|

시장보고서

상품코드

2035091

인도네시아의 택배, 특송 및 소포(CEP) 시장 : 점유율 분석, 산업 동향 및 통계 데이터, 성장 예측(2026-2031년)Indonesia Courier, Express, And Parcel (CEP) - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

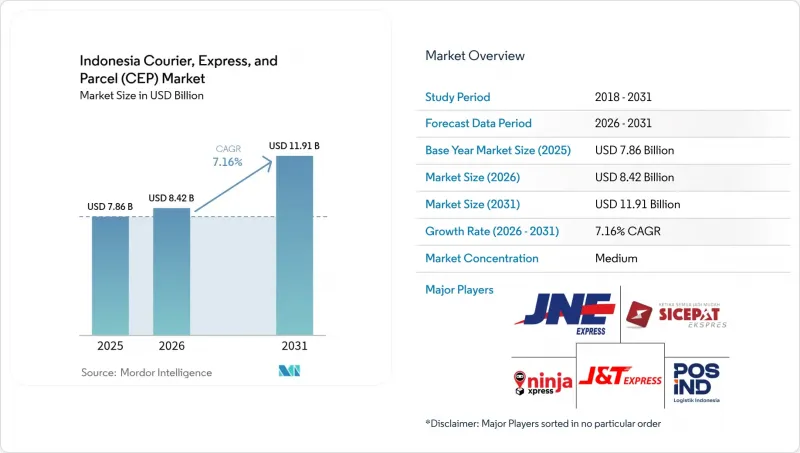

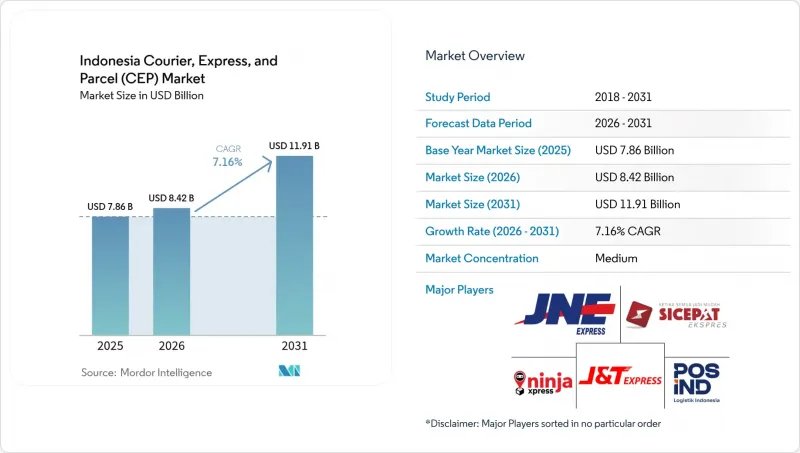

2026년 인도네시아의 택배, 특송 및 소포(CEP) 시장 규모는 84억 2,000만 달러로 추정되며, 2025년 78억 6,000만 달러에서 성장하여 2031년에는 119억 1,000만 달러에 이를 것으로 예측됩니다.

2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.16%를 나타낼 것으로 예측됩니다.

온라인 쇼핑의 급증, 전국적인 광섬유망 구축 및 유료 도로의 확장으로 인해 택배 처리량이 꾸준히 증가하고 있습니다. 스마트폰의 사용 확대와 디지털 결제의 보급으로 거래는 지속적으로 온라인으로 전환되고 있으며, 자동 분류, 스마트 창고, 경로 최적화 도구에 대한 설비투자를 촉진하고 있습니다. 사업자들은 의료 및 퀵커머스 고객에 대응하기 위해 콜드체인과 마이크로 풀필먼트에 대한 다각화를 추진하고 있으며, 한편으로는 도로와 항공로의 정비로 섬 간 운송 시간이 단축되고 있습니다. 물류비 절감을 위한 규제 조치로 인해 운송 사업자들은 차량 전동화 및 허브 자동화를 추진하고 있으며, 이로 인해 대기업과 중견기업 간의 효율성 격차가 확대되고 있습니다.

인도네시아의 택배, 특송 및 소포(CEP) 시장 동향 및 인사이트

폭발적인 이커머스 GMV의 성장과 디지털 결제의 부상

인도네시아의 디지털 경제는 현금 없는 결제를 통한 주문 완료율의 향상과 함께 인도네시아의 택배, 특송 및 소포 시장에 전례 없는 규모 수요를 가져왔습니다. 모바일 커머스가 온라인 매출의 3분의 2 이상을 차지하고 있으며, 자바-수마트라 간 주요 노선에서 소포 운송량이 더욱 증가하고 있습니다. Tokopedia와 TikTok과 같은 소셜 커머스 제휴는 젊은 층의 주문 빈도를 가속화하고 있습니다. 핀테크 대출은 소규모 판매자의 운전자금에 대한 접근성을 높이고, 지방 도시의 화주 기반을 확대하는 데 기여하고 있습니다. 배송 실패율 감소는 단가 절감과 운전자 생산성 향상으로 이어져 치열한 경쟁 속에서도 안정적인 수익률을 유지하고 있습니다.

자동 분류 허브와 스마트 창고의 급속한 전개

운송사들은 두 자릿수 취급량 증가에 대응하기 위해 크로스벨트 분류기, 비전 스캐너, AI 기반 창고 관리 시스템을 도입하고 있습니다. 자카르타의 플래그십 허브는 현재 시간당 7,200개의 소포를 처리하고 있으며, 이는 수작업으로 처리할 수 있는 용량의 4배에 달할 전망입니다. 자동화를 통해 분류 오류를 줄이고 재처리 작업을 줄이며, 동적 경로 설정 엔진에 활용되는 실시간 데이터를 생성합니다. 각 사업자는 수라바야, 메단, 마카사르에도 유사한 모듈식 시스템을 도입하여 주문 처리 주기를 단축하는 고속 노드 전국 네트워크를 구축하고 있습니다. 선발주자들은 서비스 신뢰도를 높이고, 인도네시아의 택배, 특송 및 소포 시장에서의 고객 정착률을 높이고 있습니다.

치열한 가격 경쟁으로 수익률 압박

플랫폼 통합 사업자들의 적극적인 할인으로 중견 사업자들의 순이익률은 지속 가능한 수준 이하로 떨어지고 있습니다. 배송비 보조금은 취급량을 증가시키지만 수익성을 떨어뜨리고 인도네시아의 택배, 특송 및 소포 시장 전체에 장기적인 현금 소진을 초래하고 있습니다. 운송 사업자들이 가격에 민감한 소비자들에게 세금 인상분을 전가하는 데 어려움을 겪고 있는 가운데, 부가가치세(VAT) 인상이 그 압박을 더욱 가중시키고 있습니다. 예상되는 업계 구조조정은 당장의 긴박감을 완화시킬 수 있지만, 반독점법상의 우려를 야기하고 업계 전체가 협동적 가격 변동에 취약해질 수 있습니다.

부문 분석

2025년에도 이커머스는 35.10%로 가장 큰 점유율을 유지했지만, 무료배송 캠페인의 지속으로 인해 수익률의 여지가 줄어들고 있습니다. 대량 풀필먼트에 대한 수요는 메가 분류 센터와 스마트 로커에 대한 지속적인 투자를 정당화합니다.

의료 분야는 의약품의 콜드체인 규제와 만성질환 복약순응도 프로그램에 힘입어 2026년부터 2031년까지 연평균 복합 성장률(CAGR) 7.46%로 확대될 것으로 예측됩니다. GDP 인증 보관시설과 온도관리 차량을 보유한 사업자는 프리미엄 요금을 적용함으로써 수익률을 압박하는 소매 화주에 대한 의존도를 낮추고 있습니다.

2025년 매출의 63.10%를 국내 화물이 차지하며, 인도네시아의 택배, 특송 및 소포 시장이 자와섬과 수마트라섬 수요 클러스터를 중심으로 한 국내 중심 시장임을 다시 한 번 확인시켜주고 있습니다. 2,816km에 이르는 유료 도로망 등 인프라 구축으로 섬 내 운송 리드 타임이 단축되어 익일 배송 서비스를 지원하고 있습니다. 이 부문은 집하 거점 밀집도가 높아져 경쟁력 있는 운임과 촘촘한 노선 구조를 실현하고 있습니다.

소셜커머스 수출업체들이 역내 바이어들에게 접근하고 자유무역협정으로 관세 장벽이 낮아지면서 국제 운송량은 2026년부터 2031년까지 연평균 7.35%의 성장률을 보일 것으로 예측됩니다. 규제 측면의 역풍, 특히 100달러의 면세 한도 등의 과제는 여전히 남아 있지만, 기술을 활용한 통관 절차 및 보세 전자허브가 컴플라이언스 마찰을 일부 상쇄하고 있습니다. 운송업체는 아세안 시장 진출을 목표로 하는 패션-뷰티 관련 사업자를 확보하기 위해 국경 간 추적 서비스와 현지 대응 반품 서비스를 세트로 제공합니다.

기타 특전:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 분석 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.05.20The Indonesia courier, express, and parcel market size in 2026 is estimated at USD 8.42 billion, growing from 2025 value of USD 7.86 billion with 2031 projections showing USD 11.91 billion, growing at 7.16% CAGR over 2026-2031.

A surge in online shopping, nationwide fiber-optic coverage, and toll-road expansion underpin healthy parcel volume growth. Growing smartphone usage and digital payments continue to shift transactions online, stimulating capacity investments in automated sortation, smart warehouses, and route-optimization tools. Operators increasingly diversify into cold-chain and micro-fulfillment to serve healthcare and quick-commerce clients, while road and air links reduce inter-island transit times. Regulatory initiatives targeting logistics-cost reduction push carriers toward fleet electrification and hub automation that widen efficiency gaps between scale leaders and mid-tier rivals.

Indonesia Courier, Express, And Parcel (CEP) Market Trends and Insights

Explosive E-commerce GMV Growth and Rising Digital Payments

Indonesia's digital economy channels unprecedented volumes into the Indonesia courier, express, and parcel market as cashless checkouts lift order completion rates. Mobile commerce accounts for well over two-thirds of online sales, reinforcing parcel density on core Java-Sumatra corridors. Social-commerce tie-ups such as Tokopedia-TikTok accelerate order frequency among younger demographics. Fintech lending broadens working-capital access for micro-sellers, expanding the shipper base across secondary cities. Reduced failed-delivery rates translate into lower unit costs and higher driver productivity, supporting margin stability despite intense price competition.

Rapid Rollout of Automated Sorting Hubs and Smart Warehouses

Carriers deploy cross-belt sorters, vision scanners, and AI-driven warehouse-management systems to cope with double-digit volume growth. A flagship Jakarta hub now processes 7,200 parcels per hour, quadrupling manual throughput. Automation cuts missorts, curtails re-handling labor, and generates real-time data that feeds dynamic-routing engines. Operators replicate modular systems in Surabaya, Medan, and Makassar, creating a nationwide grid of high-velocity nodes that shorten fulfillment cycles. Early movers bolster service reliability, strengthening customer stickiness in the Indonesia courier, express, and parcel market.

Intensifying Price War Compressing Margins

Aggressive discounting by platform integrators narrows net yields below sustainable thresholds for mid-tier operators. Subsidized delivery fees attract volume but erode profitability, driving prolonged cash burn across the Indonesia courier, express, and parcel market. VAT hikes compound pressure as carriers struggle to pass on higher tax outlays to price-sensitive consumers. Anticipated consolidation may relieve the immediate squeeze yet raises antitrust concerns and heightens the sector's exposure to coordinated pricing shifts.

Other drivers and restraints analyzed in the detailed report include:

- Government "Palapa Ring" and Toll-Road Projects Improving Inter-Island Connectivity

- 15-Minute Hyperlocal Delivery Models Piloted by Q-commerce Players

- Foreign-Equity Cap (49%) on Courier Licences Deterring FDI

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

E-commerce retained the biggest 35.10% slice in 2025, yet margin headroom narrows as free-shipping campaigns continue. Mass fulfillment requirements justify ongoing investment in mega-sort centers and smart lockers.

Healthcare will accelerate at a 7.46% CAGR between 2026-2031, bolstered by pharmaceutical cold-chain mandates and chronic-disease medication adherence programs. Operators with GDP-certified depots and temperature-controlled fleets leverage premium rates that dilute the sector's exposure to margin-squeezing retail shippers.

Domestic consignments generated 63.10% of 2025 revenue, reaffirming the Indonesia courier, express, and parcel market as a home-focused arena anchored by Java and Sumatra demand clusters. Infrastructure upgrades, such as the 2,816 km toll-road network, cut intra-island lead times and support next-day ground services. The segment benefits from scaled pickup density, enabling competitive tariffs and dense route structures.

International traffic will log a 7.35% CAGR between 2026-2031 as social-commerce exporters tap regional buyers and free-trade agreements reduce tariff friction. Regulatory headwinds remain, notably the USD 100 de-minimis limit, yet tech-enabled customs clearance and bonded e-hubs partly offset compliance friction. Carriers bundle cross-border tracking with localized returns to capture fashion and beauty merchants eyeing ASEAN penetration.

The Indonesia Courier, Express, and Parcel (CEP) Market Report is Segmented by Destination (Domestic and International), Speed of Delivery (Express and Non-Express), Model (Business-To-Business (B2B), and More), Shipment Weight (Heavy Weight, Light Weight, and Medium Weight), Mode of Transport (Air, Road, and Others), and End User Industry (E-Commerce, and More). The Market Forecasts are Provided in Terms of Value (USD).

List of Companies Covered in this Report:

- DHL Group

- FedEx

- Grab Holdings Limited

- J&T Express

- Lion Parcel (a part of Lion Group)

- Ninja Van (including Ninja Express)

- PT Citra Van Titipan Kilat (TIKI)

- PT Garuda Indonesia (Persero) TBK

- PT Globalindo Dua Satu Express (21 Express)

- PT ID Express Logistik Indonesia

- PT Jalur Nugraha Ekakurir (JNE Express)

- PT Kereta Api Indonesia (including KAI Logistik)

- PT Pandu Siwi Group (Pandu Logistics)

- PT Pos Indonesia (Persero)

- PT Repex Wahana (RPX)

- PT Satria Antaran Prima TBK (SAPX Express)

- PT SiCepat Express Indonesia

- PT Synergy First Logistics

- PT Yapindo Transportama (PCP Express)

- United Parcel Service (UPS)

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Demographics

- 4.3 GDP Distribution by Economic Activity

- 4.4 GDP Growth by Economic Activity

- 4.5 Inflation

- 4.6 Economic Performance and Profile

- 4.6.1 Trends in E-Commerce Industry

- 4.6.2 Trends in Manufacturing Industry

- 4.7 Transport and Storage Sector GDP

- 4.8 Export Trends

- 4.9 Import Trends

- 4.10 Fuel Price

- 4.11 Logistics Performance

- 4.12 Infrastructure

- 4.13 Regulatory Framework

- 4.14 Value Chain and Distribution Channel Analysis

- 4.15 Market Drivers

- 4.15.1 Explosive E-commerce GMV Growth and Rising Digital Payments

- 4.15.2 Rapid Rollout of Automated Sorting Hubs and Smart Warehouses

- 4.15.3 Government "Palapa Ring" and Toll-Road Projects Improving Inter-Island Connectivity

- 4.15.4 15-minute Hyperlocal Delivery Models Piloted by Q-commerce Players

- 4.15.5 Data-Driven Route-Optimization Cutting Last-Mile Costs for MSMEs

- 4.15.6 Micro-Fulfilment Franchising Unlocking Tier-2/3 City Penetration

- 4.16 Market Restraints

- 4.16.1 Intensifying Price War Compressing Margins

- 4.16.2 Foreign-Equity Cap (49 %) on Courier Licences Deterring FDI

- 4.16.3 Shortage of Insured Couriers Raising Social-License Risk

- 4.16.4 Minimum-Value Import Rule (USD 100) Throttling Cross-Border Parcels

- 4.17 Technology Innovations in the Market

- 4.18 Porter's Five Forces Analysis

- 4.18.1 Threat of New Entrants

- 4.18.2 Bargaining Power of Buyers

- 4.18.3 Bargaining Power of Suppliers

- 4.18.4 Threat of Substitutes

- 4.18.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 Destination

- 5.1.1 Domestic

- 5.1.2 International

- 5.2 Speed of Delivery

- 5.2.1 Express

- 5.2.2 Non-Express

- 5.3 Model

- 5.3.1 Business-to-Business (B2B)

- 5.3.2 Business-to-Consumer (B2C)

- 5.3.3 Consumer-to-Consumer (C2C)

- 5.4 Shipment Weight

- 5.4.1 Heavy Weight Shipments

- 5.4.2 Light Weight Shipments

- 5.4.3 Medium Weight Shipments

- 5.5 Mode of Transport

- 5.5.1 Air

- 5.5.2 Road

- 5.5.3 Others

- 5.6 End User Industry

- 5.6.1 E-Commerce

- 5.6.2 Financial Services (BFSI)

- 5.6.3 Healthcare

- 5.6.4 Manufacturing

- 5.6.5 Primary Industry

- 5.6.6 Wholesale and Retail Trade (Offline)

- 5.6.7 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Key Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share for Key Companies, Products and Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 FedEx

- 6.4.3 Grab Holdings Limited

- 6.4.4 J&T Express

- 6.4.5 Lion Parcel (a part of Lion Group)

- 6.4.6 Ninja Van (including Ninja Express)

- 6.4.7 PT Citra Van Titipan Kilat (TIKI)

- 6.4.8 PT Garuda Indonesia (Persero) TBK

- 6.4.9 PT Globalindo Dua Satu Express (21 Express)

- 6.4.10 PT ID Express Logistik Indonesia

- 6.4.11 PT Jalur Nugraha Ekakurir (JNE Express)

- 6.4.12 PT Kereta Api Indonesia (including KAI Logistik)

- 6.4.13 PT Pandu Siwi Group (Pandu Logistics)

- 6.4.14 PT Pos Indonesia (Persero)

- 6.4.15 PT Repex Wahana (RPX)

- 6.4.16 PT Satria Antaran Prima TBK (SAPX Express)

- 6.4.17 PT SiCepat Express Indonesia

- 6.4.18 PT Synergy First Logistics

- 6.4.19 PT Yapindo Transportama (PCP Express)

- 6.4.20 United Parcel Service (UPS)

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment