|

시장보고서

상품코드

2063308

프랑스의 화물 중개 서비스 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)France Freight Brokerage Services - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

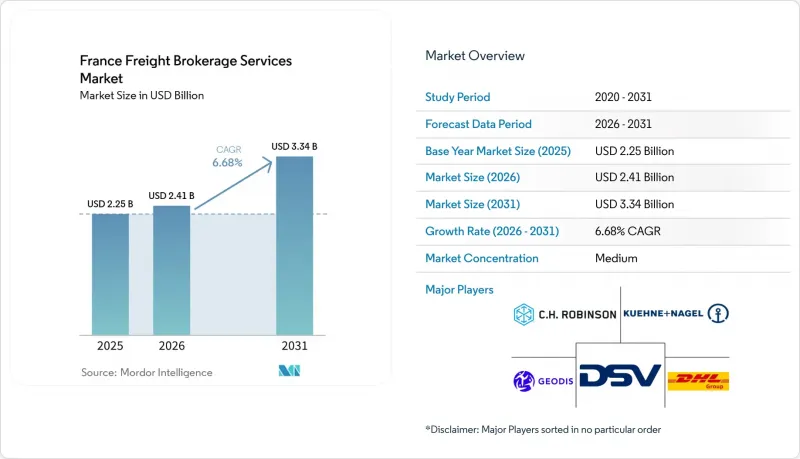

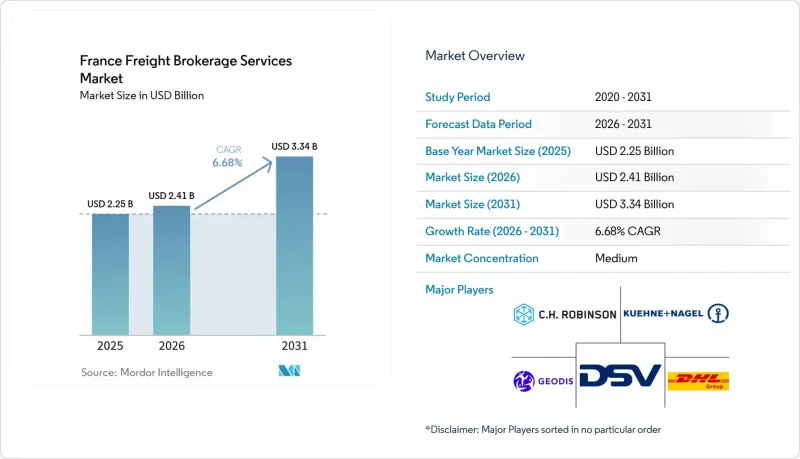

Mordor Intelligence에 의하면, 프랑스의 화물 중개 서비스 시장 규모는 2025년 22억 5,000만 달러로 평가되었고, 2026년에는 24억 1,000만 달러로 추정되고, 2031년까지 33억 4,000만 달러에 이를 것으로 예측되며, 2026-2031년 CAGR 6.68%로 성장할 전망입니다.

본 보고서는 서비스별(FTL, LTL), 차량별(건조 화물차, 냉장 화물차 등), 운송 거리별(장거리, 지역 내, 단거리), 사업 형태별(기존, 자산 보유형 등), 최종 사용자별(제조 및 자동차, 건설 등), 고객 규모별(대기업, 중견기업, 중소기업)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

프랑스의 화물 중개 서비스 시장 동향 및 분석

CSRD에 따른 공급망 가시화 의무화가 브로커 도입 촉진

CSRD는 2025년 1월부터 약 5만 개 기업에 대해 스코프 3 운송 배출량 공개를 의무화하고 있으며, 화주들은 ISO 14083 표준을 준수하는 탄소 데이터와 실시간 추적 서비스를 제공하는 업체와 제휴해야 하는 상황에 직면해 있습니다. 규정 위반에 따른 벌금과 연간 평균 120만 유로(142만 달러)에 달하는 보고 비용이, 자동화된 대시보드를 갖춘 브로커 업체로의 아웃소싱을 촉진하고 있습니다. 현재 프랑스의 다국적 기업들은 환경 보고를 조달 기준의 상위 3개 항목으로 꼽고 있으며, 중개업체들이 복잡한 감사 규정을 화주들이 쉽게 이해할 수 있는 간결한 인터페이스로 전환함에 따라 프랑스의 화물 중개 서비스 시장이 확대되고 있습니다. 이 지침의 역외 적용으로 인해 EU 역외공급업체도 동일한 보고 대상이 됨에 따라, 국경을 초월한 중개 서비스에 대한 수요가 확대되고 있습니다. 조기 도입 기업들은 블록체인을 활용한 배출량 계산 증명 및 기업 자원 계획(ERP) 시스템과의 API 연동을 통해 차별화를 꾀하고 있습니다.

도시형 집하 허브의 확대가 크로스 도킹 중개를 뒷받침하고 있습니다.

2026년까지 파리 15곳, 리옹 8곳에 설치될 마이크로 허브가 제로 배출 배송 구역에 물품을 공급하게 되며, 중개업체는 여러 화주로부터의 팔레트 적재 화물을 통합하여 트럭 적재율을 80-85%까지 높일 수 있게 됩니다. 이미 지자체 규제로 인해 주요 도심 지역에서는 3.5톤을 초과하는 유로 5 디젤 차량의 통행이 금지되어 있기 때문에 중개업체들은 부가가치가 높은 크로스도킹이나 시간 지정 배송 서비스에 대해 추가 요금을 청구하고 있습니다. 또한, 집하 센터는 배송 경로를 단축하고 라스트 마일 소요 시간을 30-40% 단축함으로써, 전자상거래 분야의 당일 배송 약속을 뒷받침하고 있습니다. 유럽투자은행 및 지방 자치단체의 공공 보조금은 민간 주도의 허브 투자에 따른 위험을 완화하고, 도시 지역의 LTL(소량 혼재) 중개 물동량을 더욱 증가시키고 있습니다.

중개 수수료의 투명성에 대한 독점금지법의 감시가 규정 준수 비용을 증가시킵니다.

EU 경쟁 당국은 현물 화물 시장에서 12-25%에 달하는 숨겨진 마진을 조사했으며, 중개업체들에게 운송업체에 지급하는 금액을 서비스 수수료에서 분리할 것을 요구하고 있습니다. 프랑스 경쟁 당국은 현재 내역이 명시된 청구서 발행을 의무화하고 있으며, 이로 인해 IT 시스템 업그레이드, 법적 검토, 고객 재교육이 불가피하게 되었고, 이 모든 요인이 중견 기업의 EBITDA를 압박하고 있습니다. 매출액의 최대 10%에 달할 수 있는 벌금은 리스크를 높여, 프랑스 화물 중개 서비스 시장의 지리적 확장과 기술 투자를 둔화시키고 있습니다.

부문별 분석

2031년까지 연평균 성장률(CAGR) 8.06%로 매출이 확대될 전망이며, 프랑스 화물 중개 서비스 시장 규모에서 소량 화물(LTL)이 차지하는 비중은 증가 추세를 보이고 있습니다. 한편, 2025년 시점에서도 풀 트럭 적재(FTL)가 여전히 57.53%의 점유율을 차지했습니다. 파리와 리옹 시내의 물류 허브는 LTL 트럭의 가동률을 높여, 전자상거래 사업자들을 유치하는 당일 배송 약속을 뒷받침하고 있습니다. 반면, FTL은 공장에서 창고까지 안정적인 운송 경로를 제공하고 있지만, 운전기사 부족과 보험료 급등으로 인한 압박에 직면해 있습니다.

AI를 활용한 화물 통합을 통해 LTL 매칭 시간이 3시간으로 단축되었으며, 정시 배송률이 향상되고 있습니다. FTL 간선 운송과 LTL 도시 내 운송을 결합한 하이브리드 솔루션은 부문 간의 경계를 모호하게 만들어, 중개업체가 번들 서비스를 추가 판매할 수 있도록 하고 있습니다. 위험물 및 초대형 화물을 위한 전문 서비스는 건설업과 화학 업계 수요에 힘입어, 틈새 시장임에도 불구하고 안정적인 시장을 유지하고 있습니다.

드라이 컨테이너는 프랑스 화물 중개 서비스 시장 규모의 40.68%를 차지하고 있지만, 백신 및 생물학적 제제의 운송량이 증가함에 따라 냉장 컨테이너 시장은 연평균 성장률(CAGR) 8.68%로 확대되고 있습니다. 1분기 건강 캠페인 기간 중 발생한 온도 관리형 운송 능력 부족으로 인해, 중개업체들은 15-20%의 할증료를 청구할 수 있었으며, 이는 프랑스 화물 중개 서비스 시장을 활성화시켰습니다. 트레일러에 장착된 IoT 센서가 압축기 고장을 감지함으로써 화물의 부패를 방지하고, 운송업체의 서비스 수준을 향상시키고 있습니다.

의약품 GDP(적정 보관 기준) 준수 및 엔드투엔드 시리얼화를 통해 가시성에 대한 수요가 높아짐에 따라, 중개업체들은 온도 관리의 무결성을 검증하는 블록체인 로그에 대한 투자를 확대되고 있습니다. 플랫베드와 탱커는 건설 및 화학제품 운송에 힘입어 안정적인 시장 점유율을 유지하고 있지만, 경기 순환의 영향을 쉽게 받기 때문에 시장 전체의 성장률에는 미치지 못하는 상황입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

AJY 26.06.22According to Mordor Intelligence, the france freight brokerage services market size is expected to increase from USD 2.25 billion in 2025 to USD 2.41 billion in 2026 and reach USD 3.34 billion by 2031, growing at a CAGR of 6.68% over 2026-2031.

This report is Segmented by Service (FTL, LTL), by Equipment (Dry Van, Refrigerated Van, and More), by Haul Length (Long-Haul, Regional, Local), by Business (Traditional, Asset-Based, and More), by End-User (Manufacturing/Automotive, Construction, and More), and by Customer Size (Large Enterprise, Mid-Market, Small Business). The Market Forecasts are Provided in Terms of Value (USD).

France Freight Brokerage Services Market Trends and Insights

Supply-Chain-Visibility Mandates Under CSRD Drive Broker Adoption

CSRD obliges around 50,000 companies to disclose Scope 3 transport emissions from January 2025, pushing shippers to partner with providers that deliver ISO 14083-aligned carbon data and real-time tracking. Compliance penalties and average annual reporting costs of EUR 1.2 million (USD 1.42 million) encourage outsourcing to brokers with automated dashboards. French multinationals now rank environmental reporting among their three top procurement criteria, expanding the France freight brokerage services market as brokers translate complex audit rules into simple shipper interfaces. The directive's extraterritorial reach draws non-EU suppliers into the same reporting net, enlarging cross-border brokerage demand. Early adopters differentiate through blockchain proofs of emission calculations and API connectivity with enterprise resource planning systems.

Expansion of Urban Consolidation Hubs Boosts Cross-Docking Brokerage

Fifteen micro-hubs in Paris and eight in Lyon feed zero-emission delivery zones by 2026, letting brokers aggregate palletized loads from multiple shippers and raise truck fill rates to 80-85%. Municipal rules already bar Euro 5 diesel above 3.5 tons from key downtown districts, so brokers charge premiums for value-added cross-docking and time-window services. Consolidation centers also shorten courier routes, lowering last-mile travel time by 30-40% and supporting same-day e-commerce commitments. Public grants from the European Investment Bank and local authorities de-risk private hub investment, further lifting urban LTL brokerage volumes.

Antitrust Scrutiny on Broker Fee Transparency Raises Compliance Costs

EU competition authorities probe hidden margins of 12-25% on spot loads, pressing brokers to unbundle carrier pay from service fees. The French Competition Authority now requires itemized invoices, forcing IT upgrades, legal reviews, and customer re-education that together trim EBITDA for mid-sized firms. Potential fines of up to 10% of revenue heighten risk, slowing geographic expansion and technology spending in the France freight brokerage services market.

Other drivers and restraints analyzed in the detailed report include:

- Hydrogen-Truck Subsidy Scheme Enlarges Green Capacity Pools

- Post-Brexit Digital Customs Clearance Stimulates Cross-Channel Brokerage Volumes

- Volatile Rail and EV-Truck Electricity Prices Erode Multimodal Cost Parity

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Less-than-truckload accounted for a rising slice of the France freight brokerage services market size as its revenue grows at 8.06% CAGR to 2031, while full-truckload still commands 57.53% share in 2025. Consolidation hubs inside Paris and Lyon lift LTL truck utilization and support same-day delivery promises that attract e-commerce merchants. In contrast, FTL serves steady factory-to-warehouse corridors but is pressured by driver shortages and higher insurance.

Improved load pooling through AI cuts LTL pairing time to three hours, enhancing on-time performance. Hybrid solutions that stitch an FTL trunk with LTL urban legs blur segment lines, enabling brokers to upsell bundled services. Specialized offerings for hazardous and oversized cargo remain niche but stable, anchored by construction and chemical demand.

Dry vans delivered 40.68% of the France freight brokerage services market size, yet refrigerated units expand at 8.68% CAGR as vaccine and biologic volumes climb. Temperature-controlled capacity shortages during Q1 health campaigns allowed brokers to charge 15-20% premiums, boosting the France freight brokerage services market. IoT probes in trailers now alert on compressor faults, cutting spoilage and raising carrier service levels.

GDP compliance and end-to-end serialization for medicines intensify demand for visibility, prompting brokers to invest in blockchain logs that verify temperature integrity. Flatbeds and tankers keep a steady share tied to construction and chemical shipments, while their growth lags the headline market due to cyclical exposure.

List of Companies Covered in this Report:

- DHL Group

- DSV

- Geodis

- C.H Robinson

- Kuehne + Nagel

- Sennder

- Upply

- FM Logistic

- Clicktrans

- Emo Trans

- Carmovia

- Alpega Teleroute

- Groupe CAT

- Transporeon

- B2PWeb

- Cocolis

- Fretlink

- Chronotruck

- FretBay

- Waygoo

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 Introduction

- 1.1 Study Assumptions & Market Definition

- 1.2 Scope of the Study

2 Research Methodology

3 Executive Summary

4 Market Landscape

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Supply-chain-visibility mandates under CSRD drive broker adoption

- 4.2.2 Expansion of urban consolidation hubs boosts cross-docking brokerage

- 4.2.3 Hydrogen-truck subsidy scheme ("H2 Mobility France") enlarges green capacity pools

- 4.2.4 Post-Brexit digital customs clearance stimulates cross-Channel brokerage volumes

- 4.2.5 AI-enabled dynamic-pricing engines improve load-matching efficiency

- 4.2.6 Circular-economy reverse-logistics flows create profitable backhaul lanes

- 4.3 Market Restraints

- 4.3.1 Antitrust scrutiny on broker fee transparency raises compliance costs

- 4.3.2 Volatile rail & EV-truck electricity prices erode multimodal cost parity

- 4.3.3 Escalating cyber-attacks on freight platforms dampen shipper trust

- 4.3.4 Spike in carrier insurance premiums tightens independent-haulage capacity

- 4.4 Value / Supply-Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces

- 4.7.1 Bargaining Power of Buyers

- 4.7.2 Bargaining Power of Suppliers

- 4.7.3 Threat of New Entrants

- 4.7.4 Threat of Substitutes

- 4.7.5 Competitive Rivalry

5 Market Size & Growth Forecasts

- 5.1 By Service

- 5.1.1 Full-Truckload (FTL)

- 5.1.2 Less-than-Truckload (LTL)

- 5.1.3 Others

- 5.2 By Equipment / Trailer Type

- 5.2.1 Dry Van

- 5.2.2 Refrigerated Van

- 5.2.3 Flatbed / Step-Deck

- 5.2.4 Tanker (Bulk Liquid & Chemical)

- 5.2.5 Others

- 5.3 By Haul Length

- 5.3.1 Long-Haul (More than 500 miles)

- 5.3.2 Regional (100-500 miles)

- 5.3.3 Local (Less than 100 miles)

- 5.4 By Business Model

- 5.4.1 Traditional Freight Brokerage

- 5.4.2 Asset-Based Freight Brokerage

- 5.4.3 Agent Model Freight Brokerage

- 5.4.4 Digital Freight Brokerage

- 5.5 By End-User Industry

- 5.5.1 Manufacturing & Automotive

- 5.5.2 Construction & Infrastructure Projects

- 5.5.3 Oil, Gas, Mining & Chemicals

- 5.5.4 Agriculture & Food / Beverage

- 5.5.5 Retail, FMCG & Wholesale Distribution

- 5.5.6 Healthcare & Pharmaceuticals

- 5.5.7 E-commerce & 3PL Fulfilment

- 5.5.8 Other End-User Industry

- 5.6 By Customer Size

- 5.6.1 Large Enterprise Shippers (More than USD 100 M)

- 5.6.2 Mid-Market Shippers (USD 10-100 M)

- 5.6.3 Small Businesses (Less than USD 10 M)

6 Competitive Landscape

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles {(includes Global level Overview, Market level overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share for key companies, Products & Services, and Recent Developments)}

- 6.4.1 DHL Group

- 6.4.2 DSV

- 6.4.3 Geodis

- 6.4.4 C.H Robinson

- 6.4.5 Kuehne + Nagel

- 6.4.6 Sennder

- 6.4.7 Upply

- 6.4.8 FM Logistic

- 6.4.9 Clicktrans

- 6.4.10 Emo Trans

- 6.4.11 Carmovia

- 6.4.12 Alpega Teleroute

- 6.4.13 Groupe CAT

- 6.4.14 Transporeon

- 6.4.15 B2PWeb

- 6.4.16 Cocolis

- 6.4.17 Fretlink

- 6.4.18 Chronotruck

- 6.4.19 FretBay

- 6.4.20 Waygoo

7 Market Opportunities & Future Outlook

- 7.1 White-space & Unmet-need Assessment