|

시장보고서

상품코드

2072917

인도의 국경간 전자상거래 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)India Cross-Border E-Commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

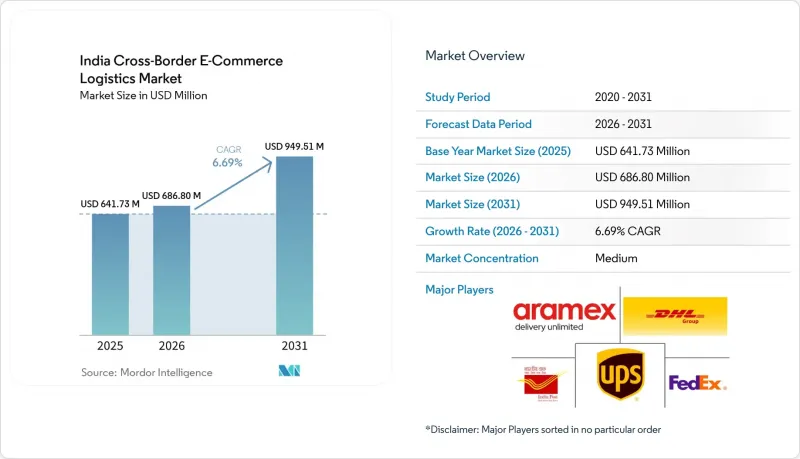

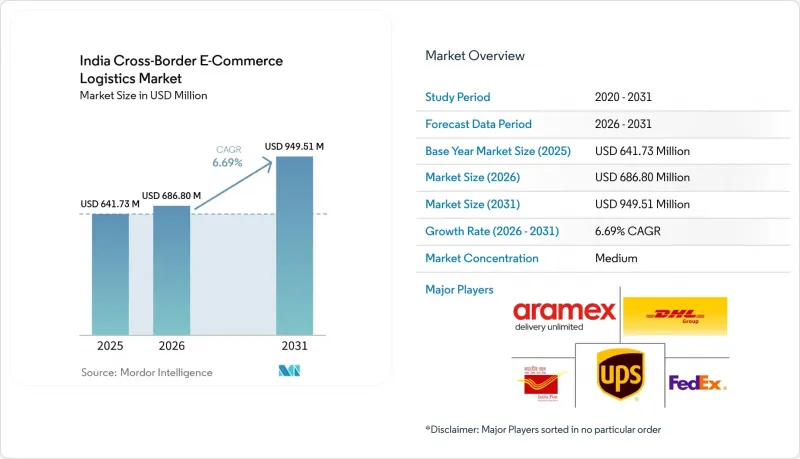

Mordor Intelligence에 의하면, 인도 국경간 전자상거래 물류 시장 규모는 2025년 6억 4,173만 달러에서 2026년에는 6억 8,680만 달러로 확대되어 2031년까지 9억 4,951만 달러에 이를 것으로 예상되고 있어 2026년부터 2031년까지 CAGR 6.69%로 성장할 전망입니다.

인도의 국경간 전자상거래 물류 시장은 전자상거래 수출 허브인 ‘닥 가르 니리얏 켄드라(Dak Ghar Niryat Kendras)’와 택배 서비스의 원활화, 그리고 중소기업 및 영세기업(MSME)을 위한 마켓플레이스 직접 진출을 결합한 보다 광범위한 수출 촉진 정책에 힘입어, 주요 대도시권을 넘어 판매자 기반을 꾸준히 확대되고 있습니다. 본 보고서는 제품 카테고리(식품, 퍼스널케어, 패션, 가구, 전자기기, 기타), 물류 기능(운송, 부가가치 서비스(VAS) 등), 비즈니스 모델(B2C 등), 배송 속도(특급, 일반), 그리고 물류 흐름의 방향(아웃바운드(북미, 유럽 등), 인바운드(북미, 유럽 등))별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

인도 국경간 전자상거래 물류 시장 동향과 인사이트

전자상거래 수출 허브, DNK 및 수출 장려 지원

인도의 수출 촉진 체계는 물리적 접근 지점과 디지털 처리 지원을 결합하게 됨에 따라, 소규모 판매자들에게 더욱 실용적인 형태로 변모하고 있습니다. 정부는 전국에 1,013곳의 “닥 가르 니리얏 켄드라(Dak Ghar Niryat Kendras)”를 설치하여, 이를 통해 원격지나 2차 클러스터에 위치한 수출업체들에게 비공식적인 우회책이 아닌 공식적인 수출 접근 거점을 제공합니다. 해당 공식 프레임워크에는 물류 비용과 시간 절감, 규제 합리화, 재수입 절차 간소화를 목적으로 전자상거래 수출 허브가 건설되고 있다는 점도 명시되어 있습니다. 여기에는 통관, 포장, 품질 인증, 창고 보관에 관한 종합적인 지원이 포함됩니다. 실제로 소포 수출은 판매자 수요뿐만 아니라 재현 가능한 프로세스의 품질에 좌우되기 때문에 이는 인도의 국경간 전자상거래 물류 시장에 있어 중요한 의미를 지닙니다. 또한, 이는 그동안 제품 공급은 있었으나 실질적인 수출 경로가 부족했던 지역에서 인도의 국경간 전자상거래 물류 시장이 새로운 물동량을 유치할 수 있음을 의미합니다.

인도의 패션, 인테리어, 미용, 전통 공예품에 대한 전 세계 수요

인도가 이미 온라인 수출 분야에서 확고한 입지를 다진 품목에 대해서는 수요 환경이 계속해서 양호합니다. 아마존 세계 셀링은 2025년 10월, 인도 판매자들의 전자상거래 수출 누적액이 200억 달러를 돌파했다고 발표했습니다. 2024년의 주요 수출 시장으로는 미국, 영국, 독일, 캐나다, 아랍에미리트, 프랑스, 이탈리아, 스페인, 사우디아라비아 등이 꼽히고 있습니다. 이 발표에 따르면, 지난 10년 동안 가장 빠르게 성장한 품목군에는 헬스케어, 퍼스널케어, 미용이 포함되어 있으며, 수출 소포 흐름에서 전자기기를 제외한 품목군의 중요성이 높아지고 있습니다. 인도의 국경 간 전자상거래 물류 시장에서 이는 중요한 의미를 지닙니다. 왜냐하면 브랜드 파워가 강하고 인지도가 높은 카테고리는 저가 일반 상품 소포에 비해 비싼 운임이나 DDP(관세·통관비 포함) 조건으로의 처리, 반품 처리를 더 수월하게 감당할 수 있기 때문입니다. 이것이 바로 인도의 국경 간 전자상거래 물류 시장에서 주로 가격 경쟁에 의존하는 카테고리보다 패션, 인테리어, 미용 및 문화적 독창성을 지닌 제품들이 더 강력한 장기적 지지를 얻고 있는 이유 중 하나입니다.

통관, 서류 절차 및 결제 대조의 복잡성

통관 및 결제 절차는 소규모 수출업체들에게 여전히 일관되게 대응하기 어려운 상황입니다. 인도 중앙은행(RBI)의 PA-CB 프레임워크에 따라, 수출입 국경 간 온라인 결제 거래를 중개하는 사업자는 직접적인 규제 대상이 되며, 가맹점 등록, 거래 처리, 결제 계좌, 실사, 보고에 관한 명확한 규정이 마련되었습니다. 이는 장기적인 시스템 품질 향상을 위한 긍정적인 한 걸음이지만, 동시에 국경 간 전자상거래가 중개업체나 판매자에게 더 이상 규정 준수 부담이 적은 활동이 아니게 되었음을 뒷받침하고 있습니다. 인도의 국경 간 전자상거래 물류 시장에서는 수출업체가 여러 이해관계자간에 플랫폼 워크플로우, 결제 일정, 통관 신고, 배송 약속을 조율해야 하기 때문에 여전히 업무상의 마찰이 발생하고 있습니다. 소규모 판매업체에게 있어 진정한 과제는 단순히 수요에 접근하는 것만이 아닙니다. 지연이나 예외, 대조 불일치 없이 모든 서류 작성 및 결제 절차를 완료할 수 있는지가 과제입니다.

부문별 분석

2025년, 패션·라이프스타일 분야는 인도 국경간 전자상거래 물류 시장 점유율의 30.76%를 차지하며, 시장 내 최대 카테고리가 되었습니다. 이러한 위상은 액세서리, 의류, 신발에 대한 꾸준한 수요를 반영한 것으로, 인도는 이러한 분야에서 탄탄한 제조 역량과 확고한 수출 브랜드력을 모두 갖추고 있습니다. 또한, 이러한 제품들은 취급하기 편한 크기로 출하되며, 마켓플레이스 주도의 판매 모델에 적합하기 때문에 소포 중심의 무역과도 잘 어울립니다. 따라서 인도 국경간 전자상거래 물류 시장 전체의 취급량 형성에 있어 패션·라이프스타일 부문은 계속해서 중심적인 역할을 수행하고 있습니다.

헬스 & 뷰티/퍼스널케어 시장은 2026년부터 2031년까지 연평균 성장률(CAGR) 7.68%로 확대될 것으로 예상되며, 가장 빠르게 성장하는 제품 부문이 될 전망입니다. 아마존이 2025년 10월에 발표한 최신 정보에 따르면, 헬스·퍼스널케어 및 뷰티 부문은 지난 10년 동안 인도 판매자들에게 가장 빠르게 성장한 카테고리 중 하나였으며, 이는 인도의 국경간 전자상거래 물류 시장에서 이미 확인된 성장세를 뒷받침하고 있습니다. 미용 분야는 많은 저가 의류 상품 라인에 비해 평균 주문 금액이 일반적으로 높은 경향이 있어 구조적으로도 유리하며, 이로 인해 프리미엄 배송 및 DDP(관세·통관 포함) 처리의 수익성이 향상됩니다. 가전제품, 가정용 기기, 가구는 여전히 시장에 기여하는 비중이 작지만, 포장, 통관 평가, 파손 방지 대책 면에서 더 복잡한 요건을 수반합니다. 식품 및 음료 부문은 절대적인 규모 면에서는 여전히 작지만, 해외 거주 인도인들의 재구매 수요가 안정적인 소포 운송을 뒷받침하는 에스닉 식품 및 특산품 부문에서 물류 경로의 깊이를 더하고 있습니다. 수공예품은 '패션·라이프스타일' 분야는 여전히 중요한 성장 동력으로 자리 잡고 있으며, 이는 문화적으로 차별화된 제품이 수출 구성의 질에 있어 여전히 중요함을 보여줍니다.

2025년 인도 국경간 전자상거래 물류 시장 규모 중 운송 부문이 71.42%를 차지하고 있으며, 이는 장거리 운송이 여전히 전체 운영 과정에서 가장 큰 비중을 차지하고 있음을 보여줍니다. 국경 간 소포 거래는 특히 패션, 건강 관련 카테고리 및 프리미엄 소비재 주문의 경우 시간 지정 배송에 의존하고 있기 때문에 이 부문에서 항공 화물은 여전히 매우 중요한 역할을 하고 있습니다. 운송 부문의 경쟁력은 라스트 마일에서 인도가 이루어지기 전에 여러 국경과 서비스 구역을 넘어 화물을 운송해야 하는 오랜 기간 지속되어 온 수요를 반영하고 있습니다. 그 결과, 인도의 국경 간 전자상거래 물류 시장에서 운송 부문은 여전히 수익 창출의 기반이 되고 있습니다.

부가가치 서비스 및 기타 부문은 2026년부터 2031년까지 연평균 성장률(CAGR) 11.87%를 기록하며 성장할 것으로 예상되며, 가장 빠르게 성장하는 부문이 될 전망입니다. 이것은 “통관 서비스(Customs-as-a-Service)”,DDP 관리, 반품 지원, 라벨 재부착 및 목적지별 규정 준수 처리에 대한 수요 증가를 반영하고 있습니다. 쿠네 나겔(Kune Nagel)사가 인도 5개 도시에서 10만 m²의 용량을 증설한 것은 풀필먼트 인프라가 단순한 면적 확대에 그치지 않고 자동화를 통해 확장되고 있으며, 이러한 고부가가치 서비스 계층을 뒷받침하고 있음을 보여줍니다. 해상 운송 및 내륙 수로 운송은 체계화된 B2B 물류에서 그 중요성이 점점 더 커지고 있습니다. 특히, 마스쿠가 FI3에 이어 두 번째 직항 노선으로 FI2(극동 아시아-인도) 서비스를 시작한 이후로는 이러한 경향이 더욱 두드러지고 있습니다. 철도 운송 규모는 여전히 작지만, 마스크가 하이데라바드에서 나바 셰바까지 주 1회 운행하는 냉장 철도 노선은 특정 수출 부문을 대상으로 한 전문적인 복합 운송 옵션이 확대되고 있음을 보여줍니다. 따라서 인도의 국경 간 전자상거래 물류 업계는 단순한 기본 화물 운송보다 서비스의 다층화가 더욱 중요한 수익 구조로 전환되고 있습니다. 앞으로 인도의 국경간 전자상거래 물류 시장에서는 창고 관리, 규정 준수 대응, 반품 처리를 한데 묶은 패키지 서비스를 제공하는 사업자가 더 많은 부가가치를 창출해 나갈 것으로 전망됩니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the india cross-border e-commerce logistics market size is expected to increase from USD 641.73 million in 2025 to USD 686.80 million in 2026 and reach USD 949.51 million by 2031, growing at a CAGR of 6.69% over 2026-2031.

The India cross-border e-commerce logistics market is supported by a broader export enablement push that now combines e-commerce export hubs, Dak Ghar Niryat Kendras, courier facilitation, and direct marketplace onboarding for MSMEs, steadily broadening the seller base beyond the largest metros. This report is Segmented by Product Category (Foods, Personal Care, Fashion, Furniture, Electronics, Others), by Logistics Function (Transportation, VAS, and More), by Business Model (B2C, and More), by Delivery Speed (Express, Standard), and by Flow Direction (Outbound [North America, Europe, and More], Inbound [North America, Europe, and More]). The Market Forecasts are in Value (USD).

India Cross-Border E-Commerce Logistics Market Trends and Insights

E-Commerce Export Hubs, DNKs, and Export-Incentive Support

India's export enablement architecture is becoming more practical for small sellers because it now combines physical access points with digital processing support. The government had established 1,013 Dak Ghar Niryat Kendras across the country, which give exporters in remote and secondary clusters a formal export access node rather than an informal workaround. The same official framework also states that e-commerce export hubs are being built to reduce logistics costs and time, streamline regulation, and simplify re-imports, with integrated support around customs clearance, packaging, quality certification, and warehousing. In practice, this matters for the India cross-border e-commerce logistics market because parcel exports depend on repeatable process quality, not only on seller demand. It also means the India cross-border e-commerce logistics market can pull new volume from places that previously had product supply but lacked a viable export channel.

Global Demand for Indian Fashion, Decor, Beauty, and Heritage Products

Demand conditions remain favorable for categories where India already has a visible online export identity. Amazon Global Selling stated in October 2025 that Indian sellers had crossed USD 20 billion in cumulative e-commerce exports, with the United States, United Kingdom, Germany, Canada, UAE, France, Italy, Spain, and Saudi Arabia among key export markets in 2024. The same release showed that health and personal care and beauty were among the fastest-growing categories over the last 10 years, and non-electronics categories are becoming more important in export parcel flows. For the India cross-border e-commerce logistics market, that matters because categories with stronger brand pull and higher perceived value can absorb premium freight, DDP handling, and returns processing more easily than low-value commodity parcels. That is one reason the India cross-border e-commerce logistics market is seeing stronger long-run support from fashion, decor, beauty, and culturally differentiated products than from categories that compete mainly on price.

Customs, Documentation, and Payment Reconciliation Complexity

The customs and payment layer is still difficult for small exporters to handle consistently. RBI's PA-CB framework brought entities facilitating cross-border online payment transactions for import and export under direct regulation, with clear rules around merchant onboarding, transaction handling, settlement accounts, due diligence, and reporting. That is a positive step for long-term system quality, but it also confirms that cross-border commerce is no longer a light-compliance activity for intermediaries or sellers. The India cross-border e-commerce logistics market still faces operating friction when exporters must align platform workflows, payment timelines, customs declarations, and delivery commitments across several parties. For smaller sellers, the real challenge is not just access to demand. It is the ability to complete every documentation and settlement step without delays, exceptions, or reconciliation gaps.

Other drivers and restraints analyzed in the detailed report include:

- Marketplace and Aggregator-Led MSME Export Onboarding

- Faster Cross-Border Fulfillment Through Courier Digitization and Visibility Tools

- US De Minimis Withdrawal Disrupting Low-Ticket Parcel Economics

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fashion and lifestyle held 30.76% of the India cross-border e-commerce logistics market share in 2025, making it the largest category in the market. Its position reflects steady demand for accessories, apparel, and footwear, where India combines manufacturing depth with a recognizable export identity. These products also align well with parcel-led trade because they ship in manageable sizes and fit marketplace-led selling models. That keeps fashion and lifestyle central to volume formation across the India cross-border e-commerce logistics market.

Health and beauty / personal care is projected to expand at a 7.68% CAGR over 2026-2031, making it the fastest-growing product segment. Amazon's October 2025 update showed that health and personal care and beauty were among the fastest-growing categories for Indian sellers over the last decade, supporting the momentum already visible in the India cross-border e-commerce logistics market. Beauty is also structurally favorable because average order values tend to be stronger than in many low-ticket apparel lines, which improves the economics of premium shipping and DDP handling. Consumer electronics, household appliances, and furniture remain smaller contributors, but they create more complex packaging, customs valuation, and damage-control requirements. Foods and beverages is still smaller in absolute terms, yet it adds corridor depth in ethnic and specialty categories where repeat diaspora demand supports steady parcel traffic. Handicrafts remained an important growth lever inside Fashion and Lifestyle, which shows that culturally differentiated products continue to matter for export mix quality.

Transportation accounted for 71.42% of the India cross-border e-commerce logistics market size in 2025, which confirms that line-haul movement still absorbs most value in the operating stack. Air freight remains especially important in this segment because cross-border parcel trade depends on time-definite delivery, particularly for fashion, health-linked categories, and premium consumer orders. The dominance of transportation also reflects the long-standing need to move shipments across multiple borders and service zones before the last-mile handoff occurs. As a result, transport still anchors revenue generation in the India cross-border e-commerce logistics market.

The value-added services and others segment is forecast to grow at a 11.87% CAGR over 2026-2031, making it the fastest-growing segment. This reflects stronger demand for customs-as-a-service, DDP management, returns support, relabeling, and destination-specific compliance processing. Kuehne+Nagel's 100,000 m2 capacity addition across five Indian cities shows that fulfillment infrastructure is being expanded through automation rather than just square footage, which supports these higher service layers. Sea transport and inland waterway activity are becoming more relevant for organized B2B flows, especially after Maersk launched its FI2 Far East Asia to India service as a second direct lane alongside FI3. Rail remains smaller, but Maersk's weekly reefer rail link from Hyderabad to Nhava Sheva shows that specialized multimodal options are expanding for specific export sectors. The India cross-border e-commerce logistics industry is therefore shifting toward a margin structure where service layering matters more than basic freight movement alone. Over time, the India cross-border e-commerce logistics market should see more value captured by operators that convert warehousing, compliance, and returns processing into a bundled offering.

Complete Report Scope:

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (Accessories, Apparel, Footwear)

- Furniture

- Consumer Electronics and Household Appliances

- Other Products

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Delivery Speed

- Express

- Standard

- By Flow Direction

- Outbound (Exports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Inbound (Imports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Outbound (Exports)

List of Companies Covered in this Report:

- DHL Group

- FedEx

- United Parcel Service of America, Inc. (UPS)

- Aramex

- India Post

- Delhivery, Ltd.

- Shiprocket X

- Blue Dart Express Pvt. Ltd.

- DTDC Express Pvt. Ltd.

- XpressBees

- Allcargo Gati Logistics Pvt. Ltd.

- SEKO Logistics

- Kuehne+Nagel

- A.P. Moller - Maersk

- NimbusPost

- Ekart Logistics

- Amazon, Inc.

- ShipGlobal.in

- IThink Logistics

- Shadowfax

- Easyship

- Shipyaari

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Cross-border E-commerce Logistics in E-commerce Market

- 4.2 Trends in E-Commerce Industry

- 4.3 Consumer Behavior and Demand-Supply Analysis

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 E-Commerce Export Hubs, DNKs, and Export-Incentive Support

- 4.6.2 Global Demand for Indian Fashion, Decor, Beauty, and Heritage Products

- 4.6.3 Marketplace and Aggregator-Led MSME Export Onboarding

- 4.6.4 Faster Cross-Border Fulfillment Through Courier Digitization and Visibility Tools

- 4.6.5 Postal-Route Incentive Parity Improving Low-AOV Parcel Economics

- 4.6.6 RBI-Regulated Cross-Border Payment Rails and UPI-Linked Settlement Innovation

- 4.7 Market Restraints

- 4.7.1 Customs, Documentation, and Payment Reconciliation Complexity

- 4.7.2 High Landed Cost, DDP Burden, and Reverse-Logistics Losses

- 4.7.3 US De Minimis Withdrawal Disrupting Low-Ticket Parcel Economics

- 4.7.4 EU ICS2 And VAT Data-Compliance Tightening for SME Exporters

- 4.8 Technology Innovations Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Rivalry Among Competitors

- 4.10 Evolution of Cross-border E-commerce Logistics Requirements

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Product Category

- 5.1.1 Foods and Beverages

- 5.1.2 Personal and Household Care

- 5.1.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.1.4 Furniture

- 5.1.5 Consumer Electronics and Household Appliances

- 5.1.6 Other Products

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing, Distribution and Inventory Management

- 5.2.3 Value-added Services and Others

- 5.2.1 Transportation

- 5.3 By Business Model

- 5.3.1 B2C

- 5.3.2 B2B

- 5.3.3 C2C

- 5.4 By Delivery Speed

- 5.4.1 Express

- 5.4.2 Standard

- 5.5 By Flow Direction

- 5.5.1 Outbound (Exports)

- 5.5.1.1 North America

- 5.5.1.2 Europe

- 5.5.1.3 Asia-Pacific

- 5.5.1.4 Middle East and Africa

- 5.5.1.5 South America

- 5.5.2 Inbound (Imports)

- 5.5.2.1 North America

- 5.5.2.2 Europe

- 5.5.2.3 Asia-Pacific

- 5.5.2.4 Middle East and Africa

- 5.5.2.5 South America

- 5.5.1 Outbound (Exports)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 FedEx

- 6.4.3 United Parcel Service of America, Inc. (UPS)

- 6.4.4 Aramex

- 6.4.5 India Post

- 6.4.6 Delhivery, Ltd.

- 6.4.7 Shiprocket X

- 6.4.8 Blue Dart Express Pvt. Ltd.

- 6.4.9 DTDC Express Pvt. Ltd.

- 6.4.10 XpressBees

- 6.4.11 Allcargo Gati Logistics Pvt. Ltd.

- 6.4.12 SEKO Logistics

- 6.4.13 Kuehne+Nagel

- 6.4.14 A.P. Moller - Maersk

- 6.4.15 NimbusPost

- 6.4.16 Ekart Logistics

- 6.4.17 Amazon, Inc.

- 6.4.18 ShipGlobal.in

- 6.4.19 iThink Logistics

- 6.4.20 Shadowfax

- 6.4.21 Easyship

- 6.4.22 Shipyaari

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment