|

시장보고서

상품코드

2065500

유럽의 LED 칩 시장 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)Europe LED Chips - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

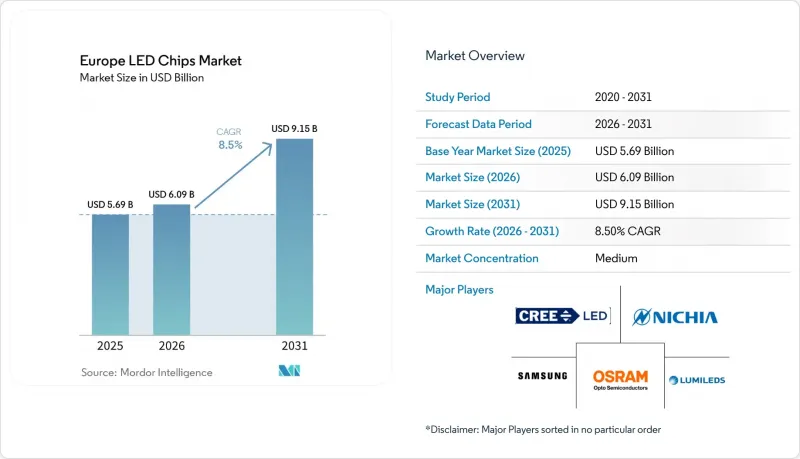

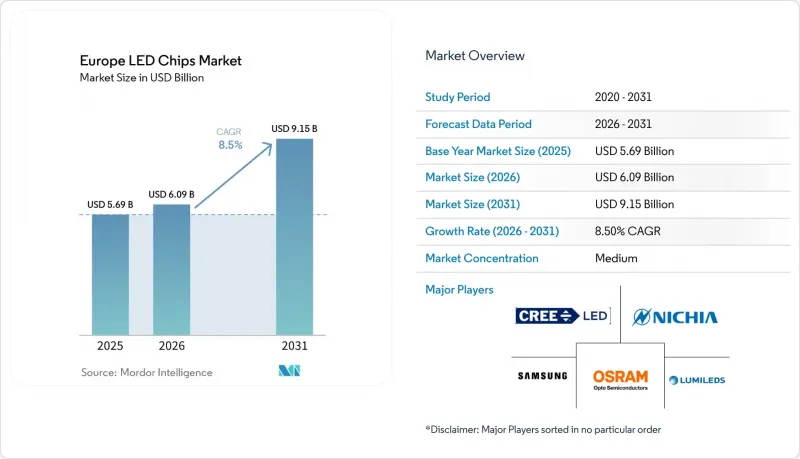

Mordor Intelligence에 의하면, 유럽의 LED 칩 시장 규모는 2025년 56억 9,000만 달러로 평가되었고, 2026년에는 60억 9,000만 달러로 추정되고, 2031년까지 91억 5,000만 달러에 이를 것으로 예상되며, 2026-2031년 CAGR 8.5%로 성장할 전망입니다.

본 보고서는 LED 칩 기술별(기존 LED, Mini-LED, Micro-LED), 반도체 소재별(GaN/InGaN, 기타 반도체 소재), 용도별(일반 조명, 자동차, 백라이트 및 디스플레이, 소비자용 전자기기, 산업용 및 특수 조명) 및 지역별(영국, 프랑스, 기타 유럽)로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

유럽의 LED 칩 시장 동향 및 인사이트

스마트 시티 가로등으로의 전환

지자체는 전기 요금을 최대 75% 절감하기 위해 공공 조명 시설 개보수를 추진하고 있습니다. 파리시는 2024년에 7만 개의 조명 기구를 원격 진단 기능이 탑재된 LED 조명 기구로 교체하기 위해 7억 유로(7억 6,300만 달러) 규모의 계약을 체결했습니다. 뮈루즈시는 1만 4,000개의 조명 기구를 현대화하기 위해 2,400만 유로(2,616만 달러)를 투자하여 2026년 여름까지 공사를 완료할 계획입니다. 프랑스의 ‘Lum'ACTEE+’ 프로그램에서는 2028년까지 전국에서 최대 400만 개의 조명 기구를 교체하기 위해 1,500만 유로(1,635만 달러)가 배정되었습니다. 스마트 제어를 통해 드라이버 IC 및 연결 모듈이 추가되고, 1개당 반도체 사용량이 증가함에 따라 유럽 전체의 LED 칩 시장 규모가 확대되고 있습니다.

전기차 헤드램프 통합의 확대

유럽의 각 자동차 제조업체들은 2027년 1월 이후 출시되는 신차에 어댑티브 프론트 라이팅의 탑재를 의무화하는 ECE 규정 123의 개정에 대응하기 위해 고밀도 LED 매트릭스 탑재를 추진하고 있습니다. ams OSRAM의 ‘EVIYOS HD25’ 마이크로 LED 어레이는 2만 5,600개의 개별 제어 가능한 픽셀을 갖추고 있으며, 이미 아우디 ‘Q6 e-tron’ 및 NIO ‘ET9’를 위해 양산이 시작되었습니다. 폭스바겐의 2026년형 ‘투아레그’와 ‘티구안’에는 19,200픽셀의 IQ. Light 헤드램프가 탑재되어 있어, 마주 오는 차량에 눈부심을 주지 않으면서도 최대의 밝기를 유지합니다. 독일에 OEM 기업들이 집중되어 있어 현지 칩 수요를 뒷받침하고 있으며, 닛야 화학공업이 2024년에 아헨에 개설한 혁신 센터는 자동차 제조업체와의 협력 관계를 강화하고 있습니다.

마이크로 LED의 양산화에 따른 높은 설비 투자 비용

한 조사 기관에 따르면, 2025년에는 재료비의 86.2%가 기판과 전사 장치에서 발생할 것으로 추정됩니다. 스프링거(Springer)사의 2024년 리뷰에 따르면, OLED 패널의 경제성과 대등한 수준을 달성하려면 99.9999% 이상의 수율이 필요하다고 결론지었으나, 현재 세대의 장비로는 대형 기판에서 이 기준을 충족하는 경우가 거의 없습니다. 애플라이드 머티리얼즈(Applied Materials)와 동종 업계의 다른 기업들은 처리량을 10배로 늘리기 위해 노력하고 있지만, OLED와의 비용 균형을 달성하는 것은 2028년부터 2030년 이전에는 어려울 것으로 전망됩니다. 한국의 대기업처럼 수십억 달러 규모의 설비 투자 능력을 갖추지 못한 유럽의 디스플레이 조립 제조업체들은 경제성이 개선될 때까지 틈새 시장인 자동차용 HUD나 웨어러블 패널에 주력할 수밖에 없을 가능성이 있습니다.

부문별 분석

2025년, 유럽의 LED 칩 시장 점유율은 성숙한 공급망과 일반 조명 및 자동차 외장 램프에 적합한 중출력 다이의 가격이 0.10달러 미만인 점에 힘입어, 기존 LED가 80.26%를 차지했습니다. 니치아 화학공업의 757 시리즈가 65mA에서 220루멘/와트를 달성하는 등, 효율이 점진적으로 향상됨에 따라 이 부문은 가격에 민감한 이용 사례에서 경쟁력을 유지하고 있습니다. 미니 LED는 중간 위치를 차지하고 있으며, 마이크로 LED의 제약 요인인 물질 이동 문제를 겪지 않으면서도 수천 개의 로컬 디밍 구역을 구현할 수 있어, 프리미엄 TV나 차량용 인포테인먼트 화면의 표준적인 업그레이드 경로로 자리 잡고 있습니다.

마이크로 LED는 초대형 TV, 픽셀 크기가 10마이크로미터 미만인 스마트 워치 디스플레이, 그리고 10,000니트의 밝기가 필요한 자동차용 헤드업 디스플레이에 시범 도입됨에 따라 연평균 성장률(CAGR) 12.34%로 성장하고 있습니다. PlayNitride사와 Plessey사는 5마이크로미터 미만의 모노리식 마이크로 LED-on-실리콘 어레이 개발을 추진하고 있으며, 이 아키텍처를 차세대 AR 헤드셋에서 OLED의 후속 기술로 자리매김하고 있습니다. 에코디자인 규제로 인해 리트로핏(기존 제품의 교체) 기간이 단축됨에 따라 기존 LED의 매출은 정체될 전망이지만, 막대한 도입 대수 덕분에 장기적인 수요는 확보될 것으로 보입니다. 미니 LED는 2028년까지 TV 출하 대수가 1,500만 대를 넘어설 것으로 예상되며, 마이크로 LED가 비용 면에서 주류 수준에 도달할 때까지 그 기세를 유지할 것으로 전망됩니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

LSHAccording to Mordor Intelligence, the europe lED chip market size is expected to increase from USD 5.69 billion in 2025 to USD 6.09 billion in 2026 and reach USD 9.15 billion by 2031, growing at a CAGR of 8.5% over 2026-2031.

This report is Segmented by LED Chip Technology (Conventional LEDs, Mini-LED, and Micro-LED), Semiconductor Material (GaN/InGaN, and Other Semiconductor Materials), Application (General Lighting, Automotive, Backlighting/Displays, Consumer Electronics, and Industrial/Specialty Lighting), and Geography (United Kingdom, France, and Rest of Europe). The Market Forecasts are Provided in Terms of Value (USD).

Europe LED Chips Market Trends and Insights

Shift Toward Smart City Streetlighting

Municipalities are retrofitting public lighting to shrink electricity bills by up to 75%. Paris awarded a EUR 700 million (USD 763 million) contract in 2024 to replace 70,000 fixtures with LED luminaires equipped with remote diagnostics. Mulhouse committed EUR 24 million (USD 26.16 million) to modernize 14,000 lamps, targeting completion by summer 2026. France's Lum'ACTEE+ program earmarked EUR 15 million (USD 16.35 million) for a nationwide upgrade of up to 4 million luminaires by 2028. Smart controls boost per-pole semiconductor content by adding driver ICs and connectivity modules, elevating the overall Europe LED chip market value.

Expanding EV Headlamp Integration

Europe's vehicle makers are embedding increasingly dense LED matrices to comply with amendments to ECE Regulation 123, which mandate adaptive front lighting on new models after January 2027. ams OSRAM's EVIYOS HD25 micro-LED array offers 25,600 addressable pixels and is already in volume production for the Audi Q6 e-tron and the NIO ET9. Volkswagen's 2026 Touareg and Tiguan carry 19,200-pixel IQ. Light headlamps that maintain maximum illumination while avoiding glare for oncoming traffic. German OEM concentration anchors chip demand locally, and Nichia's 2024 Aachen innovation center strengthens vendor collaboration with automakers.

High Capital Cost for Micro-LED Mass Transfer

The research company estimated that, in 2025, 86.2% of the materials stemmed from substrates and transfer tools. Springer's 2024 review concluded that yields above 99.9999% are necessary to match OLED panel economics, but current equipment generations rarely meet this benchmark on large substrates. Applied Materials and peers are striving to lift throughput tenfold, yet cost parity with OLED appears unlikely before 2028-2030. European display assemblers, lacking the multibillion-dollar capex muscle of Korean giants, may be forced to focus on niche automotive HUD and wearable panels until the economics improve.

Other drivers and restraints analyzed in the detailed report include:

- EU Green Deal Energy-Efficiency Targets

- Rapid Adoption of Mini-LED Backlit Displays

- Supply Volatility of Gallium and Indium

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Conventional LEDs dominated the European LED chip market share at 80.26% in 2025, buoyed by mature supply chains and sub-USD 0.10 pricing for mid-power die suited to general lighting and exterior automotive lamps. Incremental efficiency gains, such as Nichia's 757 series reaching 220 lumens per watt at 65 milliamps, keep the segment competitive for price-sensitive use cases. Mini-LED occupies the middle ground, enabling thousands of local dimming zones without the mass-transfer hurdles that restrain micro-LED, and is becoming the default upgrade path for premium televisions and in-vehicle infotainment screens.

Micro-LED is advancing at a 12.34% CAGR through pilot deployments in ultra-large televisions, smartwatch faces with sub-10-micrometer pixels, and automotive heads-up displays requiring 10,000-nit brightness. PlayNitride and Plessey are pushing monolithic micro-LED-on-silicon arrays below 5 micrometers, positioning the architecture as a successor to OLED in next-generation AR headsets. Conventional LED revenue will plateau as Ecodesign rules compress retrofit windows, yet its vast installed base secures a lengthy tail. Mini-LED is expected to exceed 15 million television shipments by 2028, maintaining momentum until micro-LED hits mainstream cost thresholds.

List of Companies Covered in this Report:

- Nichia Corporation

- OSRAM Opto Semiconductors GmbH

- Samsung Electronics Co., Ltd.

- Lumileds Holding B.V.

- Cree LED

- Seoul Semiconductor Co., Ltd.

- LG Innotek Co., Ltd.

- II-VI Incorporated

- Epistar Corp.

- ams-OSRAM AG

- Rohinni LLC

- PlayNitride Inc.

- Plessey Semiconductors Ltd.

- Lextar Electronics Corp.

- OptoGaN Ltd.

- Everlight Electronics Co., Ltd.

- San'an Optoelectronics Co., Ltd.

- Dominant Opto Technologies Sdn Bhd

- Brightek Optoelectronic Co., Ltd.

- Crystal IS, Inc.

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Rapid Adoption of Mini-LED Backlit Displays

- 4.2.2 Expanding EV Headlamp Integration

- 4.2.3 Shift Toward Smart City Streetlighting

- 4.2.4 EU Green Deal Energy-Efficiency Targets

- 4.2.5 Increased Local Wafer-Level Packaging Capacity

- 4.2.6 Proliferation of UV-C LED Disinfection Systems

- 4.3 Market Restraints

- 4.3.1 Supply Volatility of Gallium and Indium

- 4.3.2 High Capital Cost for Micro-LED Mass Transfer

- 4.3.3 IP Fragmentation and Royalty Disputes

- 4.3.4 Competition From OLED in Premium Displays

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Impact of Macroeconomic Factors on the Market

- 4.8 Porter's Five Forces Analysis

- 4.8.1 Bargaining Power of Suppliers

- 4.8.2 Bargaining Power of Buyers

- 4.8.3 Threat of New Entrants

- 4.8.4 Threat of Substitutes

- 4.8.5 Intensity of Competitive Rivalry

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By LED Chip Technology

- 5.1.1 Conventional LEDs

- 5.1.2 Mini-LED

- 5.1.3 Micro-LED

- 5.2 By Semiconductor Material

- 5.2.1 GaN / InGaN

- 5.2.2 AlGaInP

- 5.2.3 Other Semiconductor Materials

- 5.3 By Application

- 5.3.1 General Lighting

- 5.3.2 Automotive

- 5.3.3 Backlighting / Displays

- 5.3.4 Consumer Electronics

- 5.3.5 Industrial / Specialty Lighting

- 5.4 By Geography

- 5.4.1 United Kingdom

- 5.4.2 Germany

- 5.4.3 France

- 5.4.4 Rest of Europe

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Nichia Corporation

- 6.4.2 OSRAM Opto Semiconductors GmbH

- 6.4.3 Samsung Electronics Co., Ltd.

- 6.4.4 Lumileds Holding B.V.

- 6.4.5 Cree LED

- 6.4.6 Seoul Semiconductor Co., Ltd.

- 6.4.7 LG Innotek Co., Ltd.

- 6.4.8 II-VI Incorporated

- 6.4.9 Epistar Corp.

- 6.4.10 ams-OSRAM AG

- 6.4.11 Rohinni LLC

- 6.4.12 PlayNitride Inc.

- 6.4.13 Plessey Semiconductors Ltd.

- 6.4.14 Lextar Electronics Corp.

- 6.4.15 OptoGaN Ltd.

- 6.4.16 Everlight Electronics Co., Ltd.

- 6.4.17 San'an Optoelectronics Co., Ltd.

- 6.4.18 Dominant Opto Technologies Sdn Bhd

- 6.4.19 Brightek Optoelectronic Co., Ltd.

- 6.4.20 Crystal IS, Inc.

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 White-Space and Unmet-Need Assessment