|

시장보고서

상품코드

2072771

독일의 카톤 보드 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

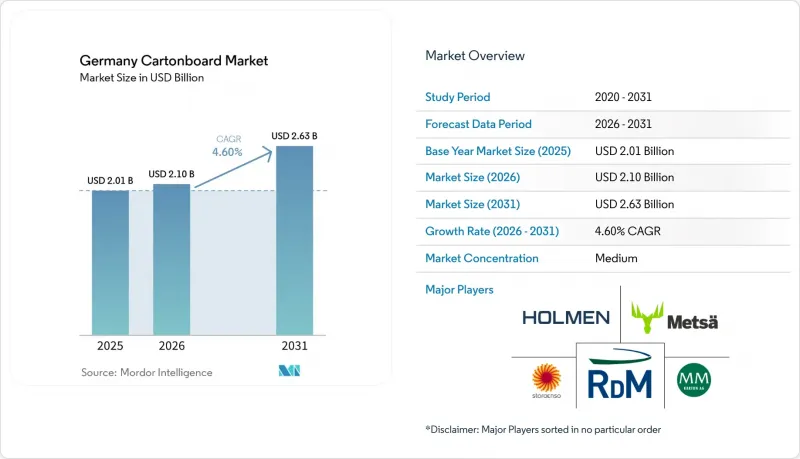

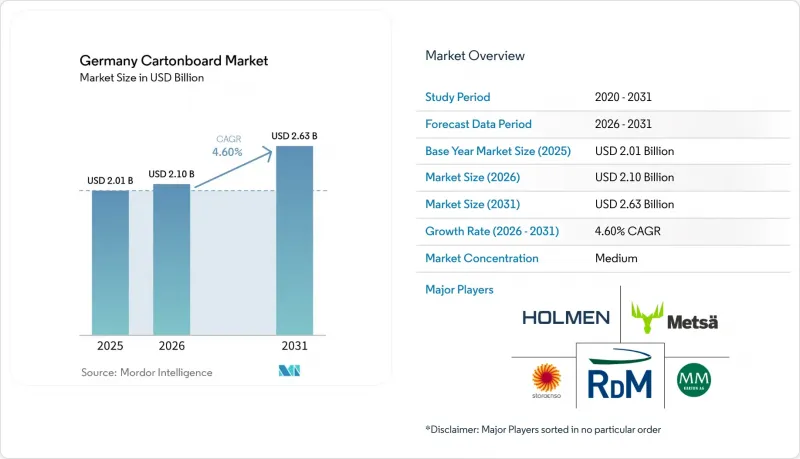

Mordor Intelligence에 의하면, 독일의 카톤 보드 시장 규모는 2025년에 20억 1,000만 달러로 평가되었고, 2026년 21억 달러로 추정되고, 2031년까지 26억 3,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 4.60%를 나타낼 전망입니다.

본 보고서는 제품 등급별(고형 표백 카톤 보드, 고형 미표백 카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드서비스용 카톤 보드), 포장 형태별(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 최종 사용자 산업별(식품, 음료, 의약품 및 헬스케어, 담배 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일의 카톤 보드 시장 동향 및 인사이트

PPWR이 주도하는 '재활용성을 고려한 설계(Recyclability-By-Design)'의 도입

PPWR은 2025년 2월에 발효되며, 2026년 8월에 본격적인 운영 단계에 들어갑니다. 이는 EU 시장에 출시되는 포장재가 조화로운 재활용 가능성 분류 및 적합성 요건을 명확히 준수해야 함을 의미합니다. 독일에서는 이 요건이 기존의 규정 준수 체제에 추가로 적용되는 형태가 됩니다. 이는 Zentrale Stelle Verpackungsregister(포장 등록 중앙 기관) 및 VerpackG(포장법)의 틀에 따라, 이미 제조업체, 가공업체, 브랜드 소유자에게 등록, 데이터 보고 및 재활용 가능성 평가를 위한 명확한 절차가 제시되어 있기 때문입니다. 2026년 8월이라는 전환점을 앞두고 조달 동향은 이미 변화하고 있으며, 브랜드 소유주들은 재활용 가능성, 단일 소재 구조, 그리고 더욱 엄격해진 규제 심사를 견딜 수 있는 문서화에 대해 입찰 사양을 강화하고 있습니다. 이러한 변화로 인해 종이 및 플라스틱, 호일 복합 구조에 비해 카톤 보드의 경쟁력이 높아지고 있습니다. 왜냐하면 섬유 기반 포장재는 재료 간의 경쟁을 최소화하면서도 디자인과 재활용 가능성이라는 두 가지 기대를 모두 충족시킬 수 있기 때문입니다. 또한, 인증을 받은 재활용 가능 제품군을 제공할 수 있고, 등급, 코팅, 가공 공정에 걸쳐 보다 명확한 추적성을 확보할 수 있는 제지 제조업체의 위상도 높아집니다. 이러한 선언이 일상적인 포장 거버넌스의 일부로 자리 잡으면서, 독일의 카톤 보드 시장은 단순한 수량 대체가 아닌, 더 높은 사양 수요로 전환되고 있습니다.

식품 및 음료 포장재에서 플라스틱에서 섬유로의 전환

독일 식품 및 음료 포장 분야에서 플라스틱 대체 움직임이 더욱 탄력을 받고 있는데, 이는 소매업체의 요구, 소비자의 기대, 그리고 EU 규정을 준수하는 포장 규제가 모두 재활용 가능한 섬유 소재를 지향하고 있기 때문입니다. 식품 소매 업계의 대규모 자체 브랜드(PB) 프로그램이 이러한 전환에 탄력을 불어넣고 있습니다. 왜냐하면, 단 한 번의 디자인 변경 결정만으로도 플라스틱을 많이 사용한 형태에서 접이식 카톤 보드, 외식 산업용 카톤 보드, 배리어 코팅이 적용된 카톤 보드로 막대한 양의 포장재를 전환할 수 있기 때문입니다. 그 상업적 영향은 단순히 톤수에 그치지 않습니다. 식품과 접촉하는 가공품의 경우, 제품의 안전성을 확보하면서도 재활용 가능성을 입증할 수 있는 코팅이나 구조가 요구되기 때문에 공급업체 입장에서는 기술적 장벽이 높아지고 있습니다. 따라서 독일의 카톤 보드 시장은 단순히 부가가치가 낮은 대체품을 공급하는 데 그치지 않고, 식품 포장 분야에서 부가가치가 더 높은 부문을 확대해 나가고 있습니다. 헨켈과 MM 보드 앤 페이퍼는 2025년, TOPCOLOR(R) BARRIER AROMA를 사용한 100% 카톤 보드 솔루션으로 블리스터 팩을 대체한 사례를 통해 이러한 방향성을 제시했으며, 해당 패키지는 '2025년 독일 포장상'를 수상했습니다. 2025년 매출액 중 식품 부문이 46.21%를 차지한 점을 고려할 때, 이 최종 용도 부문에서 지속적으로 진행되고 있는 포장 재설계 활동은 독일의 카톤 보드 시장에 코팅 및 제품 개발을 위한 대규모의 지속 가능한 기반을 마련해 주고 있습니다.

에너지 및 재생 섬유 비용의 변동

에너지 가격 변동은 2026년 독일 카톤 보드 시장에 있어 여전히 가장 시급한 비용 위험 요인으로 남아 있습니다. 이는 제지 공장이 연료, 운송 및 원자재 비용이 급격하고 불규칙하게 변동할 수 있는 환경에서 가동을 계속하고 있기 때문입니다. 마이어-멜른호프사는 2026년 4월 실적 속보에서 에너지, 운송 및 화학제품 비용의 대폭적인 상승이 이익률 하락의 주된 요인이라고 밝혔으며, 경영진은 이러한 압박이 2026년 3월 이후 두드러지게 나타나기 시작했다고 지적했습니다. 재활용 펄프의 등급은 에너지 집약적인 가공 공정이나 폐지 가격 변동에 대해 경제성이 더욱 민감하기 때문에 특히 영향을 받기 쉬운 상황에 놓여 있습니다. 독일의 탄탄한 회수·재활용 체계는 공급망의 원활한 유지에 기여하고 있지만, 그 집중도가 높기 때문에 재생 펄프의 가격 변동이 생산자가 바라는 것보다 빠른 속도로 제지 공장에 파급될 가능성이 있습니다. 열병합 발전 설비, 바이오매스 시스템 또는 전력 구매 계약을 보유한 사업자는 급격한 비용 변동을 흡수하기 쉬운 입장에 있지만, 판매 가격이 압박을 받고 있는 상황에서는 그러한 투자에도 자본이 필요합니다. 그 결과, 독일의 카톤 보드 시장이 현재의 원가 주기를 거치면서, 이익률을 유지할 수 있는 공급업체와 유연성이 부족한 공급업체 간의 격차가 더욱 벌어지고 있습니다.

부문별 분석

2025년, 접이식 카톤 보드는 독일 카톤 보드 시장 점유율의 38.13%를 차지했으며, 독일 카톤 보드 제품 구성에서 가장 큰 비중을 차지하는 제품 등급으로서의 위상을 유지했습니다. 이러한 우위는 식품 소매, 의약품 2차 포장, 고급 소비재 등 폭넓은 분야에서 활용 가능하다는 점에 기인하며, 이러한 분야에서는 강성, 인쇄 적합성, 재활용성이 실용적인 형태로 조화를 이루어 기능해야 합니다. 독일에서 이러한 운영상의 균형이 중요한 이유는 많은 가공업체들이 고속 생산 라인을 가동하고 있어, 포장의 품질이나 외관을 해치지 않으면서도 효율적인 처리 능력을 뒷받침할 수 있는 기재를 필요로 하기 때문입니다. 화이트 라이닝 칩보드 역시 식품 외부 포장재나 저가 소비재 분야에서 여전히 중요한 위치를 차지하고 있지만, 재생 섬유 등급은 에너지 관련 비용 변동의 영향을 더 쉽게 받기 때문에 2026년에는 경제성이 더 큰 압박에 직면할 것으로 보입니다.

솔리드 블리치드 보드(SBB)는 가장 빠르게 성장하는 등급으로, 2026-2031년 연평균 성장률(CAGR) 7.53%를 나타낼 것으로 전망됩니다. 독일의 카톤 보드 시장 규모 중 이 분야는 보다 깔끔한 시각적 효과와 더욱 강력한 위생적 매력을 요구하는 화장품 및 OTC(일반의약품) 용도에 의해 주도되고 있습니다. 브랜드 소유주들은 더 밝은 표면, 더 균일한 인쇄 결과, 그리고 더 철저한 제품 보호를 원하고 있으며, 재생지의 대체재로 일관된 마감을 얻을 수 없는 경우 특정 포장을 SBB나 기타 프리미엄 신섬유 등급으로 꾸준히 전환하고 있습니다. 액체 포장용 카톤 보드(LPB)와 푸드서비스용 카톤 보드(FSB)는 여전히 시장 규모가 작지만, 음료 및 식품 접촉용 포장이 여전히 차단 성능이 필요한 섬유 기반 디자인으로 더욱 전환됨에 따라 두 제품 모두 수요가 증가하고 있습니다. 무표백 카톤 보드(SBB)는 식품 안전 용도나 크라프트 스타일의 프리미엄 제품 시장을 중심으로 한 소규모 틈새 시장에 대응하고 있으며, 그 시장 점유율은 접이식 상자용 카톤 보드나 SBB에 비해 제한적이긴 하지만 그 역할은 안정적입니다. 각 등급 전반을 살펴보면, 독일의 카톤 보드 시장에서는 입증된 재활용 가능성과 차단 성능의 신뢰성이 더욱 중요시되고 있으며, 이에 따라 검증된 재활용 가능 제품 포트폴리오와 명확한 기술 문서를 보유한 공급업체의 위상이 높아지고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJYAccording to Mordor Intelligence, the germany cartonboard market size was valued at USD 2.01 billion in 2025 and is estimated to grow from USD 2.10 billion in 2026 to reach USD 2.63 billion by 2031, at a CAGR of 4.60% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), End-User Industry (Food, Beverage, Pharmaceutical and Healthcare, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Cartonboard Market Trends and Insights

PPWR-Led Recyclability-By-Design Adoption

The PPWR entered into force in February 2025 and moves into its core operational phase in August 2026, which means packaging placed on the EU market must align more clearly with harmonized recyclability classifications and conformity requirements. In Germany, that requirement lands on top of an established compliance system, because the Zentrale Stelle Verpackungsregister and the VerpackG framework already give producers, converters, and brand owners a clear route for registration, data reporting, and recyclability assessment. Procurement behavior is already shifting ahead of the August 2026 milestone, with brand owners tightening tender specifications around recyclability, mono-material structures, and documentation that can withstand closer regulatory review. That change improves the position of cartonboard against paper-plastic-foil structures because fiber packs can meet both design and recyclability expectations with fewer material conflicts. It also improves the standing of mills that can offer certified recyclable portfolios and clearer traceability across grades, coatings, and converting steps. As those declarations become part of routine packaging governance, the Germany cartonboard market is moving toward higher-specification demand instead of simple volume replacement.

Plastic-To-Fiber Shift In Food And Beverage Packs

Plastic substitution in German food and beverage packaging is moving with more force because retailer mandates, consumer expectations, and EU-aligned packaging rules are all pointing toward recyclable fiber formats. Large own-label programs in food retail are giving that shift scale, because a single redesign decision can move substantial packaging volumes from plastic-heavy formats toward folding boxboard, foodservice board, and barrier-coated cartonboard. The commercial effect is not limited to tonnage, since food-contact conversion requires coatings and structures that can preserve product safety while still supporting recyclability claims, which raises the technology threshold for suppliers. That is why the Germany cartonboard market is gaining a larger premium layer inside food packaging, rather than only adding lower-value replacement volumes. Henkel and MM Board and Paper illustrated this direction in 2025 when they replaced a blister pack with a 100% cartonboard solution using TOPCOLOR(R) BARRIER AROMA, and that pack won the German Packaging Award 2025. Because food represented 46.21% of 2025 revenues, continued redesign activity in this end-use gives the Germany cartonboard market a large and durable platform for further coating and product development.

Energy And Recovered-Fiber Cost Volatility

Energy volatility remains the most immediate cost risk for the Germany cartonboard market in 2026, because mills are still operating in an environment where fuel, transport, and input costs can move quickly and unevenly. Mayr-Melnhof stated in its April 2026 trading update that significantly higher energy, transport, and chemical costs were the main driver of margin compression, and management said these pressures had become noticeable since March 2026. Recycled-fiber grades are especially exposed because their economics are more sensitive to energy-intensive processing and to changes in recovered paper pricing. Germany's strong collection and recovery system helps keep supply chains active, but that same concentration can make cost movements in recovered fiber pass through mills faster than producers would prefer. Operators with co-generation assets, biomass systems, or power purchase agreements are better placed to absorb sudden cost shifts, yet those investments also require capital at a time when selling prices are under pressure. The result is a sharper split between suppliers that can defend margins and those that face weaker flexibility as the Germany cartonboard market moves through the current cost cycle.

Other drivers and restraints analyzed in the detailed report include:

- Pharma And OTC Carton Demand Resilience

- Folding Carton Preference For Shelf Impact And Compliance

- European Cartonboard Overcapacity And Import Pressure

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding Boxboard held 38.13% of the Germany cartonboard market share in 2025, which kept it as the largest product grade across the country's cartonboard mix. Its lead comes from a broad fit across food retail, pharmaceutical secondary packaging, and premium consumer goods, where stiffness, printability, and recyclability all need to work together in a practical format. That operating balance matters in Germany because many converters run high-speed lines and need a substrate that supports efficient throughput without compromising pack quality or presentation. White-Lined Chipboard also remains important in outer food packs and lower-premium consumer goods, but its 2026 economics are under greater strain because recycled-fiber grades are more exposed to energy-linked cost volatility.

Solid Bleached Board is the fastest-growing grade, with a forecast CAGR of 7.53% from 2026 to 2031, and this part of Germany cartonboard market size is being lifted by cosmetics and OTC healthcare applications that require cleaner visual performance and stronger hygiene positioning. Brand owners moving toward brighter surfaces, more even print results, and tighter product protection are steadily shifting selected packs toward SBB and other premium fresh-fiber grades when recycled alternatives cannot deliver a consistent finish. Liquid Packaging Board and Food Service Board remain narrower in scale, but both gain when beverage and food-contact packs move further into fiber-based designs that still need barrier performance. Solid Unbleached Board serves a smaller niche centered on food-safe uses and kraft-style premium positioning, which keeps its role stable even if its share is more limited than Folding Boxboard or SBB. Across the grade landscape, the Germany cartonboard market is putting more weight on documented recyclability and barrier credibility, which improves the standing of suppliers with verified recyclable portfolios and clearer technical documentation.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Mayr-Melnhof Karton Aktiengesellschaft

- Metsa Board Corporation

- Stora Enso Oyj

- RDM Group S.p.A.

- Holmen AB

- Billerud Aktiebolag

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Moritz J. Weig GmbH & Co. KG

- Edelmann GmbH

- August Faller GmbH & Co. KG

- STI - Gustav Stabernack GmbH

- Pankakoski Mill Oy

- Sappi Germany GmbH

- Sonoco Consumer Products Europe GmbH

- Koehler Paper SE

- WEIG-Packaging GmbH & Co. KG

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Impact of Macroeconomic Factors on the Market

- 4.3 Market Drivers

- 4.3.1 PPWR-Led Recyclability-by-Design Adoption

- 4.3.2 Plastic-to-Fiber Shift in Food and Beverage Packs

- 4.3.3 Pharma and OTC Carton Demand Resilience

- 4.3.4 Folding Carton Preference for Shelf Impact and Compliance

- 4.3.5 ZSVR Fee Incentives Favoring Pure-Fiber Designs

- 4.3.6 Barrier-Coated Board Replacing Plastic Windows and Fluorinated Formats

- 4.4 Market Restraints

- 4.4.1 Energy and Recovered-Fiber Cost Volatility

- 4.4.2 European Cartonboard Overcapacity and Import Pressure

- 4.4.3 Reusable Foodservice Rules Limiting One-Way Pack Growth

- 4.4.4 Barrier Reformulation and Requalification Costs

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Mayr-Melnhof Karton Aktiengesellschaft

- 6.4.2 Metsa Board Corporation

- 6.4.3 Stora Enso Oyj

- 6.4.4 RDM Group S.p.A.

- 6.4.5 Holmen AB

- 6.4.6 Billerud Aktiebolag

- 6.4.7 Smurfit Westrock plc

- 6.4.8 Graphic Packaging International, LLC

- 6.4.9 Moritz J. Weig GmbH & Co. KG

- 6.4.10 Edelmann GmbH

- 6.4.11 August Faller GmbH & Co. KG

- 6.4.12 STI - Gustav Stabernack GmbH

- 6.4.13 Pankakoski Mill Oy

- 6.4.14 Sappi Germany GmbH

- 6.4.15 Sonoco Consumer Products Europe GmbH

- 6.4.16 Koehler Paper SE

- 6.4.17 WEIG-Packaging GmbH & Co. KG

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment