|

시장보고서

상품코드

2034994

중국의 반도체 디바이스 시장 : 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China Semiconductor Device - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

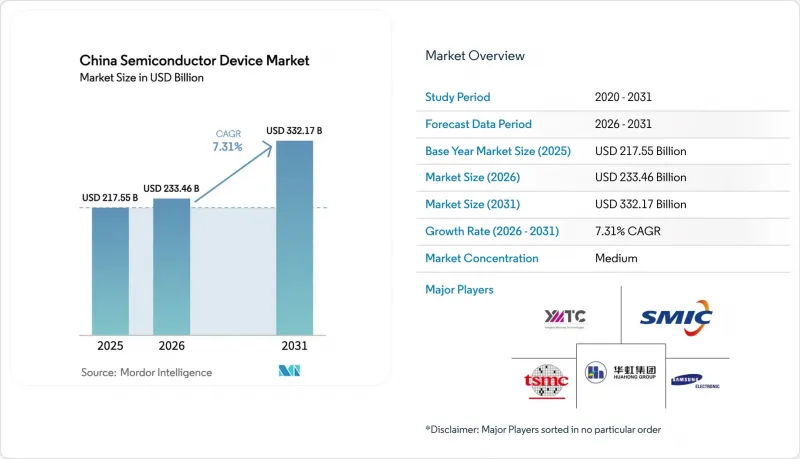

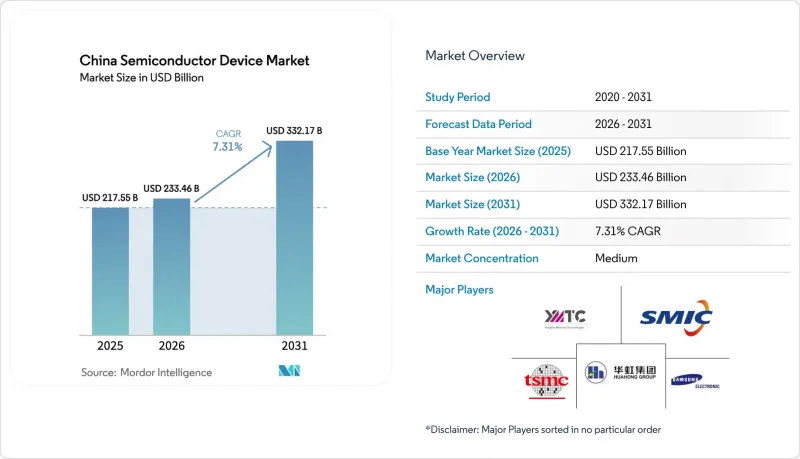

중국의 반도체 디바이스 시장 규모는 2025년에 2,175억 5,000만 달러로 평가되었고 2026년 2,334억 6,000만 달러에서 2031년까지 3,321억 7,000만 달러에 이를 것으로 예측되며, 예측 기간(2026-2031년) CAGR은 7.31%를 나타낼 전망입니다.

정부 주도의 자금 지원, 활발한 민간 투자, 그리고 기술 자립을 위한 정책 정책으로 인해 이 산업은 전략적 우선순위가 되었습니다. 국내 파운드리의 빠른 생산능력 증가, 3D NAND 및 첨단 패키징 기술의 혁신, 5G, AI, 신에너지 자동차 수요 증가가 이러한 확장을 뒷받침하고 있습니다. 극자외선(EUV) 장비에 대한 엄격한 수출 규제로 인해 10nm 이하 노드로의 전환이 둔화되고 있지만, 업체들은 성숙한 노드의 효율성 향상, 화합물 반도체 및 EUV를 피할 수 있는 새로운 아키텍처에 집중하고 있습니다. 경쟁 압력으로 인해 통합이 진행되고 있으며, EDA 분야의 Empyrean과 Xpeedic의 합병과 YMTC의 자금 조달 라운드가 그 예입니다. 이는 규모 확대, 수직계열화, 지적재산권(IP) 축적의 추세를 보여줍니다.

중국의 반도체 디바이스 시장 동향과 인사이트

'중국제조 2025'에 따른 IC 생산능력 확대 계획 가속화

중국은 2024년 파운드리 생산능력을 15% 확대할 것으로 예정됐으며, SMIC, 화홍(Huahong), Nexchip이 성숙 노드 라인을 증설함에 따라 2025년에는 14% 추가 증설이 예정되었습니다. 국산화 움직임은 현재 제조 공정을 넘어 포토레지스트 박리 및 습식 세정 장비까지 확대되고 있으며, 국내 업체들은 높은 채택률을 보이고 있습니다. 2027년까지 중국은 전 세계 28nm 생산능력의 31%를 차지할 것으로 예상되며, 이는 성숙 노드에서 가격 형성을 재편할 것으로 예측됩니다. 이 계획의 성패는 안정적인 전력 공급, 공정 엔지니어링 인력, 그리고 수출 규제 리스크를 줄일 수 있는 세컨드 소스 설비 라인에 달려 있습니다. 이를 종합해 볼 때, 이번 개발은 소비자, 산업 및 자동차용 일렉트로닉스에 대한 국내 공급을 확고히 하고, 전체 생태계의 가동률과 수익률을 높일 수 있을 것입니다.

중국 Tier 1 클라우드 제공업체들의 AI 중심 엣지 컴퓨팅 수요

알리바바는 2025년부터 2027년까지 AI 지원 클라우드 인프라에 3,800억 위안(529억 달러)을 투자할 것을 약속했고, 텐센트와 바이두도 비슷한 수준의 지출을 발표했습니다. GPU, 고대역폭 메모리, 네트워크 스위치용 ASIC에 대한 수요는 국내 팹 및 메모리 제조업체에 대한 주문으로 이어지고 있습니다. DeepSeek의 기반 모델은 소프트웨어와 하드웨어를 통합할 수 있는 중국의 능력을 보여주며, 해외 가속기에 대한 의존도를 낮추고 있습니다. 엣지 AI 워크로드는 저지연 On-Premise 연산을 선호하기 때문에 구매자는 국가 데이터 주권 규정을 준수하는 국내 설계 SoC로 향하고 있습니다. 따라서 하이퍼스케일러의 설비 투자와 칩 레벨의 혁신 사이의 선순환은 중기 성장의 주요 원동력이 될 것입니다.

EUV 및 EDA 툴에 대한 미국 수출 관리 기관 목록에 따른 규제 강화

2024년 10월과 12월에 발효된 미국 규제에 따라 EUV 스캐너, 첨단 증착 장비 및 하이엔드 EDA 라이선스가 중국 내 반도체 공장에 출하되는 것이 금지되었습니다. 국내 업체들은 양산에서 28nm 공정에 머물러 있어, ASML의 EUV 장비 없이 7nm 공정의 개념증명(PoC) 웨이퍼 개발을 진행해야 합니다. 해결 방안으로는 1nm 게이트 길이로 시험 운영되고 있는 2차원 재료 트랜지스터, 고급 DUV 멀티패터닝 등이 있지만, 상업적 수율을 달성하기 위해서는 아직 몇 년이 더 걸릴 것으로 예측됩니다. 장비 리드타임의 장기화, 소프트웨어 라이선스의 불확실성, 컴플라이언스 감사로 인해 노드 마이그레이션의 속도가 느려지고 있습니다.

부문 분석

2025년에는 집적회로가 매출의 86.02%를 차지할 것으로 예상됐으며, AI, 5G, 서버 수요로 인해 다이 사이즈 확대와 적층형 V-캐시 솔루션이 요구됨에 따라 그 비중은 더욱 소폭 상승할 것으로 전망됩니다. 중국의 반도체 시장에서 집적회로는 CAGR 8.02% 성장하여 2031년까지 692억 달러 이상의 신규 생산액을 창출할 것으로 예측됩니다. YMTC의 232단 3D NAND와 CXMT의 DDR5 수율 80%는 메모리 분야의 모멘텀을 뒷받침하고 있으며, SMIC의 12인치 라인은 견조한 민수 및 산업용 수요에 힘입어 89.6%의 가동률을 유지하고 있습니다.

이산형 파워 디바이스, 광전자, 센서가 나머지 13.98%의 점유율을 차지하고 있으며, NEV 전동화 및 5G용 광부품 수요 증가에 따른 수혜를 받고 있습니다. 국내 SiC 다이오드 생산능력은 18개월마다 2배씩 증가하고 있으며, 스마트폰용 3D 센싱용 VCSEL 출하가 국내 팹으로 전환되고 있습니다. 금액 기준으로는 규모가 작지만, 자동차 안전, 스마트팩토리 도입, AR/VR 하드웨어에서 중요한 차별화 요소로 작용하며 다분야에 걸친 회복력을 뒷받침하고 있습니다.

중국의 반도체 소자 시장은 소자 유형별(개별 반도체(다이오드, 트랜지스터 등), 광전자(LED, 레이저 다이오드 등), 센서 및 MEMS(압력, 액추에이터 등), 집적회로), 비즈니스 모델별(IDM, 설계/팹리스 벤더), 최종사용 산업별(자동차, 통신, 민수, 산업용, 컴퓨팅/데이터 스토리지, 데이터 스토리지, AI, 정부) 등으로 세분화하여 조사하였습니다. 팹리스 벤더), 최종 이용 산업(자동차, 통신, 소비재, 산업용, 컴퓨팅/데이터 스토리지, 데이터센터, AI, 정부)으로 구분됩니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The China semiconductor device market size was valued at USD 217.55 billion in 2025 and estimated to grow from USD 233.46 billion in 2026 to reach USD 332.17 billion by 2031, at a CAGR of 7.31% during the forecast period (2026-2031).

State-directed funding, vigorous private investment, and a policy mandate for technological self-sufficiency have turned the industry into a strategic priority. Rapid capacity additions at domestic foundries, breakthroughs in 3D NAND and advanced packaging, and rising demand from 5G, AI, and new-energy vehicles underpin the expansion. Tight export controls on extreme-ultraviolet (EUV) tools have slowed the migration to sub-10 nm nodes; yet, firms have redirected their efforts toward improving mature-node efficiency, compound semiconductors, and novel architectures that bypass EUV. Competitive pressure has led to increased consolidation, as exemplified by Empyrean-Xpeedic in EDA and YMTC's funding round, illustrating a trend toward scale, vertical integration, and IP accumulation.

China Semiconductor Device Market Trends and Insights

Accelerated "Made-in-China 2025" IC Capacity Expansion Programs

China expanded foundry capacity by 15% in 2024 and is scheduled to add another 14% in 2025 as SMIC, Huahong, and Nexchip ramp mature-node lines. Localization now stretches beyond fabrication to photoresist stripping and wet-clean tools, where domestic suppliers have achieved high usage rates. By 2027, China is projected to hold 31% of global 28 nm capacity, reshaping pricing at mature nodes. The program's success hinges on stable power, process-engineering talent, and second-source equipment lines that mitigate export-control exposure. Taken together, the rollout cements domestic supply for consumer, industrial, and automotive electronics, lifting utilization rates and margins across the ecosystem.

AI-Centric Edge-Computing Demand from Tier-1 Chinese Cloud Providers

Alibaba pledged CNY 380 billion (USD 52.9 billion) over 2025-2027 for AI-ready cloud infrastructure, while Tencent and Baidu announced comparable outlays. Demand spans GPUs, high-bandwidth memory, and network switch ASICs, channeling orders to local fabs and memory houses. DeepSeek's foundation model showcases China's ability to align software and hardware, easing reliance on foreign accelerators. Edge-AI workloads favor low-latency, on-premise compute, steering buyers toward domestically designed SOCs that comply with national data-sovereignty rules. The virtuous loop between hyperscaler capex and chip-level innovation is therefore a prime mid-term growth catalyst.

US Export-Control Entity-List Restrictions on EUV and EDA Tools

Washington's October 2024 and December 2024 rules bar shipment of EUV scanners, advanced deposition gear, and high-end EDA licenses to Chinese fabs. Domestic producers remain confined to 28 nm for mass production and must innovate around 7 nm proof-of-concept wafers without ASML EUV. Work-arounds include 2D-material transistors piloted at 1 nm gate length and advanced DUV multiple-patterning, but commercial yields are years away. Longer equipment lead-times, software license uncertainty, and compliance audits dampen the pace of node migration.

Other drivers and restraints analyzed in the detailed report include:

- Automotive-Grade SiC/GaN Adoption in NEV Powertrains

- National 5G Base-Station Build-Out Driving RF Front-End IC Uptake

- Talent Drain to Overseas Design Houses

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Integrated circuits accounted for 86.02% revenue in 2025, and their share is forecast to edge higher as AI, 5G, and server demand require larger die sizes and stacked V-cache solutions. Within the Chinese semiconductor market, integrated circuits are expected to expand at an 8.02% CAGR, adding more than USD 69.2 billion in new output by 2031. YMTC's 232-layer 3D NAND and CXMT's 80% DDR5 yield underscore momentum in memory, while SMIC's 12-inch lines run at 89.6% utilization on robust consumer and industrial demand.

Discrete power devices, optoelectronics, and sensors together occupy the remaining 13.98% share but are benefiting from NEV electrification and 5G optical-component pull. Domestic SiC diode capacity is doubling every 18 months, and VCSEL shipments for 3D sensing in smartphones are moving to local fabs. Although smaller in value, these categories contribute critical differentiation in automotive safety, smart-factory deployments, and AR/VR hardware, sustaining multi-segment resilience.

China Semiconductor Device Market is Segmented by Device Type (Discrete Semiconductors [Diodes, Transistors, and More], Optoelectronics [LEDs, Laser Diodes, and More], Sensors and MEMS [Pressure, Actuators, and More], and Integrated Circuits), Business Model (IDM, and Design/ Fabless Vendor), and End-Use Industry (Automotive, Communication, Consumer, Industrial, Computing/Data Storage, Data Center, AI, and Government).

List of Companies Covered in this Report:

- Semiconductor Manufacturing International Corp (SMIC)

- Taiwan Semiconductor Manufacturing Co (TSMC)

- Hua Hong Group

- Intel Corp

- Samsung Electronics Co Ltd

- SK Hynix Inc

- Micron Technology Inc

- Yangtze Memory Technologies Co (YMTC)

- JCET Group Co Ltd

- Advanced Micro Devices Inc

- Qualcomm Inc

- Broadcom Inc

- Nvidia Corp

- NXP Semiconductors NV

- Infineon Technologies AG

- STMicroelectronics NV

- Texas Instruments Inc

- Will Semiconductor Co Ltd

- Goodix Technology

- ASE Technology Holding Co

- Renesas Electronics Corp

- Rohm Co Ltd

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Accelerated "Made-in-China 2025" IC Capacity Expansion Programs

- 4.2.2 AI-centric Edge-Computing Demand from Tier-1 Chinese Cloud Providers

- 4.2.3 Automotive-grade SiC/GaN Adoption in NEV Powertrains

- 4.2.4 National 5G Base-station Build-out Driving RF-Front-End IC Uptake

- 4.2.5 Industrial Upgrade to "Industry 4.0" Smart-Factories

- 4.2.6 Post-pandemic rebound of AIoT-enabled consumer devices (smart wearables, AR/VR)

- 4.3 Market Restraints

- 4.3.1 US Export-control Entity-List Restrictions on EUV and EDA Tools

- 4.3.2 Talent Drain to Overseas Design Houses

- 4.3.3 Electricity-Intensive Fabs Facing Provincial Carbon-Quota Caps

- 4.3.4 Persistent Price Volatility of 300 mm Prime Wafers

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Outlook

- 4.6 Technological Trends

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Intensity of Rivalry

- 4.8 Impact Assessment of Macroeconomic Factors

- 4.9 Semiconductor Foundry Landscape

- 4.9.1 Foundry Revenue and Share by Players

- 4.9.2 IDM vs Fabless Sales

- 4.9.3 Installed Wafer Capacity (by Fab Location)

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Device Type (Shipment Volume for Device Type is Complementary)

- 5.1.1 Discrete Semiconductors

- 5.1.1.1 Diodes

- 5.1.1.2 Transistors

- 5.1.1.3 Power Transistors

- 5.1.1.4 Rectifier and Thyristor

- 5.1.1.5 Other Discrete Devices

- 5.1.2 Optoelectronics

- 5.1.2.1 Light-Emitting Diodes (LEDs)

- 5.1.2.2 Laser Diodes

- 5.1.2.3 Image Sensors

- 5.1.2.4 Optocouplers

- 5.1.2.5 Other Device Types

- 5.1.3 Sensors and MEMS

- 5.1.3.1 Pressure

- 5.1.3.2 Magnetic Field

- 5.1.3.3 Actuators

- 5.1.3.4 Acceleration and Yaw Rate

- 5.1.3.5 Temperature and Others

- 5.1.4 Integrated Circuits

- 5.1.4.1 By Integrated Circuit Type

- 5.1.4.1.1 Analog

- 5.1.4.1.2 Micro

- 5.1.4.1.2.1 Microprocessors (MPU)

- 5.1.4.1.2.2 Microcontrollers (MCU)

- 5.1.4.1.2.3 Digital Signal Processors

- 5.1.4.1.3 Logic

- 5.1.4.1.4 Memory

- 5.1.4.2 By Technology Node (Shipment Volume Not Applicable)

- 5.1.4.2.1 < 3nm

- 5.1.4.2.2 3nm

- 5.1.4.2.3 5nm

- 5.1.4.2.4 7nm

- 5.1.4.2.5 16nm

- 5.1.4.2.6 28nm

- 5.1.4.2.7 > 28nm

- 5.1.4.1 By Integrated Circuit Type

- 5.1.1 Discrete Semiconductors

- 5.2 By Business Model

- 5.2.1 IDM

- 5.2.2 Design/ Fabless Vendor

- 5.3 By End-user Industry

- 5.3.1 Automotive

- 5.3.2 Communication (Wired and Wireless)

- 5.3.3 Consumer

- 5.3.4 Industrial

- 5.3.5 Computing/Data Storage

- 5.3.6 Data Center

- 5.3.7 AI

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products and Services, and Recent Developments)

- 6.4.1 Semiconductor Manufacturing International Corp (SMIC)

- 6.4.2 Taiwan Semiconductor Manufacturing Co (TSMC)

- 6.4.3 Hua Hong Group

- 6.4.4 Intel Corp

- 6.4.5 Samsung Electronics Co Ltd

- 6.4.6 SK Hynix Inc

- 6.4.7 Micron Technology Inc

- 6.4.8 Yangtze Memory Technologies Co (YMTC)

- 6.4.9 JCET Group Co Ltd

- 6.4.10 Advanced Micro Devices Inc

- 6.4.11 Qualcomm Inc

- 6.4.12 Broadcom Inc

- 6.4.13 Nvidia Corp

- 6.4.14 NXP Semiconductors NV

- 6.4.15 Infineon Technologies AG

- 6.4.16 STMicroelectronics NV

- 6.4.17 Texas Instruments Inc

- 6.4.18 Will Semiconductor Co Ltd

- 6.4.19 Goodix Technology

- 6.4.20 ASE Technology Holding Co

- 6.4.21 Renesas Electronics Corp

- 6.4.22 Rohm Co Ltd

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-space and Unmet-Need Assessment