|

시장보고서

상품코드

2072769

미국의 카톤 보드 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)United States Cartonboard - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

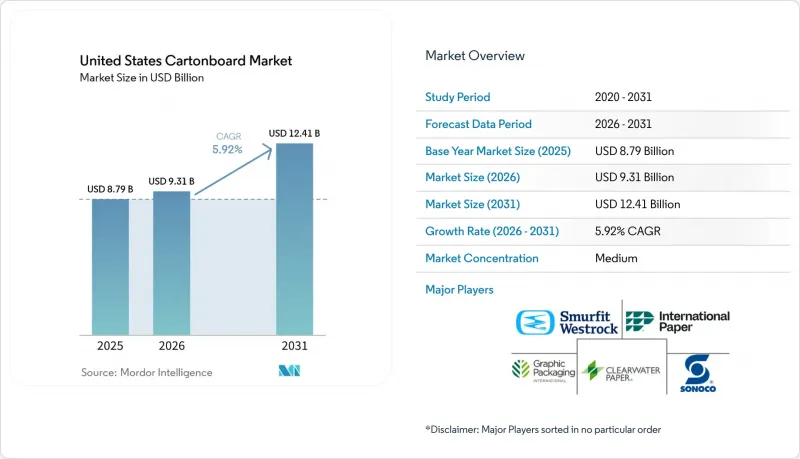

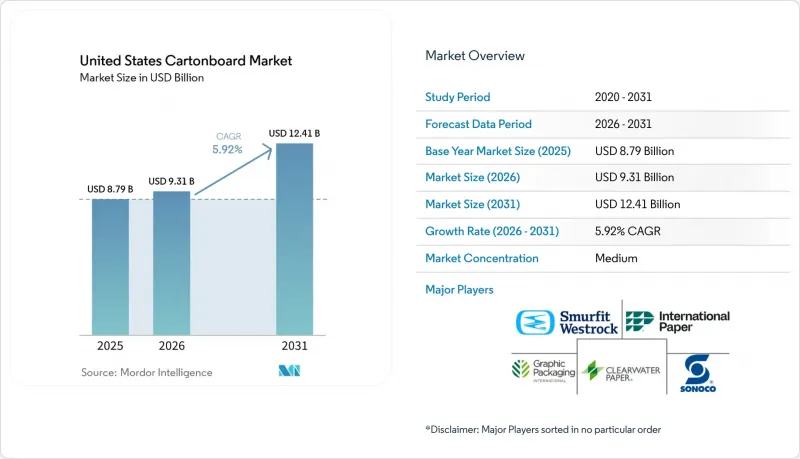

Mordor Intelligence에 의하면, 미국 카톤 보드 시장 규모는 2025년에 87억 9,000만 달러로 평가되었고 2026년 93억 1,000만 달러에서 2031년까지 124억 1,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 5.92%를 나타낼 전망입니다.

본 보고서는 제품 등급(고형 표백 카톤 보드, 고형 미표백 카톤 보드, 접이식 상자용 카톤 보드, 화이트 라이닝 칩보드, 액체 포장용 카톤 보드, 푸드서비스용 카톤 보드), 포장 형태(접이식 상자, 액체 포장, 슬리브 및 트레이 등), 그리고 최종 사용자 산업(식품, 음료, 제약 및 헬스케어, 담배 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

미국 카톤 보드 시장 동향과 인사이트

포장 식품 및 신선식품·편의점 식품에 대한 수요 증가

식품은 미국 카톤 보드 시장에서 여전히 가장 광범위한 수요 기반을 형성하고 있으며, 2025년에는 건조 식품, 냉동 식품, 냉장 제품 및 편의성을 중시한 포맷을 합쳐 총 수요의 38.14%를 차지했습니다. 또한, 식품 구성 면에서도 프리미엄 건강식품, 밀키트, 자사 브랜드 식품 라인에서 원재료의 투명성, 보존성 확보 및 매장 내 존재감 제고를 보여주는 브랜드 카톤 보드 포장재로 전환했습니다. 페이퍼보드 패키징 협의회(Paperboard Packaging Council)가 Fastmarkets RISI와 공동으로 작성한 2025-26년 전망에 따르면, 식품은 2029년까지 연평균 1% 이상 성장할 것으로 예상되는 7대 최종 용도 시장 중 하나로 꼽혔으며, 이는 카톤 보드 소비량을 안정적으로 뒷받침하는 요인이 되었습니다. 이러한 수요 양상은 내습성, 내유성 및 식품 접촉 용도에 관한 FDA의 21 CFR 요건 준수 등 특정 성능 요건을 충족하는 등급을 선호하는 경향을 보였습니다. 그 결과, 미국의 카톤 보드 시장에서는 광범위한 상품 유통 채널을 통해 차별화되지 않은 제품을 대량으로 판매하는 것보다, 특정 사양을 충족할 수 있는 공급업체가 점점 더 높이 평가받게 되었습니다. 이러한 변화로 인해 단순한 대량 조달이 아닌, 기능, 규정 준수, 브랜드 가치를 기준으로 선정하는 구매자가 늘어나면서 수익의 질도 향상되었습니다.

헬스 & 뷰티 포장 분야의 프리미엄화와 매장 내 임팩트에 대한 요구

헬스케어, 미용, 퍼스널케어 분야의 각 브랜드는 특히 인쇄 품질이나 패키지 마감 상태가 소매 구매 결정에 영향을 미치는 경우, 가격 포지셔닝의 시각적 요소로 카톤 보드를 활용했습니다. Circana사의 보고서에 따르면, 2025년 미국의 프리미엄 화장품 소매 매출액은 전년 대비 4% 증가한 360억 달러에 달한 반면, 대중 시장용 화장품 매출액은 5% 증가한 727억 달러를 기록했으며, 프리미엄 및 가성비 제품 모두에서 카톤 보드 포장재에 대한 수요가 활발하게 이어졌습니다. 프리미엄 브랜드들은 고휘도의 무지 표백 카톤 보드나 세련된 접이식 카톤 보드의 마감을 선호하는 경향이 있었습니다. 한편, 대중 시장 브랜드는 완전히 럭셔리 등급의 사양으로 전환하지는 않으면서도 그래픽과 구조를 업그레이드함으로써 매장에서의 가시성을 높였습니다. 또한 캘리포니아주, 콜로라도주, 메인주, 메릴랜드주, 미네소타주, 오리건주, 워싱턴주에서는 2026년부터 2027년까지 주 차원의 포장재 EPR(생산자 책임 회수) 법 시행이 지속됨에 따라, 재활용 가능한 섬유계 포장재의 도입이 더욱 촉진되었습니다. 이러한 정책 환경으로 인해, 회수가 어렵고 향후 수수료 부담 위험에 노출되기 쉬운 복잡한 다중 소재 포장에 비해, 섬유계 포장은 규정 준수 측면에서 실용적인 우위를 차지했습니다. 미국 카톤 보드 시장에서 이는 미적 가치와 규제 준수 여부가 점점 더 밀접하게 연결되고 있음을 의미하며, 화장품 코너에서 접이식 카톤 보드에 대한 지속적인 수요를 뒷받침했습니다.

버진 펄프, 에너지 및 운송 비용의 변동

2026년에는 펄프, 에너지, 운송비에 대한 부담이 동시에 가중되면서, 투입 비용의 인플레이션이 계속해서 미국 카톤 보드 시장에 있어 가장 시급한 제약 요인으로 작용했습니다. 소노코사는 2026년 4월부터 무도장 재생 카톤 보드의 가격을 톤당 70달러 인상한다고 발표했으며, 이어 가공 카톤 보드 제품에 대해서도 8%의 가격 인상을 단행했습니다. 이는 비용 상승이 얼마나 신속하게 하류로 전가되고 있는지를 보여줍니다. 스마핏 웨스트록사는 2026년 6월부터 컨테이너용 카톤 보드 가격을 톤당 50달러 인상할 예정이며, 인터내셔널 페이퍼사도 에너지 비용과 운임 급등에 따라 같은 기간에 톤당 70달러의 가격 인상을 발표했습니다. 2026년 1분기 AF 및 PA 데이터에 따르면, 북미의 컨테이너보드 생산량은 전년 동기 대비 8% 이상 감소했으며, 이는 공급 상황이 긴박해지면서 생산자들의 가격 결정력이 강화되었음을 보여줍니다. 오하이오 주립대학교 역시 미국의 펄프 생산 비용이 남미보다 40% 높다는 분석 결과를 인용했는데, 이로 인해 국내 제조업체들은 갑작스러운 비용 충격을 내부적으로 흡수할 여지가 제한적이었습니다. 이러한 압박은 중소 가공업체들에게 가장 큰 타격이었습니다. 이는 그들의 구매력이 제한적이고, 조달 측면의 유연성이 낮으며, 폭넓은 제품 포트폴리오를 통해 인플레이션의 영향을 분산시킬 수 있는 능력도 부족했기 때문입니다.

부문별 분석

2025년, 액체 포장용 카톤 보드는 미국 카톤보드 시장의 29.31%를 차지하며, 국내에서 가장 큰 비중을 차지하는 제품 등급이 되었습니다. 이러한 선도적인 지위는 유제품, 주스, 식물성 음료, 무균 식품 등의 분야에서 꾸준한 수요가 뒷받침한 결과였으며, 이러한 분야에서는 차단 성능, 인쇄 적합성, 유통 기한과 같은 특징을 더 단순한 대체품으로 재현하는 것이 여전히 어려웠습니다. 고형 표백 카톤 보드는 의약품 및 화장품용 프리미엄 접이식 상자 분야에서 중요한 위치를 유지했습니다. 이는 규제 대상 용도에서 백도, 인쇄면, 그리고 식품·의약품과의 접촉에 관한 규정 준수 사항이 명확한 상업적 가치를 지녔기 때문입니다. 무표백 카톤 보드는 음료 멀티팩, 고급스러운 표면 외관보다 강성이 더 중요시되는 기타 강도 위주의 용도에서 그 적용 범위는 좁지만 안정적인 역할을 수행해 왔습니다. 접이식 상자용 카톤 보드는 헬스케어, 미용, 식품·식료품 부문에서 무표백 카톤 보드와 경쟁했으나, Stora Enso Oyj 및 Metsa Board Corporation과 같은 유럽 공급업체들은 2026년 미국 가공업체에 제품을 공급할 때 관세와 관련된 역풍에 직면했습니다.

푸드서비스용 카톤 보드는 미국 카톤 보드 시장에서 가장 빠르게 성장하고 있는 제품 등급으로, PFAS 배합 변경 및 플라스틱 대체가 실용화 단계로 접어들면서 2026년부터 2031년까지 연평균 성장률(CAGR) 6.18%로 확대될 것으로 예측됩니다. Sappi 북미는 메인주 서머셋 공장에서 “"LusterFSB OGR" 를 출시했습니다. 이 등급은 폴리에틸렌 코팅을 사용하지 않고도 내유성 및 내그리스성을 확보하도록 설계되어, 외식 산업용 가공 분야에서 시급히 요구되는 배합 변경 필요에 부응하고 있습니다. 클리어워터 페이퍼사는 2026년 3월, FDA 21 CFR 요건을 충족하는 경량 접이식 카톤 보드 용지 "Velora"를 출시했습니다. 이 제품은 프리미엄 SBS를 대체할 수 있는 가격 경쟁력을 중시하는 국내산 대체품을 찾는 가공업체를 주요 타겟으로 하고 있습니다. 2026년 5월 메인주에서 식물성 섬유 유래 PFAS가 포함된 식품 포장재에 대한 규제가 발효됨에 따라, 규제 압력은 더욱 거세졌습니다. 한편, 워싱턴주와 캘리포니아주는 식품 접촉용 포장재의 규정 준수 분야에서 계속해서 주도적인 역할을 수행하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the united states cartonboard market size was valued at USD 8.79 billion in 2025 and estimated to grow from USD 9.31 billion in 2026 to reach USD 12.41 billion by 2031, at a CAGR of 5.92% during the forecast period (2026-2031).

This report is Segmented by Product Grade (Solid Bleached Board, Solid Unbleached Board, Folding Boxboard, White-Lined Chipboard, Liquid Packaging Board, and Food Service Board), Packaging Format (Folding Cartons, Liquid Packaging, Sleeve and Tray, and More), and End-User Industry (Food, Beverage, Pharma and Healthcare, Tobacco, and More). The Market Forecasts are Provided in Terms of Value (USD).

United States Cartonboard Market Trends and Insights

Rising Packaged Food And Fresh Convenience Demand

Food remained the broadest demand base for the United States cartonboard market, accounting for 38.14% of total demand in 2025 across dry grocery, frozen meals, refrigerated products, and convenience-led formats. The food mix also shifted toward branded cartons that signaled ingredient clarity, storage integrity, and stronger shelf presence in premium health food, meal kit, and private-label grocery lines. The Paperboard Packaging Council's 2025-26 outlook, prepared with Fastmarkets RISI, identified food as one of 7 end-use markets expected to expand by more than 1% annually through 2029, and that supported a steady floor for board consumption. That demand pattern favored grades with specific performance requirements, including moisture resistance, grease resistance, and compliance with 21 CFR FDA requirements for food-contact uses. As a result, the United States cartonboard market increasingly rewarded suppliers that could qualify targeted specifications rather than sell undifferentiated tonnage into broad commodity channels. That shift also improved revenue quality because more buyers were selecting based on function, compliance, and branding value rather than on simple volume procurement.

Premiumization And Shelf-Impact Requirements In Health And Beauty Packaging

Health, beauty, and personal care brands used cartonboard as a visible part of price positioning, especially where print quality and pack finish influenced retail conversion. Circana reported that United States prestige beauty retail sales reached USD 36 billion in 2025, up 4% year over year, while mass beauty sales rose 5% to USD 72.7 billion, keeping demand active across both premium and value carton formats. Prestige brands leaned toward higher-brightness solid bleached board and refined folding carton finishes, while mass-market brands upgraded graphics and structure to improve shelf visibility without moving fully into luxury-grade specifications. State packaging EPR laws also strengthened the case for recyclable fiber formats because implementation continued in California, Colorado, Maine, Maryland, Minnesota, Oregon, and Washington during 2026 and 2027. That policy setting gave fiber-based packs a practical compliance edge over complex multi-material formats that were harder to recover and more exposed to future fee pressure. In the United States cartonboard market, this meant aesthetic value and regulatory fit increasingly moved together, which supported durable demand for folding cartons in beauty aisles.

Virgin Fiber, Energy, And Freight Cost Volatility

Input cost inflation remained the most immediate restraint on the United States cartonboard market because fiber, energy, and freight pressures rose simultaneously in 2026. Sonoco announced a USD 70 per ton price increase for uncoated recycled paperboard, effective in April 2026, followed by an 8% increase on converted paperboard products, showing how quickly higher costs were being passed downstream. Smurfit Westrock moved on a USD 50 per ton increase in containerboard, effective in June 2026, and International Paper announced USD 70 per ton hikes for the same period as energy and freight costs rose. AF and PA data for Q1 2026 showed North American containerboard production fell by more than 8% year over year, and that tightening supply conditions strengthened producer pricing power. The Ohio State University also cited analysis showing that United States pulp production costs were 40% higher than in South America, leaving domestic producers with less room to absorb sudden cost shocks internally. The pressure was most severe for smaller converters because they had limited buying leverage, narrower sourcing flexibility, and weaker ability to spread inflation across a broad product portfolio.

Other drivers and restraints analyzed in the detailed report include:

- Pharmaceutical Serialization And Tamper-Evident Carton Demand

- Shift From Plastic Rings To Paperboard Beverage Multipacks

- Food-Contact Compliance Constraints On Recycled And Barrier-Coated Board

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Liquid packaging board accounted for 29.31% of the United States cartonboard market in 2025, making it the largest product grade in the country. Its lead position came from durable demand across dairy, juice, plant-based beverages, and aseptic food formats, where barrier performance, printability, and shelf life remained difficult to replicate with simpler substitutes. Solid bleached board stayed important in premium folding carton applications for pharmaceuticals and beauty because brightness, print surface, and food or drug contact compliance carried clear commercial value in regulated uses. Solid unbleached board served a narrower but stable role in beverage multipacks and other strength-led applications where rigidity mattered more than premium surface appearance. Folding boxboard competed with SBB in health, beauty, and food grocery segments, although European suppliers such as Stora Enso Oyj and Metsa Board Corporation faced tariff-related headwinds in 2026 when serving United States converters.

Food service board was the fastest-growing product grade in the United States cartonboard market and was projected to advance at a 6.18% CAGR from 2026 to 2031 as PFAS reformulation and plastic substitution moved into commercial execution. Sappi North America introduced LusterFSB OGR at its Somerset Mill in Maine, and the grade was designed to deliver oil- and grease-resistance without polyethylene coatings, addressing an immediate reformulation need in foodservice converting. Clearwater Paper launched Velora in March 2026 as a lightweight folding carton paperboard that met FDA 21 CFR requirements and was targeted at converters seeking a cost-conscious domestic alternative to premium SBS. The regulatory pull grew stronger as Maine's plant-fiber PFAS food packaging restriction took effect in May 2026, while Washington and California continued to set the pace on food-contact packaging compliance.

Complete Report Scope:

- By Product Grade

- Solid Bleached Board

- Solid Unbleached Board

- Folding Boxboard

- White-Lined Chipboard

- Liquid Packaging Board

- Food Service Board

- By Packaging Format

- Folding Cartons

- Liquid Packaging

- Sleeve and Tray

- Other Packaging Formats (Cups, Foodservice Containers)

- By End-User Industry

- Food

- Beverage

- Pharmaceutical and Healthcare

- Tobacco

- Cosmetics and Toiletries

- Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

List of Companies Covered in this Report:

- Smurfit Westrock plc

- Graphic Packaging International, LLC

- Clearwater Paper Corporation

- Sonoco Products Company

- International Paper Company

- Huhtamaki Oyj

- Tetra Pak International S.A.

- SIG Group AG

- Elopak ASA

- Carton Service CSI, LLC

- Oliver Inc.

- Nosco, Inc.

- JohnsByrne Company

- Metsa Board Corporation

- Stora Enso Oyj

- Sappi North America, Inc.

- Billerud Aktiebolag (publ)

- Pactiv Evergreen Inc.

- Evergreen Packaging LLC

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Packaged Food and Fresh Convenience Demand

- 4.2.2 Premiumization and Shelf-Impact Requirements in Health and Beauty Packaging

- 4.2.3 Pharmaceutical Serialization and Tamper-Evident Carton Demand

- 4.2.4 Shift From Plastic Rings to Paperboard Beverage Multipacks

- 4.2.5 Higher-Paper-Content Aseptic Carton Innovation

- 4.2.6 Retailer Pull for PFAS-Free Fiber Foodservice Packaging

- 4.3 Market Restraints

- 4.3.1 Virgin Fiber, Energy, and Freight Cost Volatility

- 4.3.2 Food-Contact Compliance Constraints on Recycled and Barrier-Coated Board

- 4.3.3 PFAS Reformulation and Requalification Costs

- 4.3.4 Barcode, Serialization, and Converting-Line Upgrade Burdens

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Product Grade

- 5.1.1 Solid Bleached Board

- 5.1.2 Solid Unbleached Board

- 5.1.3 Folding Boxboard

- 5.1.4 White-Lined Chipboard

- 5.1.5 Liquid Packaging Board

- 5.1.6 Food Service Board

- 5.2 By Packaging Format

- 5.2.1 Folding Cartons

- 5.2.2 Liquid Packaging

- 5.2.3 Sleeve and Tray

- 5.2.4 Other Packaging Formats (Cups, Foodservice Containers)

- 5.3 By End-User Industry

- 5.3.1 Food

- 5.3.2 Beverage

- 5.3.3 Pharmaceutical and Healthcare

- 5.3.4 Tobacco

- 5.3.5 Cosmetics and Toiletries

- 5.3.6 Other End-User Industries (Toy, Apparel, Automotive, Household, Electrical, Foodservice)

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Smurfit Westrock plc

- 6.4.2 Graphic Packaging International, LLC

- 6.4.3 Clearwater Paper Corporation

- 6.4.4 Sonoco Products Company

- 6.4.5 International Paper Company

- 6.4.6 Huhtamaki Oyj

- 6.4.7 Tetra Pak International S.A.

- 6.4.8 SIG Group AG

- 6.4.9 Elopak ASA

- 6.4.10 Carton Service CSI, LLC

- 6.4.11 Oliver Inc.

- 6.4.12 Nosco, Inc.

- 6.4.13 JohnsByrne Company

- 6.4.14 Metsa Board Corporation

- 6.4.15 Stora Enso Oyj

- 6.4.16 Sappi North America, Inc.

- 6.4.17 Billerud Aktiebolag (publ)

- 6.4.18 Pactiv Evergreen Inc.

- 6.4.19 Evergreen Packaging LLC

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment