|

시장보고서

상품코드

2063402

유럽의 전사적 자원 계획(ERP) : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe Enterprise Resource Planning - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

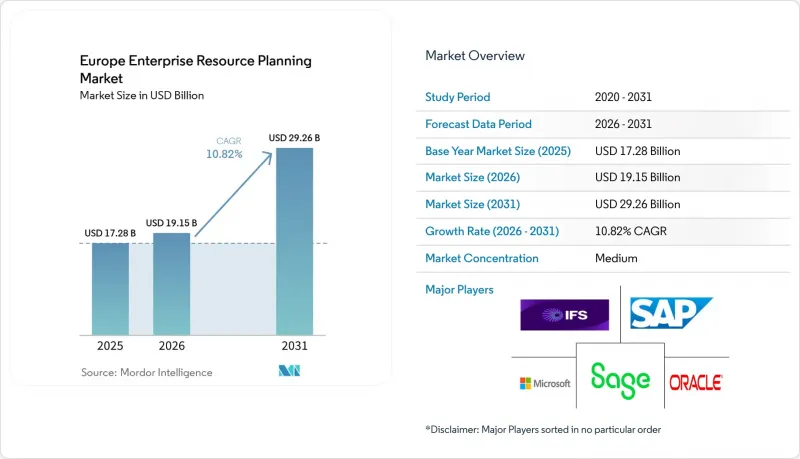

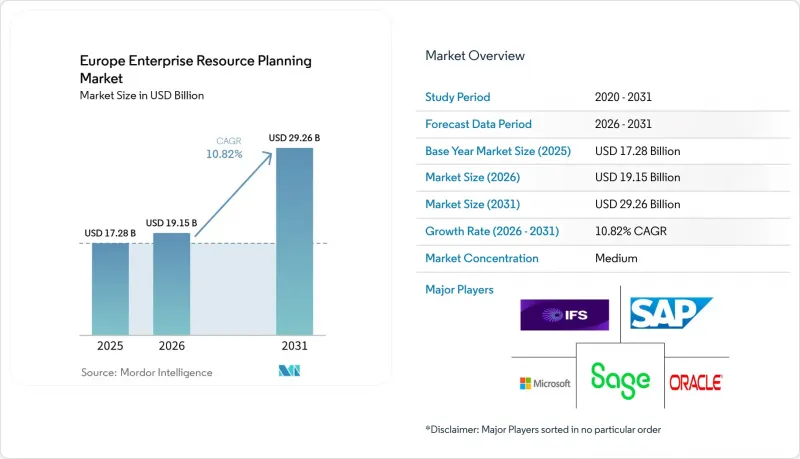

Mordor Intelligence에 의하면, 유럽의 전사적 자원 계획(ERP) 시장 규모는 2025년 172억 8,000만 달러로 평가되었습니다. 2026년에는 191억 5,000만 달러로 확대되어 2026-2031년에 걸쳐 CAGR 10.82%로 성장을 지속하여, 2031년까지 292억 6,000만 달러에 이를 것으로 예측됩니다.

본 보고서는 아키텍처(클라우드 네이티브 제품군, 모바일 퍼스트 ERP, 기타), 부문(재무 및 회계, 기타), 배포 모델(On-Premise, 클라우드), 조직 규모(대기업, 중소기업), 업종(제조업, 은행, 금융서비스 및 보험(BFSI), 기타), 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 전사적 자원 계획(ERP) 시장 동향 및 인사이트

클라우드 ERP 솔루션으로의 전환

클라우드 전환은 하드웨어 의존도가 높은 도입 환경을, 지출과 수요의 주기를 일치시키는 종량제 구독 모델로 전환함으로써 유럽의 기업 자원 계획(ERP) 시장의 비용 구조를 재정의하고 있습니다. SAP의 RISE 프로그램과 Microsoft Dynamics 365 클라우드 제품군의 기록적인 성장은 예측 가능한 운영 비용을 추구하는 CFO들에게 매력적인 ‘사용량 기반 경제’로의 전면적인 전환을 뒷받침하고 있습니다. 유럽의 소버린 클라우드 리전이 가동됨에 따라 데이터 소재지에 대한 우려가 해소되어, 공공 행정 및 의료 등 규제 대상 분야에 진출할 수 있게 되었습니다. 사용자 그룹의 조사 결과, 2023년부터 2025년에 걸쳐 S/4HANA 클라우드 도입 규모가 두 배로 늘어남에 따라, 중견 제조업체들의 도입이 가속화되고 있습니다. 유럽의 ERP 시장에서는 각 벤더사가 고정 가격의 전환 패키지를 제공하고 있으며, 이를 통해 프로젝트 기간이 단축되고 예산 초과 위험이 줄어들기 때문에 위험 회피 성향이 강한 산업 그룹조차도 레거시 시스템 폐지에 나서고 있습니다.

AI와 고급 분석의 통합

생성형 AI는 시범 운영 단계에서 본격적인 운영 단계로 전환되었으며, 조달, 재무, 인사 각 모듈에 대화형 코파일럿이 도입되었습니다. 조기 도입 기업에서는 인사이트를 얻는 데 걸리는 시간과 수작업에 의한 대조 작업을 약 절반으로 줄임으로써, 차세대 ERP 제품군의 가치 제안을 강화하고 있습니다. 유럽의 제조업체들은 예측 모델을 활용해 공급망의 충격을 시뮬레이션함으로써, 관세나 물류 혼란에 대비한 선제적인 재고 배치를 가능하게 하고 있습니다. 각 벤더사는 유럽의 AI 법규를 준수하기 위해 투명성이 높은 감사 추적을 도입하고, 채용 평가 점수 산정 등 고위험 기능에 대해서도 설명이 가능하고 사람이 직접 관리할 수 있도록 보장하고 있습니다. 이러한 AI의 급속한 도입은 사용자의 생산성을 높이고, 라이선스 업그레이드를 촉진하며, 유럽의 전사적 자원 관리(ERP) 시장을 디지털 운영 모델의 핵심으로 확고히 자리매김하고 있습니다.

높은 이전 및 통합 비용

복잡하고 다양한 맞춤 설정이 가능한 기존 시스템 환경은 기업이 최신 플랫폼으로 전환할 때 예산을 부풀리게 하며, 데이터 정제, 인터페이스 재작성, 병행 운영 기간 등을 포함하면 당초 견적의 2배가 되는 경우도 드물지 않습니다. 희소한 SAP 및 Oracle 기술에 대한 컨설팅 비용은 시간당 500달러를 초과하여, 중견 제조업체의 자본 배분에 부담을 주고 있습니다. 고정 가격의 전환형 상품이나 크레딧이 포함된 클라우드 서비스는 재무적 위험을 완화해 주지만, 이를 완전히 제거해 주지는 않습니다. 따라서 규제 산업에서는 비즈니스 타당성이 확실해질 때까지 프로젝트를 연기하는 움직임이 나타나고 있으며, 이것이 유럽의 ERP 시장에 단기적인 걸림돌이 되고 있습니다.

부문별 분석

클라우드 네이티브 제품군은 2025년 지출의 41.78%를 차지하며, 실시간 분석 및 자동 패치 적용의 핵심으로 자리매김했습니다. 벤더는 업무 중단 없이 AI 기능을 추가하는 월간 업데이트를 출시하고 있으며, 이를 통해 사용자들은 항상 최신 기능을 이용할 수 있을 것으로 기대하고 있습니다. 연평균 성장률(CAGR) 9.65%로 성장하고 있는 모바일 우선 플랫폼은 현장 기술자나 창고 피킹 담당자에게 연결이 복구되는 순간 즉시 동기화되는 오프라인 지원 앱을 제공하고 있으며, 이 기능은 현재 유틸리티 및 물류 산업의 분산된 인력에게 필수적인 요소로 자리 잡고 있습니다. IFS Cloud Mobile 및 유사한 솔루션들은 엣지 캐시가 예기치 못한 가동 중지 시간을 줄이고 재고 회전율을 높이는 것으로 입증되어, 시장 점유율의 점진적인 증가에 기여하고 있습니다.

다국적 기업들이 자회사에는 경량 클라우드 시스템을 도입하는 한편, 핵심 재무 시스템은 엄격한 관리 하에 있는 스택에 남겨두는 이중 계층 아키텍처가 점차 보급되고 있습니다. 이러한 접근 방식은 현지의 민첩성과 본사의 감독 기능 간의 균형을 맞추고 있습니다. 공장 현장의 엣지 대응 ERP 유닛은 로봇 및 검사 카메라의 운영을 밀리초 단위로 조정하고, 집계된 지표를 클라우드상의 상위 시스템으로 전송합니다. 이 하이브리드형 패턴은 품질 관리 루프를 강화하고 인더스트리 4.0의 요구 사항을 준수함으로써, 유럽 ERP 시장에서 벤더 종속성을 더욱 공고히 하고 있습니다.

재무 및 회계 모듈은 2025년 매출의 28.67%를 차지하며, 27개 세제를 아우르는 법정 기록 시스템과 감사의 일관성을 지키는 ‘게이트키퍼’로서의 역할을 강조했습니다. 지속적인 결산 처리, 자동화된 대조, 내장형 분석을 통해 사이클 타임이 단축되어 재무 팀은 부가가치가 높은 분석에 집중할 수 있게 됩니다. 소매업체들이 전자상거래, 주문 조정, 서비스 참여를 단일 데이터 모델로 통합함에 따라, 고객 관계 관리 및 상거래 모듈 시장은 연평균 성장률(CAGR) 8.85%로 확대되고 있습니다. 실시간 재고 배분과 동적 가격 책정은 지정학적 요인으로 인한 공급 충격 시 이익률 보호를 도모하는 동시에 고객 경험을 향상시킵니다.

공급망 솔루션은 여전히 미션 크리티컬한 역할을 수행하며, 홍해나 철도의 병목 현상에 대응하여 화물 운송 경로와 대체 공급업체의 조합을 시뮬레이션합니다. 인적 자본 관리 솔루션은 사내 인력과 프로젝트 수요를 매칭하는 AI 기반 기술 온톨로지를 통해 차별화를 꾀함으로써, 지역별 인력 부족 문제를 완화합니다. 제조 실행 및 품질 관리 모듈에는 전자 배치 기록 기능이 통합되어 있어, GMP 감사 요건을 충족할 뿐만 아니라 업스트림 단계의 지속가능성 정보 공개로 이어지는 상세한 데이터를 제공함으로써, 유럽의 기업 자원 계획(ERP) 시장에서 다중 모듈 도입을 정착시키고 있습니다.

기타 혜택

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the europe enterprise resource planning market size is expected to grow from USD 17.28 billion in 2025 to USD 19.15 billion in 2026 and is forecast to reach USD 29.26 billion by 2031 at a 10.82% CAGR over 2026-2031.

This report is Segmented by Architecture (Cloud-Native Suite, Mobile-First ERP, and More), Business Function (Finance and Accounting, and More), Deployment Model (On-Premise, and Cloud), Organization Size (Large Enterprises, and Small and Medium Enterprises), Industry Vertical (Manufacturing, BFSI, and More), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

Europe Enterprise Resource Planning Market Trends and Insights

Shift to Cloud ERP Solutions

Cloud migration is redefining the cost profile of the European enterprise resource planning market by converting hardware-heavy installations into pay-as-you-go subscriptions that match expenditure with demand cycles. Record growth in SAP's RISE program and Microsoft Dynamics 365 cloud suites underscores a wholesale pivot toward consumption economics that appeal to finance chiefs seeking predictable operating costs. The availability of European sovereign cloud regions calms residency concerns and unlocks regulated sectors such as public administration and healthcare. Mid-market manufacturers are accelerating adoption after user-group surveys confirmed a doubling of S/4HANA cloud footprints between 2023 and 2025. In the Europe ERP market, vendors package fixed-price migration bundles that compress project timelines and de-risk budget overruns, encouraging even risk-averse industrial groups to retire legacy estates.

Integration of AI and Advanced Analytics

Generative AI is moving from pilot to production, placing conversational copilots within procurement, finance, and human resources modules. Early adopters reduce time-to-insight and manual reconciliations by roughly half, strengthening the value proposition of next-generation ERP suites. European manufacturers use predictive models to simulate supply-chain shocks, enabling proactive stock positioning in response to tariff or logistics disruptions. Vendors embed transparent audit trails to comply with the European AI Act, ensuring high-risk functions, such as recruitment scoring, remain explainable and human-governed. This rapid infusion of AI raises user productivity, drives licence upgrades, and cements the Europe enterprise resource planning market as a centerpiece of digital operating models.

High Migration and Integration Costs

Complex, customization-rich estates inflate budgets when enterprises shift to modern platforms, often doubling initial estimates once data cleansing, interface rewrites, and dual-running periods are included. Consulting fees for scarce SAP and Oracle skills have climbed above USD 500 per hour, squeezing capital allocation at mid-market manufacturers. Fixed-price migration bundles and credit-backed cloud offers temper, but do not eliminate, financial risk, prompting regulated industries to defer projects until business-case certainty firms up and feeding a near-term drag on the Europe ERP market.

Other drivers and restraints analyzed in the detailed report include:

- Regulatory Mandates on Data Privacy (GDPR, NIS2)

- SME Uptake Through EU Recovery and Resilience Facility

- Data-Sovereignty and Residency Concerns

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Cloud-native suites captured 41.78% of 2025 spending, establishing themselves as the control tower for real-time analytics and automated patching. Vendors release monthly updates that add AI features without disrupting operations, raising user expectations for evergreen functionality. Mobile-first platforms, expanding at a 9.65% CAGR, equip field technicians and warehouse pickers with offline-capable apps that sync the moment connectivity returns, a capability now central to distributed workforces across utilities and logistics. IFS Cloud Mobile and similar offerings demonstrate how edge caching cuts unplanned downtime and accelerates inventory turns, contributing incremental share gains.

Two-tier architectures gain traction as multinationals deploy lightweight cloud systems at subsidiaries while core financials remain on high-control stacks, an approach that balances local agility with headquarters oversight. Edge-enabled ERP units on factory floors orchestrate millisecond-level operations for robots and inspection cameras, then feed aggregated metrics to the cloud parent. This hybrid pattern tightens quality loops and conforms to Industrie 4.0 mandates, strengthening vendor lock-in within the Europe enterprise resource planning market.

Finance and accounting modules accounted for 28.67% of 2025 revenue, underscoring their role as statutory systems of record and gatekeepers of audit integrity across 27 tax regimes. Continuous close, automated reconciliation, and embedded analytics reduce cycle times and free finance teams for value-add analysis. Customer relationship and commerce modules are advancing at an 8.85% CAGR as retailers stitch together e-commerce, order orchestration, and service engagement in a single data model. Real-time inventory allocations and dynamic pricing drive margin protection during geopolitical supply shocks while enhancing customer experience.

Supply-chain suites remain mission-critical, simulating freight corridors and alternative supplier mixes in response to Red Sea or rail bottlenecks. Human capital management solutions differentiate via AI-driven skills ontologies that match internal talent with project demand, alleviating regional labor shortages. Manufacturing execution and quality modules embed electronic batch records, satisfying GMP audits and delivering granularity that flows upstream into sustainability disclosures, anchoring multi-module adoption inside the European enterprise resource planning market.

List of Companies Covered in this Report:

- SAP SE

- Microsoft Corporation

- Oracle Corporation

- Unit4 N.V.

- IFS AB

- Infor Inc.

- Sage Group Plc

- Workday Inc.

- SYSPRO (Pty) Ltd.

- Acumatica Inc.

- Ramco Systems Ltd.

- Visma AS

- Epicor Software Corporation

- QAD Inc.

- Cetek ERP LLC

- Abas Software GmbH

- Deltek Inc.

- Priority Software Ltd.

- Exact Holding B.V.

- Odoo S.A.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Shift to Cloud ERP Solutions

- 4.2.2 Integration of AI and Advanced Analytics

- 4.2.3 Regulatory Mandates on Data Privacy (GDPR, NIS2)

- 4.2.4 SME Uptake Through EU Recovery and Resilience Facility

- 4.2.5 Across Carbon-Accounting Requirements Supply Chains

- 4.2.6 Edge-Based ERP for Real-Time Manufacturing Control

- 4.3 Market Restraints

- 4.3.1 High Migration and Integration Costs

- 4.3.2 Data-Sovereignty and Residency Concerns

- 4.3.3 Shortage of ERP-Specialised Talent in Europe

- 4.3.4 Energy-Price Volatility Pressuring IT Budgets

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Architecture

- 5.1.1 Cloud-Native Suite

- 5.1.2 Mobile-First ERP

- 5.1.3 Social / Collaborative ERP

- 5.1.4 Two-Tier / Edge ERP

- 5.2 By Business Function

- 5.2.1 Finance and Accounting

- 5.2.2 Supply-Chain and Operations

- 5.2.3 Human Capital Management

- 5.2.4 Customer Relationship and Commerce

- 5.2.5 Manufacturing Execution and Quality

- 5.3 By Deployment Model

- 5.3.1 On-Premise

- 5.3.2 Cloud

- 5.4 By Organization Size

- 5.4.1 Large Enterprises

- 5.4.2 Small and Medium Enterprises

- 5.5 By Industry Vertical

- 5.5.1 Manufacturing

- 5.5.2 Retail and E-commerce

- 5.5.3 BFSI

- 5.5.4 Government and Public Sector

- 5.5.5 IT and Telecom

- 5.5.6 Healthcare and Life Sciences

- 5.5.7 Other Industry Verticals

- 5.6 By Geography

- 5.6.1 United Kingdom

- 5.6.2 Germany

- 5.6.3 France

- 5.6.4 Italy

- 5.6.5 Spain

- 5.6.6 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 SAP SE

- 6.4.2 Microsoft Corporation

- 6.4.3 Oracle Corporation

- 6.4.4 Unit4 N.V.

- 6.4.5 IFS AB

- 6.4.6 Infor Inc.

- 6.4.7 Sage Group Plc

- 6.4.8 Workday Inc.

- 6.4.9 SYSPRO (Pty) Ltd.

- 6.4.10 Acumatica Inc.

- 6.4.11 Ramco Systems Ltd.

- 6.4.12 Visma AS

- 6.4.13 Epicor Software Corporation

- 6.4.14 QAD Inc.

- 6.4.15 Cetek ERP LLC

- 6.4.16 Abas Software GmbH

- 6.4.17 Deltek Inc.

- 6.4.18 Priority Software Ltd.

- 6.4.19 Exact Holding B.V.

- 6.4.20 Odoo S.A.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment