|

시장보고서

상품코드

2062320

북미의 전자상거래 창고 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America E-Commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

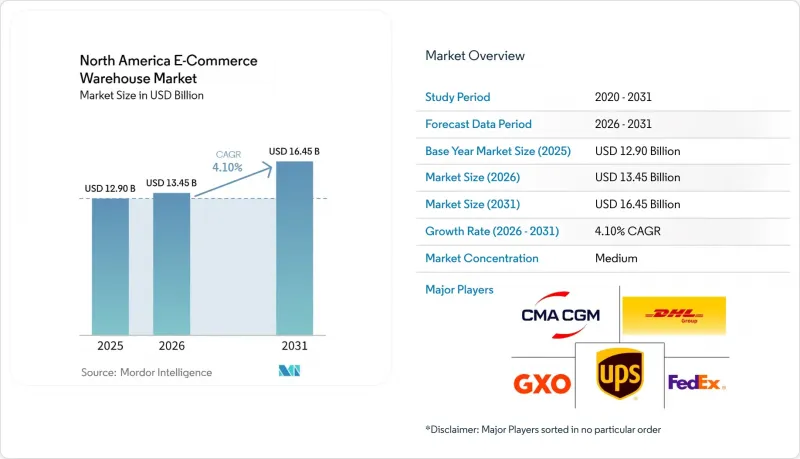

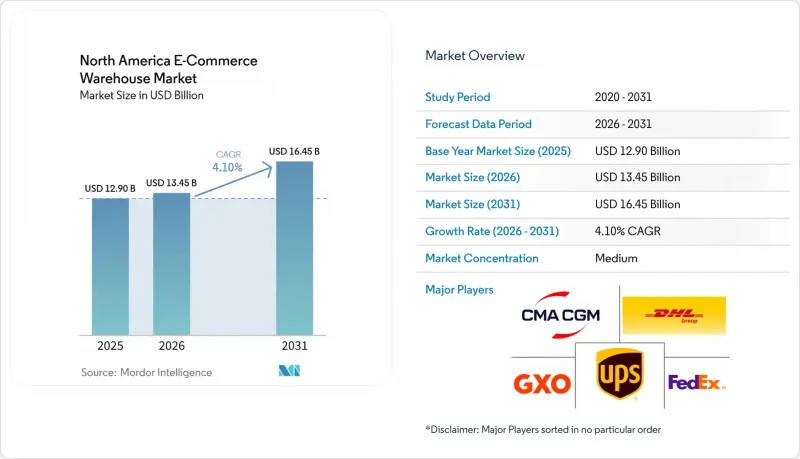

Mordor Intelligence에 의하면, 북미 전자상거래 창고 시장 규모는 2025년에 129억 달러, 2026년에 134억 5,000만 달러가 되어, 2031년까지 164억 5,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.1%로 성장할 전망입니다.

시장의 꾸준한 성장 이면에는 팔레트 단위의 B2B 주문과 신속한 소비자 배송이 동일한 산업용 공간을 놓고 경쟁하게 되면서, 창고 경제의 근본적인 재편이 숨어 있습니다. 본 보고서는 창고 유형(풀필먼트 센터, 창고, 다크 스토어, 마이크로 풀필먼트 센터 등), 서비스 유형(보관, 피킹·포장 등), 자동화 수준(수동, 반자동, 자동), 최종 사용자 산업(의류 및 신발 등) 및 국가별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 전자상거래 창고 시장 동향과 인사이트

B2B 전자상거래의 급증으로 인해 팔레트 단위의 보관 수요가 확대되고 있습니다.

B2B 디지털 판매의 확대에 따라, 피킹 및 포장 구역에 인접하여 팔레트 단위의 이동을 처리할 수 있는 하이브리드 랙에 대한 수요가 증가하고 있습니다. 2024년, 미국의 B2B 전자상거래 시장 규모는 1조 8,800억 달러를 넘어섰으며, 이는 창고 관리 알고리즘을 통해 하룻밤 사이에 재구성 가능한 슬로팅 시스템에 대한 수요를 촉진하고 있습니다. 일부 멀티테넌트 시설에서는 이미 일일 처리량의 30-40%가 팔레트 단위 주문으로 차지하고 있어, 천장 높이와 도크 도어를 둘러싼 경쟁이 치열해지고 있습니다. 그 결과, 신속한 변경 조항을 포함한 유연한 임대 계약이 장기 단일 용도 계약보다 더 빠른 속도로 증가하고 있습니다. 이러한 변화는 도매업체를 거치지 않고 온라인으로 직접 판매하는 제조업체들도 끌어들이고 있으며, 이로 인해 일정 변동성이 커지면서 연중무휴 24시간 운영이 유리해지고 있습니다.

구독 서비스와 DTC 브랜드의 성장이 키트화 및 맞춤화 역량을 주도하고 있습니다.

DTC(Direct-to-Consumer) 매출은 2025년에 1,200억 달러를 넘어, 출하 전 맞춤화가 필요한 더 작고 빈도가 높은 소포로의 추세가 강화되면서 주문당 처리 시간이 증가하고 있습니다. 각 운영사는 바닥 면적의 20-30%를 품질 관리 스테이션이나 맞춤형 포장 설비를 갖춘 키트 조립 셀에 할당하고 있으며, 평방피트당 수익을 40-50% 향상시키는 대신 더 높은 밀도의 인력 배치를 수용하고 있습니다. 미국 연방거래위원회(FTC)의 규정에 따른 복잡한 표시 의무는 추적 가능성과 관련된 시스템 요건을 더욱 엄격하게 만들고 있습니다. 성수기 수요 급증 시 워크셀 수를 신속하게 확대할 수 있는 시설은 현재 구독 플랫폼으로부터 더 많은 RFP(제안 요청서)를 확보하고 있습니다.

화재 및 홍수 위험에 따른 창고 보험료 급등

2025년, 미국 전역에서 상업용 부동산 보험료는 8.4% 상승했으나, 산불이나 홍수 위험 지역에서는 25-40%나 급등하여, 경우에 따라서는 재산세 지출을 초과하기도 했습니다. 로봇 자산으로 인해 보험 가치가 상승하기 때문에 완전 자동화된 시설에서 가장 급격한 상승세가 나타납니다. 기존 건물에서는 연간 평방피트당 5-7달러인 반면, 일부 시설에서는 연간 15달러를 넘는 견적이 제시되고 있습니다. 사업자들은 현재 네트워크 설계의 일환으로 FEMA(연방재난관리청)의 홍수 위험 구역 및 산불 위험 평가 결과를 지도에 반영하고 있으며, 최종 구간 거리를 약간 늘리는 대신 보유 비용을 절감하고 있습니다. 게다가 보험사들도 더욱 엄격해져 입지와 건물 사양을 면밀히 검토하고 있습니다. 그 결과, 개발업자와 사업자들은 이익률 압박, 확장 계획의 둔화, 그리고 특히 홍수나 화재 피해를 입기 쉬운 지역에서의 입지 선정의 자유도 저하라는 문제에 직면하고 있습니다.

부문별 분석

2025년 현재, 풀필먼트 센터는 북미 전자상거래 물류 시장 점유율의 43.47%를 차지하고 있으며, 이는 대량 보관 및 크로스도킹에 대한 지역적 수요에 힘입은 결과입니다. 한편, 소매업체들이 인구 밀집 도시 지역에서 2시간 배송을 약속하기 위해 수요를 확대함에 따라, 다크 스토어와 마이크로 풀필먼트 센터 시장은 2031년까지 연평균 성장률(CAGR) 9.34%를 나타낼 것으로 전망됩니다. 회전율이 높은 SKU가 도심 근교의 높은 임대료를 정당화해 주기 때문에 다크 스토어의 북미 전자상거래 물류창고 시장 규모는 꾸준히 확대될 것으로 전망됩니다. 컨테이너 하역(인바운드)에서는 여전히 물류 허브가 주류를 이루고 있지만, 온라인 식료품 시장의 확대에 따라 콜드체인 시설에 대한 수요도 급증하고 있습니다.

개발업체는 유휴 상태인 대형 소매점을 도심 지역의 다크 스토어로 전환하고 있으며, 이를 통해 매장 내 통로에서 쇼핑하는 방식에 비해 피킹 효율이 40-50% 향상되었습니다. 그러나 지자체에서는 과거 소매 상권에 대한 트럭 통행량과 소음 문제를 놓고 논의가 오가는 가운데, 구역 지정 문제를 둘러싼 갈등이 불거지고 있습니다. 도시 지역의 고층 창고 건설은 높이 제한으로 인해 여전히 드문 편이며, 지붕 높이 규제를 위반하지 않으면서 용적을 확대할 수 있는 메자닌 구조의 건설이 활성화되고 있습니다. 입지 접근성의 가치 덕분에 사업자들은 교외 창고에서 나타나는 임대료 인하 영향에서 벗어날 수 있었으며, 이는 북미 전자상거래 창고 시장 수요 양극화가 뚜렷이 드러나고 있음을 보여줍니다.

2025년 기준, 북미 전자상거래 물류창고 시장 규모의 46.15%를 보관 서비스가 차지했으나, 부가가치 서비스는 2031년까지 연평균 성장률(CAGR) 8.81%를 기록하며 다른 어떤 부문보다 높은 성장률을 보이고 있습니다. 북미 전자상거래 창고 시장의 우위는 키트화, 간편 조립, 선물 포장, 엄격한 품질 관리(QC) 업무를 단일 시설 내에서 통합할 수 있는 제3자 물류(3PL) 업체들에게 집중되어 있습니다. 운영자가 15분 단위로 인건비를 청구하기 때문에 팔레트당 수익이 증가하며, 랙 보관만 하는 경우와 비교했을 때 매출 총이익률이 2배가 되는 경우도 드물지 않습니다.

DTC 브랜드가 이러한 서비스를 이용하는 이유는 자체적으로 주문 처리할 경우 제품 출시 주기가 지연되기 때문입니다. 현재, 작업자는 회전율이 높은 재고 레인 옆에 작업 셀을 배치하여 이동 거리를 최소화함으로써, 매일의 주문 처리 효율을 높이고 있습니다. 그러나 이러한 업무 영역에서는 반복적이고 세밀한 작업이 요구되어 이직률이 최대 30%에 달하기 때문에 시장에 진출한 기업들은 직원들의 이직 방지를 위해 게임화 요소를 도입한 대시보드나 단계별 임금 체계를 도입하고 있습니다. 또한, 성수기에 사전 심사를 마친 긱 워커를 공급하는 유연한 노동 플랫폼도 등장하고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the north america e-commerce warehouse market size is projected to be USD 12.9 billion in 2025, USD 13.45 billion in 2026, and reach USD 16.45 billion by 2031, growing at a CAGR of 4.1% from 2026 to 2031.

The market's measured expansion masks a fundamental restructuring of warehouse economics as pallet-level B2B orders and high-velocity consumer shipments now compete for the same industrial footprints. This report is Segmented by Warehouse Type (Fulfillment Centers, Distribution Centers, Dark Stores and Micro-Fulfillment Centers, and More), by Service Type (Storage, Picking and Packing, and More), Automation Level (Manual, Semi-Automated, Automated), by End-User Industry (Apparel and Footwear, and More), and by Country. The Market Forecasts are Provided in Terms of Value (USD).

North America E-Commerce Warehouse Market Trends and Insights

B2B E-Commerce Surge Expanding Pallet-Level Storage Needs

Heightened B2B digital sales now require hybrid racking that supports full-pallet moves adjacent to pick-and-pack zones. United States B2B e-commerce exceeded USD 1.88 trillion in 2024, fueling demand for slotting systems that can be re-configured overnight through warehouse management algorithms. Some multi-tenant facilities already report 30-40% of daily volume in pallet orders, intensifying competition for ceiling height and dock doors. Flexible leases with quick change-over clauses are therefore outpacing long-term single-use contracts. The shift also attracts manufacturers bypassing wholesalers to sell directly online, which adds scheduling volatility that favors 24/7 operations.

Subscription and DTC Brand Growth Driving Kitting and Personalization Capacity

DTC sales exceeded USD 120 billion in 2025 and are trending toward smaller, more frequent boxes that must be personalized before shipping, raising labor minutes per order. Operators carve 20-30% of floor space into kitting cells equipped with QA stations and bespoke packaging, accepting denser headcounts in exchange for 40-50% higher revenue per square foot. Complex labeling obligations under United States Federal Trade Commission rules add to system requirements for traceability. Facilities that can scale work-cell counts rapidly during holiday spikes now win more RFPs from subscription platforms.

Escalating Warehouse-Insurance Premiums for Fire and Flood Risk

Commercial property premiums rose 8.4% nationwide in 2025, but spiked 25-40% in wildfire and flood zones, occasionally surpassing property-tax outlays. Fully automated sites see the sharpest uptick because robotics assets elevate insured values; some quotes exceed USD 15 per square foot each year versus USD 5-7 for conventional buildings. Operators now map FEMA floodplains and wildfire risk scorings as part of network design, trading slightly longer final-mile distances for lower carrying costs. Furthermore, insurers are becoming more discerning, scrutinizing both locations and building specifications. Consequently, developers and operators are contending with squeezed profit margins, a deceleration in expansion efforts, and diminished leeway in site selection, particularly in areas vulnerable to flooding or prone to fires.

Other drivers and restraints analyzed in the detailed report include:

- Free-Return Culture Escalating Reverse-Logistics Square Footage

- Oversized Imports Spurring High-Bay Warehouse Demand

- Construction-Material Supply Volatility Delaying New Builds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfillment centers accounted for 43.47% of the North America e-commerce warehouse market share in 2025, underpinned by regional demand for bulk storage and cross-docking. At the other end, dark stores and micro-fulfillment centers post a 9.34% CAGR to 2031 as retailers chase two-hour delivery promises in dense metros. The North America e-commerce warehouse market size for dark stores is projected to expand steadily as high-velocity SKUs justify higher rent profiles close to city cores. Distribution hubs still dominate inbound container deconsolidation, whereas cold-chain facilities accelerate alongside online grocery adoption.

Developers repurpose dormant big-box retail into urban dark stores, boosting pick rates by 40-50% compared with in-aisle shopping models. Yet zoning battles erupt as municipalities debate truck traffic and noise in former retail districts. High-bay construction within city limits remains rare due to height caps, encouraging mezzanine builds that stretch cubic capacity without breaching roof-height codes. Proximity's value shields operators from the rate cuts now visible at suburban sheds, underscoring bifurcated demand inside the North America e-commerce warehouse market.

Storage retained 46.15% of the North America e-commerce warehouse market size in 2025, but value-added services are on an 8.81% CAGR path that outpaces any other category through 2031. North America e-commerce warehouse market advantages accrue to 3PLs able to integrate kitting, light assembly, gift wrapping, and stringent QC routines under one roof. Revenue per pallet climbs as operators bill labor in fifteen-minute increments, frequently doubling gross margins relative to racked storage alone.

DTC brands resort to these services because in-house fulfillment would delay launch cycles. Operators now allocate work cells next to high-velocity inventory lanes, minimizing travel and lifting daily order-processing efficiency. However, these zones carry turnover rates up to 30% due to repetitive fine-motor tasks, so market participants deploy gamified dashboards and stepped wage ladders to retain staff. Flexible labor platforms also emerge, supplying pre-vetted gig workers during holiday peaks.

List of Companies Covered in this Report:

- DHL Group

- GXO Logistics

- FedEx

- United Parcel Service of America, Inc. (UPS)

- XPO, Inc.

- GEODIS

- C.H. Robinson

- Kenco Logistics

- Ryder System, Inc.

- Lineage, Inc.

- Americold

- NFI Industries

- Omni Logistics

- Penske Corporation

- Stord

- ShipNetwork

- Red Stag Fulfillment

- Buske Logistics

- CMA CGM Group (Including CEVA Logistics)

- DSV A/S

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 B2B E-Commerce Surge Expanding Pallet-Level Storage Needs

- 4.2.2 Subscription and DTC Brand Growth Driving Kitting and Personalization Capacity

- 4.2.3 Free-Return Culture Escalating Reverse-Logistics Square Footage

- 4.2.4 Oversized Imports (Furniture, Fitness) Spurring High-Bay Warehouse Demand

- 4.2.5 Carbon-Credit Funded "Green Warehouse" Projects Unlocking Capex

- 4.2.6 Rooftop Drone-Hub Integration Along FAA Delivery Corridors

- 4.3 Market Restraints

- 4.3.1 Escalating Warehouse-Insurance Premiums for Fire and Flood Risk

- 4.3.2 Construction-Material Supply Volatility Delaying New Builds

- 4.3.3 IoT Data-Privacy Regulations Complicating Sensor Deployment

- 4.3.4 Shortage of Robotics-Maintenance Technicians Elevating Downtime Risk

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value, USD)

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centers

- 5.1.2 Distribution Centers (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking and Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Fully Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By Country

- 5.5.1 United States

- 5.5.2 Canada

- 5.5.3 Mexico

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (Includes Global Level Overview, Market Level Overview, Core Segments, Financials as Available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 GXO Logistics

- 6.4.3 FedEx

- 6.4.4 United Parcel Service of America, Inc. (UPS)

- 6.4.5 XPO, Inc.

- 6.4.6 GEODIS

- 6.4.7 C.H. Robinson

- 6.4.8 Kenco Logistics

- 6.4.9 Ryder System, Inc.

- 6.4.10 Lineage, Inc.

- 6.4.11 Americold

- 6.4.12 NFI Industries

- 6.4.13 Omni Logistics

- 6.4.14 Penske Corporation

- 6.4.15 Stord

- 6.4.16 ShipNetwork

- 6.4.17 Red Stag Fulfillment

- 6.4.18 Buske Logistics

- 6.4.19 CMA CGM Group (Including CEVA Logistics)

- 6.4.20 DSV A/S