|

시장보고서

상품코드

2063853

아시아태평양의 LED 칩 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Asia Pacific LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

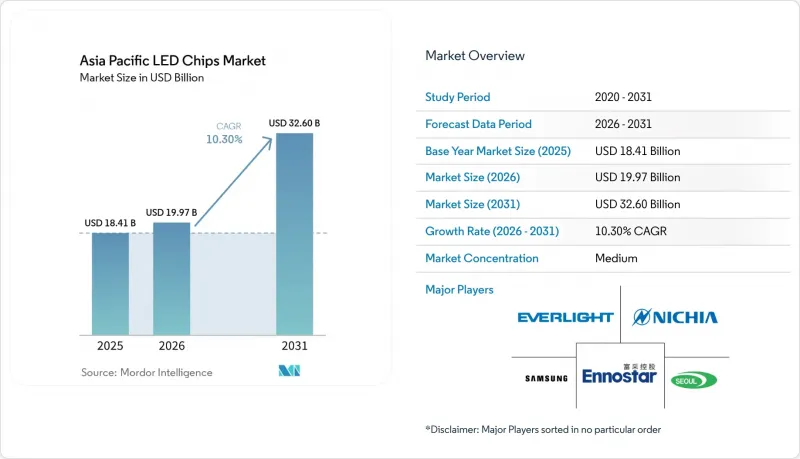

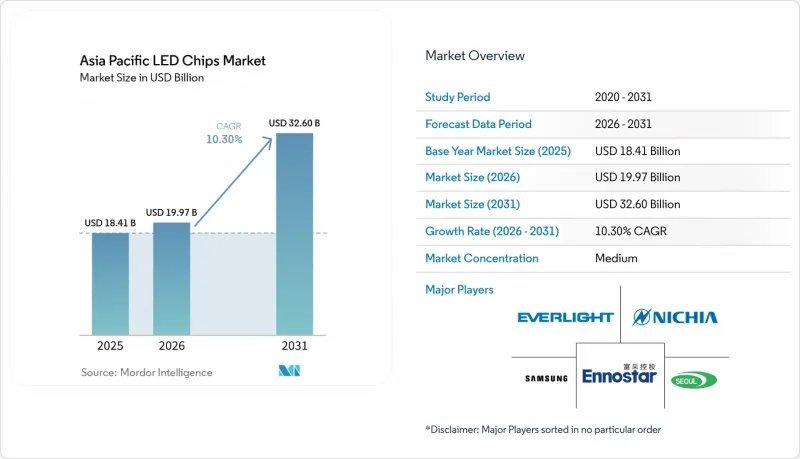

Mordor Intelligence에 의하면, 아시아태평양의 LED 칩 시장 규모는 2025년 184억 1,000만 달러로 평가되었습니다. 2026년에는 199억 7,000만 달러로 확대되어 2026년부터 2031년에 걸쳐 CAGR 10.3%로 성장을 지속하여, 2031년에는 326억 달러에 이를 것으로 예측됩니다.

본 보고서는 LED 칩 기술(기존 LED, Mini-LED, Micro-LED), 반도체 소재(GaN/InGaN, AlGaInP, 기타 반도체 소재), 용도(일반 조명, 자동차, 기타) 및 지역(중국, 일본, 인도, 한국, 동남아시아, 기타 아시아태평양)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

아시아태평양의 LED 칩 시장 동향 및 인사이트

LED 칩 제조를 위한 정부 주도의 ‘메이크 인 인디아’ 우대 조치

인도의 생산 연계형 인센티브 제도는 인증된 LED 부품의 증분 매출액에 대해 4-6%의 보상을 지급하고 있으며, 국내 부가가치율을 20% 미만에서 80%로 급격히 끌어올리는 것을 목표로 하는 기존 공장의 확장 및 신규 팹 건설을 뒷받침하고 있습니다. 승인된 신청자들은 이미 10억 달러 이상을 투자하겠다고 약속했으며, 이를 통해 전 세계 반도체 제조업체들이 공급처를 다각화하고 특정 국가에 대한 의존도를 낮출 수 있는 길이 열렸습니다. 성공의 열쇠는 GaN 에피택시 장비, 숙련된 인력, 그리고 지원 인프라에 대한 병행 투자에 달려 있으며, 이러한 분야는 현재 정책적 우선순위가 높아지고 있습니다.

동남아시아의 이륜차 전기화

베트남, 태국, 인도네시아에서는 전동 스쿠터와 전동 오토바이가 도시 교통의 주류를 이루고 있어, 저전력형 LED 헤드램프, 테일램프, 계기판에 대한 수요가 급증하고 있습니다. 어댑티브 빔과 주간 주행등이 채택됨에 따라 차량당 칩 탑재량은 증가하고 있지만, 열대 기후인 탓에 열 성능에 대한 요구 사항은 매우 엄격합니다. 자동차 제조업체들은 조립의 복잡성과 보증 비용을 줄일 수 있는 모듈식 LED 어셈블리를 선호하고 있으며, 견고한 열 설계 역량을 갖춘 칩 공급업체에는 큰 이익이 돌아갈 것으로 보입니다.

6인치 GaN 에피택셜 웨이퍼의 수급 불균형

LED, 파워, RF 소자 제조업체들은 제한된 6인치 GaN 웨이퍼 생산 능력을 놓고 경쟁을 벌이고 있으며, 8인치 라인으로의 전환이 지연되면서 이러한 긴장감은 더욱 고조되고 있습니다. 가격 변동과 할당 위험으로 인해, 자체 에피택시 설비를 보유하지 않거나 전략적 공급 계약을 체결하지 않은 칩 제조업체의 이익률은 압박을 받고 있습니다. 이러한 동향은 중국, 대만, 한국에서 수직 통합 움직임을 가속화하고 있지만, 시판 웨이퍼 공급에 의존하는 팹리스 설계 회사들에게는 진입 장벽이 높아지는 결과를 초래하고 있습니다.

부문별 분석

기존 LED 부문은 2025년에 80.36%의 점유율을 유지했으며, 칩 1개당 0.10달러 미만의 신뢰할 수 있는 루멘 단가라는 경제성을 바탕으로 아시아태평양의 LED 칩 시장 규모를 지탱하고 있습니다. 미니 LED 어레이는 TV나 모니터에서 수천 개의 로컬 디밍 구역을 지원하면서도 마이크로 LED와 같은 완전한 매스 트랜스퍼의 부담을 피함으로써, 프리미엄 중급 시장을 개척하고 있습니다. 고급 TV 제조업체들은 화면 크기를 43인치에서 100인치로 확대하고 있으며, 패널당 칩 수를 늘림으로써 부가가치가 높은 비닝 및 열 관리 서비스에 유리한 기회를 창출하고 있습니다. 마이크로 LED 칩은 여전히 출하량의 5% 미만에 그치고 있지만, 초대형 TV 및 증강현실(AR) 웨어러블 기기용 직접 발광 디스플레이 시범 프로젝트를 배경으로 연평균 성장률(CAGR) 14.34%를 기록하며 성장하고 있습니다. 식스 시그마 전사 수율 및 병렬 레이저 장비를 습득한 공급업체는 마이크로 LED의 처리량이 향상됨에 따라 초기 기술적 우위를 상당한 수익으로 전환할 수 있을 것으로 전망됩니다.

일반적인 기존 LED 시장의 가격 압박은 계속해서 매출 총이익률을 압박하고 있으며, 대형 팹 업체들은 고정비를 분산시키기 위해 웨이퍼 취급의 자동화 및 대형 리액터 도입을 추진하고 있습니다. TV 백라이트 분야에서 미니 LED의 최적 적용 범위가 확대되고 있습니다. 이는 주요 브랜드들이 양자점과 고밀도 LED 매트릭스를 결합하여 OLED와 같은 명암비를 구현하고 있기 때문이며, 이 부문의 성장 여지는 예측 기간을 넘어 계속 확대되고 있습니다. 마이크로 LED의 아키텍처는 루멘당 가격 결정력이 미니 LED의 2-3배에 달하지만, 아시아태평양의 LED 칩 시장에서는 최첨단 기술이라는 주장보다 확실한 납기가 여전히 중시되고 있으며, 이것이 마이크로 LED의 생산 능력 확대가 신중하면서도 꾸준한 속도로 진행되고 있는 이유입니다. 중국, 한국, 대만의 기술 로드맵은 현재 단계적인 수율 향상을 목표로 하는 이정표를 순차적으로 설정하고 있으며, 2028년까지 99.9999%의 전송 성능을 달성하는 것을 목표로 하고 있습니다. 이는 대량 도입에 있어 결정적인 전환점이 될 것으로 보입니다.

추가적인 장점 :

- Excel 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the asia pacific lED chips market size is expected to grow from USD 18.41 billion in 2025 to USD 19.97 billion in 2026 and is forecast to reach USD 32.60 billion by 2031 at 10.3% CAGR over 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, Micro-LED), Semiconductor Material (GaN/InGaN, Algainp, Other Semiconductor Materials), Application (General Lighting, Automotive, and More), and Geography (China, Japan, India, South Korea, Southeast Asia, Rest of Asia Pacific). The Market Forecasts are Provided in Terms of Value (USD).

Asia Pacific LED Chips Market Trends and Insights

Government-Led "Make In India" Incentives For LED Chip Fabrication

India's Production Linked Incentive scheme grants 4-6% rewards on incremental sales of qualified LED components, spurring brownfield expansions and new fabs that target a steep jump in domestic value addition from below 20% toward 80%. Approved applicants have already pledged more than USD 1 billion, unlocking a pathway for global chip producers to diversify sourcing and cut reliance on any single country.Success depends on parallel investment in GaN epitaxy reactors, trained talent, and supportive infrastructure, areas now moving up the policy priority list.

Electrification Of Two-Wheeler Mobility In Southeast Asia

Electric scooters and motorcycles dominate urban transport in Vietnam, Thailand, and Indonesia, creating a surge in demand for power-efficient LED headlamps, taillights, and instrument clusters. Adaptive beams and daytime running lights raise the chip content per vehicle, while the tropical climate sets strict thermal performance requirements. Vehicle makers favor modular LED assemblies that lower assembly complexity and warranty costs, positioning chip vendors with robust thermal engineering capabilities for outsized gains.

Supply-Demand Mismatch Of 6-Inch GaN Epitaxial Wafers

LED, power, and RF device makers are competing for finite 6-inch GaN wafer capacity, a tension aggravated by the slow migration to 8-inch lines. Price volatility and allocation risk squeeze margins for chip producers lacking captive epitaxy or strategic supply agreements. The dynamic fuels vertical integration moves across China, Taiwan, and South Korea, but raises entry barriers for fabless design houses that depend on merchant wafer supply.

Other drivers and restraints analyzed in the detailed report include:

- Corporate Net-Zero Targets Accelerating Industrial LED Retrofits

- Expanding Mini-LED Backlighting Adoption In High-End TVs

- Persistent Yield Challenges In Micro-LED Mass Transfer

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

The conventional LED segment retained 80.36% share in 2025, anchoring the Asia Pacific LED chips market size with dependable cost-per-lumen economics at sub-USD 0.10 per chip. Mini-LED arrays have carved out a premium middle ground, supporting thousands of local dimming zones in televisions and monitors while avoiding the full mass-transfer burden of micro-LEDs. Premium TV makers are scaling screen sizes from 43-inch to 100-inch, raising chip counts per panel and creating fertile ground for value-added binning and thermal management services. Micro-LED chips, although still below 5% volume, are advancing at a 14.34% CAGR on the back of direct-emissive display pilots for ultra-large TVs and augmented-reality wearables. Suppliers that master six-sigma transfer yields and parallel laser tools stand to translate early technical wins into outsized revenue as micro-LED throughput improves.

Price pressure in commodity conventional LEDs continues to compress gross margins, prompting large fabs to automate wafer handling and adopt larger-format reactors to dilute fixed costs. Mini-LED's sweet spot in television backlighting is widening as blue-chip brands pair quantum dots with denser LED matrices to deliver OLED-like contrast, extending the segment's runway beyond the forecast horizon. Micro-LED architectures command pricing power that is two to three times higher than mini-LEDs on a per-lumen basis, but the Asia Pacific LED chips market still values predictable delivery schedules over bleeding-edge claims, explaining the cautious but steady pace of micro-LED capacity additions. Technology roadmaps across China, South Korea, and Taiwan now sequence incremental yield milestones, aiming for 99.9999% transfer performance by 2028, which will be a decisive inflection for volume adoption.

List of Companies Covered in this Report:

- Nichia Corporation

- Samsung Electronics Co., Ltd.

- Seoul Semiconductor Co., Ltd.

- Cree LED, an SGH Company

- Epistar Corporation

- EVERLIGHT Electronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- OSRAM Opto Semiconductors GmbH

- LG Innotek Co., Ltd.

- Toyoda Gosei Co., Ltd.

- Lumileds Holding B.V.

- NationStar Optoelectronics Co., Ltd.

- Lite-On Technology Corporation

- TYNTEK Corporation

- Lextar Electronics Corporation

- Bridgelux, Inc.

- Ams-OSRAM AG

- Rohinni, LLC

- PlayNitride Inc.

- HC SemiTek Corporation

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Expanding Mini-LED Backlighting Adoption in High-End TVs

- 4.2.2 Government-Led "Make in India" Incentives for LED Chip Fabrication

- 4.2.3 Growing Demand for UV-C LED Chips in Sterilization Systems

- 4.2.4 Electrification of Two-Wheeler Mobility in Southeast Asia

- 4.2.5 Phosphor-Free Micro-LED Architectures Reducing Cost per Lumen

- 4.2.6 Corporate Net-Zero Targets Accelerating Industrial LED Retrofits

- 4.3 Market Restraints

- 4.3.1 Persistent Yield Challenges in Micro-LED Mass Transfer

- 4.3.2 Supply-Demand Mismatch of 6-Inch GaN Epitaxial Wafers

- 4.3.3 Intellectual-Property Cross-Licensing Barriers for Start-Ups

- 4.3.4 Volatile Rare-Earth Phosphor Prices Affecting Chip Margins

- 4.4 Industry Value Chain Analysis

- 4.5 Impact of Macroeconomic Factors on the Market

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Industry Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Geography

- 5.4.1 China

- 5.4.2 Japan

- 5.4.3 India

- 5.4.4 South Korea

- 5.4.5 Southeast Asia

- 5.4.6 Rest of Asia Pacific

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 Samsung Electronics Co., Ltd.

- 6.4.3 Seoul Semiconductor Co., Ltd.

- 6.4.4 Cree LED, an SGH Company

- 6.4.5 Epistar Corporation

- 6.4.6 EVERLIGHT Electronics Co., Ltd.

- 6.4.7 San'an Optoelectronics Co., Ltd.

- 6.4.8 OSRAM Opto Semiconductors GmbH

- 6.4.9 LG Innotek Co., Ltd.

- 6.4.10 Toyoda Gosei Co., Ltd.

- 6.4.11 Lumileds Holding B.V.

- 6.4.12 NationStar Optoelectronics Co., Ltd.

- 6.4.13 Lite-On Technology Corporation

- 6.4.14 TYNTEK Corporation

- 6.4.15 Lextar Electronics Corporation

- 6.4.16 Bridgelux, Inc.

- 6.4.17 Ams-OSRAM AG

- 6.4.18 Rohinni, LLC

- 6.4.19 PlayNitride Inc.

- 6.4.20 HC SemiTek Corporation

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment