|

시장보고서

상품코드

2063325

독일의 화학제품 창고 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

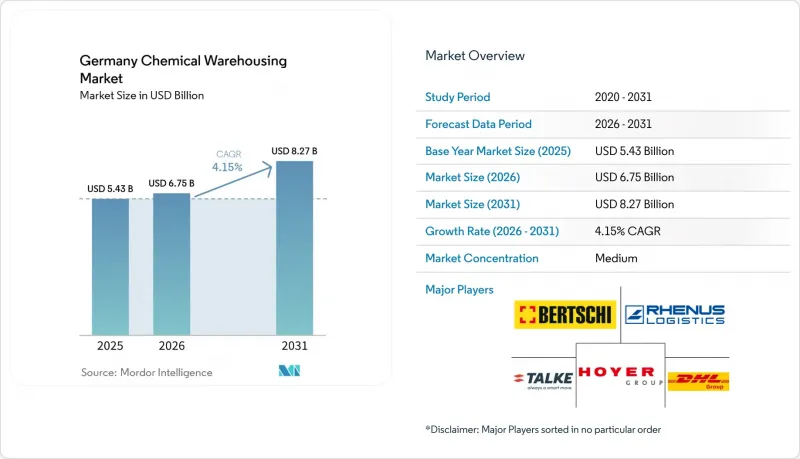

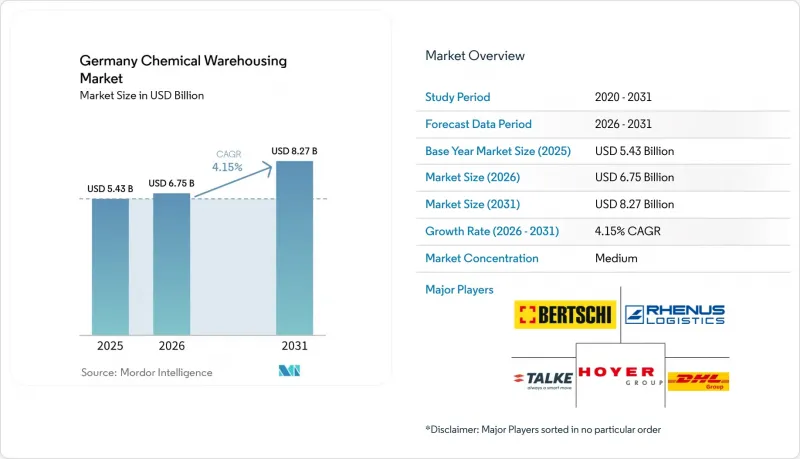

Mordor Intelligence에 의하면, 독일의 화학제품 창고 시장 규모는 2025년 54억 3,000만 달러로 평가되었고, 2026년에는 67억 5,000만 달러로 추정되고, 2031년까지 82억 7,000만 달러에 이를 것으로 예상되고 있으며, 2026-2031년 CAGR 4.15%로 성장할 전망입니다.

독일 내 화학제품 구성의 변화, REACH 부속서 VIII의 규제 강화, 그리고 배터리 재료 클러스터의 부상으로 인해, 기존의 석유화학제품이나 특수 화학제품의 재고 관리 수준을 훨씬 뛰어넘는 형태로 보관 요건이 재편되고 있습니다. 본 보고서는 창고 유형별(일반 창고, 특수 화학제품 창고 등), 화학제품 유형별(인화성 액체, 부식성 물질 등) 및 최종 사용자 산업별(기초 화학제품 제조, 특수 화학제품 제조, 의약품 및 생명과학, 농약 등)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일의 화학제품 창고 시장 동향 및 인사이트

REACH 부속서 VIII에 따른 보관 규제의 강화로 인한 수요

2024년 1월 이후, 유럽화학물질청(ECHA)은 창고에서 배치 단위로 혼합물을 분리 및 추적할 수 있는지 여부를 검증하는 감사를 강화하고 있으며, 이에 따라 재고 관리 소프트웨어 업그레이드, RFID 태그 도입 및 전용 환기 구역 설치가 요구되고 있습니다. 2025년에는 검사를 받은 독일 시설의 34%가 격리 테스트에 불합격하여, 중규모 거점 1곳당 120만-180만 유로(13억-20억 달러)의 개보수 비용이 발생했습니다. 대규모 제3자 물류(3PL) 기업들은 이러한 비용을 전국적인 네트워크 전반에 분산시켜 가격 결정력을 높이고 있습니다. 한편, 소규모 창고들은 이익률 압박에 직면하거나 독일 화학제품 창고 시장에서 철수할 수밖에 없는 상황에 놓여 있습니다. 블록체인을 활용한 보관 이력 관리 모듈은 창고 관리 시스템의 표준 부가 기능으로 자리 잡고 있으며, 주요 사업자들에게 새로운 기술 서비스 수익원을 창출하고 있습니다.

동독의 배터리 재료 붐이 용매 및 전해액 창고 수요를 견인하고 있습니다.

슈바르츠하이데에 위치한 BASF의 양극재 공장과 Northvolt의 기가팩토리 건설 계획에 따라, 습도 100ppm 미만이며 질소 분위기 하에서 보관이 가능한 리튬 염 및 전해액 용매에 대한 보관 수요가 증가하고 있습니다. 작센주와 브란덴부르크주의 토지 가격은 서부 지역보다 30-40% 저렴하여, ISO 탱크 세척 스테이션과 연계된 맞춤형 '드라이룸' 창고를 공급하려는 개발업자들의 관심을 끌고 있습니다. 자동차 제조업체들이 지역 밀착형 공급망을 추진하는 가운데, 동부의 화학 허브와 최종 조립 공장을 연결하는 복합 일괄 운송 노선이 독일 화학제품 창고 시장의 동부로의 이동을 뒷받침하고 있습니다.

변동하는 에너지 요금이 냉장 및 환기 설비의 운영 비용을 상승시키고 있습니다.

2025년 유럽 전역의 산업용 전력 가격은 여전히 극심한 변동성을 보이며 높은 수준을 유지해, 온도 관리형 및 초저온 창고의 운영 비용을 크게 상승시켰습니다. 이로 인해 냉동 및 에너지 관련 비용이 전년 대비 크게 증가했습니다. 일부 중견 제약 등급 물류 업체들은 장기 고정가 에너지 계약 재협상에 어려움을 겪은 끝에, 독일 화학제품 창고 시장의 일부에서 철수할 수밖에 없었습니다. 현장 태양광 발전 및 배터리 저장 솔루션은 전력망에 대한 의존도를 낮추고 효율을 높이는 데 도움이 되지만, 초기 투자 비용이 높기 때문에 도입은 주로 자본력이 있는 대형 사업자로 제한되어 있습니다.

부문별 분석

2025년 기준, 독일 화학제품 창고 시장 규모의 44.65%를 특수 화학제품 창고가 차지했으며, 이는 독일의 2,000억 유로(2,343억 6,000만 달러) 규모 화학 산업 기반에 힘입은 결과입니다. 온도 관리형 창고는 규모는 작지만, -80℃에서 25℃에 이르는 다온도대 보관이 필요한 바이오의약품, mRNA 백신, 고부가가치 첨가제 등에 힘입어 연평균 성장률(CAGR) 5.77%로 성장할 것으로 전망됩니다. 에너지 효율이 높은 냉장 설비, 로봇 셔틀, IoT 기후 센서가 시장 선도 기업의 차별화 요인으로 작용하고 있는 반면, 소규모 일반 창고들은 DIN 14096 규격으로의 업그레이드 자금을 조달하는 데 어려움을 겪으며 독일 화학제품 창고 시장 내 점유율을 잃고 있습니다.

현재, 제2의 투자 물결은 -80℃ 냉동고와 2-8℃ 보관실을 동일 시설 내에 함께 갖춘 스마트 콜드체인 거점으로 향하고 있으며, 이를 통해 세포 치료제의 운송 위험이 감소하게 됩니다. 이러한 보관 구역에 촉매 및 전자 화학약품 전용 보관 공간을 결합한 사업자는 교차 판매의 가능성을 높이고 있습니다. 업계 재편이 진행되는 가운데, 다온도대 대응이 가능한 메가사이트는 제약 및 특수 화학제품 고객사를 위한 원스톱 허브로서의 입지를 굳혀가고 있습니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the germany chemical warehousing market size is expected to increase from USD 5.43 billion in 2025 to USD 6.75 billion in 2026 and reach USD 8.27 billion by 2031, growing at a CAGR of 4.15% over 2026-2031.

Germany's evolving chemicals mix, tighter REACH Annex VIII rules, and the rise of battery-materials clusters are reshaping storage requirements well beyond traditional petrochemical and specialty-chemical inventories. This report is Segmented by Warehouse Type (General Warehousing, Speciality Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), and by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, Pharmaceuticals & Life Sciences, Agrochemicals, and More ). The Market Forecasts are Provided in Terms of Value (USD).

Germany Chemical Warehousing Market Trends and Insights

Enforcement-Driven Demand for REACH Annex VIII Compliant Storage

Since January 2024, the European Chemicals Agency has intensified audits that test whether warehouses can segregate and trace mixtures at the batch level, compelling upgrades in inventory software, RFID tagging, and dedicated ventilation zones. In 2025, 34% of inspected German facilities failed segregation tests, triggering retrofit bills of EUR 1.2-1.8 million (USD 1.3-2.0 billion) per mid-sized site. Larger 3PLs amortize these costs across national networks, gaining price power, while smaller depots face margin compression or forced exit from the Germany chemical warehousing market. Blockchain-based chain-of-custody modules are becoming standard add-ons to warehouse-management systems, creating a new tech-service revenue stream for leading operators.

East-German Battery-Materials Boom Boosting Solvent & Electrolyte Warehousing

BASF's cathode plant in Schwarzheide and Northvolt's gigafactory pipeline ignite demand for lithium-salt and electrolyte solvent storage engineered for <100 ppm humidity and nitrogen blanketing. Land in Saxony and Brandenburg costs 30-40% below western zones, drawing developers eager to supply bespoke "dry-room" warehouses that interface with ISO tank cleaning stations. As automotive OEMs push for regionalized supply chains, intermodal routes linking eastern chemical hubs to final assembly plants reinforce the Germany chemical warehousing market's eastward shift.

Volatile Energy Tariffs Inflating Refrigeration & Ventilation Opex

Industrial electricity prices in 2025 remained highly volatile and elevated across Europe, significantly increasing operating costs for temperature-controlled and sub-zero warehousing. This led to a meaningful rise in refrigeration and energy-related expenses year over year. Some mid-sized pharma-grade logistics operators were forced to exit parts of the German chemical warehousing market after struggling to renegotiate long-term fixed energy contracts. Although onsite solar and battery storage solutions help reduce grid dependence and improve efficiency, their high upfront capital requirements limit adoption mainly to larger, well-capitalized players.

Other drivers and restraints analyzed in the detailed report include:

- Biochemical Scale-Ups Requiring Segregated GMO-Free Storage Zones

- Deployment of Modular "ChemCube" Micro-Warehouses Near Innovation Campuses

- Stricter DIN 14096 Fire-Protection Code Prolonging Certification Cycles

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Specialty chemical warehouses represented 44.65% of the Germany chemical warehousing market size in 2025, anchored by the country's EUR 200 billion (USD 234.36 billion) chemicals base. Temperature-controlled depots, although smaller, are projected to grow at a 5.77% CAGR, driven by biologics, mRNA vaccines, and high-value excipients requiring -80 °C to 25 °C multipoint storage. Energy-efficient refrigeration, robotic shuttles, and IoT climate sensors differentiate market leaders, while smaller general warehouses struggle to finance DIN 14096 upgrades and lose share inside the Germany chemical warehousing market.

A second wave of investment now targets smart cold-chain nodes that co-locate -80 °C freezers and 2-8 °C rooms under one roof, cutting transit risks for cell therapies. Operators that combine these zones with specialty bays for catalysts or electronic chemicals increase cross-selling potential. As consolidation proceeds, multi-temperature mega-sites position themselves as one-stop hubs for pharmaceutical and specialty clients.

List of Companies Covered in this Report:

- DHL Group

- Rhenus Logistics

- HOYER Group

- TALKE Logistics

- Bertschi AG

- Kuehne+Nagel

- Den Hartogh Logistics

- DSV

- Hellmann Worldwide Logistics

- CMA CGM Group (Including CEVA Logistics)

- Infraserv Logistics

- NOSTA Group

- DACHSER

- Yusen Logistics

- Nippon Express

- H.Essers

- Mainfreight

- C. Steinweg Group

- LogCoop GmbH

- WEILKE Group

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Enforcement-driven demand for REACH Annex VIII compliant storage

- 4.2.2 East-German battery-materials boom boosting solvent & electrolyte warehousing

- 4.2.3 Biochemical scale-ups requiring segregated GMO-free storage zones

- 4.2.4 Deployment of modular "ChemCube" micro-warehouses near innovation campuses

- 4.2.5 CCU pilot plants creating need for liquid CO2 and intermediate storage

- 4.2.6 Railport electrification (Betuweroute & Hinterland) catalysing multimodal chem hubs

- 4.3 Market Restraints

- 4.3.1 Volatile energy tariffs inflating refrigeration & ventilation Opex

- 4.3.2 Stricter DIN 14096 fire-protection code prolonging certification cycles

- 4.3.3 Regulatory limbo on Li-ion bulk storage delaying investment decisions

- 4.3.4 Burgerinitiative-led opposition stalling hazmat site permitting

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Rhenus Logistics

- 6.4.3 HOYER Group

- 6.4.4 TALKE Logistics

- 6.4.5 Bertschi AG

- 6.4.6 Kuehne+Nagel

- 6.4.7 Den Hartogh Logistics

- 6.4.8 DSV

- 6.4.9 Hellmann Worldwide Logistics

- 6.4.10 CMA CGM Group (Including CEVA Logistics)

- 6.4.11 Infraserv Logistics

- 6.4.12 NOSTA Group

- 6.4.13 DACHSER

- 6.4.14 Yusen Logistics

- 6.4.15 Nippon Express

- 6.4.16 H.Essers

- 6.4.17 Mainfreight

- 6.4.18 C. Steinweg Group

- 6.4.19 LogCoop GmbH

- 6.4.20 WEILKE Group

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment