주는 카톤 보드의 외관이 더 높은 가격 책정과 더욱 엄격하게 관리되는 조달 기준을 뒷받침하고 있습니다. 또한, 유제품 및 즉시 음용(RTD) 음료 부문에서는 표준 접이식 카톤과는 다른 성능 특성이 요구되는 무균 포장 방식에 의존하고 있기 때문에 액체 포장용 카톤 보드 역시 중요한 역할을 계속하고 있습니다.

외식 산업용 보드는 2026-2031년 연평균 성장률(CAGR) 7.57%를 나타낼 것으로 예측되며, 가장 빠르게 확대될 부문이 될 전망입니다. 이는 패스트푸드점, 배달 플랫폼, 그리고 1인분 단위의 소비가 컵, 용기, 테이크아웃 용기에 대한 수요를 계속해서 견인하고 있기 때문입니다. 베트남의 음식점 총 수는 2025년에 329,500개로 추산되며, 2026년 말까지 333,600개에 달할 것으로 예상되어, 도시 지역에서 일회용 카톤 보드 제품의 보급을 촉진하고 있습니다. 베트남의 카톤 보드 업계에서는 이로 인해 수요가 많은 화이트 라이닝이 적용된 칩보드와, 외식 산업 및 액체 용도 분야에서 더욱 빠르게 성장하는 가치 사이에서 더욱 명확한 구분이 생겨나고 있습니다. 또한, 이는 장벽 성능, 안정적인 성형성 및 식품 접촉 시 품질 관리에 투자하는 공급업체가, 표준 재생 카톤 보드 등급에만 초점을 맞추고 있는 가공업체보다 프리미엄 제품군에서 더 큰 시장 점유율을 확보할 가능성이 높다는 것을 의미합니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the vietnam cartonboard market size was valued at USD 1.54 billion in 2025 and estimated to grow from USD 1.66 billion in 2026 to reach USD 2.29 billion by 2031, at a CAGR of 6.65% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, Cosmetics, and More). The Market Forecasts are Provided in Terms of Value (USD).

Vietnam Cartonboard Market Trends and Insights

Rising Processed Food And Beverage Consumption

Vietnam's food and beverage sector generated VND 726.5 trillion (USD 27.94 billion) in 2025 and is projected to reach VND 760 trillion (USD 29.23 billion) in 2026, which keeps a broad demand base in place for milk cartons, dry food cartons, frozen food packs, and other secondary paperboard formats. That spending matters to the Vietnam cartonboard market because it supports demand across multiple board grades simultaneously, rather than relying on a single end-use pocket. As household purchases move further toward packaged and branded food, converters benefit from repeat demand driven by labeling, transport protection, and visual shelf presentation in modern retail and foodservice channels. The demand profile also favors suppliers that can handle mixed jobs across beverages, dairy, frozen products, and dry grocery lines without long lead times or inconsistent print quality. The result is a steadier order book for folding cartons, foodservice packs, and liquid board applications, helping the Vietnam cartonboard market maintain growth even as lower-value commodity formats remain under pricing pressure.

E-Commerce And Retail-Ready Packaging Expansion

Vietnam's e-commerce market recorded GMV of VND 458.16 trillion (USD 16.58 billion) in 2025, and revenue in the first quarter of 2026 rose 32.74% year on year to VND 134.6 trillion (USD 5.19 billion). The Ministry of Industry and Trade's digital economy platform also stated that Vietnam's e-commerce market is targeting USD 37 billion in 2026, which points to continued expansion in direct-to-consumer shipments and branded packaging demand. This shift supports the Vietnam cartonboard market because packaging is increasingly expected to protect goods in transit and still perform as a display-ready unit when it reaches the buyer or retailer. That change improves the position of converters with digital and UV offset capabilities, since shorter runs, greater artwork variation, and faster product refresh cycles are becoming more common. It also shifts the value mix away from plain transit packs and toward litho-laminated and better-finished folding cartons, giving the Vietnam cartonboard market a stronger revenue profile than pure volume growth would suggest.

Recovered Fiber Price Volatility And Import Dependence

Vietnam banned imports of mixed paper and left old corrugated containers as the dominant imported recovered fiber grade, which keeps domestic mills exposed to international trade flows and pricing changes in recycled fiber. US wastepaper unit prices rose from USD 167 per tonne in 2020 to USD 204 per tonne in 2024, which shows how input cost swings can move quickly across the supply chain before easing again. This is a direct issue for the Vietnam cartonboard market because white-lined chipboard remains the largest product-grade segment and depends on recycled fiber layers in its cost structure. When fiber costs move sharply, mills and converters cannot always pass those changes through to customers on fixed or price-sensitive contracts, especially in food and FMCG work. The result is a recurring margin squeeze that slows value growth, weakens planning visibility, and keeps commodity-focused suppliers more vulnerable than specialty-grade operators with tighter customer relationships.

Other drivers and restraints analyzed in the detailed report include:

- Plastic Substitution And EPR-Led Paper Packaging Shift

- Pharmaceutical Localization And Compliance Packaging Demand

- Fragmented Converter Base And Persistent Price Competition

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

White-lined chipboard held 36.27% of the Vietnam cartonboard market share in 2025, maintaining its lead by balancing acceptable print quality with cost efficiency across food, beverage, and everyday FMCG packaging applications. The grade remains central to the Vietnam cartonboard market, where domestic buyers still closely weigh substrate cost in large-volume secondary cartons and multipack applications. Solid bleached board and folding boxboard continue to serve more demanding packaging lines in pharmaceuticals, cosmetics, and premium food, where surface finish, branding quality, and cleaner board appearance support better pricing and more controlled procurement standards. Liquid packaging board also retained an important role because dairy and ready-to-drink categories depend on aseptic formats that require a different performance profile than standard folding carton jobs.

The food service board is projected to grow at a 7.57% CAGR during 2026-2031, making it the fastest-expanding grade, as quick-service restaurants, delivery platforms, and single-serve consumption continue to drive demand for cups, containers, and takeaway packs. Vietnam's total food and beverage outlet count was estimated at 329,500 in 2025 and is projected to reach 333,600 by the end of 2026, supporting a broader adoption of disposable paperboard formats across urban centers. Within the Vietnam cartonboard industry, this creates a clearer split between large-volume white-lined chipboard demand and faster-value growth in food service and liquid applications. It also means suppliers that invest in barrier performance, consistent forming behavior, and food-contact quality control are likely to capture a larger share of the premium mix than converters that focus only on standard recycled-board grades.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Tetra Pak International S.A.

- Oji Interpack Vietnam Co., Ltd.

- SONG LAM Trading & Packaging Production CO., Ltd.

- Khang Thanh Manufacturing JSC

- Starprint Vietnam Joint Stock Company

- BINH MINH PAT CO., LTD

- Ngoc Diep Joint Stock Company

- intBOX Intelligent Packaging Corporation

- New Life Packaging Printing Company

- Hoang Vuong Paper Packaging Co., Ltd.

- Viet Van Nhat CO., LTD

- Avestar Packaging Group Joint Stock Company

- Kraft of Asia Paperboard & Packaging Co., Ltd.

- My Huong Paper Manufacturing JSC

- Dong Tien Packaging and Paper Co., Ltd.

- Sai Gon Paper Corporation

- Miza Nghi Son Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 Rising Processed Food and Beverage Consumption

- 4.3.2 E-commerce and Retail-Ready Packaging Expansion

- 4.3.3 Plastic Substitution and EPR-Led Paper Packaging Shift

- 4.3.4 Pharmaceutical Localization and Compliance Packaging Demand

- 4.3.5 Tetra Pak Capacity Expansion Supporting Liquid Carton Adoption

- 4.3.6 Export-Buyer Traceability and FSC Requirements Reshaping Converter Selection

- 4.4 Market Restraints

- 4.4.1 Recovered Fiber Price Volatility and Import Dependence

- 4.4.2 Fragmented Converter Base and Persistent Price Competition

- 4.4.3 PolyAl Beverage Carton Recycling Bottlenecks

- 4.4.4 Imported Barrier and Liquid Board Dependence

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Tetra Pak International S.A.

- 6.4.2 Oji Interpack Vietnam Co., Ltd.

- 6.4.3 SONG LAM Trading & Packaging Production CO., Ltd.

- 6.4.4 Khang Thanh Manufacturing JSC

- 6.4.5 Starprint Vietnam Joint Stock Company

- 6.4.6 BINH MINH PAT CO., LTD

- 6.4.7 Ngoc Diep Joint Stock Company

- 6.4.8 intBOX Intelligent Packaging Corporation

- 6.4.9 New Life Packaging Printing Company

- 6.4.10 Hoang Vuong Paper Packaging Co., Ltd.

- 6.4.11 Viet Van Nhat CO., LTD

- 6.4.12 Avestar Packaging Group Joint Stock Company

- 6.4.13 Kraft of Asia Paperboard & Packaging Co., Ltd.

- 6.4.14 My Huong Paper Manufacturing JSC

- 6.4.15 Dong Tien Packaging and Paper Co., Ltd.

- 6.4.16 Sai Gon Paper Corporation

- 6.4.17 Miza Nghi Son Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment