|

시장보고서

상품코드

2063307

독일의 화물 중개 서비스 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Germany Freight Brokerage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

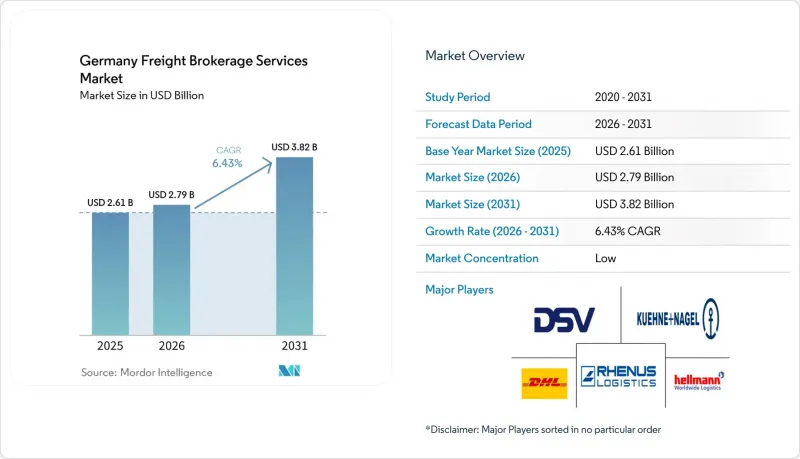

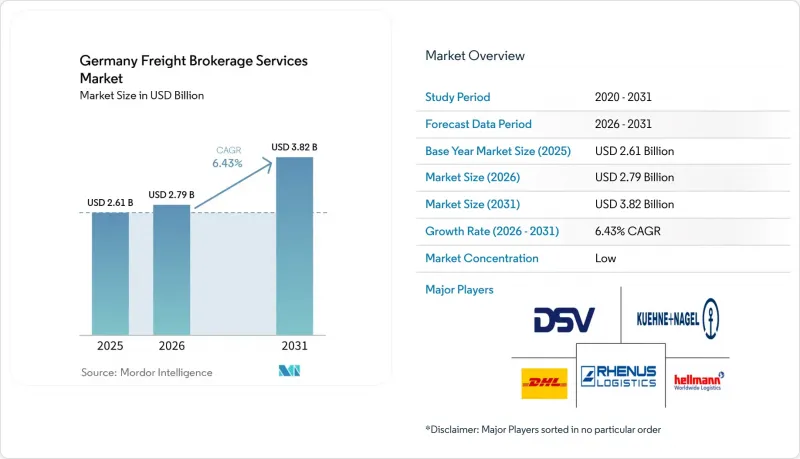

Mordor Intelligence에 의하면, 독일의 화물 중개 서비스 시장 규모는 2025년에 26억 1,000만 달러로 평가되었습니다. 2026년에 27억 9,000만 달러에 달하고, 2031년까지 38억 2,000만 달러에 이를 것으로 예측되며, 2026-2031년에 걸쳐 CAGR은 6.43%를 나타낼 전망입니다.

수요가 확대되고 있는 배경으로는 제조업체들이 유라시아 무역 경로를 다각화하고 있다는 점, 화주들이 화물의 실시간 가시성을 요구하고 있다는 점, 연방 정부의 정책에 따라 제로 배출 트럭의 통행료 면제가 유지되고 있다는 점 등을 들 수 있습니다. 본 보고서는 서비스(전체 트럭 적재, 기타), 차량·트레일러 유형(드라이 밴, 냉장 밴, 기타), 운송 거리(장거리, 지역 내, 단거리), 비즈니스 모델(기존, 자산 보유형, 기타), 최종 사용자 산업(제조·자동차, 기타), 고객 규모(대기업, 기타)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

독일의 화물 중개 서비스 시장 동향 및 인사이트

홍해 우회 노선 개통 이후 수요가 증가함에 따라, 독일을 경유하는 유라시아 간 철도 운송에서 도로 운송으로의 환적이 확대되고 있습니다.

해적 행위의 위험이 지속됨에 따라 아시아와 유럽 간 해상 화물 운송이 유라시아 철도로 전환되고 있으며, 2024년 중국과 EU 간 철도 운송량은 전년 대비 80.2% 증가한 380,434 TEU에 달했습니다. 뒤스부르크와 함부르크는 내륙 터미널에서 트럭으로 컨테이너를 환적하는 관문 역할을 하고 있으며, 이는 중개업자에게 높은 이익률을 안겨주고 시간적 제약이 있는 화물을 창출하고 있습니다. 서쪽으로 향하는 철도 운송으로 인해 독일 국내에 남는 빈 컨테이너가 감소함에 따라, 빈 컨테이너 재배치 수요도 확대되고 있어 중개업자들은 북해 연안 항구로의 역방향 운송을 주선할 수밖에 없는 상황입니다. 홍해 항로의 상황이 정상화되지 않는 한, 브로커들은 적어도 2027년까지는 이러한 철도 주도 수요 증가에 의존할 수 있으며, 독일의 화물 중개 서비스 시장에서 사업 운영에 새로운 수익원을 확보할 수 있게 될 것입니다.

전기 트럭에 대한 보조금 확대가 새로운 운송 회랑을 개척합니다.

독일은 주요 아우토반을 따라 1,410기의 고출력 충전기를 설치하기 위해 17억 4,000만 달러를 배정했습니다. 이 조치로 인해 배터리 구동 트럭의 킬로미터당 에너지 비용이 40% 절감되어, 운송 중개업체의 노선 선택의 폭이 넓어집니다. 제로 배출 대형 차량에 대한 통행료 면제는 현재 2031년 중반까지 연장되어 있으며, 이를 통해 총 소유 비용이 절감됨에 따라 중규모 운송 사업자들이 디젤 견인차의 조기 교체를 추진하도록 장려되고 있습니다. 전기자동차 차량군에서 수집한 텔레매틱스 데이터를 활용하는 중개업체는 충전기가 부족한 장소를 우회하여 경로를 변경하고, 정차 시간을 단축함으로써, 친환경 화물을 선호하는 화주에게 저탄소 운송 능력을 어필할 수 있습니다. A3, A5, A7호선 연선의 충전 클러스터는 이미 디젤차 전용 차선에서 오는 물동량을 전환하고 있습니다. 따라서 이 프로그램은 비용 절감과 새로운 판매 포인트라는 두 가지 이점을 모두 제공하며, 독일의 화물 중개 서비스 시장의 성장을 뒷받침하고 있습니다.

EU 모빌리티 패키지 IV : 임금 평등 감사가 규정 준수 비용을 증가시킵니다.

2026년 1월부터 독일에서는 파견 운전기사에게 시간당 15.1달러의 최저임금이 적용됨에 따라, 동유럽 운송업체들이 가지고 있던 기존 25%의 임금 우위성이 사라지게 됩니다. 브로커들은 현재 급여 파일과 타코그래프 기록을 감사하는 데 추가적인 시간을 할애하고 있으며, 그렇지 않을 경우 엄중한 처벌을 받을 위험이 있습니다. 2026년 7월부터 소형 밴에도 적용되는 ‘스마트 타코그래프 2’ 규정에 따라 감사 범위가 더욱 확대될 예정입니다. 일부 소규모 중개업체들은 규정 준수 도구への 투자를 피하기 위해 국경을 넘는 경로에서 철수하고 있으며, 이로 인해 운송 능력이 부족해져 현물 가격이 상승하는 한편, 중개업체의 이익률도 압박받고 있습니다.

부문별 분석

2025년, 독일의 화물 중개 서비스 시장에서 풀 트럭 로드(FTL)가 73.22%의 점유율을 차지했습니다. 이는 자동차 산업의 저스트-인-시퀀싱 운송과 벌크 화학물질 운송이 전용 트레일러에 의존하고 있었기 때문입니다. 계약 노선을 통해 화주는 예측 가능한 운임을 확보할 수 있으며, 중개업자는 반복적인 운송 물량을 통해 안정적인 이익률을 확보하고 있습니다. A4, A6, A9를 따라 구축된 물류망이 확충됨에 따라 남북 간 당일 배송이 가능해졌으며, 이는 1차 공급업체에게 매우 중요한 요소입니다.

소량 화물(LTL) 솔루션은 전자상거래 소포의 혼적 및 소량 산업용 주문에 힘입어 2031년까지 연평균 성장률(CAGR) 8.09%를 기록하며 성장할 것으로 전망됩니다. IDS Logistik과 Spedition Kleine의 제휴를 통해 해당 회사의 그레벤브로이히 허브에는 하루 800건의 배송이 처리되고 있으며, 이는 도크 스케줄링 API가 야드 체류 시간을 70% 단축할 수 있음을 입증하는 사례입니다. 현재 2-10개의 팔레트 분량의 화물을 통합하는 중개업체들은 AI를 활용해 적재 효율을 최적화하고 공차 주행 거리를 줄임으로써 수익성을 높이고, LTL 사업자를 위한 독일의 화물 중개 서비스 시장 규모를 확대되고 있습니다.

드라이밴 트레일러는 특수한 취급이 최소한으로만 필요한 소비재, 포장 식품, 산업용 부품을 운송하기 위해 사용되었으며, 2025년에는 설비 수익의 38.41%를 차지했습니다. 이러한 높은 보급률 덕분에 가장 광범위한 운송업체 풀을 확보하고 있으며, 현물 운임에 대한 경쟁을 유지하고 있습니다.

냉장 밴 시장은 백신용 콜드체인 감사 및 온라인 식료품 판매 확대에 힘입어 연평균 성장률(CAGR) 8.67%를 나타낼 것으로 전망됩니다. 스페인과 이탈리아에서 수입되는 제철 과일 운송으로 인해, 겨울 성수기에는 독일행 냉장 트레일러의 스팟 운임이 일반 화물 운송의 2배에 달할 전망입니다. 전력망에 연결된 주차 공간에서 전기식 냉장 장치를 사전 예약하는 중개업체는 디젤 할증료 절감 효과 외에도 탄소 중립을 중시하는 식품 소매업체들의 지지를 얻고 있으며, 이로 인해 온도 관리가 필요한 틈새 시장에서 독일의 화물 중개 서비스 시장 규모가 확대되고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTH 26.06.22According to Mordor Intelligence, the germany freight brokerage services market size is projected to be USD 2.61 billion in 2025, USD 2.79 billion in 2026, and reach USD 3.82 billion by 2031, growing at a CAGR of 6.43% from 2026 to 2031.

Demand expands because manufacturers diversify Eurasian trade routes, shippers chase real-time load visibility, and federal policy keeps toll exemptions for zero-emission trucks. This report is Segmented by Service (Full-Truckload, and More), Equipment/Trailer Type (Dry Van, Refrigerated Van, and More), Haul Length (Long-Haul, Regional, and Local), Business Model (Traditional, Asset-Based, and More), End-User Industry (Manufacturing & Automotive, and More), Customer Size (Large Enterprise, and More). The Market Forecasts are Provided in Terms of Value (USD).

Germany Freight Brokerage Services Market Trends and Insights

Post-Red-Sea Diversion boosting Eurasian Rail-to-Road Trans-loading through Germany

Persistent piracy risk has pushed Asia-Europe ocean cargo toward Eurasian rail, lifting China-EU rail volume to 380,434 TEU in 2024, an 80.2% jump year on year. Duisburg and Hamburg act as gateways where inland terminals shift containers to trucks for final delivery, creating high-margin, time-sensitive loads for brokers. Empty-box repositioning also grows as westbound rail leaves fewer empties in Germany, compelling brokers to organize backhauls to North Sea ports. Unless Red Sea routes normalize, brokers can rely on this rail-driven uplift through at least 2027, embedding new revenue channels in Germany freight brokerage services market operations.

Electrified-Truck Subsidy Wave Unlocking New Capacity Corridors

Germany has allocated USD 1.74 billion for 1,410 high-power chargers along major autobahns, a move that lowers per-kilometer energy cost by 40% for battery trucks and widens lane options for brokers. Toll exemptions for zero-emission heavy vehicles now run to mid-2031, shrinking the total cost of ownership and encouraging mid-sized carriers to replace diesel tractors sooner. Brokers that ingest telematics data from electric fleets can reroute around scarce chargers, cut dwell time, and advertise low-carbon capacity to shippers seeking greener loads. Charging clusters on A3, A5, and A7 already shift volume from diesel lanes. The program therefore delivers both cost savings and new selling points that propel Germany freight brokerage services market growth.

EU Mobility Package IV Wage-Parity Audits Inflating Compliance Overhead

From January 2026, Germany will enforce a USD 15.1 hourly wage floor for posted drivers, erasing the historical 25% rate edge held by Eastern European carriers. Brokers now spend extra hours auditing payroll files and tachograph logs, or risk stiff penalties. Smart Tachograph 2 rules, hitting light vans in July 2026, widen the audit scope. Some small brokers are exiting cross-border lanes rather than funding compliance tools, which tightens capacity and raises spot prices but also crimps broker margins.

Other drivers and restraints analyzed in the detailed report include:

- AI-Based Dynamic Lane-Pricing Demanded by Top 500 German Shippers

- Corporate Scope-3 Emissions Audits Creating Premium for Tracked Loads

- Cyber-Attacks on Freight-Exchange APIs Increasing Insurance Premiums

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Full-truckload commanded 73.22% of Germany freight brokerage services market share in 2025, as automotive just-in-sequence shipments and bulk chemicals relied on dedicated trailers. Contract lanes give shippers predictable rates, and brokers earn steady margins from repeat volume. Network depth along A4, A6, and A9 supports same-day north-south runs, a critical feature for tier-one suppliers.

Less-than-truckload solutions are projected to grow at an 8.09% CAGR to 2031, supported by e-commerce parcel consolidation and small-batch industrial orders. IDS Logistik's tie-up with Spedition Kleine brings 800 daily deliveries into its Grevenbroich hub, a case that proves how dock-scheduling APIs can cut yard dwell by 70%. Brokers aggregating 2-10-pallet loads now leverage AI to optimize cube and reduce empty miles, lifting yield and enhancing the Germany freight brokerage services market size for LTL operators.

Dry-van trailers held 38.41% of equipment revenue in 2025 because they move consumer goods, packaged foods, and industrial parts with minimal special handling. Their ubiquity ensures the widest carrier pool, which keeps spot quotes competitive.

Refrigerated vans are forecast to expand at an 8.67% CAGR, fueled by cold-chain audits for vaccines and the spread of online grocery. Seasonal fruit runs from Spain and Italy boost Germany-bound reefer spot rates to double dry-van levels during winter peaks. Brokers that pre-book electric reefer units at grid-connected parking bays enjoy lower diesel surcharges and gain loyalty from carbon-conscious food retailers, increasing the size of the German freight brokerage services market captured in the temperature-controlled niche.

List of Companies Covered in this Report:

- DSV A/S (including DB Schenker)

- DHL Group

- Kuehne+Nagel

- Rhenus Logistics

- Hellmann Worldwide Logistics

- Dachser

- Sennder

- Transporeon

- C.H. Robinson

- Yusen Logistics (Part of NYK Line)

- GEODIS

- Rohlig Logistics

- Emo Trans

- Trucksters

- Fiege Logistics

- Cargoline

- System Alliance Europe

- Carmovia

- Ontruck

- SLYNX

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Electrified-Truck Subsidy Wave Unlocking New Capacity Corridors

- 4.2.2 AI-Based Dynamic Lane-Pricing Demanded by Top 500 German Shippers

- 4.2.3 Post-Red-Sea Diversion Boosting Eurasian Rail-to-Road Trans-loading through Germany

- 4.2.4 Corporate Scope-3 Emissions Audits Creating Premium for Tracked Loads

- 4.2.5 Shift from FOB to DDP Terms in Mittelstand Exports Raising Brokerage Need for Door-To-Door Control

- 4.2.6 Federal "ETA Transparency Mandate" Accelerating API Adoption

- 4.3 Market Restraints

- 4.3.1 EU Mobility Package IV Wage-Parity Audits Inflating Compliance Overhead

- 4.3.2 Cyber-Attacks on Freight-Exchange APIs Increasing Insurance Premiums

- 4.3.3 Logistic-Hub Zoning Freeze in Nordrhein-Westfalen Limiting Cross-Dock Expansion

- 4.3.4 Volatile OEM Production Cycles (EV and Semiconductor Swings) Driving Demand Unpredictability

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Threat of New Entrants

- 4.7.2 Bargaining Power of Buyers

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size and Growth Forecasts

- 5.1 By Service

- 5.1.1 Full-Truckload (FTL)

- 5.1.2 Less-than-Truckload (LTL)

- 5.1.3 Others

- 5.2 By Equipment / Trailer Type

- 5.2.1 Dry Van

- 5.2.2 Refrigerated Van

- 5.2.3 Flatbed / Step-Deck

- 5.2.4 Tanker (Bulk Liquid & Chemical)

- 5.2.5 Others

- 5.3 By Haul Length

- 5.3.1 Long-Haul (More than 500 miles)

- 5.3.2 Regional (100-500 miles)

- 5.3.3 Local (Less than 100 miles)

- 5.4 By Business Model

- 5.4.1 Traditional Freight Brokerage

- 5.4.2 Asset-Based Freight Brokerage

- 5.4.3 Agent Model Freight Brokerage

- 5.4.4 Digital Freight Brokerage

- 5.5 By End-User Industry

- 5.5.1 Manufacturing & Automotive

- 5.5.2 Construction & Infrastructure Projects

- 5.5.3 Oil, Gas, Mining & Chemicals

- 5.5.4 Agriculture & Food / Beverage

- 5.5.5 Retail, FMCG & Wholesale Distribution

- 5.5.6 Healthcare & Pharmaceuticals

- 5.5.7 E-commerce & 3PL Fulfilment

- 5.5.8 Other End-User Industry

- 5.6 By Customer Size

- 5.6.1 Large Enterprise Shippers (More than USD 100 M)

- 5.6.2 Mid-Market Shippers (USD 10-100 M)

- 5.6.3 Small Businesses (Less than USD 10 M)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)

- 6.4.1 DSV A/S (including DB Schenker)

- 6.4.2 DHL Group

- 6.4.3 Kuehne+Nagel

- 6.4.4 Rhenus Logistics

- 6.4.5 Hellmann Worldwide Logistics

- 6.4.6 Dachser

- 6.4.7 Sennder

- 6.4.8 Transporeon

- 6.4.9 C.H. Robinson

- 6.4.10 Yusen Logistics (Part of NYK Line)

- 6.4.11 GEODIS

- 6.4.12 Rohlig Logistics

- 6.4.13 Emo Trans

- 6.4.14 Trucksters

- 6.4.15 Fiege Logistics

- 6.4.16 Cargoline

- 6.4.17 System Alliance Europe

- 6.4.18 Carmovia

- 6.4.19 Ontruck

- 6.4.20 SLYNX

7 Market Opportunities and Future Outlook

- 7.1 White-Space and Unmet-Need Assessment