|

시장보고서

상품코드

2063670

북미의 LED 칩 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)North America LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

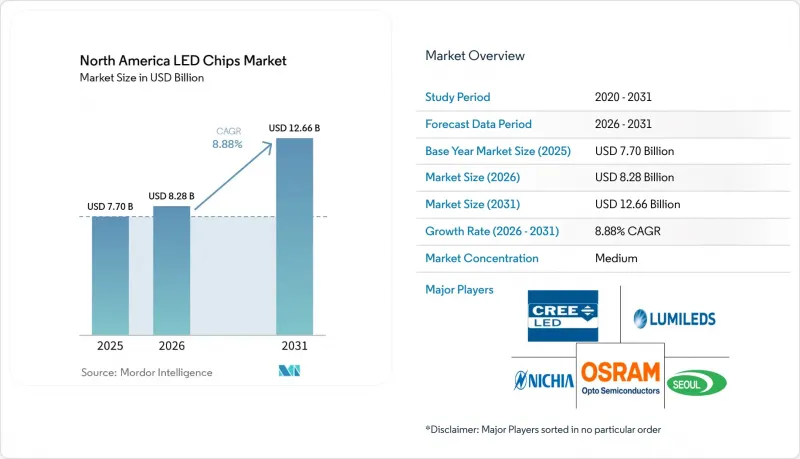

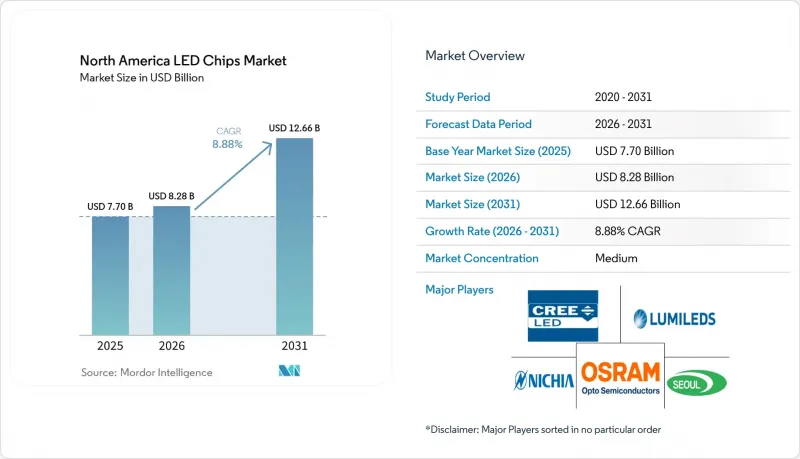

Mordor Intelligence에 의하면, 북미 LED 칩 시장 규모는 2025년 77억 달러, 2026년 82억 8,000만 달러에서 2031년까지 126억 6,000만 달러로 확대되어 2026년부터 2031년까지 연평균 복합 성장률(CAGR)은 8.88%를 나타낼 것으로 예측됩니다.

본 보고서는 LED 칩 기술(기존 LED, Mini-LED 등), 반도체 소재(GaN/InGaN, AlGaInP 등), 용도(일반 조명, 자동차, 백라이트/디스플레이, 소비자용 전자기기 등) 및 국가(미국, 캐나다 등)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

북미 LED 칩 시장 동향과 인사이트

상업용 부동산에서 에너지 절약형 조명에 대한 수요 증가

유틸리티 프로그램에 따라 2026년에는 평균 규정 조명 인센티브가 17% 인상되었으며, 주차장 및 월팩 등 실외 부문에서는 30%가 넘는 증가율을 기록했습니다. 섹션 179D의 세액 공제는 현행 임금 요건을 충족하는 프로젝트의 경우 현재 1제곱피트당 최대 5.81달러에 달하며, 이로 인해 기본 세제 혜택이 5배로 늘어나 리모델링 공사의 내부수익률이 향상되고 있습니다. 설치 후 모니터링 결과에 따르면, 창고 개보수를 통해 조명 에너지 사용량을 40-65% 절감할 수 있으며, 24시간 365일 가동되는 시설의 경우 18개월 이내에 투자 회수가 가능한 것으로 나타났습니다. 또한 1세대 LED 조명 기구의 수명이 다해감에 따라 교체용 칩에 대한 지속적인 수요가 촉진되고 있습니다. LED에서 LED로의 업그레이드를 명시적으로 허용하는 프로그램이 늘어나면서, 신축 공사가 주춤하는 시기임에도 불구하고 북미 LED 칩 시장은 호황을 누리고 있습니다. 고효율 청색 다이오드와 수명이 긴 적색 형광체 블렌드를 공급하는 제조업체는 이 두 번째 개선 주기를 포착하는 데 있어 가장 유리한 입장에 있습니다.

지능형 가로등을 활용한 스마트 시티 프로젝트의 확대

멤피스시는 77,000개의 조명 기구를 네트워크 제어 기능이 탑재된 LED 조명으로 교체하는 4,700만 달러 규모의 프로젝트를 완료하여, 연간 3,700만 kWh의 에너지 절감과 2만 6,000메트르톤의 온실가스 배출 감축을 달성했습니다. LEOTEK과 1NCE는 지자체 입장에서 로밍의 복잡성을 해소하고 국경을 초월한 확장을 가속화할 수 있는 즉시 사용 가능한 셀룰러 IoT 플랫폼을 출시했습니다. 보스턴, 시러큐스, 그리고 미시간주의 유틸리티 관할 구역에서 초기 도입이 진행되고 있습니다. 교통, 대기질, 공공 Wi-Fi 센서를 조명 기구에 통합함으로써 각 도시는 가로등 네트워크를 수익을 창출하는 데이터 플랫폼으로 전환하고 있습니다. 이러한 다기능 조명 기구에는 전류 균일성과 순방향 전압의 일관성을 확보하기 위해 엄격한 비닝 처리가 적용된 LED 칩이 필요하며, 이것이 북미 LED 칩 시장의 평균 판매 가격 상승을 부추기고 있습니다. 또한, 5일 이내 수리를 보장하는 성능 기반 유지보수 계약은 수직 통합된 서비스 네트워크를 보유한 공급업체에 유리하게 작용하고 있습니다.

MOCVD 장비 공급망 차질

AIXTRON과 Veeco Instruments는 전 세계 MOCVD 반응기의 약 3분의 2를 공급하고 있으며, 싱글 챔버 장비의 가격은 150만-300만 달러입니다. 정밀 질량 유량 제어기 및 진공 서브시스템의 부품 부족으로 인해 납기 기간이 18개월 이상으로 늘어났으며, 애리조나주와 온타리오주에서 계획되었던 웨이퍼 생산 능력 확충이 지연되고 있습니다. 중고 리액터가 중고 시장에서 가끔 나오기는 하지만, 구형 장비를 200mm GaN 공정에 대응시키려면 고가의 업그레이드 키트가 필요합니다. 인피니온은 지난해 유럽에서 최초로 가동된 300mm GaN 파워 웨이퍼 라인을 시연하며, 이에 따른 규모의 경제성을 부각시켰습니다. 장비 납기 지연이 계속된다면, 북미의 팹은 아시아의 경쟁사들에 뒤처질 위험이 있으며, 북미 LED 칩 시장의 성장 속도는 둔화될 것입니다.

부문별 분석

2025년, 북미 LED 칩 시장 점유율의 83.77%를 기존 방식의 디바이스가 차지하고 있으며, 일반 조명 및 간판 용도에서 백색 LED의 비용 경쟁력이 두드러지고 있습니다. 마이크로 LED 칩은 생산량이 극히 일부에 그치지만, 스마트 워치 디스플레이, 자동차의 필러 투 필러 디스플레이, 증강현실(AR) 헤드셋 등을 배경으로 연평균 성장률(CAGR) 11.32%를 기록하며 성장하고 있습니다. 가민사는 2026년에 출시 예정인 플래그십 멀티스포츠 워치에 1.39인치 마이크로 LED 패널을 채택했습니다. 그 이유로 햇빛 아래에서의 가시성과 20일간의 배터리 사용 시간을 꼽고 있습니다. VueReal사의 대량 인쇄 방식을 통해 온타리오주는 이러한 웨어러블 기기공급 거점으로서의 입지를 확고히 하고 있습니다.

기존 LED 제조업체들은 고반사율 리드 프레임이나 하이브리드 광학 시스템과 같은 패키지 기술의 혁신을 통해 시장 점유율을 유지하고 있으며, 이를 통해 발광 효율을 220 lm/W 이상으로 높이고 있습니다. 그러나 직접 발광형 픽셀이 색상 편차로 인한 아티팩트를 제거하고, 헤드업 디스플레이에서 3,000니트를 넘는 최대 휘도를 구현함에 따라, 향후 프리미엄 시장의 성장은 마이크로 LED 쪽으로 기울고 있습니다. 파일럿 라인에서 마이크로 LED의 전사 수율이 99.9%를 넘어서면, 이 기술은 2031년까지 북미 LED 칩 시장의 10%를 차지할 가능성이 있으며, 반면 미니 LED는 하이엔드 TV 백라이트 시장에서 중위권을 차지하게 될 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the north america lED chips market size is projected to expand from USD 7.70 billion in 2025 and USD 8.28 billion in 2026 to USD 12.66 billion by 2031, registering a CAGR of 8.88% between 2026 and 2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and More), Semiconductor Material (GaN/InGaN, Algainp, and More), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and More), and Country (United States, Canada, and More). The Market Forecasts are Provided in Terms of Value (USD).

North America LED Chips Market Trends and Insights

Growing Demand for Energy-Efficient Lighting in Commercial Real Estate

Utility programs raised average prescriptive lighting incentives by 17% in 2026, with outdoor categories such as parking garages and wall packs exceeding 30% increases. Section 179D deductions now reach up to USD 5.81 per square foot for projects that satisfy prevailing-wage requirements, multiplying the base tax benefit by 5 and boosting retrofit internal rates of return. Post-installation monitoring shows that warehouse retrofits can cut lighting energy use by 40-65% and achieve payback in less than 18 months for 24/7 facilities, stimulating recurring demand for replacement chips as first-generation LED luminaires approach end-of-life. The increase in programs that explicitly allow LED-to-LED upgrades keeps the North America LED chips market vibrant even in periods of slower new construction. Manufacturers that supply high-efficacy blue dies and long-lifetime red phosphor blends are best positioned to capture this second retrofit cycle.

Expansion of Smart City Projects with Intelligent Street Lighting

Memphis completed a USD 47 million conversion of 77,000 luminaires to LED fixtures with networked controls, delivering annual energy savings of 37 million kWh and reducing greenhouse-gas emissions by 26,000 metric tons. LEOTEK and 1NCE launched an out-of-the-box cellular-IoT platform that removes roaming complexity for municipalities and accelerates cross-border deployments, with initial rollouts in Boston, Syracuse, and Michigan utility territories. By embedding traffic, air-quality, and public-Wi-Fi sensors into luminaires, cities convert street-lighting grids into revenue-generating data platforms. These feature-rich fixtures require LED chips with strict binning for current uniformity and forward-voltage alignment, which are driving average selling prices higher in the North America LED chips market. Performance-based maintenance agreements that guarantee five-day repair times also favor suppliers with vertically integrated service networks.

Supply Chain Disruptions for MOCVD Equipment

AIXTRON and Veeco Instruments supply about two-thirds of global MOCVD reactors, and single-chamber tools cost USD 1.5-3 million. Component shortages for precision mass-flow controllers and vacuum subsystems have stretched deliveries beyond 18 months, delaying planned wafer-capacity additions in Arizona and Ontario. While secondary markets occasionally free up used reactors, retrofitting older tools to run 200 mm GaN processes requires expensive upgrade kits. Infineon demonstrated the first operational 300 mm GaN power wafer line in Europe last year, highlighting the scale economies at stake. North American fabs risk falling behind Asian competitors if equipment delays persist, moderating the expansion rate of the North America LED chips market.

Other drivers and restraints analyzed in the detailed report include:

- Automotive OEM Shift Toward Advanced Headlamp Technologies

- Surging Mini-LED Backlight Adoption in High-End TVs and Monitors

- Thermal Management Challenges in High-Power Chips

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional devices captured 83.77% of the North America LED chip market share in 2025, underscoring white LEDs' cost leadership in general lighting and signage deployments. Micro-LED dies, although a fraction of volume, are advancing at an 11.32% CAGR on the back of smartwatch faces, automotive pillar-to-pillar displays, and augmented-reality headsets. Garmin selected a 1.39-inch micro-LED panel for its flagship multisport watch, set to debut in 2026, citing sunlight readability and 20-day battery life. VueReal's mass-printing approach positions Ontario as a supply node for these wearables.

Conventional LED makers defend their market share through package innovations, such as high-reflectivity lead frames and hybrid optics, that push efficacy above 220 lm W-1. Yet future premium growth tilts toward micro-LED because direct-emissive pixels eliminate color-shift artifacts and deliver peak brightness exceeding 3,000 nits in head-up displays. As micro-LED transfer yields improve beyond 99.9% in pilot lines, the technology could command 10% of the North America LED chip market by 2031, with mini-LED occupying the middle tier for high-end television backlights.

List of Companies Covered in this Report:

- Cree LED, Inc.

- Lumileds Holding B.V.

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Samsung Electronics Co., Ltd.

- Epistar Corporation

- San'an Optoelectronics Co., Ltd.

- LG Innotek Co., Ltd.

- Bridgelux, Inc.

- Everlight Electronics Co., Ltd.

- Luminus Devices, Inc.

- Citizen Electronics Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Broadcom Inc.

- Rohm Semiconductor

- Kingbright Electronic Co., Ltd.

- Coherent Corp.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Growing Demand for Energy-Efficient Lighting in Commercial Real Estate

- 4.2.2 Expansion of Smart City Projects with Intelligent Street Lighting

- 4.2.3 Automotive OEM Shift Toward Advanced Headlamp Technologies

- 4.2.4 Surging Mini-LED Backlight Adoption in High-End TVs and Monitors

- 4.2.5 Rising Investments in North America Micro-LED Pilot Lines

- 4.2.6 UVC LED Retrofit Programs for Indoor Air Disinfection

- 4.3 Market Restraints

- 4.3.1 Supply Chain Disruptions for MOCVD Equipment

- 4.3.2 Patent Litigations Increasing Royalty Costs

- 4.3.3 Thermal Management Challenges in High-Power Chips

- 4.3.4 Limited Gallium Nitride Wafer Availability

- 4.4 Industry Supply-Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Country

- 5.4.1 United States

- 5.4.2 Canada

- 5.4.3 Mexico

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Cree LED, Inc.

- 6.4.2 Lumileds Holding B.V.

- 6.4.3 Nichia Corporation

- 6.4.4 OSRAM Opto Semiconductors GmbH

- 6.4.5 Seoul Semiconductor Co., Ltd.

- 6.4.6 Samsung Electronics Co., Ltd.

- 6.4.7 Epistar Corporation

- 6.4.8 San'an Optoelectronics Co., Ltd.

- 6.4.9 LG Innotek Co., Ltd.

- 6.4.10 Bridgelux, Inc.

- 6.4.11 Everlight Electronics Co., Ltd.

- 6.4.12 Luminus Devices, Inc.

- 6.4.13 Citizen Electronics Co., Ltd.

- 6.4.14 Toyoda Gosei Co., Ltd.

- 6.4.15 Broadcom Inc.

- 6.4.16 Rohm Semiconductor

- 6.4.17 Kingbright Electronic Co., Ltd.

- 6.4.18 Coherent Corp.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment