|

시장보고서

상품코드

2063933

중국의 LED 칩 시장 : 점유율 분석, 업계 동향과 통계, 성장 예측(2026-2031년)China LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

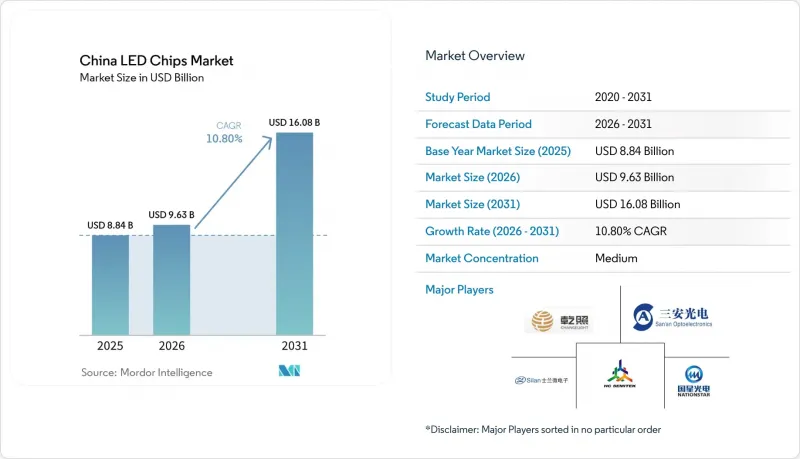

Mordor Intelligence에 의하면, 중국 LED 칩 시장 규모는 2025년에 88억 4,000만 달러, 2026년에 96억 3,000만 달러, 2031년까지 160억 8,000만 달러에 이를 것으로 예측되며, 2026년부터 2031년까지 CAGR 10.8%로 성장할 전망입니다.

본 보고서는 LED 칩 기술(기존 LED, Mini-LED, Micro-LED), 반도체 소재(GaN/InGaN, AlGaInP, 기타 반도체 소재) 및 용도(일반 조명, 자동차, 백라이트/디스플레이, 소비자용 전자기기, 산업용/특수 조명)별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국 LED 칩 시장 동향과 인사이트

국내 반도체 제조에 대한 정부 보조금

국가 IC 기금의 3단계에서는 2024년에 470억 달러가 배정되며, 이 중 18%가 화합물 반도체에 할당되어 인증된 LED 팹용 MOCVD 반응기의 비용을 최대 50% 절감할 예정입니다. 주 차원의 공동 출자를 통해 85억 달러가 추가로 조달됨에 따라, 생산 능력이 급속히 확대되고 단기 자금 조달이 확보될 것입니다. 다만, 보조금을 받는 기업은 2027년까지 설비의 90%를 국산 제품으로 조달하고, 연간 생산성 지표에서 15%를 달성해야 합니다. 이러한 요건들은 이미 규모를 확립한 대기업에 유리하게 작용합니다. Sanan은 2024년 순이익의 22%에 해당하는 정부 보조금을 수령했다고 보고했으며, 이로 인해 지속적인 의존 관계가 부각되고 있습니다. 자금 지원은 생산량 확대를 가속화하지만, 실적 기준은 선도 기업을 둘러싼 경쟁 우위를 강화하고 경쟁력이 약한 신규 시장 진출기업을 도태시킴으로써 중국 LED 칩 시장의 중기적 구조를 형성하고 있습니다.

고효율 GaN-on-Si 에피택시 기술로의 전환

Sanan과 HC SemiTek은 기판 비용이 30-40% 낮은 점과 8인치 웨이퍼 특유의 다이 밀도 향상이라는 장점에 매료되어, 2025년 1분기부터 2026년 1분기에 걸쳐 양사의 GaN-on-Si 장비를 총 31대에서 47대로 확대했습니다. 2025년에 발표된 버퍼층 기술의 획기적인 발전으로 인해 수율은 91%에 달했으며, 사파이어 플랫폼과의 격차 대부분이 해소되었습니다. 고휘도 부문에서는 여전히 열적 이유로 사파이어가 선호되지만, GaN-on-Si는 저비용 램프와 중출력 백라이트를 가능하게 하여 해당 분야 수요를 확대되고 있습니다. 웨이퍼의 뒤틀림 관리와 열적 불일치 문제를 극복한 제조업체는 이익률 개선을 실현하는 동시에 기존 생산 라인의 수명을 연장할 수 있으며, 이를 통해 중국 LED 칩 시장의 성장세를 유지할 수 있게 될 것입니다.

마이크로 LED 양산화를 위한 막대한 설비 투자

최첨단 레이저 또는 정전전사 장비는 대당 1,200만-1,800만 달러에 달하지만, 소비자의 경제성 요건을 충족하는 처리량의 불과 20-40%만 제공할 수 있어, 단일 마이크로 LED 생산 라인의 설비 투자액을 5,000만 달러 이상으로 끌어올리고 있습니다. 장치의 속도가 2배로 빨라지고 불량률이 절반으로 줄어들기 전까지는 대중 시장을 겨냥한 웨어러블 기기나 TV의 상용화는 여전히 어려울 것입니다. 대부분의 국내 칩 제조업체들에게 있어 초기 단계의 수익성이 마이너스인 점은 적극적인 규모 확대를 저해하고 있으며, 중국 LED 칩 시장에 대한 단기적인 호재를 약화시키고 있습니다.

부문별 분석

기존 LED는 2025년 매출의 83%를 차지하며, 8-12%의 가격 하락에도 불구하고 중국 LED 칩 시장 규모를 지탱하고 있습니다. 이미 안정화된 4인치 및 6인치 생산 라인은 여전히 긍정적인 현금 흐름을 창출하고 있으며, 이를 통해 미니 LED 및 마이크로 LED에 대한 연구개발비용을 충당하고 있습니다. Mini-LED 백라이트의 출하 대수는 TV 기준 420만 대에 달했으며, 이는 다이(반도체 칩) 출하량의 대폭적인 증가로 이어졌습니다. 2027년까지 65인치 OLED 패널 가격이 300달러 아래로 떨어질 경우, 미니 LED 시장은 옥외 간판 및 업무용 모니터 시장으로 축소될 가능성이 있습니다. 그러나 현재 로컬 디밍에 대한 수요와 밝기 측면에서의 우위 덕분에 미니 LED는 성장세를 유지하고 있으며, 중국 LED 칩 시장 전체의 출하량 증가를 뒷받침하고 있습니다.

마이크로 LED는 2025년 매출에서 차지하는 비중이 2% 미만에 그칠 것으로 보이지만, 2031년까지 연평균 성장률(CAGR) 약 15.64%를 나타낼 것으로 예측되며, 이는 칩 유형 중 가장 높은 성장률입니다. 웨어러블 디스플레이나 자동차용 헤드업 디스플레이에는 무기 발광 소자가 제공하는 고휘도와 긴 수명이 요구되고 있습니다. 2025년 『Nature Photonics』지에 게재된 연구에서는 10µm 미만의 피치로 250 lm/W를 초과하는 효율이 입증되어, 그 물리적 실현 가능성이 증명된 동시에 제조상의 과제도 부각되었습니다. 매트릭스 전사 기술이 발전함에 따라 마이크로 LED가 궁극적으로 수익 구조를 변화시킬 가능성은 있지만, 향후 3년 동안은 기존 LED가 중국 LED 칩 시장 전체의 기술 전환을 계속 뒷받침할 것입니다.

기타 혜택:

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모와 성장 예측

제6장 경쟁 구도

제7장 시장 기회와 향후 전망

JHSAccording to Mordor Intelligence, the china lED chips market size is projected to be USD 8.84 billion in 2025, USD 9.63 billion in 2026, and reach USD 16.08 billion by 2031, growing at a CAGR of 10.8% from 2026 to 2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, Micro-LED), Semiconductor Material (GaN/InGaN, Algainp, Other Semiconductor Materials), and Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, Industrial/Specialty Lighting). The Market Forecasts are Provided in Terms of Value (USD).

China LED Chips Market Trends and Insights

Government Subsidies for Domestic Semiconductor Manufacturing

Phase III of the National IC Fund earmarked USD 47 billion in 2024, with 18% directed to compound semiconductors, lowering MOCVD reactor costs by up to 50% for qualified LED fabs.Provincial co-funding adds a further USD 8.5 billion, translating into rapid capacity gains and safeguarding near-term capital access. Subsidy recipients, however, must hit 90% domestic equipment usage and 15% annual productivity metrics by 2027, requirements that favor entrenched scale players. Sanan reported government grants equal to 22% of 2024 net income, underscoring continuing dependence. While the cash support accelerates volume, the performance thresholds strengthen the competitive moat around leaders and cull weaker entrants, shaping the medium-term structure of the China LED chips market.

Transition Toward High-Efficacy GaN-on-Si Epitaxy

Sanan and HC SemiTek expanded their combined GaN-on-Si fleet from 31 to 47 reactors between Q1 2025 and Q1 2026, attracted by 30-40% lower substrate cost and the die density gains inherent to 8-inch wafers.Buffer-layer engineering breakthroughs published in 2025 pushed yields to 91%, closing much of the gap with sapphire platforms. Although high-brightness segments still prefer sapphire for thermal reasons, GaN-on-Si enables low-cost lamps and mid-power backlighting, broadening addressable demand. Producers that master wafer bow management and thermal mismatch will unlock margin relief while extending the lifespan of conventional lines, thereby sustaining the growth momentum of the China LED chips market.

High Capital Expenditure for Micro-LED Mass Transfer

State-of-the-art laser or electrostatic transfer tools cost USD 12-18 million each yet deliver only 20-40% of the throughput that consumer economics require, pushing a single micro-LED line's capex above USD 50 million. Until tool speeds double and defect rates halve, mass-market wearables and TVs remain out of reach. For most domestic chipmakers, negative early-stage returns deter aggressive scaling, tempering the near-term uplift to the China LED chips market.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Expansion of New-Energy Vehicle Headlamp Adoption

- Rising Demand for Mini-LED Backlighting in High-End TVs

- Overcapacity in Conventional LED Chip Lines

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs generated 83% of 2025 revenue, anchoring the China LED chips market size despite 8-12% price compression. Mature 4-inch and 6-inch lines still deliver positive cash flow, subsidizing R&D into mini-LED and micro-LED. Mini-LED backlighting shipments reached 4.2 million TV units, translating into a significant uplift in die volumes. Should OLED panels fall below USD 300 for a 65-inch size by 2027, mini-LED could retrench to outdoor signage and professional monitors. Yet today's local dimming requirements and brightness advantages keep mini-LED on an expansion path that supports total unit growth in the China LED chips market.

Micro-LED, though contributing less than 2% of 2025 sales, is projected to grow at about 15.64% CAGR through 2031, the fastest among chip types. Wearable displays and automotive head-up units require the high brightness and extended lifetime that inorganic emitters provide. A 2025 Nature Photonics study validated efficiencies above 250 lm/W at sub-10 µm pitches, proving the physics while highlighting manufacturing hurdles. As mass-transfer improves, micro-LED could eventually shift revenue mix, but for the next three years, conventional LEDs will continue to bankroll technological migration across the China LED chips market.

List of Companies Covered in this Report:

- Sanan Optoelectronics Co., Ltd.

- HC SemiTek Corporation

- Xiamen Changelight Co., Ltd.

- Hangzhou Silan Microelectronics Co., Ltd.

- NationStar Optoelectronics Co., Ltd.

- Jiangsu Azure Lighting Technologies Co., Ltd.

- Focus Lightings Tech Co., Ltd.

- Zhejiang Keguang Electronics Co., Ltd. (KINGLIGHT)

- Advanced Optoelectronic Technology, Inc.

- Epistar Corporation

- Nichia Corporation

- Cree LED, an SGH Company

- Lumileds Holding B.V.

- OSRAM Opto Semiconductors GmbH

- Seoul Semiconductor Co., Ltd.

- Genesis Photonics Inc.

- Shenzhen Refond Optoelectronics Co., Ltd.

- Shenzhen MTC Co., Ltd.

- Unistars Corporation

- Tianjin Zhonghuan Semiconductor Co., Ltd.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rising Demand for Mini-LED Backlighting in High-End TVs

- 4.2.2 Government Subsidies for Domestic Semiconductor Manufacturing

- 4.2.3 Transition Toward High-Efficacy GaN-on-Si Epitaxy

- 4.2.4 Rapid Expansion of New-Energy Vehicle Headlamp Adoption

- 4.2.5 Localization Push Across Consumer Electronics Supply Chains

- 4.2.6 Integration of Micro-LED in Next-Gen Wearables

- 4.3 Market Restraints

- 4.3.1 Overcapacity in Conventional LED Chip Lines

- 4.3.2 High Capital Expenditure for Micro-LED Mass Transfer

- 4.3.3 Patent Litigation Risks with Foreign IP Holders

- 4.3.4 Volatility in Sapphire and Silicon Carbide Substrate Prices

- 4.4 Impact of Macroeconomic Factors on the Market

- 4.5 Industry Value Chain Analysis

- 4.6 Regulatory Landscape

- 4.7 Technological Outlook

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Threat of New Entrants

- 4.8.2 Bargaining Power of Suppliers

- 4.8.3 Bargaining Power of Buyers

- 4.8.4 Threat of Substitutes

- 4.8.5 Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Sanan Optoelectronics Co., Ltd.

- 6.4.2 HC SemiTek Corporation

- 6.4.3 Xiamen Changelight Co., Ltd.

- 6.4.4 Hangzhou Silan Microelectronics Co., Ltd.

- 6.4.5 NationStar Optoelectronics Co., Ltd.

- 6.4.6 Jiangsu Azure Lighting Technologies Co., Ltd.

- 6.4.7 Focus Lightings Tech Co., Ltd.

- 6.4.8 Zhejiang Keguang Electronics Co., Ltd. (KINGLIGHT)

- 6.4.9 Advanced Optoelectronic Technology, Inc.

- 6.4.10 Epistar Corporation

- 6.4.11 Nichia Corporation

- 6.4.12 Cree LED, an SGH Company

- 6.4.13 Lumileds Holding B.V.

- 6.4.14 OSRAM Opto Semiconductors GmbH

- 6.4.15 Seoul Semiconductor Co., Ltd.

- 6.4.16 Genesis Photonics Inc.

- 6.4.17 Shenzhen Refond Optoelectronics Co., Ltd.

- 6.4.18 Shenzhen MTC Co., Ltd.

- 6.4.19 Unistars Corporation

- 6.4.20 Tianjin Zhonghuan Semiconductor Co., Ltd.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment