|

시장보고서

상품코드

2063860

중국의 GPU 액체 냉각 : 시장 점유율 분석, 업계 동향 및 통계, 성장 예측(2026-2031년)China GPU Liquid Cooling - Market Share Analysis, Industry Trends & Statistics, Growth Forecasts (2026 - 2031) |

||||||

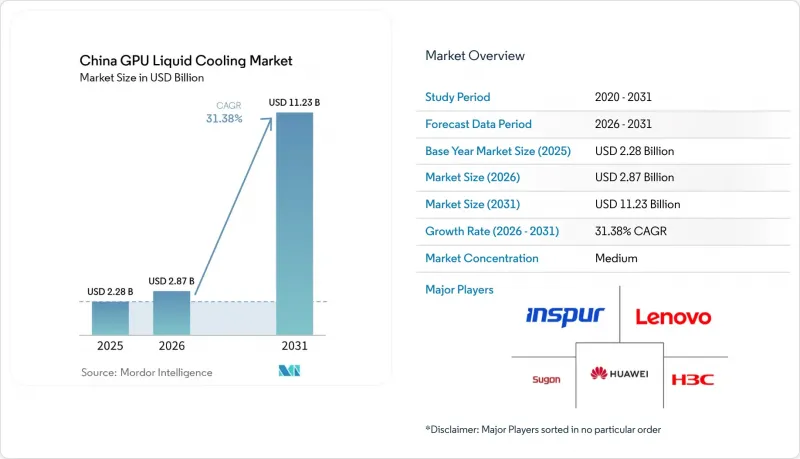

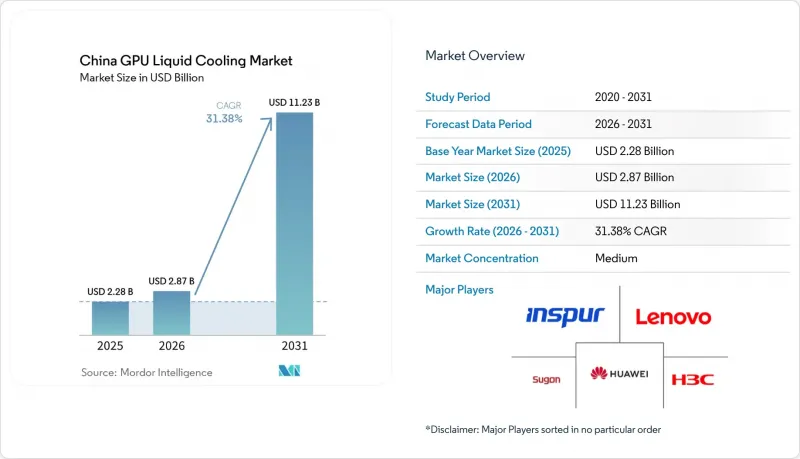

Mordor Intelligence에 의하면, 중국의 GPU 액체 냉각 시장 규모는 2025년에 22억 8,000만 달러로 평가되었습니다. 2026년 28억 7,000만 달러에서 2031년까지 112억 3,000만 달러에 이를 것으로 예상되며, 예측 기간(2026-2031년) CAGR은 31.38%를 나타낼 전망입니다.

본 보고서는 냉각 방식(단상 액체 냉각 및 이상 액체 냉각), 냉각 수준(컴포넌트 수준 냉각 및 서버/랙 수준 냉각), 적용 분야(하이퍼스케일/클라우드, 엔터프라이즈, 정부·연구용 HPC, 엣지 AI), GPU 전력 밀도(300W 미만, 300W-700W, 700W 초과) 및 지역별로 분류되어 있습니다. 시장 전망은 금액(달러) 기준으로 제시되어 있습니다.

중국의 GPU 액체 냉각 시장 동향 및 인사이트

중국 하이퍼스케일 데이터센터에서 AI 훈련 워크로드 채택이 급증하고 있습니다.

중국의 각 하이퍼스케일러 기업들은 클러스터를 수십 페타플롭스에서 수백 페타플롭스 규모로 확장하고 있으며, 가동률이 80%를 초과하더라도 액체 냉각을 통해 접합부 온도를 안정적으로 유지할 수 있습니다. 알리바바 클라우드의 527억 달러 규모의 3개년 인프라 계획에서는 차세대 언어 모델 훈련의 중심에 콜드 플레이트 랙을 배치하여, 팬의 전력 소비로 인해 전체 PUE가 악화되는 것을 방지하고 있습니다. 바이두는 열 부하가 4배로 증가한 데 따라 기존 시설의 개보수를 진행하고 있습니다. 한편, 텐센트는 2026년까지 AI 설비 투자를 50억 달러로 두 배로 늘리고, 랙당 100-200kW를 유지할 수 있는 침지 탱크를 도입하고 있습니다. 국산 AI 모델에 대한 지속적인 수요로 인해 GPU 이용률은 높은 수준을 유지하고 있으며, 이를 뒷받침할 수 있는 것은 액체 냉각뿐입니다.

700W를 초과하는 GPU의 전력 밀도 증가로 인해, 액체 냉각이 필수적으로 되었습니다.

NVIDIA의 Vera Rubin 제품군은 2026년 하반기에 출시될 예정이며, 액체 냉각 시스템을 기본으로 탑재하고 보드 전력 소비량이 1,000W 이상이 될 것으로 예상되어, 플래그십 AI 트레이닝 랙에서는 공랭식 시스템이 필요 없게 됩니다. 델타 일렉트로닉스는 이미 15대의 100kW NVL72 랙을 지원하는 1.5MW 용량의 냉각액 분배 장치를 제공하고 있으며, 한편 화웨이의 액체 냉각 방식 800G 스위치는 패브릭 요소에서 발생하는 열 스로틀링을 방지합니다. 경제성 측면에서도 액체 냉각 방식이 유리합니다. 고밀도화를 통해 설치 면적을 줄일 수 있으며, 공조 설비 비용도 절감할 수 있습니다.

공랭식 시스템에 비해 높은 초기 설비 투자(CAPEX)

콜드 플레이트 어셈블리, 퀵 커넥터 및 CDU는 초기 예산을 40-60% 가량 증가시킬 가능성이 있어, 랙당 50kW 미만의 기준치를 밑도는 사업자에게는 진입 장벽이 됩니다. 부품 비용은 금속 가공과 정밀 기계 가공에 집중되어 있으며, 이러한 분야에서는 규모의 경제가 아직 성숙 단계에 있습니다. 그러나 인텔의 TCO 비교 조사에 따르면, 랙당 전력 소비량이 100kW를 초과할 경우, 냉방 비용 절감과 공간 활용도 향상을 통해 5년 이내에 투자 회수가 가능해집니다. Midea 등 제조업체들은 2028년까지 단가를 최대 30% 인하하기 위해 대량 생산형 CDU 공장에 1억 3,800만 달러를 투자하고 있으며, 이를 통해 이러한 장벽을 완화해 나가고 있습니다.

부문별 분석

2025년, 중국의 GPU 액체 냉각 시장에서는 표준 42U 랙과의 호환성과 비교적 간편한 유지보수를 바탕으로 단일 아키텍처가 73.20%라는 가장 높은 시장 점유율을 차지했습니다. 델타의 4RU 및 6RU 인랙 CDU는 퀵 릴리스 호스를 Neptune 호환 레노버 서버에 연결하여, 시설의 배관 루프를 변경하지 않고도 H100 및 H200 GPU를 냉각합니다. 이 부문은 사업자가 캐비닛을 단계적으로 액체 냉각 방식으로 전환하는 개조 프로젝트의 대부분에서 여전히 주류를 이루고 있습니다. 반면, 메가와트급 AI 훈련실에서는 이미 2상 침지 방식이 선호되는 선택지로 자리 잡고 있습니다. Sugon의 C8000 V3.0 탱크는 랙당 900 kW의 성능을 달성하여 PUE를 1.04까지 낮추는 동시에, 더 고밀도인 네트워크 패브릭을 위한 바닥 면적을 확보하고 있습니다. Vera Rubin의 전력 엔벨로프는 장치당 1kW를 초과하므로, 700W를 초과하는 밀도 대역에서는 유체 비용이 높아지더라도 조달 방향은 2상 시스템 쪽으로 기울어질 것입니다. 2026년 하반기에 진행될 ODM 및 하이퍼스케일 기업들의 시범 프로젝트는 중국의 GPU 액체 냉각 시장 전체에서 신규 건설 프로젝트에서 콜드플레이트를 대체하여 액침 냉각이 보급되는 속도를 결정짓게 될 것입니다.

도입 동향에 따르면, 2026년에 가동을 시작한 중국의 신규 데이터센터 중 약 22%가 어떤 형태의 액체 냉각 방식을 도입했으며, 그중 이상 침지 방식이 차지하는 비율은 고작 4%에 불과했습니다. 이러한 차이는 도입에 대한 거부감이나 불소계 유체의 높은 비용에서 기인하지만, 하이퍼스케일러 각사는 유지보수 일정에서 콜드플레이트를 제외할 수 있다는 침지 방식의 장점을 높이 평가했습니다. 인텔과 알리바바 클라우드는 100kW 랙에서 PUE 1.09를 기록하며 단상 액침 냉각의 유효성을 입증했으며, 이는 콜드 플레이트 방식과 액침 냉각 방식의 경계를 모호하게 만들 수 있는 중간적인 접근 방식을 보여줍니다. GPU의 전력 소비가 증가함에 따라, 2상 시스템이 가장 빠른 성장세를 보일 것이며, 중국의 GPU 액체 냉각 시장의 향후 점유율에서 그 비중을 더욱 확대할 것으로 보입니다.

부품 수준의 냉각은 2025년 지출의 55.45%를 차지했습니다. 이는 주로 GPU 제조업체들이 콜드플레이트를 통합한 레퍼런스 설계를 출시하고 있기 때문입니다. 노드 단위의 업그레이드는 기업의 청구 처리를 간소화하고, 운영자가 미션 크리티컬한 랙만을 대상으로 할 수 있도록 해줍니다. Yinlun Co.와 같은 1급 자동차용 열교환기 제조업체는 마이크로채널 플레이트를 개선하여 로트 간 균일성을 98% 달성함으로써, 하이퍼스케일 기업들의 신뢰를 높이고 있습니다. 그러나 매니폴드와 인라인 CDU를 통합한 랙 레벨 시스템은 연평균 성장률(CAGR) 31.76%를 기록하며 성장하고 있으며, 하이퍼스케일 기업들이 150kW 이상의 캐비닛을 도입함에 따라 중국의 GPU 액체 냉각 시장 점유율을 확대되고 있습니다. XFusion의 FusionPoD는 핫 아일을 제거하여, 144개의 CPU와 GPU를 합쳐 pPUE 1.06을 달성하고 있습니다. 또한, H3C의 800G 액체 냉각식 스위치는 네트워크를 동일한 유체 루프로 통합하여 에어 갭을 해소합니다.

랙 솔루션에는 배관, 누수 감지, 모니터링 기능이 통합되어 있어 데이터 홀 층에서 엔지니어링에 소요되는 시간을 단축합니다. 대개 ISO 컨테이너로 출하되는 이 올인원 랙은 지방의 AI 허브에 위치한 미완공 건물 내부로 크레인을 이용해 반입할 수 있어, 컴퓨팅 시작까지 걸리는 시간을 단축할 수 있습니다. 베이징이나 상하이 도심에 위치한 코로케이션 시설을 개조하는 사업자들에게는 새로운 설비 루프를 설치하기 위해 콘크리트를 절단할 필요가 없기 때문에 모듈형 콜드 플레이트가 여전히 선호되고 있습니다. 따라서 두 수준이 공존하게 되겠지만, 2031년까지의 최대 수익 차이는 랙 부문에서 나타나며, 이는 중국의 GPU 액체 냉각 시장 규모를 확대하는 요인이 될 것입니다.

기타 혜택 :

- 엑셀 형식 시장 예측(ME) 시트

- 3개월간의 애널리스트 지원

자주 묻는 질문

목차

제1장 서론

제2장 조사 방법

제3장 주요 요약

제4장 시장 구도

제5장 시장 규모 및 성장 예측

제6장 경쟁 구도

제7장 시장 기회 및 향후 전망

KTHAccording to Mordor Intelligence, the china gPU liquid cooling market size was valued at USD 2.28 billion in 2025 and estimated to grow from USD 2.87 billion in 2026 to reach USD 11.23 billion by 2031, at a CAGR of 31.38% during the forecast period (2026-2031).

This report is Segmented by Cooling Type (Single-Phase Liquid Cooling, and Two-Phase Liquid Cooling), Cooling Level (Component-Level Cooling, and Server/Rack-Level Cooling), Deployment (Hyperscale/Cloud, Enterprise, Government and Research HPC, and Edge AI), GPU Power Density (Below 300W, 300W-700W, and Above 700W), and Geography. The Market Forecasts are Provided in Terms of Value (USD).

China GPU Liquid Cooling Market Trends and Insights

Surging Adoption of AI Training Workloads in Chinese Hyperscale Data Centers

Chinese hyperscalers are scaling clusters from tens to hundreds of petaflops, and liquid cooling keeps junction temperatures stable even when utilization exceeds 80%. Alibaba Cloud's USD 52.7 billion, three-year infrastructure plan places cold-plate racks at the center of next-generation language-model training, preventing fan energy from eroding overall PUE. Baidu is retrofitting legacy facilities after thermal loads quadrupled, while Tencent doubled AI capex to USD 5 billion for 2026, deploying immersion tanks that sustain 100-200 kW per rack. Sustained demand for sovereign AI models ensures continuous GPU utilization that only liquid cooling can support.

Rising GPU Power Densities Beyond 700 W Necessitating Liquid Cooling

NVIDIA's Vera Rubin family arrives in H2 2026 with liquid cooling as standard and board power at or above 1,000 W, eliminating air systems for flagship AI training racks. Delta Electronics already offers 1.5 MW coolant distribution units sized for fifteen 100 kW NVL72 racks, while Huawei's liquid-cooled 800 G switches prevent thermal throttling in fabric elements. Economics also favor liquid cooling-higher density allows smaller footprints and lowers HVAC overhead.

High Upfront CAPEX Compared With Air Cooling Retrofits

Cold-plate assemblies, quick connectors, and CDUs can lift initial budgets 40-60%, discouraging operators below the 50 kW per rack threshold. Component costs are concentrated in metallurgy and precision machining, areas where scale economies are still maturing. Intel's comparative TCO study, however, shows breakeven in under five years once racks top 100 kW, thanks to lower HVAC bills and higher space utilization. Manufacturers such as Midea are investing USD 138 million in high-volume CDU plants to reduce unit pricing by up to 30% before 2028, easing this barrier.

Other drivers and restraints analyzed in the detailed report include:

- Rapid Build-Out of Provincial AI Computing Clusters Aligned With "East Data West Compute

- Export Restrictions on Advanced GPUs Accelerating Domestic Liquid-Cooled Accelerator R&D

- Supply Chain Dependency on Imported Dielectric Fluids Amid Geopolitical Tensions

For complete list of drivers and restraints, kindly check the Table Of Contents.

Segment Analysis

Single-phase architectures captured the largest China GPU liquid cooling market share at 73.20% in 2025, buoyed by compatibility with standard 42U racks and relatively simple maintenance. Delta's 4 RU and 6 RU in-rack CDUs connect quick-release hoses to Neptune-enabled Lenovo servers that cool H100 and H200 GPUs without plumbing changes to facility loops. This segment still wins most retrofit projects where operators migrate cabinets gradually to liquid. In contrast, two-phase immersion is already the preferred choice for megawatt-class AI training halls: Sugon's C8000 V3.0 tanks achieve 900 kW per rack, shaving PUE to 1.04 and freeing floor space for denser network fabrics. Because power envelopes for Vera Rubin exceed 1 kW per device, the above-700 W density band will tilt procurement toward two-phase systems despite their higher fluid budgets. ODM and hyperscale pilots in H2 2026 will determine the pace at which immersion replaces cold plates for greenfield builds across the China GPU liquid cooling market.

Adoption patterns indicate that roughly 22% of new Chinese data centers commissioned in 2026 integrated some form of liquid cooling, of which two-phase immersion accounted for only 4%. The gap arises from training inertia and the higher cost of fluorinated fluids, yet hyperscalers value immersion's ability to eliminate cold plates from maintenance schedules. Intel and Alibaba Cloud validated single-phase immersion to 100 kW racks at 1.09 PUE, demonstrating a mid-step that could blur boundaries between cold-plate and immersion approaches. As GPU wattage climbs, two-phase systems will absorb the fastest growth slice, reinforcing their role in the future mix of the China GPU liquid cooling market.

Component-level cooling held 55.45% of 2025 spending, mainly because GPU vendors ship reference designs with integrated cold plates. Upgrades on a node-by-node basis simplify billing for enterprises and allow operators to target only mission-critical racks. Tier-1 automotive heat-exchange companies like Yinlun Co. have adapted microchannel plates achieving 98% batch-to-batch consistency, boosting trust among hyperscale buyers. However, rack-level systems, featuring integrated manifolds and in-line CDUs, are growing at a 31.76% CAGR and gaining share of the China GPU liquid cooling market size as hyperscalers chase 150 kW-plus cabinets. XFusion's FusionPoD eliminates hot aisles, delivering pPUE of 1.06 across 144 CPUs plus GPUs, and H3C's 800 G liquid-cooled switch ties the network into the same fluid loop, removing air gaps.

Rack solutions bundle plumbing, leak detection, and monitoring, which lowers engineering time on the data-hall floor. These all-inclusive racks, often shipped in ISO containers, can be craned into bare shells at provincial AI hubs, shortening time-to-compute. For operators retrofitting downtown Beijing or Shanghai colocation, component cold plates remain favored because they avoid cutting concrete for new facility loops. Therefore, both levels will coexist; yet the strongest revenue delta to 2031 sits with racks, adding scale to the China GPU liquid cooling market size.

List of Companies Covered in this Report:

- Inspur Group

- Lenovo Group Limited

- Huawei Technologies Co., Ltd.

- Sugon Information Industry Co., Ltd.

- H3C Technologies Co., Ltd.

- Tencent Holdings Ltd.

- Alibaba Group Holding Limited

- Baidu, Inc.

- Giga Computing Technology Co., Ltd.

- ASUSTeK Computer Inc.

- Super Micro Computer, Inc.

- NVIDIA Corporation

- CoolIT Systems Inc.

- Asetek A/S

- LiquidStack Holding Limited

- Submer Technologies SL

- Envicool Technology Co., Ltd.

- Delta Electronics, Inc.

- Phytium Technology Co., Ltd.

- China Mobile Limited

Additional Benefits:

- The market estimate (ME) sheet in Excel format

- 3 months of analyst support

TABLE OF CONTENTS

1 INTRODUCTION

- 1.1 Study Assumptions and Market Definition

- 1.2 Scope of the Study

2 RESEARCH METHODOLOGY

3 EXECUTIVE SUMMARY

4 MARKET LANDSCAPE

- 4.1 Market Overview

- 4.2 Market Drivers

- 4.2.1 Surging Adoption of AI Training Workloads in Chinese Hyperscale Data Centers

- 4.2.2 Government Incentives for Energy Efficient Data Center Cooling

- 4.2.3 Rising GPU Power Densities Beyond 700W Necessitating Liquid Cooling

- 4.2.4 Rapid Build-Out of Provincial AI Computing Clusters Aligned With "East Data West Compute" Program

- 4.2.5 Growing Preference for Immersion-Ready GPU Reference Designs by ODM Server Makers

- 4.2.6 Export Restrictions on Advanced GPUs Accelerating Domestic Liquid-Cooled Accelerator R&D

- 4.3 Market Restraints

- 4.3.1 High Upfront CAPEX Compared With Air Cooling Retrofits

- 4.3.2 Limited Standardization Across Component-Level Cold Plate Solutions

- 4.3.3 Stringent Cybersecurity Approval Processes for Liquid-Cooled Cloud Deployments in Government Workloads

- 4.3.4 Supply Chain Dependency on Imported Dielectric Fluids Amid Geopolitical Tensions

- 4.4 Industry Value Chain Analysis

- 4.5 Regulatory Landscape

- 4.6 Technological Outlook

- 4.7 Porter's Five Forces Analysis

- 4.7.1 Competitive Rivalry

- 4.7.2 Threat of New Entrants

- 4.7.3 Bargaining Power of Suppliers

- 4.7.4 Bargaining Power of Buyers

- 4.7.5 Threat of Substitutes

- 4.8 Impact of Macroeconomic Factors on the Market

5 MARKET SIZE AND GROWTH FORECASTS (VALUE)

- 5.1 By Cooling Type

- 5.1.1 Single-Phase Liquid Cooling

- 5.1.2 Two-Phase Liquid Cooling

- 5.2 By Cooling Level

- 5.2.1 Component-Level Cooling

- 5.2.2 Server / Rack-Level Cooling

- 5.3 By Deployment

- 5.3.1 Hyperscale / Cloud

- 5.3.2 Enterprise

- 5.3.3 Government and Research (HPC)

- 5.3.4 Edge AI

- 5.4 By GPU Power Density

- 5.4.1 Below 300W

- 5.4.2 300W - 700W

- 5.4.3 Above 700W

6 COMPETITIVE LANDSCAPE

- 6.1 Market Concentration

- 6.2 Strategic Moves

- 6.3 Market Share Analysis

- 6.4 Company Profiles (includes Global Level Overview, Market Level Overview, Core Segments, Financials as available, Strategic Information, Market Rank/Share, Products and Services, Recent Developments)

- 6.4.1 Inspur Group

- 6.4.2 Lenovo Group Limited

- 6.4.3 Huawei Technologies Co., Ltd.

- 6.4.4 Sugon Information Industry Co., Ltd.

- 6.4.5 H3C Technologies Co., Ltd.

- 6.4.6 Tencent Holdings Ltd.

- 6.4.7 Alibaba Group Holding Limited

- 6.4.8 Baidu, Inc.

- 6.4.9 Giga Computing Technology Co., Ltd.

- 6.4.10 ASUSTeK Computer Inc.

- 6.4.11 Super Micro Computer, Inc.

- 6.4.12 NVIDIA Corporation

- 6.4.13 CoolIT Systems Inc.

- 6.4.14 Asetek A/S

- 6.4.15 LiquidStack Holding Limited

- 6.4.16 Submer Technologies SL

- 6.4.17 Envicool Technology Co., Ltd.

- 6.4.18 Delta Electronics, Inc.

- 6.4.19 Phytium Technology Co., Ltd.

- 6.4.20 China Mobile Limited

7 MARKET OPPORTUNITIES AND FUTURE OUTLOOK

- 7.1 Whitespace and Unmet Need Assessment