|

시장보고서

상품코드

2062032

화학제품 창고 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Chemical Warehousing - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

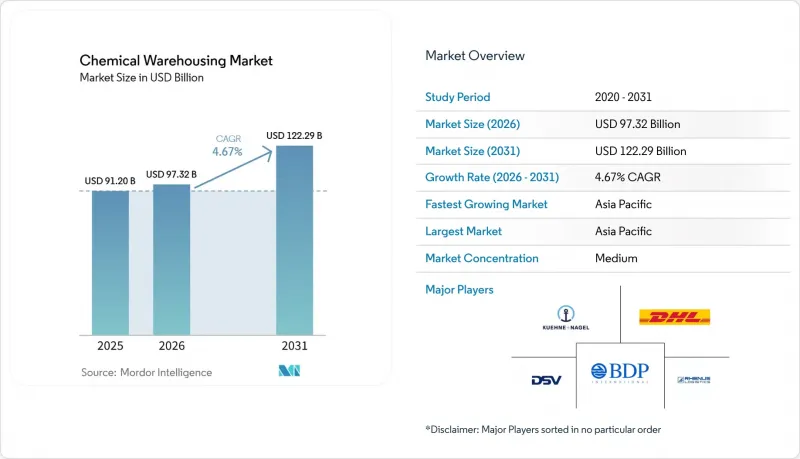

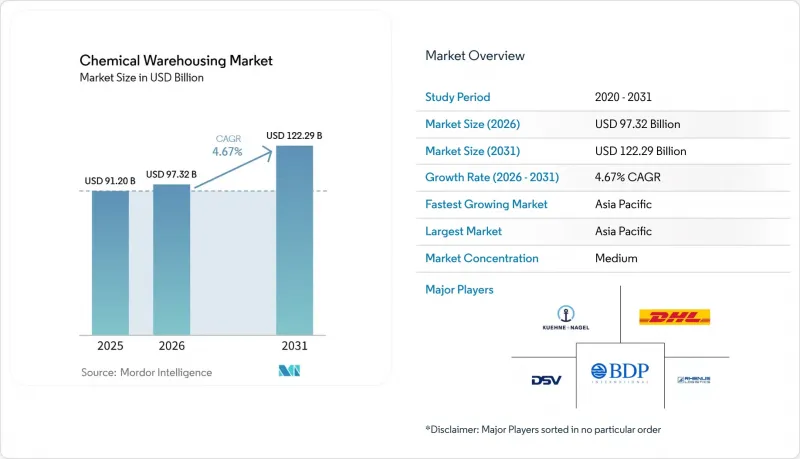

Mordor Intelligence에 의하면, 화학제품 창고 시장 규모는 2025년 912억 달러에서 2026년에는 973억 2,000만 달러로 확대되어 2031년까지 1,222억 9,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 4.67%로 성장할 전망입니다.

본 보고서는 창고 유형(일반 창고, 특수 화학제품 창고 등), 화학 물질 유형(인화성 액체, 부식성 물질 등), 최종 사용자 산업(기초 화학제품 제조, 특수 화학제품 제조 등) 및 지역(북미, 남미, 아시아태평양 등)별로 분류되어 있습니다. 시장 전망은 금액 기준(10억 달러)으로 제시되어 있습니다.

세계 화학제품 창고 시장 동향 및 인사이트

아시아태평양의 화학 생산 능력 확대가 해당 지역의 창고 수요를 견인하고 있습니다.

2026년 중국에서 가동을 시작할 예정인 새로운 폴리프로필렌 및 폴리에틸렌 생산 능력으로 인해, 중간체 및 포장용 수지의 단기 보관 수요가 증가함에 따라, 시운전 및 시장 확대기에 재고를 일시적으로 보관할 수 있는 규제 준수 시설에 대한 수요가 높아지고 있습니다. 중국의 차기 5개년 계획에 따른 정책 방향은 에너지 효율과 배출 성능을 중시하고 있으며, 이에 따라 규제 범위 내에서 운영되기 위해 높은 수준의 안전성, 격리 능력 및 지속가능성을 입증할 수 있는 인증 창고의 가치가 높아지고 있습니다. 인도의 3개 전용 화학 단지에 대한 예산 배분에는 공동 창고가 포함되어 있으며, 이는 통합된 클러스터가 프로젝트 리드타임을 단축하고 시험, 처리, 보관을 한 곳에서 수행할 수 있게 해줄 것이라는 신호로 해석됩니다. 다헤지 등 석유화학 및 특수 화학제품 허브와의 입지 통합은 체류 시간을 단축하고 복합 운송의 연계를 가능하게 합니다. 이를 통해 이러한 생태계에 임베디드된 사업자는 지속 가능한 처리 능력을 확보하기 위한 실질적인 우위를 점할 수 있습니다. 이러한 요소들이 결합되어 생산 동력과 인프라, 기준, 클러스터 경제를 연계함으로써 창고 이용률과 가격 결정력을 높여 화학제품 창고 시장을 주도하고 있습니다.

의약품 중간체의 생산 급증으로 인해 규정 준수 중심의 보관 기준이 강화되고 있습니다.

의약품 등급 중간체, 백신, 인슐린, 바이오의약품은 2-8°C 범위 내, 또는 특정 제제의 경우 초저온 환경에서 엄격한 온도 관리가 필요하며, 이에 따라 창고는 교정된 설비를 갖추고 온도 구역이 명확하게 관리되는 전용으로 설계된 콜드체인 거점으로 전환되고 있습니다. 미국의 DSCSA 일련번호 부여 제도는 창고에 대해 EPCIS 데이터 교환 및 단위 수준 식별자의 통합을 의무화하고 있으며, 시행 시한은 2026년까지 연장되었고 위반 시 부과되는 벌칙도 마련되어 있습니다. 이로 인해 조제업자나 도매업체에게 서비스를 제공하는 사업자에게는 디지털화 기준이 높아지고 있습니다. 유럽의약품청(EMA)은 팬데믹 기간 동안 연기되었던 GDP(적정 보관 기준) 현장 검사를 재개하고 있으며, 이에 따라 콜드체인 보관 전반에 걸친 교정, 규정 위반에 대한 대응, 감사 문서에 대한 감시가 강화되고 있습니다. 이러한 절차상의 조치로 인해 자본 집약도와 운영 규율이 강화되어, 실제 온도 변동 상황에서도 감사를 통과하고 견고한 표준 작업 절차서(SOP)를 유지할 수 있는 업체에 더 민감한 화물이 집중되고 있습니다. 그 결과, 더 높은 기준과 체계화된 추적성 덕분에, 특히 규제가 엄격한 북미와 유럽에서 화학제품 창고 시장의 기존 콜드체인 사업자들의 입지가 강화되고 있습니다.

지정학적 긴장으로 인한 국경을 넘는 화학물질 수송 차질이 재고 최적화를 저해하고 있습니다.

봉쇄나 분쟁으로 인한 우회 경로화로 인해 연료 가격의 기준치가 상승하고, 단기간에 주요 에너지 지표가 두 배로 증가함에 따라, 화학제품 유통업체들은 단기적으로는 더 많은 재고 완충량을 확보하고 처리 능력의 유연성을 낮출 수밖에 없는 상황에 처해 있습니다. 주요 생산자들의 가격 인상과 폴리머 및 용제 전반에 걸친 가격 조정으로 인해, 창고 내에 묶여 있는 운전 자금에 대한 수요가 증가하면서, 원활한 물류 운영을 위한 가용 공간이 부족해지고 있습니다. 희망봉을 우회하는 항로의 장기화와 출항 지연으로 인해 일시적인 혼잡과 운임 급등이 발생하고 있으며, 이러한 현상은 원인이 된 사태가 수습된 후에도 지속될 가능성이 있어 가동률 및 인력 계획 수립을 복잡하게 만들고 있습니다. 유럽에서는 주요 화학 자산의 가동률이 낮은 수준을 유지하고 있어 통합형 저장 용량이 축소되고 있으며, 최종 사용자에게 출하하기 전에 수입품의 임시 보관 및 검사가 필요한 특수 제품 취급 분야의 부담이 더욱 커지고 있습니다. 그 결과, 불확실성이 커지는 시기에 사업자들이 안전성, 서비스 수준, 비용 회수 간의 균형을 맞추려 노력하는 과정에서 화학제품 창고 시장의 유연성과 서비스 제공 비용에 단기적인 악영향이 발생하고 있습니다.

부문별 분석

2025년에는 위험물 창고가 43.67%를 차지했습니다. 이는 분리 보관, 방폭 시스템, 2차 격리 장치에 관한 규제 요건을 반영한 것으로, 화학물질 창고 시장에서 인증 시설에 대한 수요를 공고히 하고 있습니다. OSHA(미국 직업안전보건청)의 가연성 액체 보관 규정은 승인된 보관함 외부에서의 보관량을 제한하고, 범주별로 보관함의 허용 한도를 정의하고 있으며, 이에 따라 사업자는 상세한 안전 프로그램과 감사를 통해 관리되는 전용 위험물 보관 공간을 이용해야 합니다. 온도 관리 시설은 의약품 중간체 및 첨단 배터리에 사용되는 고감도 원료를 배경으로 6.32%의 성장률을 보이고 있습니다. 이러한 과정에는 교정된 시스템과 문서화된 점검을 통해 유지되는 엄격한 온도 범위 및 구역 관리가 필요합니다. 일반 화학제품 창고는 비위험물 범주를 다루고 있지만, 그 구성은 프리미엄 가격 책정, 서비스 수준 계약, 그리고 장기적인 사고 발생률 감소를 뒷받침하는 특수 품목이나 엄격한 규정 준수 요건을 갖춘 화물로 점차 전환되고 있습니다. ‘책임 있는 관리(Responsible Care)’와 같은 인증 절차나 시설별 검증은 신규 시장 진출기업이 따라잡기까지 수년이 소요되는 장기적인 차별화 요인이 되며, 규정 준수 비용의 상승과 더불어 화학제품 창고 시장에서 기존 사업자의 입지를 공고히 하고 있습니다.

온도 관리형 거점에서는 예측 유지보수 및 지속적인 모니터링을 도입하여 온도 편차를 방지하는 한편, 위험물(HAZMAT) 허브에서는 대상 화학물질의 규제 체계 및 지역 소방 법규를 준수하기 위해 가스 감지, CCTV, 출입 통제를 강화하고 있습니다. 규정 변경에 따라 배터리용 신흥 화학물질이 특정 유엔 분류나 항공 운송 규제의 적용 대상이 됨에 따라 위험물의 범위가 확대되고 있으며, 창고에서는 이를 표준 작업 절차(SOP) 및 교육 과정에 반영해야 합니다. 석유화학 및 화학제품 투자 지역 내의 집적은 여전히 유효한 전략입니다. 이는 유틸리티 및 시험 설비를 공유함으로써 사이클 타임을 단축하고 복합 일괄 운송을 간소화할 수 있기 때문입니다. 그 결과, 화학제품 창고 시장에서 위험물(HAZMAT) 시설의 확고한 우위가 유지될 뿐만 아니라, 엄격한 온도 관리 및 품질 관리가 필요한 제품이 늘어남에 따라 온도 관리형 시설의 급격한 성장이 예상됩니다.

지역별 분석

아시아태평양은 2025년에 34.90%의 시장 점유율을 차지해, 2031년까지 연평균 성장률(CAGR) 5.87%라는 가장 높은 성장세를 보일 것으로 전망됩니다. 이는 수지 및 석유화학제품의 대규모 증산에 따라 생산 거점, 수출 터미널, 시험 센터 인근에서의 중간 저장 수요가 확대되고 있기 때문입니다. 인도에서는 정책에 기반을 둔 파크 모델을 통해 공유 유틸리티, 폐수 처리 시설, 공동 창고가 클러스터 구조로 통합되어 있으며, 이를 통해 신제품 시장 출시 기간이 단축되고 사업자의 물류 리스크가 감소하고 있습니다. 수출 흐름에 연동된 대규모 암모니아 및 가성소다 처리 능력을 갖춘 전용 화학제품 항만 및 저장 거점에 대한 지역적 투자는 대량 수송과 엄격한 규정 준수가 요구되는 운송 경로를 뒷받침하는 통합 인프라로의 전환을 시사합니다. 동시에, 아시아태평양의 창고에서는 IoT를 활용한 모니터링 시스템을 도입하여, 목적지 시장에서 강화되고 있는 GDP 및 HAZMAT 기준에 대응하고 있습니다. 이러한 시장에서는 시설 내 엄격한 문서 관리 및 경보 프로토콜이 요구됩니다.

북미에서는 OSHA, EPA, DOT, DSCSA의 규제 체계에 따라 위험물 및 콜드체인 업무 전반에 걸친 인증 절차와 문서화된 품질 관리 체제가 강화되고 있으며, 그 결과 감사를 확실하게 통과할 수 있는 공급업체와의 통합이 촉진되고 있습니다. 의약품 등급 물류 시설을 운영하는 창고에서는 EPCIS 데이터 전송, 단위별 일련번호 부여 및 위변조 방지 대책에 주력하고 있으며, 이를 통해 출하 지연을 줄이고 검사 과정에서의 제품 무결성을 보호하고 있습니다. 위험물 분류와 관련하여, 사업자는 유출 방지 및 전기 분류 규정에 따른 분리 및 감시를 유지하고 있으며, 이를 통해 소규모 기업이 복잡한 화물 취급 경쟁에 참여하기 위해 충족해야 할 최소한의 역량이 확립되어 있습니다. 이러한 규정 준수 체계를 통해 북미는 화학제품 창고 시장에서 확고한 입지를 다지는 동시에, 민감한 제품 및 원자재를 위한 프리미엄 서비스 부문을 뒷받침하고 있습니다.

유럽에서는 기초 화학제품공급 과잉과 크래커 가동률 저하가 지속되고 있으며, 자산 폐쇄 및 생산 축소에 따라 일부 통합형 저장 시설이 시장에서 철수하고 있습니다. 로테르담이나 안트베르펜 항만 인근 터미널에서는 고객에게 납품하기 전에 시험이나 관리된 취급이 필요한 고순도 중간체를 대상으로 고가의 보관 서비스를 제공하고 있으며, 내륙 지역에서 이러한 특정 역량을 확보할 수 없는 수입업체들에게 공급의 안정성을 보장하고 있습니다. 공급 차질로 인한 악순환을 방지하고 현물 시장의 급등 위험을 완화하기 위해, 고정 보관료나 우선 접근권을 명시한 계약의 이용이 증가하고 있으며, 이를 통해 유럽의 유통업체들은 주요 원자재에 대한 재고 완충량을 보다 쉽게 계획할 수 있게 되었습니다. 중동 및 아프리카에서 계획 중인 생산 능력 확대와 전용 항만은 아시아태평양(APAC) 및 유럽으로의 수출 흐름을 정착시키는 것을 목표로 하고 있으며, 이에 따라 파이프라인망 및 심수 부두와 연결된 규제 준수 터미널의 전략적 가치가 높아지고 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the chemical warehousing market size is expected to increase from USD 91.20 billion in 2025 to USD 97.32 billion in 2026 and reach USD 122.29 billion by 2031, growing at a CAGR of 4.67% over 2026-2031.

This report is Segmented by Warehouse Type (General Warehousing, Specialty Chemical Warehouse, and More), by Chemical Type (Flammable Liquids, Corrosives, and More), by End-User Industry (Basic Chemicals Manufacturing, Specialty Chemicals Manufacturing, and More), and by Geography (North America, South America, Asia-Pacific, and More). The Market Forecasts are Provided in Terms of Value (USD Billion).

Global Chemical Warehousing Market Trends and Insights

Asia-Pacific Chemical Manufacturing Capacity Expansion Drives Regional Warehousing Demand

New polypropylene and polyethylene capacity coming online in China during 2026 intensifies short-term storage needs for intermediates and packaging resins, reinforcing demand for compliant facilities that can stage inventory during commissioning and market ramp-up. Policy direction under China's next five-year plan emphasizes energy efficiency and emission performance, which increases the value of certified warehouses able to demonstrate advanced safety, containment, and sustainability credentials to remain within regulatory guardrails. India's budgetary allocation for three dedicated Chemical Parks includes common warehousing, signaling that integrated clusters will shorten project lead times and bring testing, treatment, and storage under one roof. Co-location with petrochemical and specialty hubs such as Dahej reduces dwell time and enables intermodal connections, creating a practical edge for operators that embed within such ecosystems to capture sustained throughput. Together, these elements lift the chemical warehousing market by combining production momentum with infrastructure, standards, and cluster economics that elevate warehouse utilization and pricing power.

Pharmaceutical Intermediates Production Surge Elevates Compliance-Driven Storage Standards

Pharma-grade intermediates, vaccines, insulins, and biologics require stringent temperature control within 2-8°C or in ultra-cold environments for certain modalities, moving warehousing toward purpose-built cold chain nodes with calibrated equipment and mapped temperature zones. The U.S. DSCSA serialization regime pushes warehouses to integrate EPCIS data exchange and unit-level identifiers, with enforcement milestones extending into 2026 and penalties for non-compliance, which raises the digital baseline for operators that serve dispensers and wholesalers. The European Medicines Agency has resumed on-site GDP inspections after pandemic-era extensions, which elevates scrutiny on calibration, deviation handling, and audit documentation across cold chain storage. These procedural steps increase capital intensity and operating discipline, consolidating more sensitive loads with providers that can pass audits and maintain robust SOPs under real-world temperature variability. As a result, higher standards and serialized traceability strengthen the position of established cold chain players within the chemical warehousing market, particularly in North America and Europe, where enforcement is rigorous.

Geopolitical Tensions Disrupting Cross-Border Chemical Movements Constrain Inventory Optimization

Blockades and conflict-driven rerouting have raised fuel price benchmarks and doubled key energy references in compressed timelines, forcing chemical distributors to build larger inventory buffers and reduce throughput flexibility in the near term. Price surcharges from major producers and adjustments across polymers and solvents have widened working capital needs that sit on warehouse floors, which tightens available space for dynamic flows. Extended routing around the Cape and delayed sailing have created bursts of congestion and rate spikes that can persist after the trigger events, which complicates planning for occupancy and labor. In Europe, subpar utilization for core chemical assets has cut back integrated storage capacity, amplifying pressures in specialty handling where imports must be staged and tested before release to end users. The net effect is a short-term drag on flexibility and cost-to-serve inside the chemical warehousing market during periods of high uncertainty as operators balance safety, service levels, and cost recovery.

Other drivers and restraints analyzed in the detailed report include:

- Battery Chemical Production Boom for Electric Vehicles Reshapes Lithium Supply Chain Infrastructure

- Increasing Global Trade of Hazardous Chemicals Intensifies Port-Proximate Storage Demand

- Limited Availability of Specialized Tank Storage Capacity Constricts High-Purity Chemical Flows

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Hazardous materials warehouses accounted for 43.67% in 2025, reflecting regulatory requirements for segregated storage, explosion-proof systems, and secondary containment, which institutionalize demand for certified sites within the chemical warehousing market. OSHA's flammable liquid storage controls limit volumes outside approved cabinets and define cabinet thresholds by category, which pushes operators into purpose-built HAZMAT spaces governed by detailed safety programs and audits. Temperature-controlled facilities are growing at 6.32% on the back of pharma intermediates and sensitive inputs used in advanced batteries, which require tight thermal bands and mapped zones maintained by calibrated systems and documented checks. General chemical warehouses support non-hazardous categories, but the mix is tilting toward specialty and compliance-heavy loads that support premium pricing, service level agreements, and lower incident profiles over time. Certification pathways like Responsible Care and facility-specific verifications create multi-year differentiation that takes new entrants years to match, which strengthens incumbents inside the chemical warehousing market as compliance costs rise.

Temperature-controlled nodes deploy predictive maintenance and continuous monitoring to prevent thermal excursions, while HAZMAT hubs expand gas detection, CCTV, and controlled access to comply with chemical-of-interest frameworks and local fire codes. Regulatory changes are widening the HAZMAT scope as emerging chemistries for batteries receive specific UN classifications and air-transport controls that warehouses must build into their SOPs and training. Clustering within petrochemical and chemical investment regions remains a winning move because shared utilities and testing can reduce cycle times and simplify intermodal transfers. The net effect is durable leadership for HAZMAT sites in the chemical warehousing market and outsized growth in temperature-controlled facilities as more products require strict thermal and quality controls.

Geography Analysis

Asia-Pacific held 34.90% market share in 2025 and is projected to post the fastest CAGR at 5.87% through 2031 as large additions in resins and petrochemicals expand intermediate storage requirements near production hubs, export terminals, and testing centers. Policy-backed park models in India channel shared utilities, effluent treatment, and common warehousing into cluster frameworks, which improve time-to-market for new products and compress logistics risks for operators.Regional investments in dedicated chemical ports and storage nodes, including large-scale ammonia and caustic capacity tied to export flows, point to a shift toward integrated infrastructure that supports high-volume, high-compliance shipping lanes. At the same time, APAC warehouses are deploying IoT-driven monitoring to satisfy rising GDP and HAZMAT standards in destination markets, which rely on tighter documentation and alarm protocols inside the four walls.

North America has a system of OSHA, EPA, DOT, and DSCSA rules that reinforce certification pathways and documented quality systems across HAZMAT and cold chain operations, which in turn encourages consolidation with providers that can clear audits consistently. Warehouses supporting pharma-grade flows have leaned into EPCIS data transfer, unit-level serialization, and tamper-evident practices that reduce release delays and protect product integrity under inspection. For hazardous categories, operators maintain segregation and monitoring under spill containment and electrical classification rules, which establish minimum capabilities that smaller firms must meet to compete for complex loads. This compliance infrastructure gives North America a durable position in the chemical warehousing market while supporting premium service tiers for sensitive products and ingredients.

Europe continues to show base chemical overcapacity and weaker utilization for crackers, which has removed some integrated storage as assets close or scale down output. Port-proximate terminals in Rotterdam and Antwerp manage premium-priced storage for high-purity intermediates that require testing and control handling before customer delivery, safeguarding continuity for importers that face inland shortages for these specific capabilities. Disruption cycles have lifted the use of contracts with fixed storage fees and prioritized access to reduce exposure to spot market spikes, which helps European distributors plan inventory buffers for critical feedstocks. The Middle East and Africa's planned capacity expansions and dedicated ports are designed to anchor outbound flows into APAC and Europe, which increases the strategic value of compliant terminals tied to pipeline networks and deepwater berths.

- DHL Group

- Kuehne + Nagel

- DSV

- Rhenus Logistics

- BDP International

- Bertschi AG

- Den Hartogh Logistics

- Talke Logistics

- CLX Logistics

- XPO Logistics

- Hoyer Group

- Suttons Group

- GAC

- CEVA Logistics

- Nippon Express

- NYK Line (Yusen Logistics)

- C.H. Robinson

- Broekman Logistics

- FedEx

- United Parcel Service

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Asia-Pacific Chemical Manufacturing Capacity Expansion

- 4.2.2 Growth of Contract Manufacturing in Emerging Economies

- 4.2.3 Increasing Global Trade of Hazardous Chemicals

- 4.2.4 Pharmaceutical Intermediates Production Surge

- 4.2.5 Agricultural Chemicals Seasonal Storage Requirements

- 4.2.6 Battery Chemical Production Boom for Electric Vehicles

- 4.3 Market Restraints

- 4.3.1 Geopolitical Tensions Disrupting Cross-Border Chemical Movements

- 4.3.2 High Operational Complexity in Multi-Country Storage Networks

- 4.3.3 Limited Availability of Specialized Tank Storage Capacity

- 4.3.4 Competition from Direct Manufacturer-to-Consumer Shipments

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Bargaining Power of Buyers

- 4.7.4 Threat of Substitutes

- 4.7.5 Industry Rivalry

- 4.8 Emergence of Chemical Warehousing Hubs in Middle Corridor Trade Routes

- 4.9 Increased Focus on Circular Economy Storage Solutions

5 Market Size & Growth Forecasts (Value)

- 5.1 By Warehouse Type

- 5.1.1 General Warehousing

- 5.1.2 Speciality Chemical Warehouse

- 5.1.3 Hazardous Materials (HAZMAT) Warehouses

- 5.1.4 Temperature-Controlled Chemical Warehouses

- 5.2 By Chemical Type

- 5.2.1 Flammable Liquids

- 5.2.2 Corrosives

- 5.2.3 Toxic Substances

- 5.2.4 Oxidizers

- 5.2.5 Others

- 5.3 By End-user Industry

- 5.3.1 Basic Chemicals Manufacturing

- 5.3.2 Specialty Chemicals Manufacturing

- 5.3.3 Pharmaceuticals & Life Sciences

- 5.3.4 Agrochemicals

- 5.3.5 Paints, Coatings & Adhesives

- 5.3.6 Food & Feed Additives

- 5.3.7 Oil & Gas / Petrochemicals

- 5.3.8 Others

- 5.4 By Geography

- 5.4.1 North America

- 5.4.1.1 United States

- 5.4.1.2 Canada

- 5.4.1.3 Mexico

- 5.4.2 South America

- 5.4.2.1 Brazil

- 5.4.2.2 Peru

- 5.4.2.3 Chile

- 5.4.2.4 Argentina

- 5.4.2.5 Rest of South America

- 5.4.3 Asia-Pacific

- 5.4.3.1 India

- 5.4.3.2 China

- 5.4.3.3 Japan

- 5.4.3.4 Australia

- 5.4.3.5 South Korea

- 5.4.3.6 South East Asia (Singapore, Malaysia, Thailand, Indonesia, Vietnam, and Philippines)

- 5.4.3.7 Rest of Asia-Pacific

- 5.4.4 Europe

- 5.4.4.1 United Kingdom

- 5.4.4.2 Germany

- 5.4.4.3 France

- 5.4.4.4 Spain

- 5.4.4.5 Italy

- 5.4.4.6 BENELUX (Belgium, Netherlands, and Luxembourg)

- 5.4.4.7 NORDICS (Denmark, Finland, Iceland, Norway, and Sweden)

- 5.4.4.8 Rest of Europe

- 5.4.5 Middle East and Africa

- 5.4.5.1 United Arab of Emirates

- 5.4.5.2 Saudi Arabia

- 5.4.5.3 South Africa

- 5.4.5.4 Nigeria

- 5.4.5.5 Rest of Middle East And Africa

- 5.4.1 North America

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 Kuehne + Nagel

- 6.4.3 DSV

- 6.4.4 Rhenus Logistics

- 6.4.5 BDP International

- 6.4.6 Bertschi AG

- 6.4.7 Den Hartogh Logistics

- 6.4.8 Talke Logistics

- 6.4.9 CLX Logistics

- 6.4.10 XPO Logistics

- 6.4.11 Hoyer Group

- 6.4.12 Suttons Group

- 6.4.13 GAC

- 6.4.14 CEVA Logistics

- 6.4.15 Nippon Express

- 6.4.16 NYK Line (Yusen Logistics)

- 6.4.17 C.H. Robinson

- 6.4.18 Broekman Logistics

- 6.4.19 FedEx

- 6.4.20 United Parcel Service