|

시장보고서

상품코드

2062302

유럽의 전자상거래 창고 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)Europe E-Commerce Warehouse - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

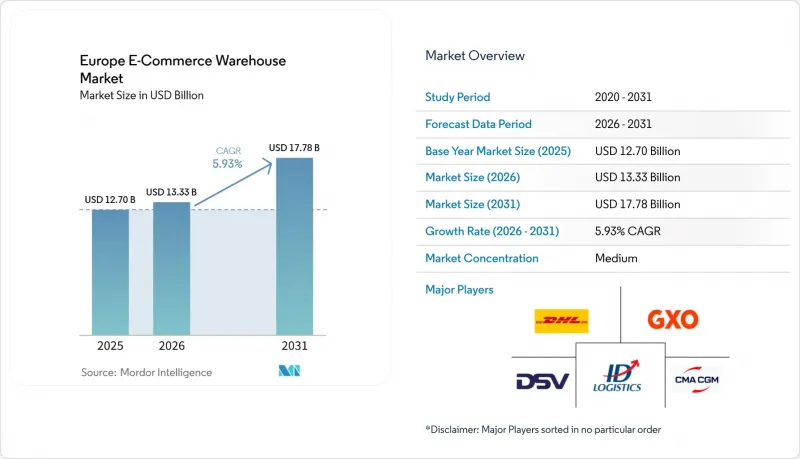

Mordor Intelligence에 의하면, 유럽 전자상거래 창고 시장 규모는 2025년에 127억 달러, 2026년에 133억 3,000만 달러가 되어, 2031년까지 177억 8,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 5.93%로 성장할 전망입니다.

현재 디지털 제품 여권(Digital Product Passport) 규제와 관련된 규정 준수 중심의 설비 투자가 주요 성장 동력이 되고 있으며, 사업자들은 단순히 시설 면적을 확대하는 것뿐만 아니라 상품 단위의 추적성을 확보해야 할 필요가 있습니다. 본 보고서는 창고 유형(풀필먼트 센터, 물류 센터, 콜드체인 창고, 다크 스토어/마이크로 풀필먼트 센터, 기타), 서비스 유형(보관, 기타), 자동화 수준(수동, 반자동, 자동), 최종 사용자 산업(의류 및 신발, 기타), 지역(독일, 영국, 프랑스, 기타)별로 세분화되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽 전자상거래 물류 센터 시장 동향과 인사이트

EU의 디지털 제품 여권이 일련번호 관리 기능을 갖춘 풀필먼트 허브의 확산을 촉진하고 있습니다.

2026년부터 시행되는 ‘디지털 제품 여권’에 따라, EU 지역 내에서 판매되는 모든 제품에는 그 수명 주기 전반에 걸쳐 추적 가능한 디지털 파일을 첨부해야 합니다. 현재 창고는 RFID, 블록체인 및 API 기반 데이터 교환을 지원해야 하므로, 투자의 초점이 랙 설비에서 정보 시스템으로 이동하고 있습니다. CEVA 로지스틱스 등 선도 기업들은 미래를 대비한 대응 역량을 확보하기 위해 이미 품목 단위 스캐너와 클라우드 커넥터의 도입을 추진하고 있습니다. 이 새로운 기준을 충족하지 못하는 사업자는 브랜드가 해당 네트워크로 전환함에 따라 고객을 잃을 위험이 있습니다. 반품된 상품은 재생산 및 재판매 과정에서도 디지털 ID를 유지해야 하므로, 전용 역물류 허브에 대한 수요도 동시에 증가하고 있습니다.

라이브 커머스 열풍이 주문 주기를 단축시키고, 마이크로 FC의 확장을 가속화하고 있습니다.

인플루언서가 주도하는 라이브 커머스 세션을 통해 소비자의 기대치는 익일 배송에서 당일 몇 시간 이내 배송으로 재정의되었습니다. 각 물류 업체들은 지하실, 주차장, 유휴 소매 점포를 고객이 밀집하는 지역에서 5km 이내에 위치한 마이크로 풀필먼트 센터로 전환하고 있습니다. AutoStore나 Exotec의 모듈식 자동화 시스템을 통해 5,000제곱미터 규모의 시설에서도 기존 메가센터와 동등한 처리 능력을 구현할 수 있습니다. Jumbo와 같은 소매업체들은 이 모델의 효과를 입증하며, 인력을 증원하지 않고도 라이브 커머스로 인한 수요 급증에 대응하고 있습니다. 현재 재고 계획은 라이브 스트리밍 이벤트 시작 전에 인기 SKU를 미리 보충하는 AI 루틴에 의존하고 있어, 품절 위험을 최소화하고 있습니다.

NIS2 사이버 보안 규제에 대한 대응이 중소기업의 IT 비용을 증가시키고 있습니다.

디지털 제품 여권 및 품목 단위 추적성에 대한 규정 준수 대응을 위한 지출이 현재 유럽의 EC 물류 창고 업계에서 주요 성장 동력이 되고 있으며, 단순한 확장에서 벗어나 30분 배송 수요에 대응할 수 있는 첨단 도시형 마이크로 풀필먼트 거점으로의 전환을 불가피하게 만들고 있습니다. 이번 전환은 유럽투자은행이 WDP 등 주요 기업에 제공하는 2억 5,000만 유로(2억 8,802만 달러) 규모의 그린 시설을 통해 지원되며, 철도를 활용한 물류와 5G를 활용한 자동화의 통합을 가능하게 하여, 도로 운송에 비해 스코프 3 배출량을 최대 75%까지 감축하고 있습니다. 그러나 NIS2 지침으로 인해 IT 관련 관리 비용이 크게 증가하면서, 중견 기업의 규정 준수 비용이 종종 50만 유로(57만 달러)를 초과하여 물리적 자동화에 대한 투자 자금을 압박하고 있습니다. 그 결과, EU에서는 27만 4,000명이 넘는 사이버 보안 전문가의 만성적인 부족 현상이 시장 재편을 가속화하고 있으며, 소규모 가족 경영 3PL 기업들이 이러한 규제 및 기술적 부담을 감당할 수 있는 대형 그룹에 의한 인수를 희망하는 상황입니다.

부문별 분석

2025년, 풀필먼트 센터는 유럽 전자상거래 물류창고 시장 점유율의 42.7%를 차지했습니다. 이들은 전국적인 서비스 범위와 대규모 재고 보관을 통해 소매업체 네트워크의 핵심을 담당하고 있습니다. 그러나 라이브 커머스와 신속 배송 모델로 인해 자본은 다크 스토어와 마이크로 풀필먼트 센터로 이동하고 있으며, 이 분야는 2031년까지 연평균 성장률(CAGR) 11.17%를 기록하며 가장 빠르게 성장하는 부문입니다. 2,000-5,000제곱미터 규모의 이 시설들은 인구 밀도가 높은 도심 지역에서 운영되고 있으며, 피킹 효율을 3배로 높여주는 ‘상품이 사람을 찾아가는’ 로봇 기술에 의존하고 있습니다. 콜루이트(Colruyt)의 ‘Collect&Go’ 프로젝트는 좁은 부지에서 생산성을 35% 향상시켰으며, 일반 상품 분야의 확장 가능성을 입증했습니다.

운영상의 핵심은 허브 앤 스포크 방식의 경제성을 유지할 것인지, 아니면 분산형 근접 모델을 채택할 것인지 하는 점입니다. 전자제품 등 고수익 분야에서는 구매자로부터 2km 반경 내에 플래시 세일용 재고를 배치할 수 있는 마이크로 사이트가 현재 선호되고 있습니다. 한편, 대량 상품이나 계절 상품은 여전히 공간 활용 효율성과 철도 부지선 접근성을 활용할 수 있는 메가 셰드형 풀필먼트 센터에 보관되고 있습니다. 이러한 이중 구조를 통해 유럽의 EC 물류창고 시장은 규모와 속도의 균형을 유지하고 있습니다.

2025년 기준으로 보관 업무는 유럽 EC 창고 시장 규모의 50.51%를 차지했으나, 해당 시장 내에서 점차 ‘인프라’적인 존재로 전환되고 있습니다. 한편, 연평균 성장률(CAGR) 10.64%의 성장이 예상되는 피킹 및 포장 업무야말로 차별화의 핵심입니다. 윈캔턴(Wincanton)과 같은 기업은 모듈형 로봇을 도입하여 피킹 효율을 5배로 높이고, 주문 발송 마감 시간인 2시간을 보장하고 있습니다. 디지털 제품 여권(DPP)에 대한 준수가 확대됨에 따라, 시리얼화 및 키트화가 표준 업무 흐름에 통합되어, 과거에는 부가 가치로 여겨졌던 것들이 이제는 필수 요건이 되었습니다.

성과 연계형 계약이 팔레트 보관료를 점차 대체하고 있습니다. 소매업체들은 주문 정확성과 처리 시간에 대한 대가를 지불하며, AI 스로틀링 도구와 머신 비전을 활용한 품질 관리 스테이션을 도입한 3PL 업체에 보상을 제공합니다. 마진이 낮은 보관 전문 업체들은 서비스 수준을 향상시키지 않으면 시장에서 도태될 위험에 직면해 있습니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHS 26.06.19According to Mordor Intelligence, the europe e-commerce warehouse market size is projected to be USD 12.7 billion in 2025, USD 13.33 billion in 2026, and reach USD 17.78 billion by 2031, growing at a CAGR of 5.93% from 2026 to 2031.

Compliance-driven capital spending tied to the Digital Product Passport regulation is now the primary growth engine, forcing operators to embed item-level traceability rather than simply adding floor space. This report is Segmented by Warehouse Type (Fulfilment Centers, Distribution Centers, Cold-Chain Warehouses, Dark Stores/Micro-Fulfillment Centers, Others), Service Type (Storage, and More), Automation Level (Manual, Semi-Automated, Automated), End-User Industry (Apparel & Footwear, and More), and Geography (Germany, UK, France, and More). The Market Forecasts are Provided in Terms of Value (USD).

Europe E-Commerce Warehouse Market Trends and Insights

EU Digital Product Passport Spurring Serialization-Ready Fulfillment Hubs

The Digital Product Passport, effective from 2026, obliges every product sold in the bloc to carry a digital file that follows the item through its life cycle. Warehouses must now support RFID, blockchain, and API-based data exchange, shifting investment from racking to information systems. Early movers such as CEVA Logistics are already installing item-level scanners and cloud connectors that future-proof capacity. Operators unable to meet the new standard risk customer defection as brands migrate to compliant networks. Demand for dedicated reverse-logistics hubs is rising in tandem because returned items must retain their digital identity during refurbishment and resale.

Live-Commerce Boom Compressing Order Cycles, Boosting Micro-FC Roll-Outs

Influencer-led live-commerce sessions have reset consumer expectations from next-day to same-hour delivery. Operators are converting basements, parking decks, and idle retail units into micro-fulfillment centers that sit within five kilometers of dense customer clusters. Modular automation from AutoStore and Exotec allows 5,000-square-meter sites to match the throughput of legacy mega-centers. Retailers such as Jumbo have proven the model, processing live-commerce spikes without adding labor. Inventory planning now relies on AI routines that preload popular SKUs before livestream events begin, minimizing out-of-stock risk.

NIS2 Cyber-Security Compliance Inflating IT Costs for SME Operators

Compliance-driven spending on Digital Product Passports and item-level traceability is now the primary growth engine for European e-commerce warehousing, forcing a shift from simple expansion toward high-tech, urban micro-fulfillment sites capable of meeting 30-minute delivery demands. This transition is supported by EUR 250 million (USD 288.02 million) green facilities from the European Investment Bank to major players such as WDP, enabling the integration of rail-served logistics and 5G-powered automation to slash Scope-3 emissions by up to 75% compared to road transport. However, the NIS2 Directive is significantly inflating IT overhead, with compliance costs for mid-sized firms often exceeding EUR 500,000 (USD 0.57 million) and siphoning capital away from physical automation. As a result, a persistent shortage of over 274,000 cybersecurity professionals in the EU is accelerating market consolidation, as smaller family-owned 3PLs seek buy-outs from larger groups that can absorb these regulatory and technical burdens.

Other drivers and restraints analyzed in the detailed report include:

- Southern-Europe E-Grocery Surge Accelerating Refrigerated Cross-Docks

- Scope-3 Decarbonization Fueling Demand for Rail-Integrated Freight Villages

- Shortfall of Recycled Materials Delaying Level(S)-Compliant Builds

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Fulfillment centers commanded 42.7% of the Europe e-commerce warehouse market share in 2025. They anchor retailer networks for national coverage and bulk inventory holding. However, live-commerce and rapid-delivery models are steering capital to dark stores and micro-fulfillment centers, the fastest-growing category at 11.17% CAGR through 2031. These 2,000-5,000 square-meter facilities operate within dense city cores and rely on goods-to-person robotics that triple pick rates. Colruyt's Collect&Go project raised productivity 35% in a compact site, showing scalability for general merchandise.

The operational gamble is whether to defend hub-and-spoke economics or embrace distributed proximity. High-margin verticals such as electronics now favor micro-sites that can stage flash-sale inventory two kilometers from buyers. Bulk goods and seasonal items remain in mega-shed fulfillment centers that still benefit from space economies and rail siding access. This dual structure keeps the Europe e-commerce warehouse market balanced between scale and speed.

Storage held 50.51% of the Europe e-commerce warehouse market size in 2025, yet it is sliding toward utility status within the Europe e-commerce warehouse market. Picking and packing, projected to grow 10.64% CAGR, is where differentiation lives. Operators like Wincanton use modular robotics to raise pick rates fivefold and guarantee two-hour cut-offs for order dispatch. Growing Digital Product Passport compliance embeds serialization and kitting into standard flows, turning what was once value-added into table stakes.

Outcome-based contracts are replacing pallet storage fees. Retailers pay for order accuracy and cycle time, rewarding those 3PLs that overlay AI slotting tools and machine-vision QC stations. Low-margin storage specialists risk displacement unless they climb the service ladder.

List of Companies Covered in this Report:

- DHL Group

- GXO Logistics

- CMA CGM Group (Including CEVA Logistics)

- DSV A/S

- ID Logistics

- XPO Inc.

- Kuehne+Nagel

- Arvato Group

- SEGRO plc

- GEODIS

- La Poste / GeoPost

- FM Logistic

- Rhenus Logistics

- Logwin Logistics

- InPost Fulfilment

- PostNL Parcels and Warehousing

- Raben Group

- Dachser SE

- Hellmann Worldwide Logistics

- BLG Logistics Group*

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 EU Digital Product Passport Spurring Serialization-Ready Fulfilment Hubs

- 4.2.2 Live-Commerce Boom Compressing Order Cycles, Boosting Micro-FC Roll-Outs

- 4.2.3 Southern-Europe E-Grocery Surge Accelerating Refrigerated Cross-Docks

- 4.2.4 Scope-3 Decarbonization Fueling Demand for Rail-Integrated Freight Villages

- 4.2.5 5G Private Networks Enabling AMR Retrofits of Inner-City Brownfield Sites

- 4.2.6 Subscription-Based Rental Models Driving Refurbishment and Reverse Hubs

- 4.3 Market Restraints

- 4.3.1 NIS2 Cyber-Security Compliance Inflating IT Costs for SME Operators

- 4.3.2 Shortfall of Recycled Materials Delaying Level(S)-Compliant Builds

- 4.3.3 Euro VII Truck Standards Raising First/Last-Mile Fleet Costs

- 4.3.4 Night-Time Traffic Caps Curbing Utilization of 24/7 Urban Facilities

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Suppliers

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts (Value)

- 5.1 By Warehouse Type

- 5.1.1 Fulfilment Centres

- 5.1.2 Distribution Centres (DCs)

- 5.1.3 Cold-Chain Warehouses

- 5.1.4 Dark Stores / Micro-Fulfillment Centers

- 5.1.5 Others (Reverse Logistics Hubs, Bonded Warehouses, Hybrid-use Spaces, etc.)

- 5.2 By Service Type

- 5.2.1 Storage

- 5.2.2 Picking & Packing

- 5.2.3 Value-Added Services and Others (Kitting, Labelling)

- 5.3 By Automation Level

- 5.3.1 Manual

- 5.3.2 Semi-Automated

- 5.3.3 Automated

- 5.4 By End-User Industry

- 5.4.1 Apparel and Footwear

- 5.4.2 Consumer Electronics

- 5.4.3 Grocery and FMCG

- 5.4.4 Pharmaceuticals, Beauty and Wellness

- 5.4.5 Home Essentials and Furnishings

- 5.4.6 Others

- 5.5 By Country

- 5.5.1 Germany

- 5.5.2 United Kingdom

- 5.5.3 France

- 5.5.4 Netherlands

- 5.5.5 Spain

- 5.5.6 Italy

- 5.5.7 Poland

- 5.5.8 Sweden

- 5.5.9 Belgium

- 5.5.10 Russia

- 5.5.11 Rest of Europe

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DHL Group

- 6.4.2 GXO Logistics

- 6.4.3 CMA CGM Group (Including CEVA Logistics)

- 6.4.4 DSV A/S

- 6.4.5 ID Logistics

- 6.4.6 XPO Inc.

- 6.4.7 Kuehne+Nagel

- 6.4.8 Arvato Group

- 6.4.9 SEGRO plc

- 6.4.10 GEODIS

- 6.4.11 La Poste / GeoPost

- 6.4.12 FM Logistic

- 6.4.13 Rhenus Logistics

- 6.4.14 Logwin Logistics

- 6.4.15 InPost Fulfilment

- 6.4.16 PostNL Parcels and Warehousing

- 6.4.17 Raben Group

- 6.4.18 Dachser SE

- 6.4.19 Hellmann Worldwide Logistics

- 6.4.20 BLG Logistics Group*