|

시장보고서

상품코드

2073557

카톤 보드 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

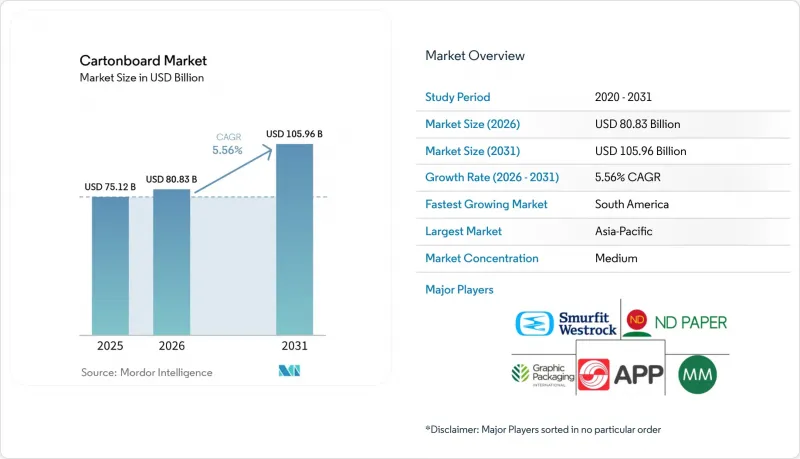

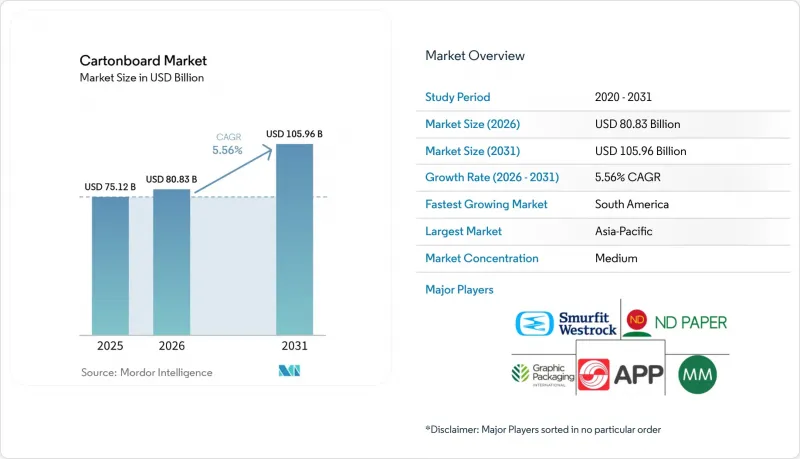

Mordor Intelligence에 의하면, 카톤 보드 시장 규모는 2025년에 761억 2,000만 달러, 2026년에 808억 3,000만 달러가 되어, 2031년까지 1,059억 6,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 5.56%로 성장할 전망입니다.

본 보고서는 제품 등급(고형 표백 카톤 보드, 고형 미표백 카톤 보드, 접이식 골카톤 보드, 뒷면 백색 칩보드, 액체 포장용 카톤 보드, 푸드서비스용 카톤 보드), 포장 형태(접이식 상자, 액체 포장 등), 최종 사용 산업(식품, 음료, 제약 및 헬스케어 등), 지역(북미, 유럽 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

세계 카톤 보드 시장 동향 및 분석

전자상거래 분야에서 카톤 보드 대체재의 급증

전자상거래 물류 네트워크에서는 제품 보호와 소포의 효율성을 유지하면서, 기존의 무거운 운송용 포장재에서 더 가벼운 카톤 보드 상자 형태로의 전환이 진행되고 있습니다. 소포의 무게가 줄어들고, 부피 중량에 따른 배송비가 낮아지는 것은 플랫폼 및 가공업체 차원에서 포장재 선택에 직접적인 영향을 미치기 때문에 이러한 변화는 카톤 보드 시장에서 중요한 의미를 지닙니다. 또한, 자동 주문 처리 라인에서 안정적으로 가동할 수 있는 200-250 g/m² 범위의 접이식 카톤 보드에 대한 수요도 증가하고 있습니다. 풀필먼트 센터에서는 고속 포장 설비의 가동 중단을 방지하기 위해 균일한 두께와 기계 방향에 대한 높은 강성이 요구되고 있으며, 품질 기준은 점점 더 엄격해지고 있습니다. 배송이 집중되는 지역 인근에서 이러한 사양을 충족할 수 있는 제조업체는 당일·익일 배송 모델의 확대에 따라 프리미엄 비즈니스 확보에 유리한 입장에 있습니다.

FMCG 업계에서 플라스틱이 없는 1차 포장로의 전환

소비자들의 엄격한 감시와 확대되는 생산자 책임 제도에 따른 비용으로 인해 플라스틱 사용을 정당화하기 어려워짐에 따라, 대형 FMCG 기업들은 플라스틱 포장을 섬유 기반 포장으로 대체하고 있습니다. 네슬레는 2024년 5월, 영국에서 “네스카페”를 대상으로 가정용 쓰레기로 재활용이 가능한 종이 리필 팩을 출시했으며, 2024년 하반기에는 “퀄리티 스트리트”용 종이 포장재의 시범 도입도 실시했습니다. 이는 종이 포장재가 틈새 시장용 선택지에 그치지 않고, 브랜드 소비재의 포장 분야로 진출하고 있음을 보여줍니다. 마스사는 종이 대체재를 도입함으로써 1,071메트르톤의 다층 플라스틱 소재를 감축했다고 발표했으며, 이 감축량의 75%는 북미에서 M&M's의 파우치 포장 전환에 기인한 것입니다. 이러한 포장 방식의 변화는 판매량이 많은 주요 식품·과자 부문 전반에 걸쳐 수요를 확대함으로써 카톤 보드 시장을 뒷받침하고 있습니다. 그 가치 제안은 단순한 지속가능성에 그치지 않습니다. 팔레트의 적재 밀도를 높임으로써 물류 효율이 향상되고, 카톤 보드 포장재의 원자재 비용 상승에 따른 영향을 완화할 수 있기 때문입니다.

에너지 가격 변동이 제지 공장의 이익률을 압박하고 있습니다.

에너지 비용의 변동은 제지 공장의 경쟁력과 이익률의 안정성에 직접적인 영향을 미치기 때문에 카톤 보드 시장에서는 여전히 가장 큰 단기적 제약 요인으로 남아 있습니다. 아소카르타(Assocarta)의 보고서에 따르면, 2025년 10월 이탈리아의 전력 도매 가격은 평균 1MWh당 111유로(125달러)였던 반면, 독일에서는 1MWh당 84유로(95달러), 프랑스에서는 1MWh당 57유로(64달러)였으며, 이는 유럽 내에서도 비용 상황이 얼마나 크게 차이가 날 수 있는지를 보여주고 있습니다. 이러한 격차는 시장 변동에 대한 내성이 낮고, 전기 요금 급등을 감당할 여력이 적은 비통합형 제지 공장에 있어 가장 큰 문제가 됩니다. 스마핏 웨스트록(SmartFit Westlock)사 역시 2026년 1분기 전망에서 원자재비 급등과 에너지 가격 상승으로 인한 예상되는 영향을 지적하고 있으며, 이러한 압박이 일시적인 것이 아니라 여전히 지속되고 있음을 뒷받침하고 있습니다. 재생에너지 및 바이오매스 자산을 보유한 대형 제조업체들은 보다 강력한 보호를 받고 있기 때문에 주요 통합형 그룹과 소규모 지역 사업자 간의 구조적 격차가 확대되고 있습니다.

부문별 분석

2025년, 접이식 카톤 보드는 카톤 보드 시장 점유율의 31.84%를 차지했으며, 인쇄 품질, 강성, 차단 성능이 요구되는 식품, 의약품, 화장품 용도로 사용되고 있어 여전히 가장 큰 제품 등급으로 자리매김했습니다. 이 등급은 규제가 엄격하고 브랜드 영향력이 큰 카테고리에서 외관과 기능성의 균형이 잘 잡혀 있어, 소비자용 포장용 카톤 보드 시장의 핵심을 이루고 있습니다. 무표백 단판 및 표백 단판은 밝기, 강도, 내습성이 더욱 중요시되는 외식 산업, 고급 제품, 음료의 2차 포장 등 보다 전문적인 요구를 지속적으로 충족시키고 있습니다. 화이트 라이닝 칩보드는 외관이 여전히 중요한 요소이며 원자재 비용이 엄격하게 관리되는 비식품 소매 포장 분야에서 비용 효율성이 뛰어난 대안으로서의 역할을 유지해 왔습니다. 액체 포장용 카톤 보드 역시 여전히 중요하며, 특히 유제품, 주스, 식물성 음료 분야에서는 무균 충진 기술을 통해 냉장 보관 없이도 유통 기한이 연장되고 있습니다.

외식 산업용 카톤 보드 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 6.18%를 나타낼 것으로 예측되며, 카톤 보드 시장에서 가장 빠르게 성장하는 제품 등급이 될 전망입니다. 이러한 성장의 주된 요인은 일회용 플라스틱 사용 금지 조치로 인해, 플라스틱 라이닝이나 폴리스티렌 용기에서 컵, 컨테이너, 테이크아웃 용기에 사용되는 PFAS 무첨가 코팅 카톤 보드로 수요가 이동하고 있기 때문입니다. Sappi사는 2025년 5월, 서머셋 공장의 PM2 전환 및 확장을 완료하고, 총 5억 2,500만 달러의 자본 지출을 투입하여 고형 표백 황산 펄프의 생산 능력을 연간 24만 톤에서 48만 톤으로 두 배로 늘렸습니다. 이 투자는 생산자들이 쇠퇴 추세를 보이는 그래픽 용지 부문에서 성장률이 높은 포장용 등급으로 자산을 전환하고 있는 실태를 보여줍니다. 또한, 미국 및 유럽의 식품 접촉 기준을 준수함으로써 고급 외식 산업용 카톤 보드 공급업체들은 품질 면에서 경쟁 우위를 확보하고 있으며, 이는 카톤 보드 업계의 견실한 이익률을 뒷받침하고 있습니다.

지역별 분석

2025년, 아시아태평양은 카톤 보드 시장 점유율의 43.62%를 차지했으며, 중국, 인도, 일본, 한국, 호주의 성장에 힘입어 전 세계 수요 기반에서 여전히 가장 큰 가치 중심지로 자리매김했습니다. 중국의 전자상거래, 식품 및 음료, 전자기기 포장 분야의 대규모 시장이 계속해서 지역 수요를 뒷받침한 반면, 인도는 FMCG(일용소비재)의 성장과 소비자용 포장 분야에서 플라스틱 대체 움직임을 통해 수요를 견인했습니다. 나인 드래곤스 페이퍼사는 2026년도 상반기 동안 사상 최대 판매량인 1,240만 톤을 기록했으며, 순이익은 전년 동기 대비 225.1% 증가했습니다. 이는 중국 내 통합형 카톤 보드 생산의 강점을 반영한 것입니다. 또한, 일본의 편의점 모델 역시 빈번한 재고 보충 주기로 인해 사용되는 정밀 성형 접이식 카톤 보드 상자에 대한 안정적인 수요를 지속적으로 뒷받침했습니다. 한국과 호주는 여전히 프리미엄 포장 시장으로 자리 잡고 있으며, 지속가능성을 중시하는 대체 흐름이 카톤 보드 시장을 지속적으로 뒷받침하고 있습니다.

남미는 2026년부터 2031년까지 연평균 성장률(CAGR) 6.57%를 나타낼 것으로 예측되며, 카톤 보드 시장에서 가장 빠르게 성장하는 지역이 될 전망입니다. 브라질은 여전히 이 지역 최대의 포장용지 생산 거점이며, ABRE의 보고서에 따르면 2025년 1분기 포장용지 생산량은 1.6%, 2분기는 1.8% 증가했습니다. 크라빈사는 2025년 3월, 피라시카바 II 공장을 가동했습니다. 이 회사는 15억 6,000만 레알(2억 7,400만 달러)을 투자해 카톤 보드 포장재의 연간 생산 능력을 24만 톤으로 확대함으로써, 지역의 가공 및 물류 인프라를 강화했습니다. 북미 역시 식품, 음료, 의약품의 포장 수요에 더해, 2026년 초 무역 불확실성에 따라 국내 조달로의 전환이 진행된 것을 배경으로, 카톤 보드 시장의 주요 수요 거점으로 자리매김했습니다. 중동 및 아프리카는 도시화, 현대적인 소매업의 확대, 액체 포장재의 채택 확대가 견조한 수요 증가를 뒷받침하며, 계속해서 신흥 성장 지역으로 자리매김했습니다.

유럽에서는 재활용이 가능한 섬유계 포장재 사용을 장려하는 규제의 긍정적 효과가 계속해서 나타났습니다. 2025년 2월 PPWR이 발효됨에 따라, 유럽연합(EU) 전역에서 재활용 가능한 포장 형태를 채택하도록 하는 정책적 추진이 더욱 강화되었습니다. 서유럽은 식품, 음료, 의약품 수요의 주요 중심지로서의 위상을 유지해 왔으며, 이러한 분야의 조달 기준이 고품질 카톤 보드 등급의 사용을 촉진했습니다. 또한 독일은 재생 가능한 원자재와 검증된 회수 시스템에 대한 수요를 강화하는 90% 회수율 목표를 포함해, 종이, 카톤 보드, 카톤 보드의 회수 체계가 잘 갖춰져 있다는 점에서 두드러졌습니다. 한편, 스칸디나비아와 이탈리아에서 버진 펄프의 신규 생산 능력이 확대됨에 따라, 일부 유럽의 재활용 카톤 보드 공장에는 공급 압박이 가중되었습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.07.09According to Mordor Intelligence, the cartonboard market size is projected to be USD 76.12 billion in 2025, USD 80.83 billion in 2026, and reach USD 105.96 billion by 2031, growing at a CAGR of 5.56% from 2026 to 2031.

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, and More), End-User Industry (Food, Beverage, Pharma and Healthcare, and More), and Geography (North America, Europe, and More). The Market Forecasts are Provided in Terms of Value (USD).

Global Cartonboard Market Trends and Insights

E-Commerce Cartonboard Substitution Surge

E-commerce logistics networks are moving from heavier transport packs toward lighter cartonboard formats where product protection and parcel efficiency can still be maintained. This shift matters in the cartonboard market because lower parcel mass and lower dimensional-weight charges directly change packaging material choices at the platform and converter level. Demand is also rising for folding boxboard grades in the 200 g/m2-250 g/m2 range that can run consistently on automated fulfillment lines. The quality bar is becoming stricter, as fulfillment centers need uniform caliper and strong machine-direction stiffness to avoid disruptions to high-speed packing equipment. Producers that can meet these specifications near dense delivery corridors are better positioned to win premium business as same-day and next-day delivery models expand.

FMCG Pivot To Plastic-Free Primary Packaging

Large FMCG companies are replacing plastic formats with fiber-based packs as consumer scrutiny and extended producer responsibility costs make plastic usage harder to justify. Nestle launched a curbside-recyclable paper refill pack for Nescafe in the UK in May 2024, and it also piloted paper packs for Quality Street later in 2024, showing that paper formats are moving into branded consumer packaging rather than remaining a niche option. Mars stated that it removed 1,071 metric tons of multilayer plastic materials by using paper alternatives, with 75% of that reduction coming from converting M&M's pouches in North America. These packaging shifts support the cartonboard market by expanding demand across mainstream food and confectionery categories with high unit volumes. The value proposition is broader than sustainability alone, since denser pallet configurations can also improve logistics efficiency and soften the higher input cost of paperboard formats.

Energy Price Volatility Compresses Mill Margins

Energy cost volatility remains the largest near-term constraint on the cartonboard market because it directly affects mill competitiveness and margin stability. Assocarta reported that Italy's wholesale electricity price averaged EUR 111 (USD 125) per MWh in October 2025, compared with EUR 84 (USD 95) per MWh in Germany and EUR 57 (USD 64) per MWh in France, showing how sharply cost conditions can diverge inside Europe. These gaps matter most for non-integrated mills, which have less insulation from market swings and less room to absorb higher utility bills. Smurfit WestRock also pointed to higher input costs and expected effects from rising energy prices in its Q1 2026 outlook, which confirms that the pressure remained active rather than temporary. Larger producers with renewable energy and biomass assets are better protected, widening the structural gap between major integrated groups and smaller regional operators.

Other drivers and restraints analyzed in the detailed report include:

- Single-Use Plastic Bans In Food And Personal Care Packaging

- Lightweighting Lowers Freight And Warehousing Costs

- Recycled Fiber Availability And Quality Imbalance

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Folding boxboard held 31.84% of the cartonboard market share in 2025 and remained the largest product grade because it serves food, pharmaceutical, and cosmetic applications that demand print quality, stiffness, and barrier performance. The grade has become central to the cartonboard market in consumer packaging because it balances appearance and functionality across regulated and highly branded categories. Solid bleached board and solid unbleached board continued to serve more specialized needs in food service, luxury goods, and beverage secondary packaging, where brightness, strength, or wet resistance mattered more. White-lined chipboard retained its role as a cost-effective option for non-food retail packaging where appearance still matters, but input costs are closely watched. Liquid packaging board also remained important, especially in dairy, juice, and plant-based beverages, where aseptic filling extends shelf life without refrigeration.

The food service board segment is projected to grow at a 6.18% CAGR during 2026-2031, making it the fastest-growing product grade in the cartonboard market. The main support comes from single-use plastic bans that are redirecting demand from plastic-lined and polystyrene formats toward PFAS-free coated cartonboard used in cups, containers, and takeaway packs. Sappi completed the conversion and expansion of Somerset Mill PM2 in May 2025, doubling solid bleached sulfate board capacity from 240,000 tpy to 480,000 tpy with total capital expenditure of USD 525 million. That investment showed how producers are shifting assets away from declining graphic paper and toward higher-growth packaging grades. Compliance with food-contact standards in the United States and Europe also gives premium foodservice board suppliers a quality moat that supports margin resilience within the cartonboard industry.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- By Geography

- North America

- United States

- Canada

- Mexico

- South America

- Brazil

- Argentina

- Rest of South America

- Europe

- United Kingdom

- Germany

- France

- Spain

- Italy

- Russia

- Rest of Europe

- Asia-Pacific

- China

- India

- Japan

- Australia

- South Korea

- Rest of Asia-Pacific

- Middle East and Africa

- Middle East

- Saudi Arabia

- United Arab Emirates

- Turkey

- Rest of Middle East

- Africa

- South Africa

- Kenya

- Rest of Africa

- Middle East

- North America

Geography Analysis

Asia-Pacific accounted for 43.62% of the cartonboard market share in 2025 and remained the largest value center within the broader global demand base, driven by China, India, Japan, South Korea, and Australia. China's scale in e-commerce, food and beverage, and electronics packaging continued to anchor regional demand, while India added support through FMCG growth and plastic substitution in consumer packaging. Nine Dragons Paper reported record sales volume of 12.4 million tonnes in 1H FY2026, with net profit up 225.1% year on year, reflecting the strength of integrated paperboard production in China. Japan's convenience retail model also sustained steady demand for precision-formatted folding cartons used in frequent replenishment cycles. South Korea and Australia remained premium packaging markets where sustainability-driven substitution continued to support the cartonboard market.

South America is projected to expand at a 6.57% CAGR during 2026-2031, making it the fastest-growing region in the cartonboard market. Brazil remained the region's largest packaging paper base, and ABRE reported packaging production growth of 1.6% in the first quarter of 2025 and 1.8% in the second quarter of 2025. Klabin inaugurated its Piracicaba II facility in March 2025, investing BRL 1.56 billion (USD 274 million) and achieving an annual corrugated packaging capacity of 240,000 tonnes, strengthening regional conversion and logistics infrastructure. North America also remained a major demand hub for the cartonboard market, supported by food, beverage, and pharmaceutical packaging demand and by domestic sourcing shifts after early 2026 trade uncertainty. The Middle East and Africa remained an emerging growth zone, with urbanization, modern retail expansion, and rising adoption of liquid packaging supporting steady demand growth.

Europe continued to benefit from rules that encourage the use of recyclable fiber-based packaging. The PPWR entered into force in February 2025 and sharpened the policy push toward recyclable packaging formats across the European Union. Western Europe remained a major center for food, beverage, and pharmaceutical demand, and procurement standards in these sectors supported the use of premium board grades. Germany also stood out for its strong paper, board, and carton collection framework, including a 90% quota that reinforces demand for recyclable materials and verified recovery systems. At the same time, new virgin-fiber capacity in Scandinavia and Italy increased supply pressure on some European recycled-board mills.

- Asia Pulp & Paper Company Ltd.

- Mayr-Melnhof Karton AG

- Nine Dragons Paper (Holdings) Limited

- Smurfit WestRock plc

- Graphic Packaging Holding Company

- Stora Enso Oyj

- International Paper Company

- Metsa Board Corporation

- Pankaboard Oyj

- Klabin S.A.

- Oji Holdings Corporation

- Mondi plc

- Rengo Co., Ltd.

- Lee & Man Paper Manufacturing Ltd.

- Georgia-Pacific LLC

- Clearwater Paper Corporation

- Sappi Limited

- Holmen AB

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 E-Commerce Cartonboard Substitution Surge

- 4.2.2 FMCG Pivot to Plastic-Free Primary Packaging

- 4.2.3 Lightweighting Lowers Freight and Warehousing Costs

- 4.2.4 Single-Use Plastic Bans in Food and Personal Care Packaging

- 4.2.5 High-Speed Digital Printing Supports SKU Proliferation

- 4.2.6 Premiumization in Luxury and Beauty Cartons

- 4.3 Market Restraints

- 4.3.1 Energy Price Volatility Compresses Mill Margins

- 4.3.2 Recycled Fiber Availability and Quality Imbalance

- 4.3.3 Barrier Coating Compliance Raises Capex and Operating Costs

- 4.3.4 Molded Fiber and Flexible Paper Substitution in Some Applications

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Investment Analysis

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Bargaining Power of Suppliers

- 4.9.2 Bargaining Power of Buyers

- 4.9.3 Threat of New Entrants

- 4.9.4 Threat of Substitute Products

- 4.9.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Argentina

- 5.4.2.3 Rest of South America

- 5.4.3 Europe

- 5.4.3.1 United Kingdom

- 5.4.3.2 Germany

- 5.4.3.3 France

- 5.4.3.4 Spain

- 5.4.3.5 Italy

- 5.4.3.6 Russia

- 5.4.3.7 Rest of Europe

- 5.4.4 Asia-Pacific

- 5.4.4.1 China

- 5.4.4.2 India

- 5.4.4.3 Japan

- 5.4.4.4 Australia

- 5.4.4.5 South Korea

- 5.4.4.6 Rest of Asia-Pacific

- 5.4.5 Middle East and Africa

- 5.4.5.1 Middle East

- 5.4.5.1.1 Saudi Arabia

- 5.4.5.1.2 United Arab Emirates

- 5.4.5.1.3 Turkey

- 5.4.5.1.4 Rest of Middle East

- 5.4.5.2 Africa

- 5.4.5.2.1 South Africa

- 5.4.5.2.2 Kenya

- 5.4.5.2.3 Rest of Africa

- 5.4.5.1 Middle East

- 5.4.1 North America

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Asia Pulp & Paper Company Ltd.

- 6.4.2 Mayr-Melnhof Karton AG

- 6.4.3 Nine Dragons Paper (Holdings) Limited

- 6.4.4 Smurfit WestRock plc

- 6.4.5 Graphic Packaging Holding Company

- 6.4.6 Stora Enso Oyj

- 6.4.7 International Paper Company

- 6.4.8 Metsa Board Corporation

- 6.4.9 Pankaboard Oyj

- 6.4.10 Klabin S.A.

- 6.4.11 Oji Holdings Corporation

- 6.4.12 Mondi plc

- 6.4.13 Rengo Co., Ltd.

- 6.4.14 Lee & Man Paper Manufacturing Ltd.

- 6.4.15 Georgia-Pacific LLC

- 6.4.16 Clearwater Paper Corporation

- 6.4.17 Sappi Limited

- 6.4.18 Holmen AB

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment