|

시장보고서

상품코드

2072918

베트남의 국경간 전자상거래 물류 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Vietnam Cross-Border E-Commerce Logistics - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

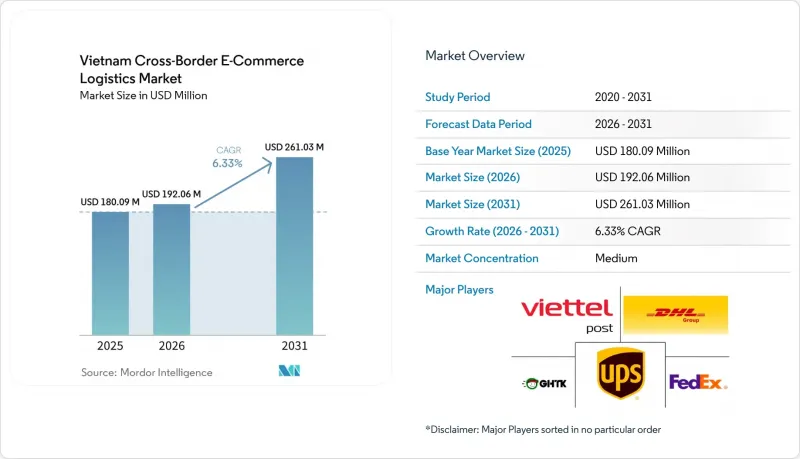

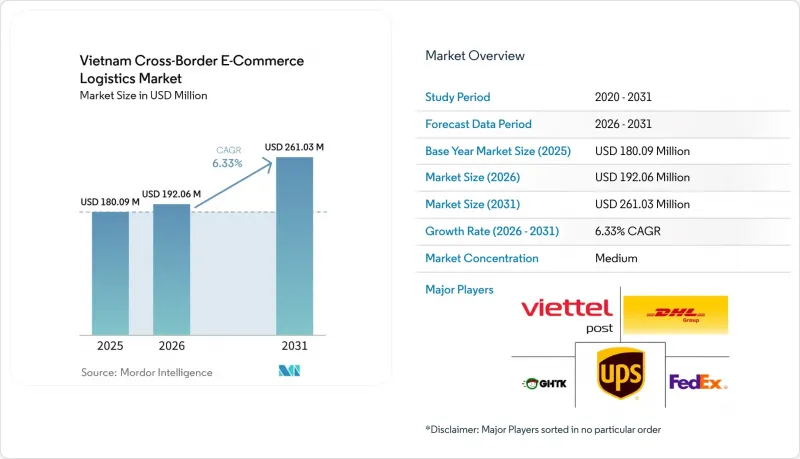

Mordor Intelligence에 의하면, 베트남 국경간 전자상거래 물류 시장 규모는 2025년에 1억 8,009만 달러로 평가되었고 2026년 1억 9,206만 달러에서 2031년까지 2억 6,103만 달러에 이를 것으로 예측되며, 예측 기간 CAGR은 6.33%입니다(2026-2031년).

베트남의 국경간 전자상거래 물류 시장은 2025년에 수출입 총액이 9,300억 달러를 돌파한 무역 환경 속에서 확대되고 있습니다. 한편, 온라인 국경간 무역액은 44억 5,000만 달러에 그치고 있는데, 이는 디지털 국경간 물류가 베트남의 광범위한 무역 기반에서 여전히 비교적 작은 비중을 차지하고 있음을 보여 주며, 따라서 향후 더욱 확대될 여지가 있음을 시사합니다. 본 보고서는 제품 카테고리(식품 및 음료, 퍼스널케어, 패션 등), 물류 기능(운송 등), 비즈니스 모델(B2C, B2B, C2C), 배송 속도(특급, 일반), 물류 흐름의 방향(수출(북미, 유럽 등), 수입(북미, 유럽 등))별로 분류되어 있습니다. 시장 전망치는 금액(달러)으로 표시되어 있습니다.

베트남의 국경간 전자상거래 물류 시장 동향 및 인사이트

정책에 기반을 둔 국경간 판매자 생태계의 공식화

베트남의 규제 환경은 2025년부터 2026년까지, 산발적으로 존재하던 규정에서 보다 통합된 체계로 전환되었습니다. “전자상거래법(제122/2025/QH15호)”는 2025년 12월에 채택되어 2026년 7월 1일에 시행되었습니다. 또한, 시행 계획에서는 각 부처 및 지방 자치 단체에 심사, 연수 및 관련 정령 제정에 관한 명확한 책임이 부여되어 있습니다. 또한, 법안 제정 과정에서 외국 플랫폼에 대해 과세, 분쟁 해결 및 소비자 보호 지원을 목적으로 베트남 국내에 법인을 설립하거나 법인을 지정하도록 의무화함으로써, 국경간 플랫폼의 설명 책임이 더욱 명확해졌습니다. 이번 변경은 베트남의 국경간 전자상거래 물류 시장에 중요한 의미를 지닙니다. 왜냐하면 정식 마켓플레이스와 관련된 소포의 흐름은 그레이 채널 네트워크를 경유하는 것보다, 추적 가능한 시스템을 갖춘 인가된 사업자를 통해 운송될 가능성이 더 높기 때문입니다. 이 정책 주기는 디지털 인프라, 물류 개선, 그리고 보다 투명한 국경간 무역 여건을 뒷받침하는 “2026년부터 2030년까지의 국가 전자상거래 개발 계획”과도 연동되어 있습니다. 그 결과, 베트남의 국경간 전자상거래 물류 시장에서는 플랫폼 규정 준수, 통관 서류, 주문 처리 데이터를 단일 운영 스택으로 통합할 수 있는 운송업체가 우위를 점할 가능성이 높습니다.

북아시아에서 시장 주도형 수입 소포의 확대

베트남으로의 소포 수요는 북아시아 공급과 베트남의 온라인 소비 간의 밀접한 연관성에 의해 계속해서 형성되고 있습니다. 업계 단체의 공식 자료에 따르면, 베트남의 온라인 국경간 무역 규모는 총 무역액에 비해 여전히 작은 것으로 나타났으며, 이는 플랫폼 주도의 수입이 소폭 증가하기만 해도 소비자 이용이 확대되면 소포 발송량이 급격히 늘어날 것임을 의미합니다. 저가 수입품에 대한 새로운 세제 조치 역시 이러한 소포의 유통 방식에 변화를 가져오고 있습니다. 이는 모든 수입 화물에 대해 부가가치세(VAT) 처리 의무가 발생함에 따라, 사업자들이 보다 체계적인 수입 절차를 도입할 수밖에 없게 되었기 때문입니다. 이에 따라 소포 수가 매우 많은 경우, 단편적인 특급 배송만 이용하는 것보다 보세 창고나 일괄 통관 모델이 더 매력적인 선택지가 되고 있습니다. 실제로, 대형 사업자가 서류 관리의 주도권을 잃지 않은 채 재고를 사전에 배치하고, 일괄 통관을 진행하며, 배송 기간을 단축할 수 있다면, 베트남의 국경간 전자상거래 물류 시장은 그 혜택을 누리게 될 것입니다.

높은 물류 및 역물류 비용 부담

비용은 판매업체와 물류업체에게 여전히 가장 명백한 운영상의 제약 요소 중 하나입니다. 제출된 초안에 포함된 VCCI 자료에 따르면, 관세, 부가가치세, 운송비를 포함할 경우, 국경간 상품의 입고 비용은 국내 재고보다 30%-50% 더 높은 경우가 많으며, 이로 인해 저가 상품 분야의 경쟁 여지가 직접적으로 좁아지고 있습니다. 베트남의 국경간 전자상거래 물류 시장은 특히 수출 경로 측면에서 취약합니다. 하노이와 호치민시 이외의 지역에서 '퍼스트 마일' 화물 집하 비용은 국제 운송이 시작되기 전부터 이미 비용 증가 요인으로 작용해 왔습니다. 역물류는 더욱 어렵습니다. 국제 반품의 경우, 여러 운송업체와 세관 검문소, 그리고 아직 표준화되지 않은 현지 검사 절차를 거치며 조정이 필요하기 때문입니다. 정부 관련 논의에서는 해결책의 일환으로 인근 해외 물류 허브나 보세창고가 이미 거론되고 있으며, 이는 비용 문제가 사소한 문제가 아니라 구조적인 과제임을 보여주고 있습니다. 해당 네트워크가 성숙기에 접어들기 전까지는 베트남의 국경간 전자상거래 물류 시장에서 소액 수출 소포의 비효율적인 상황이 지속될 뿐만 아니라, 규정 준수 및 취급 비용을 더 대규모의 발송 풀에 분산할 수 있는 사업자에 계속 의존하게 될 것입니다.

부문별 분석

2025년, 베트남의 국경간 전자상거래 물류 시장에서 가전제품 및 가정용 전기제품이 31.26%를 차지했으며, 이 부문은 소량 국경간 거래의 주요 수익원이 되었습니다. 이 지위는 비교적 높은 단가, 재구매 수요, 그리고 북아시아의 제조 생태계와의 견고한 조달 네트워크가 결합된 유리한 사업 프로파일을 반영하고 있습니다. 베트남의 국경간 전자상거래 물류 시장에서 전자제품은 통관 대행, 세심한 취급, 신속한 배송 옵션의 수익 창출에도 기여하고 있습니다. 이는 구매자가 기본적인 생활용품 카테고리에 비해 주문 처리 비용에 대한 가격 탄력성이 낮기 때문입니다. 이 카테고리는 수입 주도형 수요와 잘 부합합니다. 따라서, 소비자용 전자기기는 단순히 취급량을 늘리는 것뿐만 아니라, 국경을 넘는 리드타임이 중요한 경로에서 서비스 구성과 배송 경로의 밀도를 유지하는 역할도 수행하고 있습니다. 이러한 역할 덕분에 해당 부문은 도시 지역의 관문 및 보세 처리 거점에 걸친 네트워크 설계에 지대한 영향력을 행사하고 있습니다.

헬스케어, 미용, 퍼스널케어는 가장 빠르게 성장하고 있는 상품 카테고리이며, 2031년까지의 연평균 성장률(CAGR)은 7.32%로 예측됩니다. 이는 향후 성장이 대형 전자제품의 대량 구매에서 빈도가 더 높고 브랜드 주도의 소량 배송으로 전환되고 있음을 보여줍니다. 베트남의 국경간 전자상거래 물류 시장은 이러한 변화의 혜택을 누리고 있습니다. 미용 관련 소포는 밀도가 높고 포장이 간편하며, 부피가 큰 상품에 비해 반복적으로 해외 주문을 하는 데 적합한 경우가 많기 때문입니다. 따라서, 특히 수요가 하노이와 호치민시를 넘어 2차 도시권으로 확대됨에 따라, 이 부문은 특급 배송 서비스에 있어 중요해집니다. 또한, 패션 및 라이프스타일 분야도 전략적으로 중요한 위치를 계속 차지하고 있습니다. 베트남은 수입처일 뿐만 아니라, 국제 시장에 직접 진출하고자 하는 수출 지향적 판매업자들에게는 생산 거점 역할도 하고 있기 때문입니다. 반면, 가구는 건당 가치가 높은 반면, 베트남의 국경간 전자상거래 물류 업계에 있어 반품에 따른 경제적 부담, 파손 위험, 해외 창고 요건과 같은 과제를 안겨줍니다. 식품 및 음료 분야는 규정 준수, 제품 품질 유지, 경우에 따라서는 온도 관리가 필요하기 때문에 일반 소포 배송보다 진입 장벽이 높으며, 전문성이 더욱 요구되는 분야입니다.

2025년, 운송 부문은 베트남의 국경간 전자상거래 물류 시장 규모의 67.94%를 차지하고 있으며, 이는 국경을 넘는 물리적 이동이 여전히 시장의 핵심임을 뒷받침하고 있습니다. 이는 놀라운 일이 아닙니다. 왜냐하면, 아무리 수익성이 높은 서비스라도 판매되기 전에 모든 디지털 주문은 간선 운송, 항만 및 공항에서의 하역, 라스트 마일 배송에 의존하고 있기 때문입니다. 또한, 이 부문에는 지역별 생산 거점과 수출처 사이에 위치한 베트남의 입지 조건이 미치는 영향도 반영되어 있으며, 이로 인해 수입 및 수출 양쪽 경로에서 운송 수요가 구조적으로 높은 수준을 유지하고 있습니다. 따라서 베트남의 국경간 전자상거래 물류 시장에서 운송은 여전히 시기, 경로의 경제성, 그리고 서비스의 신뢰성을 결정짓는 핵심 기능으로 자리 잡고 있습니다. 표준 배송의 경우, 소포 처리량의 대부분이 여전히 속도보다는 비용을 중시하는 조건으로 운송되고 있다는 점에서 이 점을 뒷받침하고 있습니다. 요컨대, 주변 서비스의 고도화가 진행되고 있음에도 불구하고, 운송은 여전히 시장의 기반을 이루고 있습니다.

부가가치 서비스 등은 2031년까지 연평균 성장률(CAGR) 11.50%를 나타낼 것으로 예측되며, 베트남의 국경간 전자상거래 물류 시장에서 가장 빠르게 확대될 기능 분야가 될 전망입니다. 이는 화주나 플랫폼이 단순한 기본 운송뿐만 아니라 반품 처리, DDP 및 DDU 옵션, 통관 지원, 판매자를 위한 조정 등 통합적인 대응을 점점 더 요구하고 있음을 보여줍니다. 국가의 물류 로드맵에서는 전자상거래 물류센터, 디지털 도구, 통합 서비스 모델에 대한 투자 강화가 요구되고 있으므로, 공식적인 정책 방향도 이러한 발전을 뒷받침하고 있습니다. 통관 업무의 디지털화 또한, 여러 단계에 걸쳐 데이터를 효율적으로 제출·관리·대조할 수 있는 서비스 제공업체에 이점을 제공함으로써 이러한 추세를 뒷받침하고 있습니다. 이러한 운영 모델이 보급됨에 따라, 베트남의 국경간 전자상거래 물류 업계는 단순한 화물 운송만으로 정의되는 것이 아니라, 규제 및 운영상의 복잡성을 실용적인 서비스 수준으로 전환할 수 있는지 여부에 따라 정의되게 되었습니다. 이것이 바로 현재 운송이 여전히 주도적인 위치를 차지하고 있는 반면, 부가가치 서비스가 앞으로 이익에서 더 큰 비중을 차지하게 될 가능성이 높은 이유입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the vietnam cross-border e-commerce logistics market size was valued at USD 180.09 million in 2025 and is estimated to grow from USD 192.06 million in 2026 to reach USD 261.03 million by 2031, at a CAGR of 6.33% during the forecast period (2026-2031).

The Vietnam cross-border e-commerce logistics market is expanding within a trade system that moved past USD 930 billion in total import and export turnover in 2025, while online cross-border trade remained at USD 4.45 billion, which shows that digital cross-border logistics still serves a relatively small share of Vietnam's wider trade base and therefore has room to deepen over time. This report is Segmented by Product Category (Foods and Beverages, Personal Care, Fashion, and More), by Logistics Function (Transportation, and More), by Business Model (B2C, B2B, C2C), by Delivery Speed (Express, Standard), and by Flow Direction (Outbound [North America, Europe, and More], Inbound [North America, Europe, and More]). The Market Forecasts are Provided in Value (USD).

Vietnam Cross-Border E-Commerce Logistics Market Trends and Insights

Policy-Backed Formalization of Cross-Border Seller Ecosystems

Vietnam's regulatory setting moved from scattered rules toward a more integrated framework across 2025 and 2026. The Law on E-Commerce No. 122/2025/QH15 was adopted in December 2025 and took effect on July 1, 2026, while the implementation plan assigns ministries and local authorities clear responsibilities for review, training, and follow-on decrees. The draft law process also made cross-border platform accountability more explicit by requiring foreign platforms to establish or authorize a legal entity in Vietnam for taxation, dispute handling, and consumer protection support. That change matters for the Vietnam cross-border e-commerce logistics market because parcel flows connected to formal marketplaces are more likely to move through licensed operators with traceable systems than through gray-channel networks. The same policy cycle is linked to the national e-commerce development plan for 2026 to 2030, which supports digital infrastructure, logistics improvement, and more transparent cross-border trade conditions. As a result, the Vietnam cross-border e-commerce logistics market is likely to favor carriers that can connect platform compliance, customs documentation, and fulfillment data into one operating stack.

Marketplace-Led Import Parcel Expansion from North Asia

Inbound parcel demand continues to be shaped by the close link between North Asian supply and Vietnamese online consumption. Official association material shows that Vietnam's online cross-border trade base remains small relative to total trade, which means even modest gains in platform-led imports can lift parcel density quickly when consumer adoption broadens. The new tax treatment for low-value imports also changes how these parcels move, because every inbound shipment now carries VAT handling obligations that push operators toward more structured import processes. This makes bonded and bulk-clearance models more attractive than fragmented express-only handling for very high parcel counts. In practice, the Vietnam cross-border e-commerce logistics market benefits when large operators can pre-position stock, clear in bulk, and shorten delivery windows without losing control over documentation.

High Logistics and Reverse-Logistics Cost Burden

Cost remains one of the clearest operating limits for sellers and logistics providers. VCCI material in the supplied draft states that cross-border goods often face landed costs that are 30%-50% higher than those for locally held inventory, once duties, VAT, and transport are included, which directly reduces the room to compete on low-ticket items. The Vietnam cross-border e-commerce logistics market is particularly exposed on export routes, where first-mile collection outside Hanoi and Ho Chi Minh City still adds cost before international transit even begins. Reverse logistics is even harder because international returns require coordination across multiple carriers, customs touchpoints, and local inspection steps that are not yet standardized. Government-linked discussions have already identified nearby overseas logistics hubs and bonded storage as part of the answer, indicating that the cost issue is not a marginal problem but a structural one. Until that network matures, the Vietnam cross-border e-commerce logistics market will remain less efficient for low-value export parcels and more reliant on operators that can spread compliance and handling costs across larger shipment pools.

Other drivers and restraints analyzed in the detailed report include:

- Export Scaling for Furniture and Fashion MSMEs

- Rising Electronics and Beauty Parcel Density

- Customs, Tax, and Destination-Market Compliance Complexity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Consumer electronics and household appliances accounted for 31.26% of the Vietnam cross-border e-commerce logistics market in 2025, making the segment the main revenue driver for parcelized cross-border activity. This position reflects a favorable operating profile that combines relatively high unit values, repeat demand, and strong sourcing links with North Asian manufacturing ecosystems. In the Vietnam cross-border e-commerce logistics market, electronics also support better monetization for customs brokerage, careful handling, and faster delivery options, as buyers are less price-elastic in fulfillment than in basic commodity categories. The category fits well with import-driven demand. Consumer electronics, therefore, do more than add volume, because they help sustain service mix and route density in lanes where cross-border lead time matters. That role gives the segment an outsized influence on network design across urban gateways and bonded processing points.

Health, beauty, and personal care are the fastest-growing product categories, with a 7.32% CAGR through 2031, indicating that future growth is moving beyond large electronics baskets into more frequent, brand-led parcel flows. The Vietnam cross-border e-commerce logistics market benefits from this shift because beauty parcels are dense, easier to package, and often more compatible with repeat cross-border ordering than bulky goods are. That makes the category important for express services, especially when demand expands beyond Hanoi and Ho Chi Minh City into secondary urban centers. Fashion and lifestyle also remain strategically relevant, because Vietnam serves both as an import destination and as a production base for export-oriented sellers seeking direct international access. Furniture, by contrast, offers strong value per shipment but also exposes the Vietnam cross-border e-commerce logistics industry to more difficult return economics, damage risk, and overseas warehousing requirements. Foods and beverages add another specialized layer, because compliance, product integrity, and in some cases temperature control create higher entry barriers than those in standard parcel delivery.

Transport held 67.94% of the Vietnam cross-border e-commerce logistics market size in 2025, which confirms that physical movement across borders remains the core of the market. This is not surprising, because every digital order still depends on linehaul, port or airport handling, and last-mile execution before any higher-margin service can be sold. The segment also captures the effect of Vietnam's position between regional manufacturing centers and export destinations, which keeps transport demand structurally high across both import and export lanes. Within the Vietnam cross-border e-commerce logistics market, transport therefore remains the foundational function that determines timing, route economics, and service reliability. Standard delivery reinforces that point because a large portion of parcel volume still moves on cost-led rather than speed-led terms. In short, transport continues to anchor the market even as service sophistication around it rises.

Value-added services and others are projected to grow at an 11.50% CAGR through 2031, making it the fastest-moving functional area in the Vietnam cross-border e-commerce logistics market. This shows that shippers and platforms increasingly want integrated handling of returns, DDP and DDU choices, customs support, and seller-facing orchestration rather than basic movement alone. Official policy direction also supports that evolution, because the national logistics roadmap calls for stronger investment in e-commerce warehouses, digital tools, and integrated service models. Customs digitization strengthens the same trend by rewarding providers that can submit, manage, and reconcile data efficiently across multiple steps. As that operating model spreads, the Vietnam cross-border e-commerce logistics industry becomes less defined by freight movement alone and more by who can turn regulatory and operational complexity into a usable service layer. This is why transport still leads today, while value-added services are likely to capture more of the profit pool over time.

Complete Report Scope:

- By Product Category

- Foods and Beverages

- Personal and Household Care

- Fashion and Lifestyle (Accessories, Apparel, Footwear)

- Furniture

- Consumer Electronics and Household Appliances

- Other Products

- By Logistics Function

- Transportation

- Road

- Air

- Sea and Inland Waterways

- Rail

- Warehousing, Distribution and Inventory Management

- Value-added Services and Others

- Transportation

- By Business Model

- B2C

- B2B

- C2C

- By Delivery Speed

- Express

- Standard

- By Flow Direction

- Outbound (Exports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Inbound (Imports)

- North America

- Europe

- Asia-Pacific

- Middle East and Africa

- South America

- Outbound (Exports)

List of Companies Covered in this Report:

- DHL Group

- SF Express (KEX-SF)

- Cainiao Network

- J&T Express

- Shopee Xpress (SPX Express)

- Viettel Post

- Giao Hang Nhanh (GHN)

- Vietnam Post (VNPost)

- FedEx

- United Parcel Service of America, Inc. (UPS)

- Lazada Logistics (LEX)

- BEST Express Vietnam

- Giao Hang Tiet Kiem (GHTK)

- Boxme Global

- CJ Logistics

- Kuehne+Nagel

- CMA CGM Group (Including CEVA Logistics)

- Janio Asia

- Nhat Tin Logistics (NTX)

- JD Logistics

- A.P. Moller - Maersk

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview and Role of Cross-border E-commerce Logistics in E-commerce Market

- 4.2 Trends in E-Commerce Industry

- 4.3 Consumer Behavior and Demand-Supply Analysis

- 4.4 Regulatory Framework

- 4.5 Value Chain and Distribution Channel Analysis

- 4.6 Market Drivers

- 4.6.1 Policy-Backed Formalization of Cross-Border Seller Ecosystems

- 4.6.2 Marketplace-Led Import Parcel Expansion from North Asia

- 4.6.3 Export Scaling for Furniture and Fashion MSMEs

- 4.6.4 Rising Electronics and Beauty Parcel Density

- 4.6.5 Single-Window Customs Digitization and Bonded Inventory Enablement

- 4.6.6 Cross-Border Service-Layer Growth in Returns, Compliance, and DDP/DDU Support

- 4.7 Market Restraints

- 4.7.1 High Logistics and Reverse-Logistics Cost Burden

- 4.7.2 Customs, Tax, and Destination-Market Compliance Complexity

- 4.7.3 Removal of Low-Value Import VAT Exemption

- 4.7.4 Bulky-Product Return and Damage Economics

- 4.8 Technology Innovations Outlook

- 4.9 Porter's Five Forces Analysis

- 4.9.1 Threat of New Entrants

- 4.9.2 Bargaining Power of Suppliers

- 4.9.3 Bargaining Power of Buyers

- 4.9.4 Threat of Substitutes

- 4.9.5 Rivalry Among Competitors

- 4.10 Evolution of Cross-border E-commerce Logistics Requirements

- 4.11 Impact of Geo-Political Events on Supply Chain Shifts

5 Market Size and Growth Forecasts

- 5.1 By Product Category

- 5.1.1 Foods and Beverages

- 5.1.2 Personal and Household Care

- 5.1.3 Fashion and Lifestyle (Accessories, Apparel, Footwear)

- 5.1.4 Furniture

- 5.1.5 Consumer Electronics and Household Appliances

- 5.1.6 Other Products

- 5.2 By Logistics Function

- 5.2.1 Transportation

- 5.2.1.1 Road

- 5.2.1.2 Air

- 5.2.1.3 Sea and Inland Waterways

- 5.2.1.4 Rail

- 5.2.2 Warehousing, Distribution and Inventory Management

- 5.2.3 Value-added Services and Others

- 5.2.1 Transportation

- 5.3 By Business Model

- 5.3.1 B2C

- 5.3.2 B2B

- 5.3.3 C2C

- 5.4 By Delivery Speed

- 5.4.1 Express

- 5.4.2 Standard

- 5.5 By Flow Direction

- 5.5.1 Outbound (Exports)

- 5.5.1.1 North America

- 5.5.1.2 Europe

- 5.5.1.3 Asia-Pacific

- 5.5.1.4 Middle East and Africa

- 5.5.1.5 South America

- 5.5.2 Inbound (Imports)

- 5.5.2.1 North America

- 5.5.2.2 Europe

- 5.5.2.3 Asia-Pacific

- 5.5.2.4 Middle East and Africa

- 5.5.2.5 South America

- 5.5.1 Outbound (Exports)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 SF Express (KEX-SF)

- 6.4.3 Cainiao Network

- 6.4.4 J&T Express

- 6.4.5 Shopee Xpress (SPX Express)

- 6.4.6 Viettel Post

- 6.4.7 Giao Hang Nhanh (GHN)

- 6.4.8 Vietnam Post (VNPost)

- 6.4.9 FedEx

- 6.4.10 United Parcel Service of America, Inc. (UPS)

- 6.4.11 Lazada Logistics (LEX)

- 6.4.12 BEST Express Vietnam

- 6.4.13 Giao Hang Tiet Kiem (GHTK)

- 6.4.14 Boxme Global

- 6.4.15 CJ Logistics

- 6.4.16 Kuehne+Nagel

- 6.4.17 CMA CGM Group (Including CEVA Logistics)

- 6.4.18 Janio Asia

- 6.4.19 Nhat Tin Logistics (NTX)

- 6.4.20 JD Logistics

- 6.4.21 A.P. Moller - Maersk

7 Market Opportunities and Future Outlook

- 7.1 White-space and Unmet-Need Assessment