|

시장보고서

상품코드

2062188

북미의 창고 및 보관 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)North America Warehousing And Storage - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

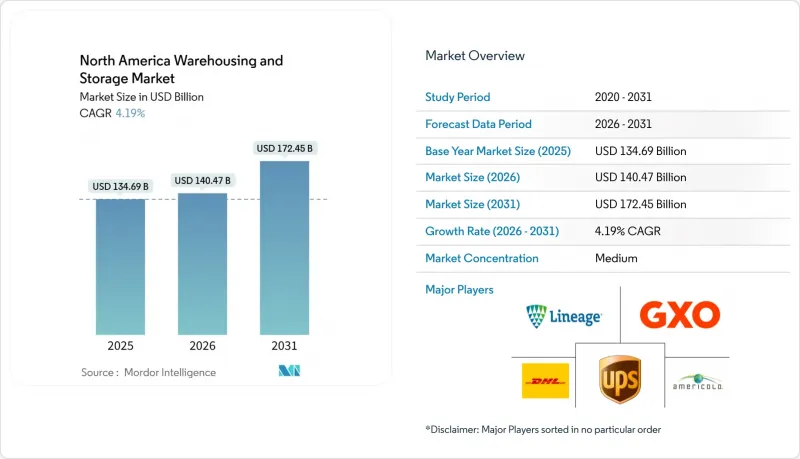

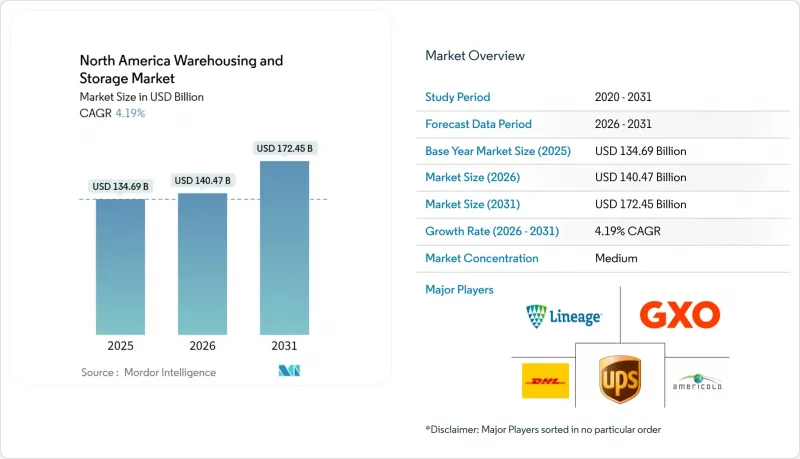

Mordor Intelligence에 의하면, 북미의 창고 및 보관 시장 규모는 2025년 1,346억 9,000만 달러로 평가되었습니다. 2026년 1,404억 7,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR은 4.19%를 나타내, 2031년에는 1,724억 5,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 창고 유형별(일반 창고 및 보관, 냉장 창고 및 보관, 농산물 창고 및 보관), 최종 사용자 산업별(전자상거래·소매, 식음료, 자동차, 제조·엔지니어링 제품, 기타), 지역별(미국, 캐나다, 멕시코)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미의 창고 및 보관 시장 동향과 인사이트

옴니채널 소매업에서의 당일 배송 전환

소매업체들은 현재 배송 시간 단축에 대응하기 위해 도심에서 10마일 반경 내에 재고를 배치하고 있습니다. 아마존의 펜실베이니아주 임페리얼과 아이다호주 남파 거점에서는 하루에 2만 건 이상의 주문을 처리하고 있는 반면, 월마트의 인디애나주 마코즈빌에 위치한 220만 제곱피트 규모의 허브에서는 자동 창고 시스템(AS/RS)을 활용해 피킹부터 출하까지의 주기를 2시간 이하로 단축하고 있습니다. 5만 제곱피트 이하의 라스트 마일 시설의 공실률은 4% 전후로, 전국 평균인 7.4%보다 낮습니다. Kase가 새로 개장한 20만 9,700제곱피트 규모의 폰타나 복합 시설은 소포 분류와 인랜드 엠파이어 지역 460만 주민을 위한 당일 배송 준비를 통합하고 있습니다. 2025년 1분기에 전자상거래 침투율이 미국 소매 매출의 16%에 달함에 따라, 인필 부지를 확보하지 못한 사업자들은 수직 통합형 경쟁사들에게 수익성이 높은 계약을 빼앗길 위험에 직면해 있습니다.

창고 자동화 및 로봇화를 통한 ROI의 급속한 개선

인건비 상승과 설비 가격 하락에 따라 로봇의 투자 회수 기간이 2-3년으로 단축되었습니다. GXO 로지스틱스에 따르면, 자율 주행 로봇을 통한 처리 능력은 30-40% 향상되었으며, 투자 회수 기간은 36개월 이하입니다. 루카스 시스템즈의 음성 안내형 스로틀링은 생산성을 20-40% 향상시키는 동시에 인건비를 10-20% 절감합니다. Stord가 4,000만 달러를 투자해 헤브론 거점을 확장한 이 프로젝트에는 52만 5,000제곱피트 규모의 자동 분류 시설이 포함되어 있으며, 이를 통해 중견 시장 배송업체들에게 기존 비용 구조보다 낮은 가격을 제공합니다. 주요 제약 요인은 인력 부족입니다. 사업자의 64%가 유지보수 기술자 채용에 어려움을 겪고 있으며, 벤더들은 다년 계약에 서비스 직원을 포함시키도록 압박받고 있습니다.

두 자릿수 산업용 임대료 상승이 사업자의 이익률을 압박하고 있습니다.

미국 주요 시장의 임대료 시세는 2020년 1제곱피트당 8-10달러에서 2025년에는 12-15달러에 달할 전망이며, 남부 캘리포니아에서는 임대료 인상률이 연 8%를 초과하고 있습니다. 그 결과 발생하는 이익률에 대한 압박으로 인해 3PL 사업자(제3자 물류 사업자)들은 리노, 피닉스 및 기타 2선 도시권으로 진출하고 있습니다. 이 지역들의 토지 비용은 해안가의 주요 거점에 비해 30-40% 저렴합니다. 그러나 장거리 운송으로 인해 배송 시간이 12-24시간 늘어나면서 당일 배송 서비스 제공이 위태로워지고 있습니다. 2026-2027년에 만료되는 임대차 계약의 갱신에 따라 임대료가 25-35% 인상될 예정이며, 이에 따라 포트폴리오를 자동화된 고밀도 시설로 재편해야 할 필요성이 대두될 것입니다.

부문별 분석

냉장 창고는 9.85%의 예상 연평균 성장률(CAGR)을 기록했습니다. 이는 사업자들이 의약품의 콜드체인 요건이나 신선식품의 온라인 판매 흐름에 대응하기 위함이며, 상온 창고의 임대료가 1제곱피트당 8-10달러인 반면, 냉장 창고에서는 12-15달러를 지불하고 있습니다. NewCold의 펜실베이니아주 레바논에 위치한 완전 자동화 시설은 기존 급속 냉동 시설에 비해 팔레트 밀도가 30% 향상된 반면, EVERSANA의 멤피스 허브에서는 바이오시밀러를 위해 -20℃의 보관 환경과 AI 재고 관리 시스템을 통합하고 있습니다.

2025년에도 일반 창고가 가장 큰 시장 규모를 유지했지만, 범용 SKU가 고밀도 자동화 시설로 전환됨에 따라 북미의 창고 및 보관 시장에서 차지하는 점유율(51.5%)은 줄어들고 있습니다. 농산물 보관은 여전히 틈새 시장에 머물러 있으며, 계절적 변동이 자동화의 투자 대비 효과를 저해하는 중서부 곡물 회랑 지역으로 한정되어 있습니다. 현재 자본은 상온 구역과 저온 구역을 동일한 시설 내에서 구획으로 나누는 하이브리드 설계로 전환되는 추세이며, 이를 통해 다양한 수익원을 확보하는 동시에 시설 리스크를 분산시키고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the north america warehousing and storage market size is expected to grow from USD 134.69 billion in 2025 to USD 140.47 billion in 2026 and is forecast to reach USD 172.45 billion by 2031 at 4.19% CAGR over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing and Storage, Refrigerated Warehousing and Storage, Farm Product Warehousing and Storage), by End-User Industry (E-Commerce and Retail, Food and Beverage, Automotive, Manufacturing and Engineering Goods, and More), and by Geography (United States, Canada, Mexico). The Market Forecasts are Provided in Terms of Value (USD).

North America Warehousing And Storage Market Trends and Insights

Omni-Channel Retail Shift to Same-Day Delivery Windows

Retailers now stage inventory within 10 miles of urban cores to meet shrinking delivery windows. Amazon's Imperial, Pennsylvania, and Nampa, Idaho sites each process 20,000-plus daily orders, while Walmart's 2.2 million square-foot McCordsville, Indiana hub uses automated storage and retrieval systems to cut pick-to-ship cycles below two hours. Vacancy in sub-50,000 square-foot last-mile facilities sits near 4% versus the 7.4% national average. Kase's new 209,700 square-foot Fontana complex integrates parcel sortation with same-day staging for 4.6 million Inland Empire residents. Operators unable to secure infill land risk ceding profitable contracts to vertically integrated rivals as e-commerce penetration climbed to 16% of United States retail sales in Q1 2025.

Rapid ROI Improvements in Warehouse Automation & Robotics

Payback periods for robotics have fallen to two to three years as labor costs soar and equipment prices drop. GXO Logistics reports 30-40% throughput gains from autonomous mobile robots with sub-36-month paybacks. Lucas Systems' voice-directed slotting delivers 20-40% productivity increases alongside 10-20% labor-cost reductions. Stord's USD 40 million Hebron expansion embeds 525,000 square feet of automated sortation, undercutting legacy cost structures for mid-market shippers. The primary constraint is talent: 64% of operators struggle to hire maintenance technicians, pushing vendors to embed service staff in multi-year contracts.

Double-Digit Industrial Rent Escalation Compressing Operator Margins

Asking rents in tier-one US markets reached USD 12-15 per square foot in 2025, up from USD 8-10 in 2020, while escalation clauses top 8% annually in Southern California. Resulting margin pressure pushes 3PLs toward Reno, Phoenix, and other secondary metros where land costs trail coastal gateways by 30-40%. Yet longer line-haul distances add 12-24 hours to delivery times, jeopardizing same-day offerings. Lease renewals coming due in 2026-2027 will impose 25-35% rent resets, forcing portfolio rationalization into automated, higher-density facilities.

Other drivers and restraints analyzed in the detailed report include:

- Post-USMCA Duty-Free Thresholds Boosting Cross-Border E-Commerce Flows

- Surplus Mall Conversions into Temperature-Controlled Distribution Nodes

- Enhanced CBP Cargo Screening Slowing Cross-Border Throughput

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Refrigerated warehousing posted a 9.85% forecast CAGR, as operators chase pharmaceutical cold-chain mandates and fresh-food e-grocery flows, paying USD 12-15 per square foot in rent against ambient's USD 8-10. NewCold's fully automated Lebanon, Pennsylvania site delivers 30% higher pallet density compared with legacy blast-freeze layouts, while EVERSANA's Memphis hub aligns -20 °C storage with AI inventory for biosimilars.

General warehousing retains the largest 2025 footprint, yet its 51.5% North America warehousing and storage market share erodes as commodity SKUs migrate toward higher-density automated sites. Farm-product storage stays niche, limited to Midwest grain corridors where seasonal volatility undermines automation ROI. Capital now flows to hybrid designs that partition ambient and cold zones under one roof, capturing diverse revenue streams while diluting site risk.

List of Companies Covered in this Report:

- Lineage, Inc.

- Americold

- DHL Group

- GXO Logistics

- Prologis

- GEODIS

- Kenco Logistics

- FedEx

- UPS Supply Chain Solutions

- Penske Logistics

- Ryder System

- CMA CGM (Including CEVA Logistics)

- DSV

- United States Cold Storage (USCS)

- Saddle Creek Logistics Services

- NFI Industries

- CJ Logistics

- Kuehne + Nagel

- Radial Inc. (bpost group)

- Metro Supply Chain

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Omni-Channel Retail Shift to Same-Day Delivery Windows

- 4.2.2 Rapid ROI Improvements in Warehouse Automation & Robotics

- 4.2.3 Post-USMCA Duty-Free Thresholds Boosting Cross-Border E-Commerce Flows

- 4.2.4 Surplus Mall Conversions into Temperature-Controlled Distribution Nodes

- 4.2.5 US West-Coast Port Electrification Grants Opening Brownfield Warehouse Sites

- 4.2.6 AI-Driven Dynamic Slotting Increasing Storage-Density Requirements

- 4.3 Market Restraints

- 4.3.1 Double-Digit Industrial Rent Escalation Compressing Operator Margins

- 4.3.2 Enhanced CBP Cargo Screening Slowing Cross-Border Throughput

- 4.3.3 Shortage Of Skilled Automation Technicians Elevating Downtime Risk

- 4.3.4 Municipal Moratoria on Diesel Yard Trucks Limiting Site Productivity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type (Value)

- 5.1.1 General Warehousing and Storage

- 5.1.2 Refrigerated Warehousing and Storage

- 5.1.3 Farm Product Warehousing and Storage

- 5.2 By End-User Industry (Value)

- 5.2.1 E-commerce & Retail

- 5.2.2 Food & Beverage

- 5.2.3 Pharma & Healthcare

- 5.2.4 Automotive

- 5.2.5 Manufacturing & Engineering Goods

- 5.2.6 Others

- 5.3 By Geography (Value)

- 5.3.1 United States

- 5.3.2 Canada

- 5.3.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 Lineage, Inc.

- 6.4.2 Americold

- 6.4.3 DHL Group

- 6.4.4 GXO Logistics

- 6.4.5 Prologis

- 6.4.6 GEODIS

- 6.4.7 Kenco Logistics

- 6.4.8 FedEx

- 6.4.9 UPS Supply Chain Solutions

- 6.4.10 Penske Logistics

- 6.4.11 Ryder System

- 6.4.12 CMA CGM (Including CEVA Logistics)

- 6.4.13 DSV

- 6.4.14 United States Cold Storage (USCS)

- 6.4.15 Saddle Creek Logistics Services

- 6.4.16 NFI Industries

- 6.4.17 CJ Logistics

- 6.4.18 Kuehne + Nagel

- 6.4.19 Radial Inc. (bpost group)

- 6.4.20 Metro Supply Chain